Amino Resin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

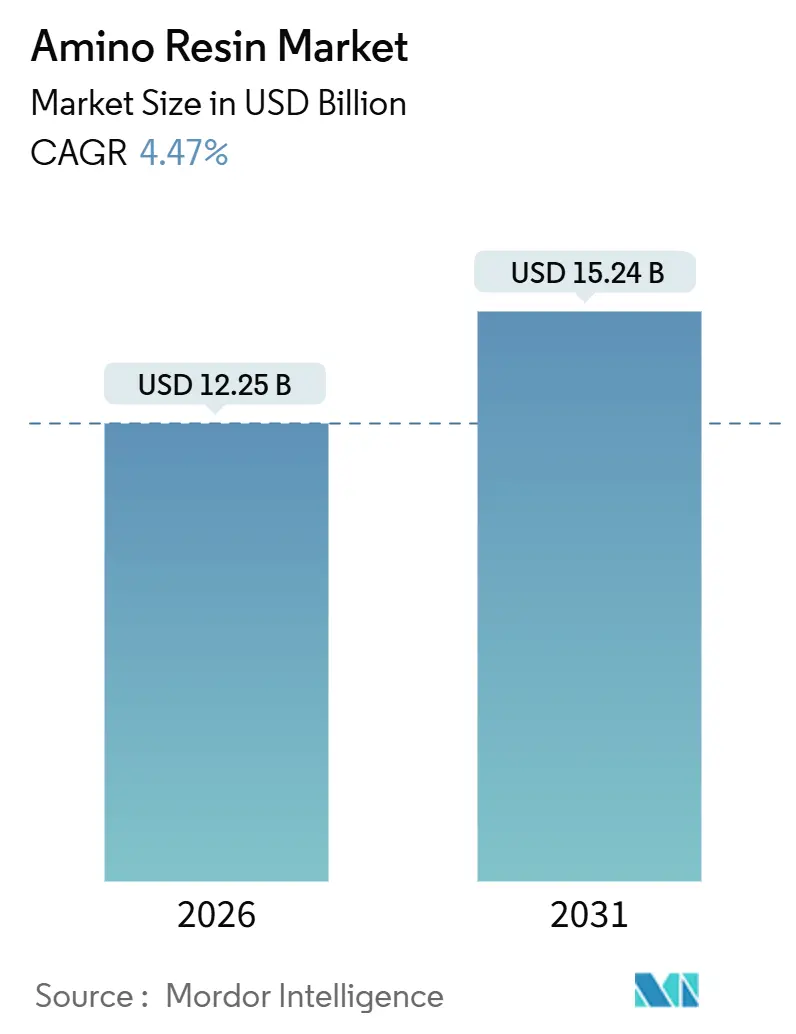

| Market Size (2026) | USD 12.25 Billion |

| Market Size (2031) | USD 15.24 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Amino Resin Market Analysis by Mordor Intelligence

The Amino Resin Market size is estimated at USD 12.25 billion in 2026, and is expected to reach USD 15.24 billion by 2031, at a CAGR of 4.47% during the forecast period (2026-2031). Demand is underpinned by the construction‐led surge in wood-panel production, rapid electrification in automotive coatings, and escalating regulatory pressure to reduce formaldehyde emissions. Urea-formaldehyde (UF) retains cost leadership, yet melamine-formaldehyde (MF) and melamine-urea-formaldehyde (MUF) grades are outgrowing UF because they meet structural-grade moisture resistance with cure windows of 120–150 °C while aligning with low-emission mandates. Feedstock price swings and tariffs on methanol, urea, and melamine continue to squeeze converter margins, intensifying the pivot toward captive resin production and low-carbon feedstocks. The amino resins market is therefore navigating a dual transformation—toward higher-performing chemistries and toward bio-based or formaldehyde-free alternatives—while remaining anchored in its largest application, wood-panel adhesives.

Key Report Takeaways

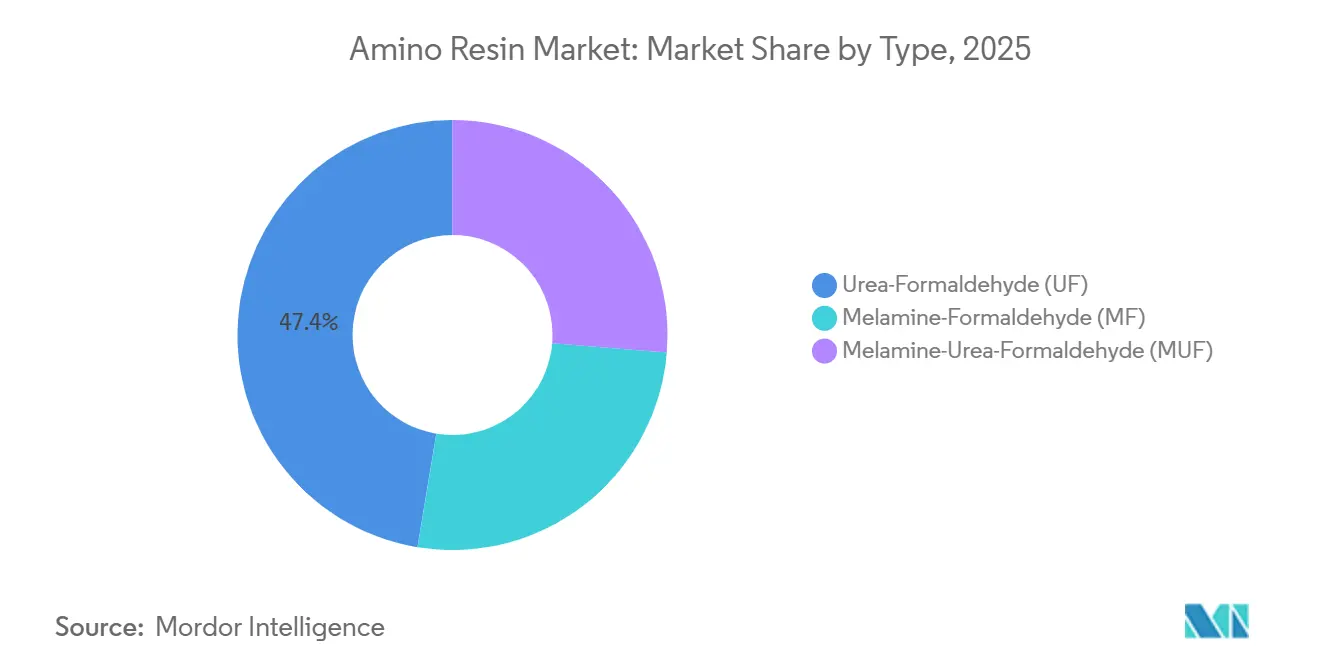

- By type, urea-formaldehyde held 47.41% of the amino resins market share in 2025, whereas melamine-formaldehyde is forecast to grow at a 5.22% CAGR through 2031.

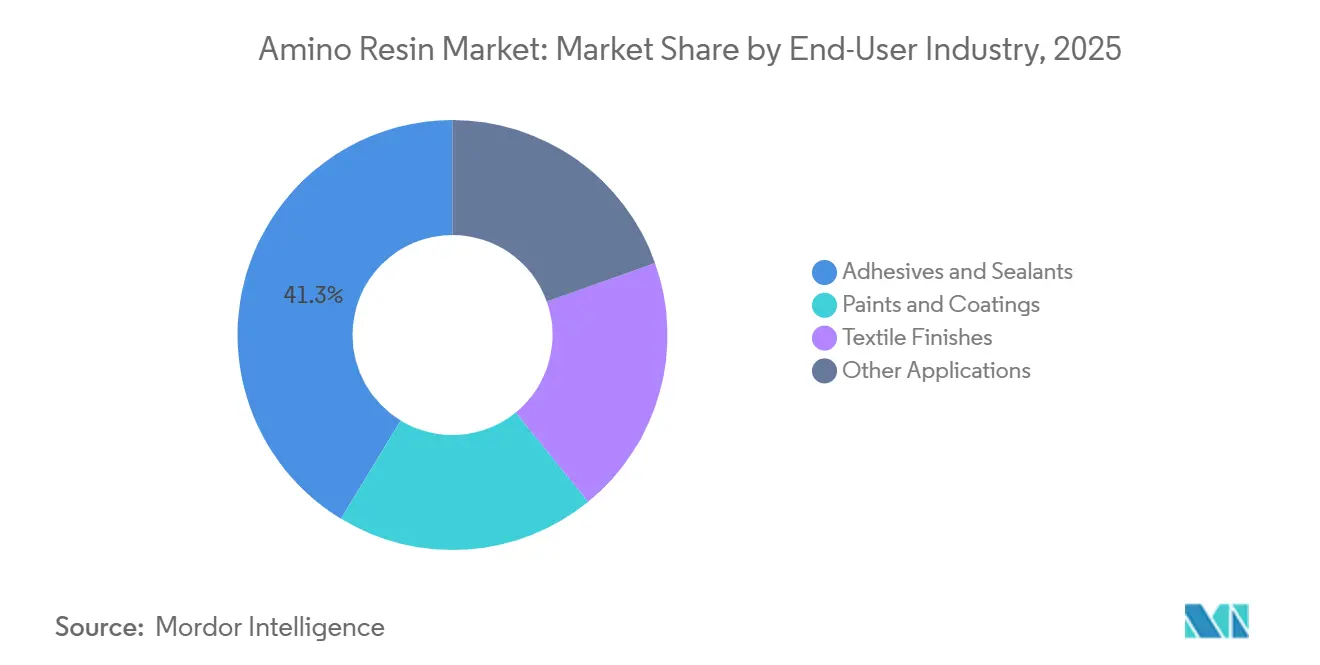

- By end-user industry, adhesives and sealants commanded 41.33% revenue in 2025, while paints and coatings are advancing at a 5.18% CAGR to 2031.

- By geography, Asia-Pacific captured 52.51% revenue in 2025; the Middle-East and Africa region is expanding at a 5.94% CAGR from 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Amino Resin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from paints and coatings | +0.8% | Global, led by Asia-Pacific and North America | Medium term (2–4 years) |

| Wood-panel adhesives boom in construction and furniture | +1.2% | Asia-Pacific, Europe, North America | Long term (≥4 years) |

| Growth of automotive OEM coatings | +0.6% | North America, Europe, China | Medium term (2–4 years) |

| Expansion of engineered flooring and laminates | +0.5% | Asia-Pacific, Europe | Long term (≥4 years) |

| Formaldehyde-free glyoxal-based resin adoption | +0.4% | Europe, North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Paints and Coatings

Melamine crosslinkers are replacing isocyanates in automotive clearcoats because they cure at lower oven temperatures, cut energy use, and avoid hazardous airborne isocyanate particles. Brands such as CYMEL and Setamine enable formulators to hit strict VOC caps in California’s SCAQMD and the EU Industrial Emissions Directive, while meeting mar-resistance and chemical-resistance benchmarks in battery-module coatings. Although vehicle production contractions in 2024 and 2025 trimmed short-term resin off-take, the pivot toward water-borne and powder platforms is generating a durable growth runway that favors highly methylated MF grades for rapid crosslink density at 140 °C[1]Allnex, “Amino Resins – Crosslinkers,” allnex.com.

Wood-Panel Adhesives Boom in Construction and Furniture

Particleboard and MDF together consume a major portion of UF output, making adhesive demand tightly correlated with new furniture and housing fit-outs. India’s MDF capacity climbed in 2025 and is tracking double-digit volume growth even as surplus capacity delays price recovery. Europe’s rail-linked resin shipments, such as Kronospan’s block-train route from Lampertswalde to Wals-Siezenheim, underline the cost and carbon savings that accompany supply-chain redesign. Meanwhile, Chinese engineered-wood exporters are channeling panels into Southeast Asia and Africa, effectively redistributing adhesive consumption across borders.

Growth of Automotive OEM Coatings

Global light-vehicle builds rebounded in 2024, keeping amino resin usage in exterior and interior topcoats broadly aligned with vehicle volumes. The rise of aluminum body structures shortens bake cycles, so OEMs prefer MF crosslinkers that hit cure targets within 20 minutes at 140 °C. Battery enclosures demand flame-retardant, dielectric coatings specified under ISO 12944, accelerating the adoption of isobutylated melamines that deliver low VOC and low free-formaldehyde content.

Expansion of Engineered Flooring and Laminates

In 2024-2025, shipments of laminate flooring and decorative overlays surged, driven by housing renovations in North America and Europe. Meanwhile, manufacturers in the Asia-Pacific region exported substantial volumes of finished panels. These overlays, reliant on MF-impregnated papers, undergo pressing at high temperatures and boast superior abrasion ratings, as per EN 13329 standards. However, a looming challenge arises: EU Regulation 2023/1464, set to take effect in August 2026, mandates a formaldehyde limit. This regulation pushes resin suppliers to either provide ultra-low-emission MF grades or incorporate scavenger additives to preserve the clarity of their overlays.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hazardous air pollutants and emission regulations | -0.6% | North America, Europe | Short term (≤2 years) |

| Growing preference for bio-based resin systems | -0.3% | Europe, North America | Medium term (2–4 years) |

| Feedstock (urea/methanol) price and tariff volatility | -0.4% | Global, acute in Europe and Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Hazardous Air Pollutants and Emission Regulations

In July 2025, the European General Court upheld the designation of melamine as a Substance of Very High Concern (SVHC), heightening regulatory uncertainties and hastening the transition to non-formaldehyde chemistries. While the EPA's TSCA Title VI caps formaldehyde emissions for particleboard and MDF, EU Regulation 2023/1464 is set to halve permissible emissions starting August 2026. These compliance mandates are pushing formulators to either reduce free-formaldehyde in UF blends or switch to glyoxal systems, incurring additional costs for testing and certification[2]U.S. Environmental Protection Agency, “Formaldehyde Emission Standards for Composite Wood Products,” epa.gov.

Growing Preference for Bio-Based Resin Systems

Viobond's lignin plant in Riga is set to replace a significant portion of phenol in plywood adhesives by 2027, marking a significant leap from pilot to industrial status for protein-based and lignin-phenolic binders. Meanwhile, GreenBond's protein resins have already made their commercial debut in European particleboard. While these bio-based resins may not yet match UF in wet-strength retention, converters are capitalizing on them to command green premiums and bolster their negotiation stance, consequently squeezing margins for conventional resins. In response, industry incumbents are introducing biomass-balanced ammonia and urea inputs, achieving carbon footprint reductions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Melamine Outpaces Urea on Moisture Resistance

Urea-formaldehyde retained 47.41% of the amino resins market share in 2025. Its advantage is a lower cost per solids content that's lower than melamine formaldehyde (MF) and the ability to cure rapidly on high-speed particleboard lines. However, UF's bond integrity falters when panels hit high temperatures or encounter elevated ambient humidity. This vulnerability has led converters to favor MF or melamine-urea-formaldehyde (MUF) for applications like exterior-grade panels, oriented strand board (OSB), and structural plywood. As a result, Melamine-Formaldehyde (MF) is projected to grow at a 5.22% CAGR through 2031. Furthermore, blends with melamine achieve ANSI Type I water-resistance at a fraction of the MF cost. Hexion’s EcoBind line, on the other hand, meets CARB Phase 2 and EPA standards without compromising on press efficiency.

While the amino resins market size for UF remains substantial, MF's enhanced durability is increasingly being favored for specifications in transport, marine applications, and exterior cladding. Highly methylated MF resins are gaining traction in industrial coatings and wrinkle-resistant textile finishes due to their solubility at high solids and moderate baking crosslinking. Hybrid melamine-urea-phenol-formaldehyde systems are eyeing European OSB 3 ratings, combining MF’s moisture resistance with the strength of phenolics. The future trajectory of each resin now hinges on regional formaldehyde regulations and the market introduction of glyoxal-based MF, which promises to match UF's rapid curing speed.

By End-User Industry: Coatings Accelerate on Automotive Electrification

Adhesives and sealants consumed 41.33% of global volume in 2025, primarily driven by their use in bonding particleboard, MDF, and plywood. However, as automotive electrification accelerates, paints and coatings will expand at a 5.18% CAGR through 2031, expanding steadily through 2031. Melamine crosslinkers play a pivotal role in EV battery-module coatings, underbody seals, and clearcoats, ensuring they maintain adhesion even when cycling between −40 °C and 120 °C. Resins like CYMEL, Setamine, and Luwipal, which cure at lower temperatures, can reduce oven energy consumption, a significant advantage in OEM decarbonization efforts.

The market for amino resins in coatings has shown consistent growth, with projections indicating further expansion by 2031. Dimethyloldihydroxyethyleneurea, known for imparting high wrinkle resistance in cotton blends at specific cure temperatures, anchors a stable demand in textile finishes. While other applications, such as tire adhesion promoters and paper wet-strength agents, offer diverse margins, a decline in graphic paper dampens overall growth. The real game-changer is the surging demand for battery packs: with each EV requiring melamine resin, this segment could potentially unlock a significant revenue stream by 2030.

Geography Analysis

Asia-Pacific commanded 52.51% of global revenue in 2025, driven by China's methanol output and the region's capacity for particleboard and MDF. India's MDF capacity saw notable growth. Additionally, anti-dumping duties on subpar imports have pushed mills to adopt CARB-equivalent UF and MUF, increasing resin intensity per panel. Despite a decline in Chinese housing starts in 2024, engineered wood exports to Southeast Asia and Africa shifted adhesive demand. In mature markets like Japan, Korea, and Australia, compliance is key, with lifecycle carbon data increasingly influencing resin choices. BASF's expansion in Nanjing, set for October 2025, will add specialty amine capacity, signaling strong confidence in Asia-Pacific's consumption.

North America and Europe, together accounting for a substantial portion of demand, grapple with cost pressures from emission caps. Under EPA TSCA Title VI, particleboard producers are pivoting to ultra-low-emission UF or are turning to MUF and phenolic substitutes. However, converters are resisting price hikes, putting pressure on merchant resin margins. Arclin's West Virginia expansion, focusing on methylamine and dimethylformamide, bolsters feedstock security ahead of the EPA's 2026 enforcement review. Meanwhile, Europe is gearing up for stricter emission ceilings and is investing in glyoxal and lignin systems due to melamine's SVHC status. Notably, Kronospan's complete acquisition of Nordalim and Bakelite Synthetics' takeover of GreenBond highlight downstream players' strategies to build captive or unique resin positions, aiming to navigate regulatory challenges.

The Middle-East and Africa will log the fastest regional CAGR of 5.94% to 2031, fueled by megaprojects in Saudi Arabia and the UAE, alongside budding furniture clusters in South Africa and Kenya. Resin producers from Europe and Asia are eyeing joint ventures for local MUF blending, a move to counter shipping costs and ensure swift lead times. While Brazil's economic fluctuations temper South America's growth, the country's eucalyptus-based MDF exports carve out a niche as a diversification hub for North American buyers. Looking ahead, Africa's tariff regimes and industrial policies will play a pivotal role in determining the trajectory of local panel manufacturing, potentially birthing a new demand node for the amino resins market.

Regulatory Landscape

Amino resins are facing tighter controls on both process emissions and downstream indoor-air emissions. In the United States, manufacturing sites are governed under the National Emission Standards for Hazardous Air Pollutants for the Manufacture of Amino/Phenolic Resins (40 CFR Part 63, Subpart OOO), while EPA TSCA Title VI caps formaldehyde emissions from composite wood products, which in turn shapes UF, MUF, and MF selection across particleboard and MDF supply chains.

In Europe, REACH (EC) No 1907/2006 drives registration and compliance obligations for substances placed on the market above 1 tonne per year, reinforcing documentation and stewardship expectations across amino resin and feedstock portfolios. For application compliance and quality control, producers and users often rely on standardized free-formaldehyde test methods such as ASTM D1979-97 and EN ISO 11402:2005, and, for paper and paperboard uses, applicable provisions under 21 CFR Part 176 for indirect food additives further define permitted chemistries.

Value Chain Analysis

The amino resin value chain starts with upstream feedstocks, primarily urea and melamine (amino compounds), and formaldehyde (an aldehyde), with methanol, butanol, or ethanol used for etherification and property tuning. Resin manufacture typically runs in two main reaction stages, hydroxymethylation followed by condensation, carried out in controlled stirred-kettle operations with temperature and pH management to meet target viscosity, free-formaldehyde levels, and cure behavior; this makes consistent availability of formaldehyde and amino feedstocks a key cost and reliability lever.

Producers distribute resins as liquid concentrates or tailored blends to formulators and converters serving wood-panel adhesives, laminates/impregnating resins, and coatings crosslinkers, where performance and certification testing are embedded in qualification cycles. Margin control and service differentiation increasingly depend on vertical integration or secured sourcing of methanol, urea, melamine, and formaldehyde, along with downstream technical support for emissions-compliant panel lines and low-VOC coating systems. Industry bodies such as the Plastics Industry Association also act as coordination points on sustainability and regulatory topics relevant to resin producers.

Competitive Landscape

The amino resin market is moderately fragmented. Innovation centers on low-carbon and bio-based chemistries. Hexion’s alliance with Bloom Biorenewables deploys aldehyde-assisted fractionation to yield white lignin for fully bio-based panels by 2026. The competitive edge is shifting from price per solids to lifecycle data, traceable feedstocks, and the ability to dual-source between conventional and green chemistries. Producers offering integrated formaldehyde, melamine, and methanol supply—or credible bio-based alternatives—are best placed to capture the next growth phase.

Amino Resin Industry Leaders

BASF SE

Hexion

Prefere Resins Holding GmbH

Georgia-Pacific Chemicals

Dynea AS

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A gap is forming around certified low-carbon and low-emission feedstocks that allow MF and MUF systems to meet tightening formaldehyde limits without giving up cure speed and moisture resistance in wood panels and overlays. The April 2026 collaboration between OCI and Prefere Resins to introduce MelaminebyOCI Novo (ISCC PLUS certified, produced using biogas) illustrates how certified melamine inputs are being positioned to help resin suppliers and panel manufacturers document lower product carbon footprints while maintaining established MF/MUF performance in laminates and engineered wood.

Supply security for melamine also presents an opportunity where downstream resin and panel capacity is expanding faster than local feedstock availability. In April 2026, Indonesia broke ground on its first domestic melamine plant in the Gresik Special Economic Zone with a stated USD 600 million investment plan and an integrated ammonia-urea-melamine chain (120,000 tpy melamine design capacity), creating a new regional source intended to reduce import dependence and support Southeast Asian wood-panel, laminate, and coatings value chains.

Recent Industry Developments

- July 2026: BASF expanded its certified biomass-balanced (BMB) additives portfolio under REDcert2, adding products such as Dispex AA 4145 MB, Rheovis PU 1333 MB, and Rheovis HS 1169 MB. While not an amino resin line item, this expansion improves access to certified, lower-footprint formulation inputs that coatings and engineered-wood systems increasingly use alongside amino resin crosslinkers and binders to meet customer sustainability requirements.

- December 2025: Hexion completed the sale of its U.S. Gulf Coast formalin business to Ancala, which created Valentra to operate the acquired sites. The divestment reshapes access to a key amino resin precursor (formaldehyde) and indicates a portfolio shift toward specialty and technology-driven resin systems rather than base chemical integration.

- May 2024: BASF finalized the divestiture of its Ludwigshafen melamine unit (51,000 tpy). This directly affected European melamine availability, tightening the feedstock backdrop for melamine-formaldehyde and MUF production and increasing the importance of diversified sourcing and integration strategies for resin producers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the amino resin market covers the revenue generated from amino resin materials sold for industrial use, mainly urea-formaldehyde (UF), melamine-formaldehyde (MF), and melamine-urea-formaldehyde (MUF), across major end uses such as wood adhesives, coatings, and textile finishing, across regions.

Scope exclusions: It excludes downstream finished goods value (such as furniture or panels) and counts only the resin material value at the point of sale.

Segmentation Overview

- By Type

- Urea-Formaldehyde (UF)

- Melamine-Formaldehyde (MF)

- Melamine-Urea-Formaldehyde (MUF)

- By End-User Industry

- Paints and Coatings

- Textile Finishes

- Adhesives and Sealants

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean view of where amino resins are consumed and how demand moves with construction activity and wood-panel output. We used public sources such as national statistical agencies for construction indicators, UN Comtrade trade statistics for resin-related flows, the USGS for chemical and industrial materials context, and customs and standards agencies for formaldehyde emission rules and test methods.

To anchor the market in business activity, company annual reports, 10-K style filings, investor presentations, and association publications were reviewed for capacity notes, product positioning, and regional demand commentary. A paid subscription for company financials and intelligence was used selectively to map plant footprints and compare segment revenue mix, and a patent database was checked to gauge where low-emission formulations are being developed. These examples are not exhaustive, and many other public sources were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary discussions were completed with participants across the value chain, including resin producers, formulators, distributors, wood panel and laminate manufacturers, and coatings and textile finish users. We used these conversations to validate typical application splits, regional pricing direction, and how formaldehyde-emission regulation affects shifts between UF, MF, and MUF, then re-checked any outliers with follow-up outreach.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 32% |

| Smaller Players: 15% | Managers: 48% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach, where construction activity, engineered wood and panel production direction, and resin intensity assumptions were used to reconstruct the addressable demand pool by region, then converted to value using region-specific pricing. To keep the totals realistic, the model was corroborated with selective bottom-up approximations, such as sampled supplier revenue splits, channel checks on typical price bands, and volume sanity checks against known end-use activity.

A few practical inputs were treated as key knobs in the model, because they move the market more than small parameter tweaks. These included regional MDF/particleboard and laminate output trends, housing starts and renovation indicators, formaldehyde emission regulation tightening and substitution behavior, the split between UF, MF, and MUF by application, and observed pricing movement tied to feedstock volatility. Where direct observations were thin, gaps were handled by using proxy indicators (like wood-panel production growth) and then adjusting the implied resin share based on expert feedback.

Forecasts were produced using scenario analysis with a light multivariate view of the key drivers, since the market can shift with regulation timing and construction cycles. Assumptions for growth and pricing were stress-tested using interview insights, and then the final series was smoothed to avoid unrealistic step-changes unless a specific event supported it.

Data Validation & Update Cycle

Outputs were checked through multiple passes, starting with basic consistency tests across regions, types, and end-use totals, then moving to variance checks against independent signals such as construction direction, wood-panel output commentary, and trade movement. When a country or segment looked off relative to these signals, we revisited input assumptions and, where needed, re-contacted industry participants to confirm what changed.

Before sign-off, another analyst reviews the model logic and the key assumptions so calculation errors and double counting are avoided. The report is refreshed annually, and interim updates are triggered when material events occur, such as major regulation changes, supply disruptions, or sharp pricing swings. Right before delivery, a final data pass is done so clients receive the most current view available.

Mordor Intelligence's Amino Resin Market Size Versus Other Published Estimates

Published market values for amino resins can vary, even when different studies target the same industry, because scope choices and timing assumptions are not identical. Differences usually come from what is counted in the market (resin value only versus extended downstream value), the base year used, and how pricing is converted across regions.

The benchmark table shows a tighter 2026 value than some other figures, and in Mordor Intelligence's model the scope is kept at amino resin material revenue (UF, MF, and MUF) rather than folding in finished wood products or broader formaldehyde-based resin families that can inflate totals. On top of that, the spread can also come from faster or slower assumed pricing progression, the treatment of compliance-led substitution toward low-emission grades, and whether a study is refreshed after major construction cycle swings or regulatory announcements.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.25 B (2026) | |

| Global Consultancy A | USD 15.48 B (2026) | Uses a broader application roll-up that appears to include more downstream value capture in wood panels and laminates, and it also assumes a higher average selling price level in 2026 across regions. |

| Industry Publisher B | USD 10.86 B (2025) | Anchors the series on a 2025 base year and can understate 2026 if construction-linked demand rebound and price normalization are not fully carried into the next-year step. |

Taken together, the range is mostly explained by scope boundaries, year selection, and the way price and substitution effects are carried through the model. Our approach stays traceable because the total is built from clear demand drivers and cross-checked with real end-use signals, which makes the number easier to reproduce and update when new information appears.

Key Questions Answered in the Report

What is the forecast value of the amino resins market by 2031?

The market is projected to reach USD 15.24 billion by 2031, reflecting a 4.47% CAGR during 2026-2031, from USD 12.25 billion in 2026.

Which resin type is expanding fastest?

Melamine-formaldehyde is growing at a 5.22% CAGR because it meets structural-grade moisture resistance while complying with tighter emission rules.

Which region leads demand for amino resins?

Asia-Pacific accounted for 52.51% of 2025 revenue, driven by China’s methanol capacity and expanding wood-panel production.

Why are paints and coatings gaining share?

Automotive electrification and low-temperature curing requirements push OEMs to specify melamine crosslinkers, driving a 5.18% CAGR in coatings demand.

How are regulations shaping product development?

EPA TSCA Title VI and EU Regulation 2023/1464 force suppliers to cut free-formaldehyde levels or deploy glyoxal- and lignin-based alternatives, adding compliance costs but spurring innovation.

Page last updated on: