Acrylic Resin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

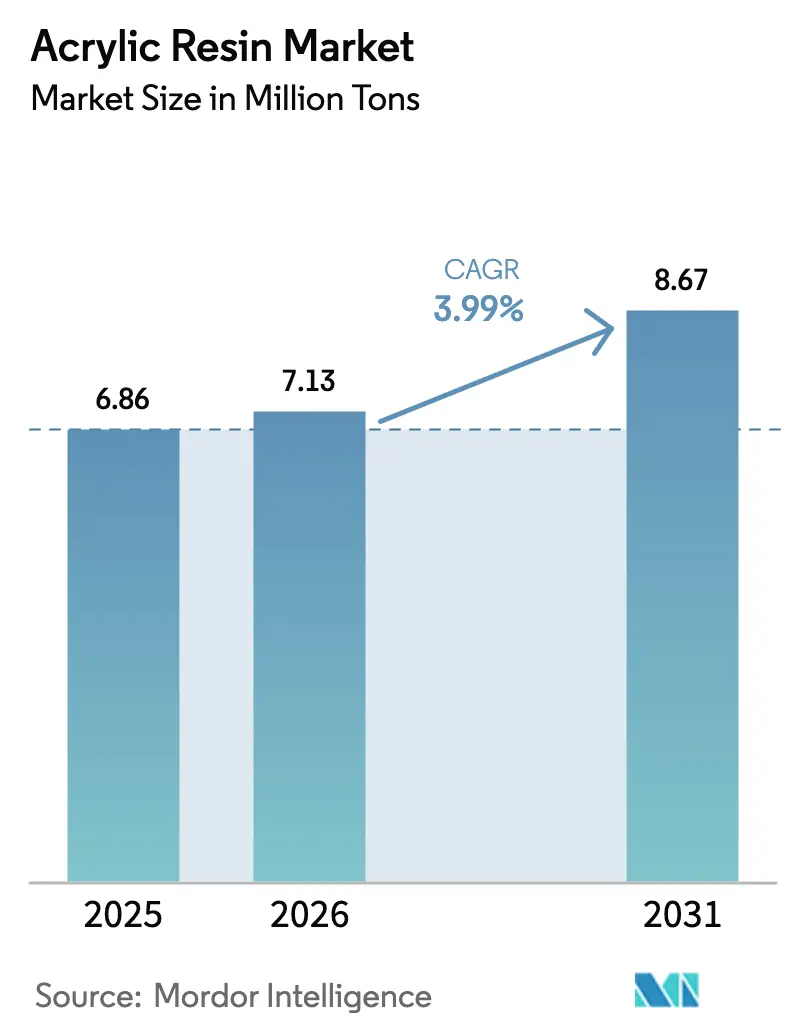

| Market Volume (2026) | 7.13 Million tons |

| Market Volume (2031) | 8.67 Million tons |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acrylic Resin Market Analysis by Mordor Intelligence

The Acrylic Resin Market size is expected to grow from 6.86 million tons in 2025 to 7.13 million tons in 2026 and is forecast to reach 8.67 million tons by 2031 at 3.99% CAGR over 2026-2031. This steady expansion reflects the material’s entrenched role in construction, automotive, and diversified industrial settings where performance requirements increasingly favor acrylic formulations over traditional resins. Momentum is reinforced by tightening low-VOC regulations that spur adoption of waterborne systems, while 3D-printing photopolymer demand adds a premium layer of growth. Supply-side responses include backward integration into feedstocks and a pivot to bio-based ethyl acrylate to hedge raw-material volatility. Competitive activity is intensifying as producers pursue capacity additions, strategic acquisitions, and circular-economy initiatives to secure long-term positioning.

Key Report Takeaways

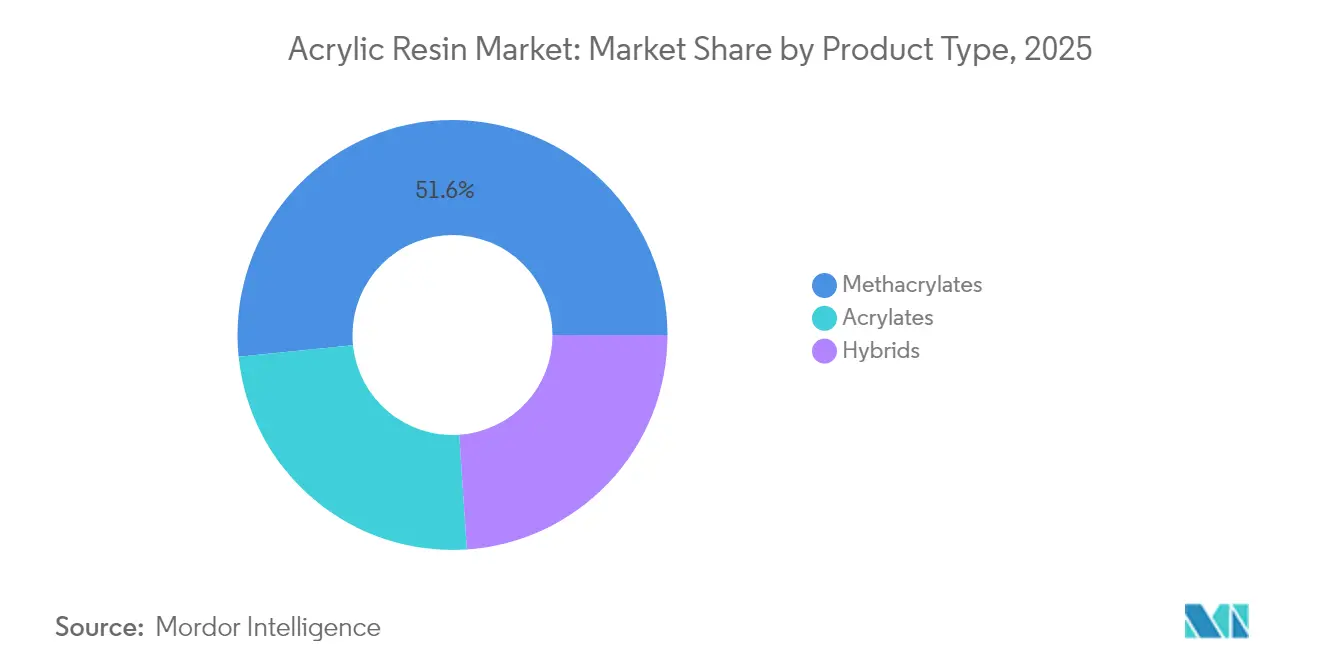

- By product type, methacrylates led with 51.62% of acrylic resin market share in 2025; acrylates are forecast to expand at a 5.18% CAGR through 2031.

- By application, paints and coatings commanded a 46.02% share of the acrylic resin market size in 2025, while adhesives and sealants are projected to grow at a 5.27% CAGR through 2031.

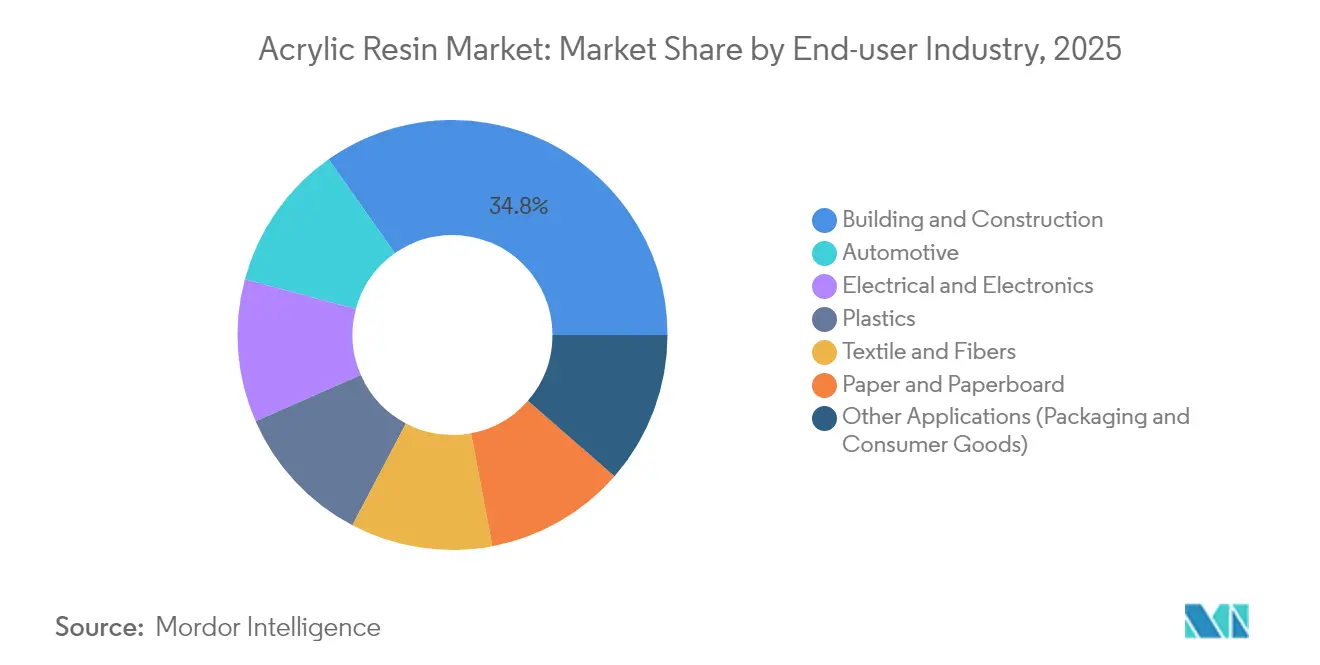

- By end-user industry, building and construction captured 34.78% of demand in 2025; automotive applications are advancing at a 5.47% CAGR to 2031.

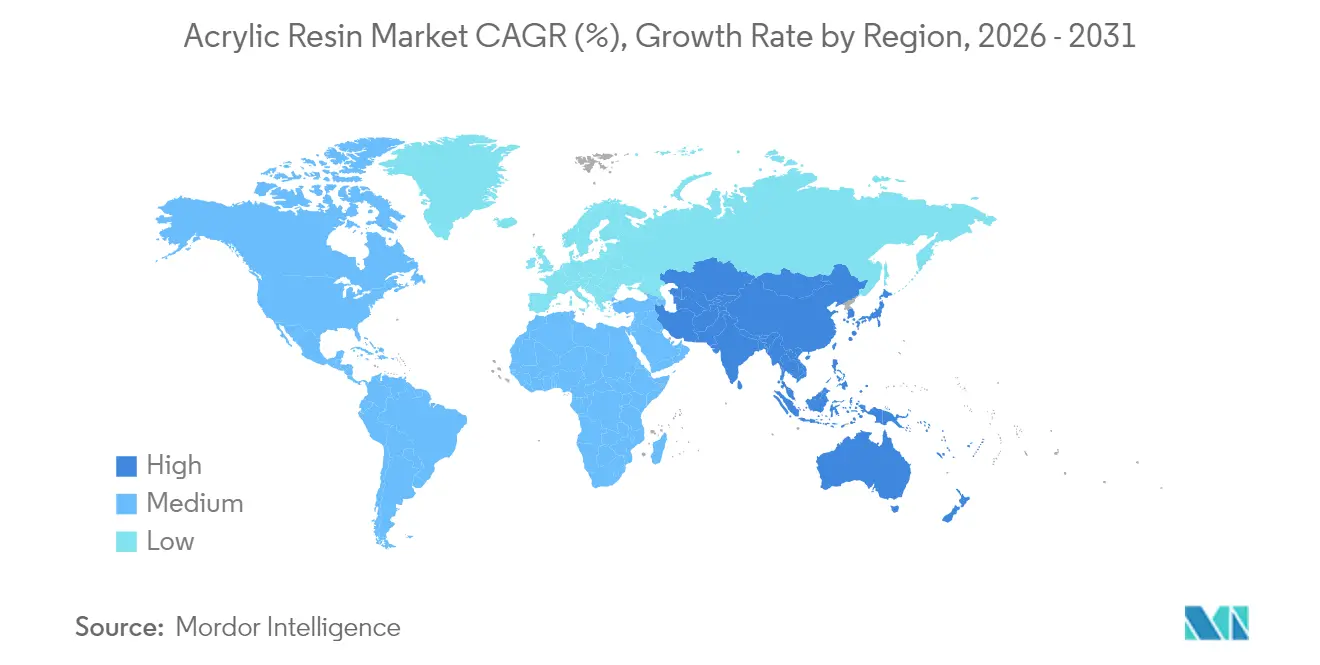

- By geography, Asia-Pacific accounted for 50.96% of the acrylic resin market in 2025 and is expanding at a 5.57% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acrylic Resin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion in construction and infrastructure activities | +1.2% | Global, with concentrated impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Rising demand for lightweight automotive components | +0.8% | North America, Europe, Asia-Pacific automotive corridors | Long term (≥ 4 years) |

| Increasing consumption of low-VOC waterborne coatings | +0.7% | North America and EU regulatory zones, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rapid adoption of 3D-printing photopolymer resins | +0.6% | North America, Europe, with emerging adoption in Asia-Pacific | Medium term (2-4 years) |

| Growth of smart/self-healing coating technologies | +0.4% | Global, with early adoption in aerospace and marine applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion in Construction and Infrastructure Activities

Global construction recovery underpins consistent acrylic resin market growth, with multi-year infrastructure programs in China, India, and the United States translating into rising coatings and panel demand. Project developers increasingly specify waterborne acrylics to meet green-building criteria, elevating consumption across exterior and interior applications. Formaldehyde-free binder technologies such as BASF’s Acrodur systems further strengthen market pull by aligning with indoor-air-quality standards. Overall, infrastructure spending assures a visible demand pipeline that anchors the acrylic resin market amid cyclical end-uses.

Rising Demand for Lightweight Automotive Components

Electrification accelerates lightweighting imperatives, and acrylic resins enable mass reduction across glazing, body panels, and battery enclosures. Collaborative product development, for example, Honda and Mitsubishi Chemical’s pre-colored PMMA parts, removes paint steps while lowering lifecycle CO₂ emissions by 50%. Regulatory fuel-economy targets in Europe and the United States guarantee long-run demand for high-strength, low-density polymers. Electric-vehicle battery housings further require thermal stability and dimensional accuracy, properties well served by methacrylate grades. Coupled with autonomous-vehicle sensor needs for optical clarity, these factors sustain premium volumes within the acrylic resin market.

Increasing Consumption of Low-VOC Water-Borne Coatings

Rule-making by the California Air Resources Board and Canada’s 2024 VOC limits is accelerating reformulation toward waterborne acrylics[1]California Air Resources Board, “Suggested Control Measure for Architectural Coatings,” arb.ca.gov. Manufacturers with compliant portfolios are securing share gains as industrial buyers pivot to safer chemistries. Water-borne systems also deliver durability and color retention benefits, boosting their value proposition beyond compliance alone. Investment in global ISCC+-certified lines enables firms such as BASF to market low-PCF acrylics with verified chain-of-custody attributes. The short-term conversion cycle positions the acrylic resin market for notable volume lifts through 2027 while permanently shifting the competitive baseline toward eco-efficient offerings.

Rapid Adoption of 3D-Printing Photopolymer Resins

High-resolution vat-polymerization processes depend on fast-curing, mechanically robust acrylic formulas. Academic research into recyclable, renewable lipoate-based resins demonstrates ongoing progress toward closed-loop photopolymers. Production-scale techniques such as continuous liquid interface production raise resin throughput, magnifying volume requirements. As aerospace and medical sectors migrate prototypes into certified production parts, they open an enduring premium niche inside the acrylic resin market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental and health hazards of acrylates | -0.9% | Global, with heightened scrutiny in North America and Europe | Short term (≤ 2 years) |

| Volatile propylene and MMA feed-stock prices | -1.1% | Global, with particular impact on integrated producers | Medium term (2-4 years) |

| Competition from bio-based polymer alternatives | -0.6% | Europe and North America leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental and Health Hazards of Acrylates

Regulators continue to evaluate exposure risks, tightening permissible monomer concentrations in manufacturing and consumer products. Enhanced ventilation, monitoring, and personal protective equipment raise compliance costs across the acrylic resin industry. Consumer awareness of VOC and odor profiles influences purchasing choices, particularly in residential coatings. Safety-driven brand differentiation is, therefore, necessary but costly for producers. Ongoing toxicology studies aim to substantiate safe-use thresholds, yet lingering perception risks cap adoption where substitute resins exist.

Volatile Propylene and MMA Feed-Stock Prices

Feedstock cost swings produce margin compression, with US propylene forecast to rise 5 cents per pound through mid-2025 amid constrained refinery capacity. Integrated majors partially offset volatility through captive production, whereas merchant participants rely on hedging tools that may be unavailable or uneconomic. Unpredictable input costs slow customer contract negotiations and can delay project approvals, moderating near-term acrylic resin market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Methacrylates Lead While Acrylates Accelerate

Methacrylates retained a 51.62% acrylic resin market share in 2025 thanks to their optical clarity and weatherability, but acrylates are on track for a 5.18% CAGR through 2031 as bio-based chemistries broaden their usage window. In volume terms, methacrylate grades serve glazing, signage, and premium coatings, anchoring the upper tier of the acrylic resin market. Acrylate polymers, propelled by adhesive and flexible-coating demand, capitalize on lower cost and easier processability, gaining ground in emerging applications. LG Chem’s roll-out of fully plant-derived acrylic acid illustrates how sustainability attributes are pulling customers toward acrylate variants.

Industry initiatives around chemical recycling are narrowing the performance gap between virgin and recovered methacrylates. Mitsubishi Chemical’s microwave-assisted depolymerization of post-consumer PMMA back to MMA monomer promises circular-economy compliance without sacrificing material quality. Advancements in catalyst architectures and reactor design further enhance throughput and property control across both product families, sharpening competitive differentiation.

By Application: Coatings Dominance Challenged by Adhesive Growth

Paints and coatings represented 46.02% of the acrylic resin market size in 2025, remaining the anchor application due to requirements for color retention, UV stability, and compliant VOC profiles. Interior architectural, industrial OEM, and protective marine segments rely heavily on waterborne acrylics to meet evolving standards. Nonetheless, adhesives and sealants will outpace coatings at a 5.27% CAGR to 2031 as construction recovery, e-commerce packaging, and automotive assembly boost demand for high-performance bonding agents. Acrylic structural adhesives offer fast cure, durability, and substrate versatility, making them indispensable in lightweight composite joining.

By End-User Industry: Construction Leadership Amid Automotive Acceleration

Building and construction retained 34.78% demand in 2025, driven by roof coatings, sealants, and decorative finishes tailored for energy-efficient structures. Infrastructure megaprojects in Asia-Pacific and stimulus-backed renovation programs in the European Union combine to create a resilient consumption backbone. Automotive is the fastest-moving end-user, expected to post a 5.47% CAGR through 2031 as electric-vehicle production scales and lightweight composite parts multiply. Acrylic grades find homes in battery enclosures, glazing units, and textured interior trims, replacing heavier metal and glass.

The electrical and electronics vertical benefits from 5G rollouts, where acrylic encapsulants deliver insulation alongside miniaturization tolerance. Textile and fiber finishes, though mature, increasingly prioritize bio-based or recycled content, creating incremental pull for greener acrylic formulations. Paper and board coatings are stabilizing due to e-commerce shipping volumes that require scuff-resistant, printable surfaces. Cross-industry synergies emerge as high-temperature automotive resins transfer into construction panels demanding improved thermal cycling endurance, underscoring the interconnected growth pathways within the acrylic resin market.

Geography Analysis

Asia-Pacific held 50.96% of global volume in 2025 and is positioned for a 5.57% CAGR through 2031, reflecting the region’s dual role as a manufacturing hub and rising consumption center. China continues to prioritize megainfrastructure investment, stimulating coatings and sealants uptake across transport, energy, and residential projects. Japan’s advanced automotive and electronics clusters carve out demand for premium methacrylate grades with tight optical and mechanical tolerances.

North America and Europe operate as technology and regulation leaders. The EPA’s revised aerosol-coating VOC rule grants a compliance grace period to 2027, yet still locks in a trajectory toward low-emission acrylic chemistries. European industry is channeling capital into chemical-recycling pilots and ISCC+ certified supply chains, reinforcing a premium on traceable low-PCF resins. Both regions lean heavily on lightweight automotive programs, adding high-margin outlets for specialty grades.

South America, the Middle East, and Africa are nascent but gathering pace. Industrialization, logistics corridors, and petrochemical joint ventures in the Gulf are fostering regional acrylic resin capacity additions. Although currency swings and regulatory heterogeneity pose hurdles, local market proximity cuts freight and import tariffs, improving cost-to-serve metrics.

Competitive Landscape

The acrylic resin market is moderately fragmented; top multinationals command significant yet contestable positions through scale, technology breadth, and geographic reach. Technology differentiation is decisive. Allnex’s merger with Nuplex created a global specialty-resin leader, enabling cross-regional delivery of high-solid, radiation-curable acrylics. Bio-based innovations, ISCC+ mass-balance certifications, and chemical-recycling breakthroughs add value propositions that command premium pricing and help customers hit carbon-reduction goals. Competitive intensity is therefore set to rise as players vie for leadership in sustainability and advanced-application submarkets within the acrylic resin market.

Acrylic Resin Industry Leaders

Arkema

BASF

Dow

Mitsubishi Chemical Group Corporation

Sumitomo Chemical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sumitomo Chemical announced commercial sales of chemically recycled acrylic resin to major electronics and automotive customers.

- July 2024: BASF secured ISCC+ certification for global sites, enabling more than 60 acrylic products with Low-PCF, Zero-PCF, bio-based, and recycled variants.

Global Acrylic Resin Market Report Scope

Acrylic resin is a group of thermoplastic materials derived from acrylic acid. Acrylic resins are made from alkyl acrylates and methacrylates as homo and co-polymers and are sometimes combined with other thermoplastic monomers. Their primary application lies in paints and coatings as primary binders and as adhesives and sealants across major end-user industries like construction, automotive, electrical, and electronics, to name a few.

The Acrylic Resin Market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into acrylates, methacrylates, and hybrid. By the application, the market is segmented into adhesives and sealants, paints and coatings, and other applications (pigment dispersion and elastomers). By end-user industry, the market is segmented into building and construction, automotive, plastics, textile and fibers, paper and paperboard, electrical and electronics, and other end-user industries (consumer goods and packaging).

The report also covers the market size and forecasts for the Acrylic Resin Market in 28 countries across five regions. For each segment, the market sizing and forecasts are done on the basis of volume (tons).

| Acrylates |

| Methacrylates |

| Hybrids |

| Paints and Coatings |

| Adhesives and Sealants |

| Other Applications (Pigment Dispersion, Elastomers, etc.) |

| Building and Construction |

| Automotive |

| Electrical and Electronics |

| Plastics |

| Textile and Fibers |

| Paper and Paperboard |

| Other Applications (Packaging and Consumer Goods) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Product Type | Acrylates | |

| Methacrylates | ||

| Hybrids | ||

| By Application | Paints and Coatings | |

| Adhesives and Sealants | ||

| Other Applications (Pigment Dispersion, Elastomers, etc.) | ||

| By End-User Industry | Building and Construction | |

| Automotive | ||

| Electrical and Electronics | ||

| Plastics | ||

| Textile and Fibers | ||

| Paper and Paperboard | ||

| Other Applications (Packaging and Consumer Goods) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the acrylic resin market and how fast is it growing?

The acrylic resin market size reached 7.13 million tons in 2026 and is projected to grow at a 3.99% CAGR, achieving 8.67 million tons by 2031.

Which region contributes most to acrylic resin demand?

Asia-Pacific accounts for 50.96% of global volume in 2025, supported by large construction programs and rising automotive output.

Which product segment is expanding fastest in the acrylic resin market?

Acrylate-based resins are expected to post a 5.18% CAGR through 2031 due to adhesive and bio-based formulation uptake.

What is driving acrylic resin use in electric vehicles?

Electric-vehicle makers rely on lightweight, thermally stable acrylic parts for battery enclosures, glazing, and interior components, pushing automotive demand to a 5.47% CAGR.

How are environmental regulations shaping product development?

Low-VOC mandates in North America and Europe accelerate the shift to water-borne acrylics and drive investment in bio-based and chemically recycled resin options.

Page last updated on: