Market Overview

| Study Period | 2021 - 2031 |

|---|---|

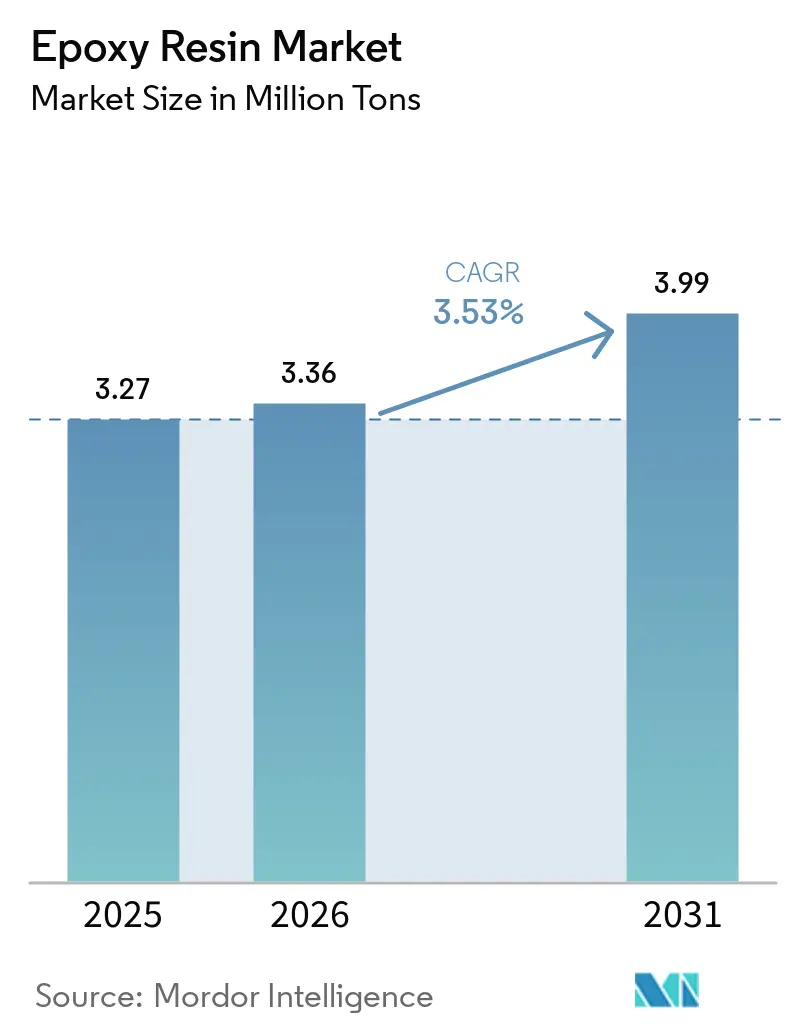

| Market Volume (2026) | 3.36 Million tons |

| Market Volume (2031) | 3.99 Million tons |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epoxy Resin Market Analysis by Mordor Intelligence

The Epoxy Resin Market size is expected to grow from 3.27 Million tons in 2025 to 3.36 Million tons in 2026 and is forecast to reach 3.99 Million tons by 2031 at 3.53% CAGR over 2026-2031. Sustained demand is rooted in the material’s unmatched mechanical, chemical, and thermal performance that underpins critical uses ranging from wind-turbine blades to semiconductor packaging. Innovation is accelerating as stricter regulations on bisphenol A (BPA) and volatile organic compounds (VOCs) advance waterborne, bio-circular, and low-VOC chemistries. Expanding renewable-energy infrastructure, electrification trends, and infrastructure spending in emerging economies add positive volume momentum, while escalating trade duties and raw-material price swings present near-term uncertainties for procurement teams. The epoxy resins market remains moderately concentrated, yet breakthrough work on recyclable and plant-derived formulations is widening the opportunity set for both incumbents and specialist newcomers.

Key Report Takeaways

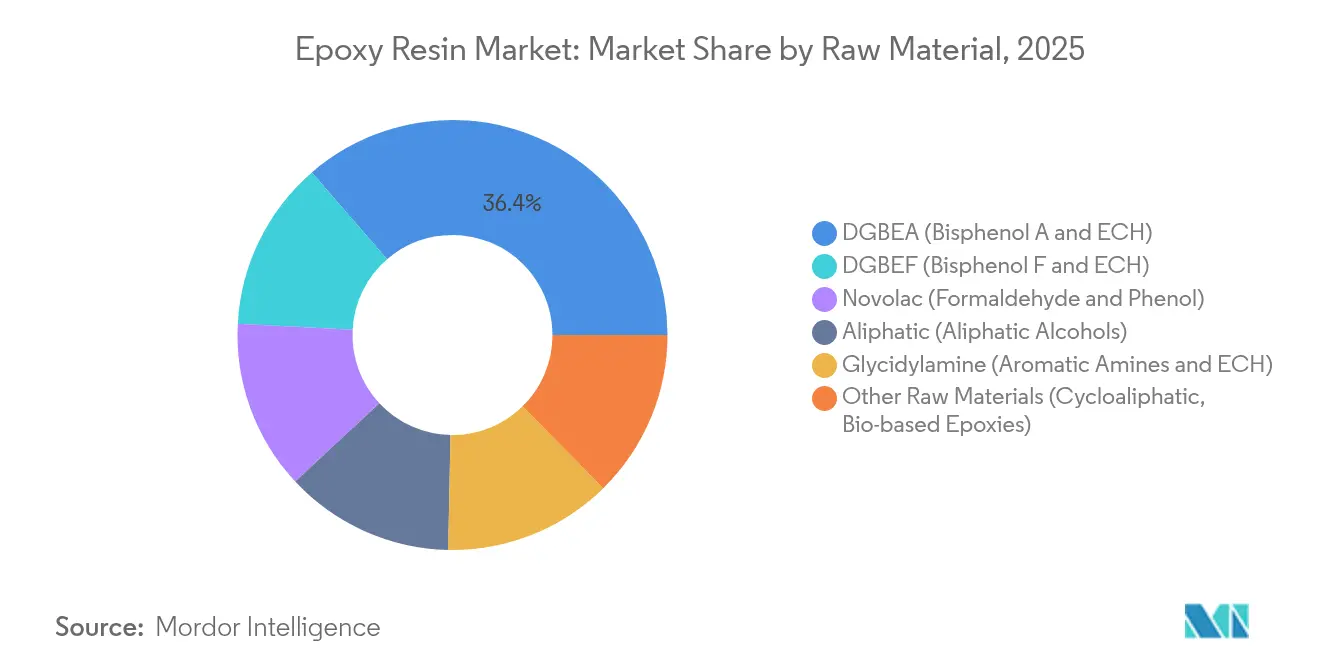

- By raw material, DGBEA resins commanded 36.35% of epoxy resins market share in 2025, while bio-based and cycloaliphatic grades are forecast to advance at a 6.66% CAGR through 2031.

- By physical form, waterborne dispersion is the fastest-growing segment, expanding at a 6.05% CAGR between 2026 and 2031.

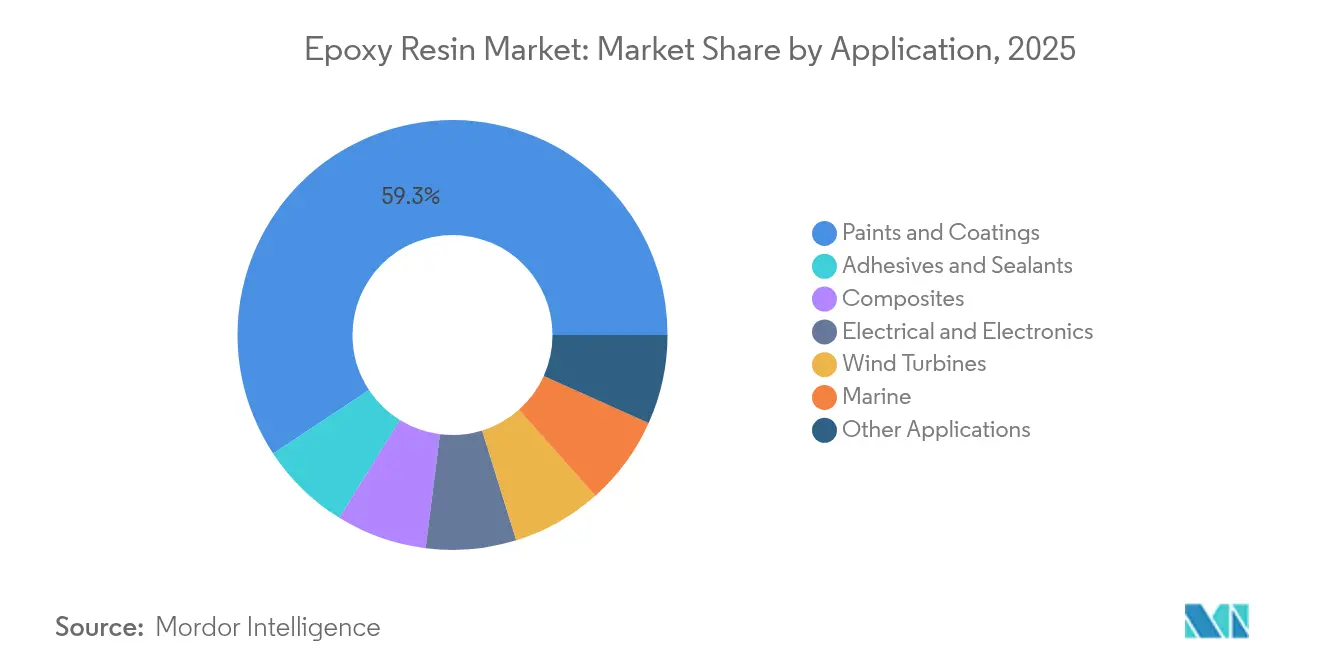

- By application, paints and coatings held 59.28% of the epoxy resins market size in 2025 and are set to advance at a 6.14% CAGR to 2031.

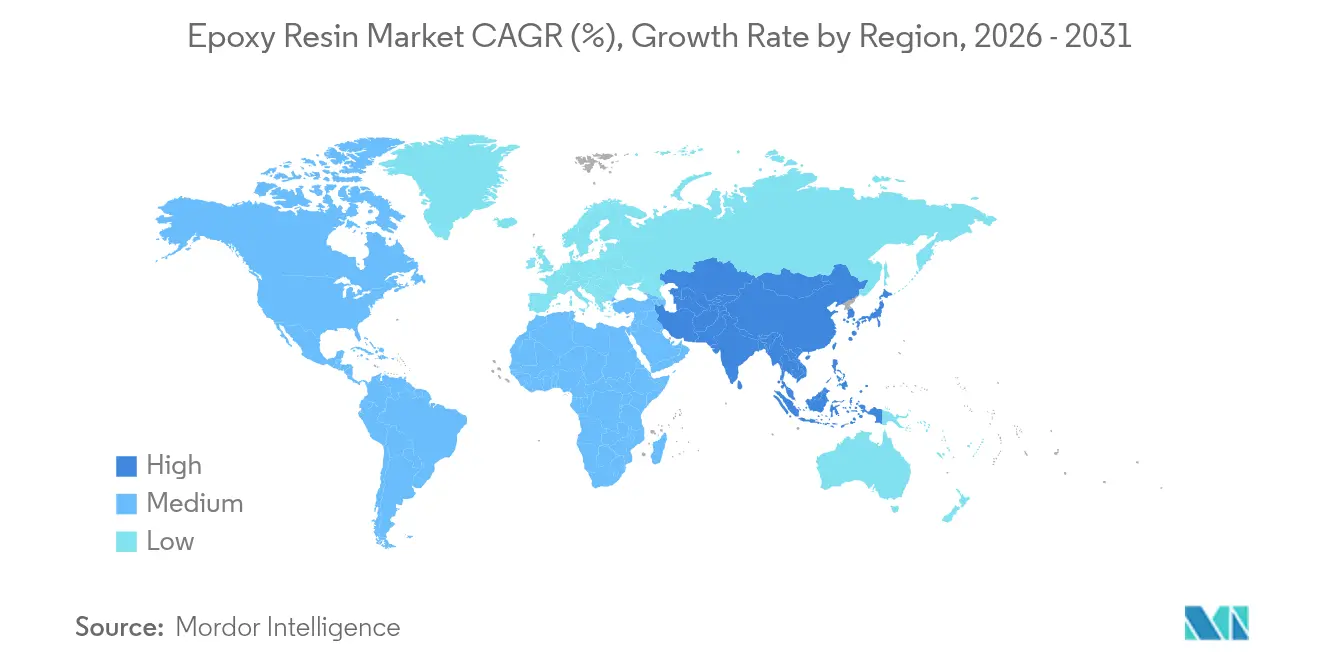

- By geography, Asia-Pacific accounted for 47.55% of 2025 global demand and is projected to post a 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Epoxy Resin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand from paints and coatings | 2.1% | Global, with APAC leading consumption | Medium term (2-4 years) |

| Wind-turbine blade composites uptake | 1.8% | Global, concentrated in North America, Europe, APAC offshore markets | Long term (≥ 4 years) |

| Increasing demand from electrical and electronics | 1.4% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Growing infrastructure-led adhesive demand | 1.2% | APAC and Middle-East and Africa | Medium term (2-4 years) |

| 3-D printed epoxy photopolymers adoption | 0.7% | North America and EU, early adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand from Paints and Coatings

Paints and coatings continued to dominate the epoxy resins market with a 60.15% revenue share in 2024. Growth is reinforced by infrastructure programs in Southeast Asia and Africa and by marine and packaging niches that depend on high-barrier, corrosion-resistant finishes. Westlake’s 2025 launch of EpoVIVE bio-circular resins illustrates how suppliers are balancing sustainability with performance[1]Westlake Corporation, “EpoVIVE Sustainable Epoxy Portfolio,” westlake.com. The shift to low-VOC formulations is aided by quantum-dot-catalyzed photochemistry that improves sunlight stability without costly UV blockers Marine-grade systems such as Amerlock 400 lengthen dry-dock cycles, lowering total lifecycle cost for fleet operators.The resulting 6.51% CAGR to 2030 positions coatings as both volume and innovation anchors for the broader epoxy resins market.

Wind-Turbine Blade Composites Uptake

Growing offshore wind installations, larger rotor diameters, and hybrid carbon-glass designs are raising epoxy performance thresholds. The Global Wind Energy Council forecasts 8.8% annual growth in new capacity, which underpins long-run resin demand. TPI Composites’ customer base supplied 88% of 2025 US onshore blades, underscoring how process know-how consolidates purchasing. Siemens Gamesa has already commercialized recyclable epoxy blades that de-bond under mild acidic conditions, easing end-of-life challenges. Machine-learning optimization of blade cure schedules further cuts waste and energy use, reinforcing epoxy’s position as the matrix of choice in the wind energy value chain.

Increasing Demand from Electrical and Electronics

Printed circuit board (PCB) production rebounded in 2024 with 6.3% growth, lifting demand for epoxy laminates and molding compounds. System-in-package architectures now require void-free encapsulation; integrated metal frames reduce gas entrapment during compression molding and are driving compound re-formulation. DIC’s EPICLON HP-4710 reaches a 350 °C glass-transition temperature, meeting thermal budgets for high-density semiconductor packages. Graphene-reinforced grades have delivered 77% tensile increases and 50 °C Tg gains, aligning epoxy with next-generation computing thermal loads. The renewed focus on regional PCB hubs in Thailand and Vietnam directs suppliers to install localized capacity, shortening lead times and reducing currency exposure.

Growing Infrastructure-Led Adhesive Demand

The global adhesives and sealants market, valued at USD 85.38 billion in 2025, tracks large-scale infrastructure projects that rely on structural bonding. Bio-based modifiers such as 5-HMF and SYLVASOLV oils improve sustainability profiles without sacrificing strength. Automotive lightweighting also substitutes adhesive joints for mechanical fasteners, boosting crash energy absorption and rust protection. UV-resistant stabilizers like Eversorb support bridges and solar-farm structures in high-irradiance zones. Prefabricated buildings exploit factory-applied epoxy adhesives that cure in controlled environments, elevating throughput and placement accuracy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -1.6% | Global, with acute impact in APAC manufacturing hubs | Short term (≤ 2 years) |

| Stricter VOC and BPA regulations | -1.1% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Anti-dumping duties disrupting trade flows | -0.9% | Global trade routes, concentrated impact on US-Asia trade | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

China expanded BPA capacity by 12.31% in H1 2024 to 5.48 million t pa, yet utilization dipped and regional prices fell 4.6% quarter-on-quarter in the epoxy resin industry. Disruptions such as the Guodu Chemical plant explosion temporarily doubled BPA prices, exposing downstream formulators to margin risk. Force-majeure declarations following extreme weather events added further supply uncertainty. Several epoxy majors are therefore building captive epichlorohydrin and BPA units to secure feedstock and hedge volatility.

Stricter VOC and BPA Regulations

The European Union banned BPA above 0.05 mg/L in food-contact materials in January 2025. The US EPA then tightened VOC limits for aerosol coatings, with compliance slated for January 2027. South Coast AQMD is finalizing even lower thresholds for automotive primers, compelling resin producers to shift toward waterborne and solid forms. Tree-bark-derived alternatives are under study, although commercialization remains several years away. Waterborne systems integrating natural rubber latex already achieve 370% elongation gains, proving the feasibility of low-VOC, high-toughness coatings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: DGBEA Dominance Faces Sustainability Pressure

DGBEA resins retained 36.35% epoxy resin market share in 2025 as the workhorse grade for wind-energy blades and automotive composites. At a 6.32% CAGR they remain integral to market expansion, yet customer audits are pushing producers to demonstrate traceable, lower-carbon BPA supply. In response, Western and Japanese suppliers are piloting mass-balance accounting and bio-circulating feedstocks to preserve DGBEA’s position in the epoxy resins market.

Specialty resins fill clear performance gaps. DGBEF offers lower viscosity for marine maintenance coatings, while novolac chemistries withstand thermal shock inside furnace linings. Aliphatic epoxies deliver UV stability essential for architectural façades. Glycidylamine versions provide superior metal adhesion in electronics housings. Bio-based and cycloaliphatic chemistries, grouped under other raw materials, are projected to be the fastest movers and could capture a measurable slice of the epoxy resins market by 2031 as closed-loop recycling and carbon accounting gain shareholder focus.

By Physical Form: Liquid Segment Adapts to Sustainability Demands

Liquid grades represented 49.10% of 2025 volume thanks to meter-mix simplicity and long open times used by blade and marine yards. Modern line-side dosing systems lower operator exposure and improve batch consistency, keeping liquids central to the epoxy resins market even as sustainability pressures mount.

Solid and solution forms remain vital in powder and spray coatings. However, waterborne dispersions are gaining ground at a 6.05% CAGR. Advances in non-ionic surfactants and room-temperature amine hardeners have produced zero-solvent floor systems that rival solvent-borne durability. Pilot projects pairing plant-oil adducts with waterborne dispersions have shown mechanical parity with traditional grades, pointing to an expanded role for these chemistries in upcoming VOC-constrained geographies.

By Application: Paints and Coatings Leadership Drives Innovation

Paints and coatings accounted for 59.28% of 2025 demand, retaining the single-largest slice of the epoxy resin market. High-build primers protect bridges, ship hulls, and chemical tanks, while packaging lines deploy BPA-safe interior can coatings. Volume opportunities extend into construction boom regions where epoxy floorings resist abrasion and aggressive cleaning agents.

Adhesives and sealants follow closely, underpinned by infrastructure and automotive programs targeting lightweight, corrosion-free joints. Composite applications add momentum via wind blades, aerospace interiors, and sporting goods. Electrical and electronics pull in high-Tg encapsulants that handle 350 °C reflow spikes in the epoxy resin industry. Wind turbines and marine niches, though niche in tonnage, offer premium margins through specification-driven chemistries that lock in multi-year supply contracts.

Geography Analysis

Asia-Pacific remained the epicenter of the epoxy resin market, securing 47.55% of 2025 demand and pointing to a 6.08% CAGR through 2031. China’s resin exports face US anti-dumping duties as high as 354.99%, prompting ventures like DCM Shriram’s USD 125 million Indian greenfield unit to serve a more regionally diversified customer base. Thailand and Vietnam capture fresh PCB and wind-blade capacity, while Japan and South Korea push ultra-high-Tg and recyclable chemistries for semiconductors and offshore wind applications.

North America leverages reshoring, infrastructure investment, and renewable-energy tax credits to strengthen its position in the epoxy resin market and buffer volatility in imported resin flows. Countervailing duties ranging from 1.01% to 547.76% spur domestic producers to reactivate idled reactors and invest in new feedstock assets. Canadian wind-farm developers specify Arctic-grade epoxy systems, and Mexico’s automotive clusters accelerate demand for structural adhesives. NREL’s plant-derived epoxy research underscores the region’s sustainability leadership.

Europe balances stringent BPA rules with cutting-edge R&D in the epoxy resin market. German automotive suppliers co-engineer thermally conductive EMCs with local resin formulators. The United Kingdom’s offshore wind boom sustains 25-year service life requirements for epoxy-primed monopiles, and France’s nuclear sector pushes radiation-resistant grades. Scott Bader’s GBP 30 million UK capacity addition highlights commitments to local supply amid global logistics flux. The Nordic region, already well advanced in circular-economy policy, pilots closed-loop epoxy recycling trials under EU-funded programs.

Competitive Landscape

Global producers such as Dow, Huntsman, Hexion, Olin, and Westlake anchor the epoxy resin market through integrated feedstock, wide product lines, and multi-continent manufacturing bases. Huntsman fortified high-performance niches by acquiring CVC Thermoset Specialties and Gabriel Performance Products, gaining tougheners and specialty curing agents that support aerospace and electronics customers[2]Huntsman Corporation, “Acquisition of CVC Thermoset Specialties,” huntsman.com. Hexion’s EcoBind platform satisfies VOC and formaldehyde regulations while maintaining composite mechanical metrics, illustrating how regulatory agility now defines competitive positioning.

Process technologies differentiate players in the epoxy sesin market. Rapid-cure two-component systems for resin-transfer-molded wind blades cut cycle time from hours to under 30 minutes, slashing plant energy bills. Partnerships such as Aditya Birla with Vartega address recyclability, integrating depolymerizable matrices into carbon-fiber value chains.

Opportunities for niche entrants in the epoxy resins market revolve around bio-based feedstocks, closed-loop systems, and 3-D printing photopolymers where responsiveness and formulation agility outpace the slower pipelines of large incumbents. Venture-backed firms are piloting plant-oil-based diglycidyl ethers that match DGBEA strength while cutting greenhouse-gas footprints by up to 40%. The continual tightening of regulatory screws suggests these specialties will progressively migrate from experimental to mainstream over the forecast horizon.

Epoxy Resin Industry Leaders

Olin Corporation

Hexion Inc.

Kukdo Chemical Co. Ltd

Huntsman International LLC

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Westlake Epoxy debuted the EpoVIVE portfolio featuring low-carbon, bio-circular epoxy resins and waterborne technologies for floorings and anti-corrosion coatings.

- February 2025: Sichuan University developed a recyclable epoxy resin with a 192 °C Tg and hydrothermal degradation capability at 200 °C for aerospace and wind applications.

Global Epoxy Resin Market Report Scope

Epoxy resins, created by reacting epoxide groups with a hardener, yield robust and durable polymer chains. These resins find widespread application in industrial lubricants, adhesives, coatings, and composites owing to their superior mechanical properties, chemical resistance, and thermal stability.

The epoxy resin market is segmented by raw material, application, and geography. By raw material, the market is segmented into DGBEA (Bisphenol A and ECH), DGBEF (Bisphenol F and ECH), novolac (formaldehyde and phenols), aliphatic (aliphatic alcohols), glycidyl amine (aromatic amines and ECH), and other raw materials. By application, the market is segmented into paints and coatings, adhesives and sealants, composites, electrical and electronics, marine, wind turbines, and other applications. The report also covers the market sizes and forecasts for the epoxy resin market in 27 countries across major regions. For each segment, the market sizing and forecasts are made on the basis of volume (tons).

By Raw Material

| DGBEA (Bisphenol A and ECH) |

| DGBEF (Bisphenol F and ECH) |

| Novolac (Formaldehyde and Phenol) |

| Aliphatic (Aliphatic Alcohols) |

| Glycidylamine (Aromatic Amines and ECH) |

| Other Raw Materials (Cycloaliphatic, Bio-based Epoxies) |

By Physical Form

| Liquid |

| Solid |

| Solution |

| Waterborne Dispersion |

By Application

| Paints and Coatings |

| Adhesives and Sealants |

| Composites |

| Electrical and Electronics |

| Wind Turbines |

| Marine |

| Other Applications (Construction, 3-D Printing Photopolymers, etc.) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material | DGBEA (Bisphenol A and ECH) | |

| DGBEF (Bisphenol F and ECH) | ||

| Novolac (Formaldehyde and Phenol) | ||

| Aliphatic (Aliphatic Alcohols) | ||

| Glycidylamine (Aromatic Amines and ECH) | ||

| Other Raw Materials (Cycloaliphatic, Bio-based Epoxies) | ||

| By Physical Form | Liquid | |

| Solid | ||

| Solution | ||

| Waterborne Dispersion | ||

| By Application | Paints and Coatings | |

| Adhesives and Sealants | ||

| Composites | ||

| Electrical and Electronics | ||

| Wind Turbines | ||

| Marine | ||

| Other Applications (Construction, 3-D Printing Photopolymers, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the epoxy resin market and its growth outlook?

The Epoxy Resin Market size is expected to grow from 3.27 Million tons in 2025 to 3.36 Million tons in 2026 and is forecast to reach 3.99 Million tons by 2031 at 3.53% CAGR over 2026-2031.

Which raw-material segment leads the epoxy resin market?

DGBEA resins held 36.35% of 2025 global demand due to their mechanical strength and established supply networks.

How are VOC and BPA regulations influencing product development?

Regulations in the EU and United States are accelerating the shift to waterborne, bio-circular, and BPA-free epoxy systems that satisfy low-emission targets without sacrificing performance.

Why is Asia-Pacific dominant in the epoxy resin market?

The region concentrates end-use manufacturing in wind energy, electronics, and construction, giving it 47.55% of 2025 global demand and a projected 6.08% CAGR through 2031.

What innovations address epoxy resin recyclability?

Catalyst-driven depolymerization at sub-200 °C and recyclable blade chemistries enable recovery of fibers and monomers, opening circular-economy pathways for high-value composites.

Page last updated on: