Impregnating Resins Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.5 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

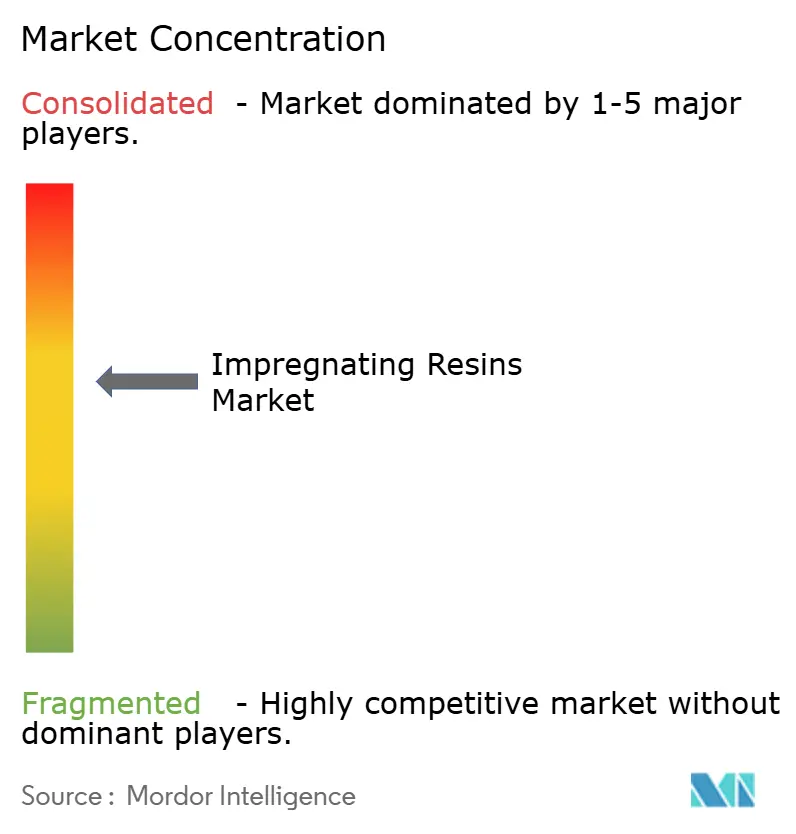

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Impregnating Resins Market Analysis by Mordor Intelligence

The Impregnating Resins Market size is expected to increase from USD 1.86 billion in 2025 to USD 1.95 billion in 2026 and reach USD 2.5 billion by 2031, growing at a CAGR of 5.04% over 2026-2031. End-users are racing to meet stricter motor-efficiency mandates, scale solvent-free production lines that comply with hazardous-air-pollutant ceilings, and localize supply chains for electrified vehicles and semiconductor fabs across the Asia-Pacific. Rapid growth in permanent-magnet synchronous motors, data-center cooling equipment, and offshore wind generators is lifting demand for Class H and Class C polyester-imide and epoxy systems. The U.S. Environmental Protection Agency’s metal HAP limit for new coating facilities is accelerating the phase-out of toluene- and xylene-based varnishes, while the European Commission’s Euro 7 regulation is pushing automakers toward higher-temperature traction-motor insulation. Capital intensity remains a hurdle, a single automated vacuum-pressure impregnation (VPI) line tops USD 5 million, but emerging contract impregnation hubs in Southeast Asia are reducing entry barriers for small manufacturers.

Key Report Takeaways

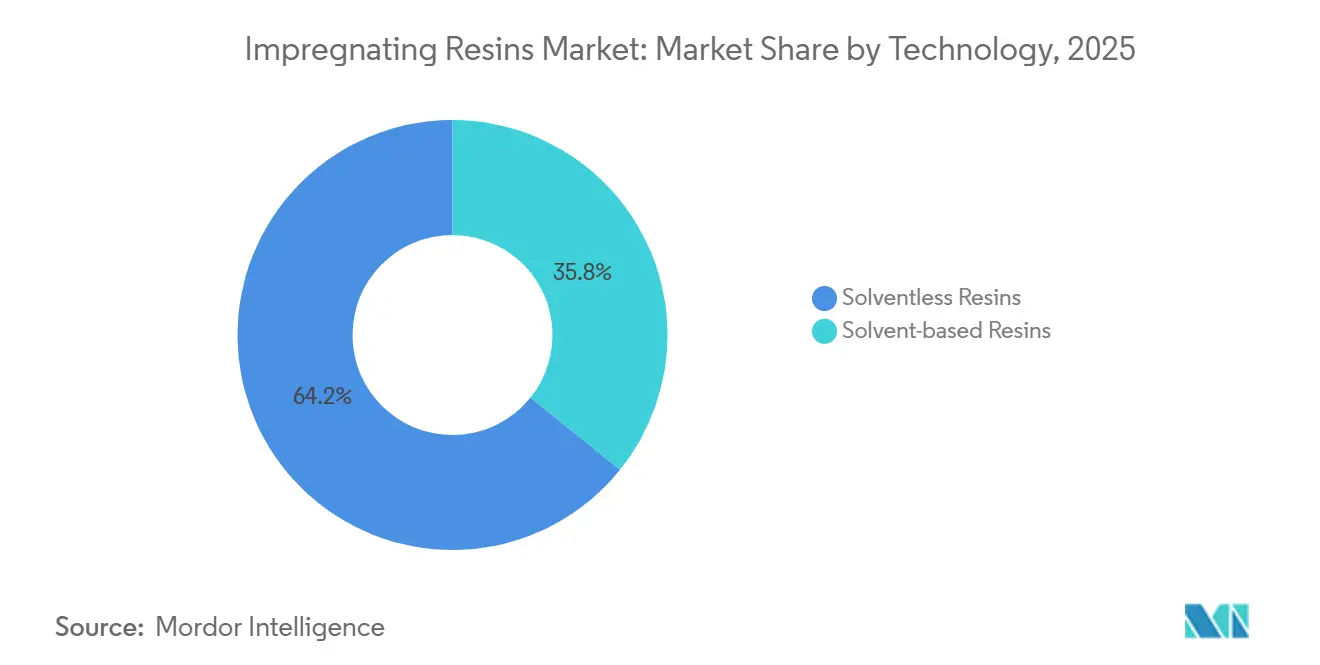

- By technology, solventless formulations held 64.23% of impregnating resins market share in 2025 and are on track for a 5.15% CAGR through 2031.

- By resin type, the Other Resins category commanded 38.67% share of the impregnating resins market size in 2025, while epoxy is projected to expand at a 5.12% CAGR between 2026 and 2031.

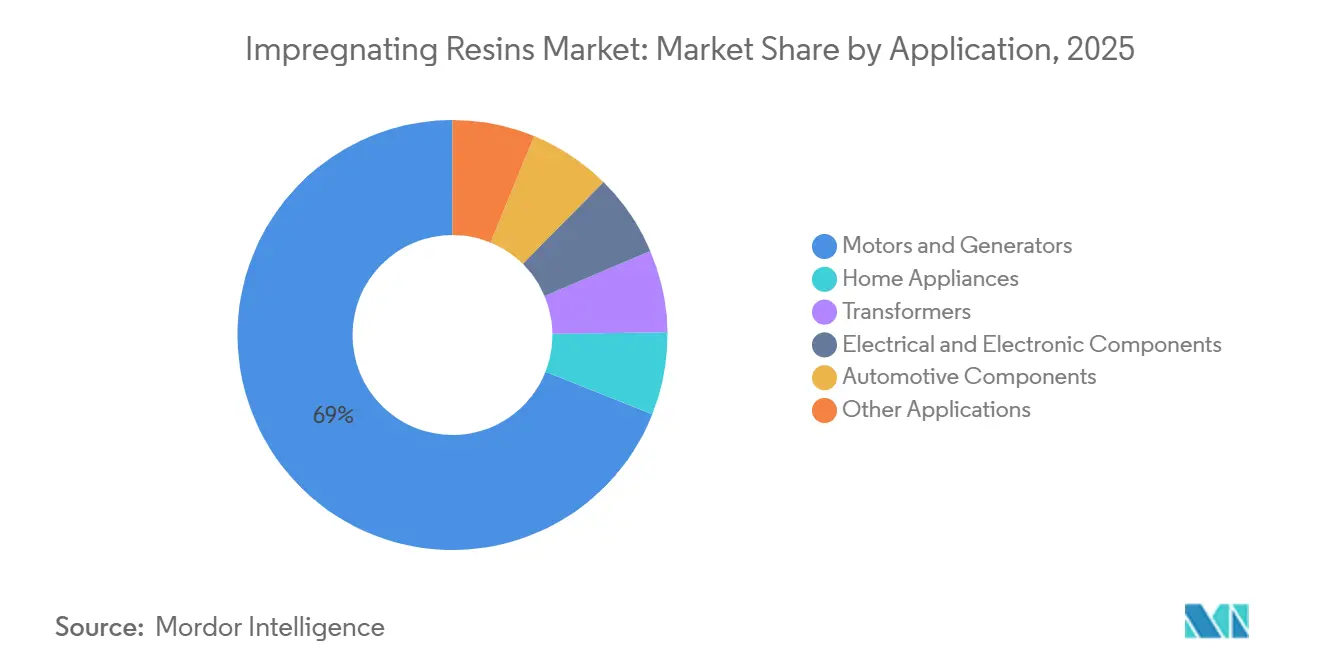

- By application, motors and generators accounted for 68.98% share of the impregnating resins market size in 2025 and are advancing at a 5.06% CAGR through 2031.

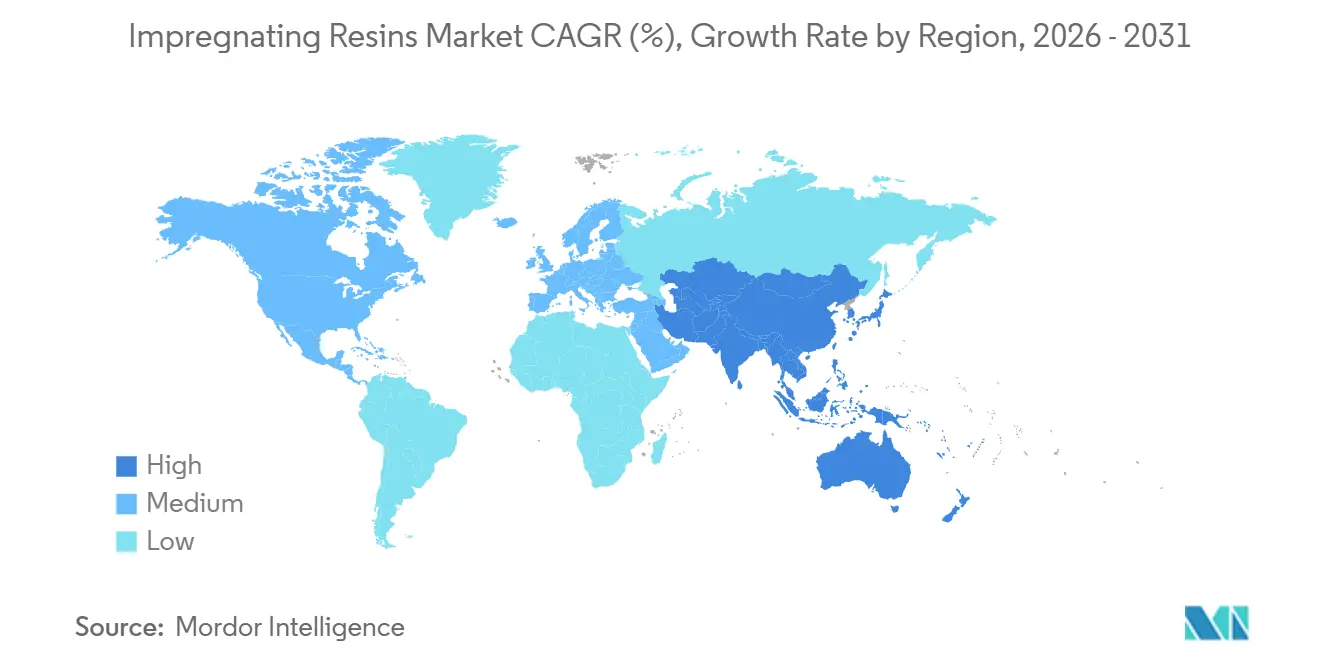

- By geography, Asia-Pacific led with 41.24% impregnating resins market share in 2025 and is forecast to grow at a 5.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Impregnating Resins Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for High-Efficiency Electric Motors | +1.8% | Global, notably EU, China, North America | Medium term (2-4 years) |

| OEM Shift toward Solvent-Free Impregnation Processes | +1.3% | North America, EU, spill-over to APAC | Short term (≤ 2 years) |

| Grid-Scale Wind-Turbine Installation Growth | +0.6% | Europe, North America, Chinese coastal provinces | Long term (≥ 4 years) |

| EV Traction-Motor Production Acceleration | +1.1% | China, South Korea, Japan, North America, EU | Medium term (2-4 years) |

| Miniaturization of Consumer Electronics | +0.5% | Japan, South Korea, Taiwan, China, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for High-Efficiency Electric Motors

Escalating minimum energy-performance standards are shrinking permissible motor losses and forcing OEMs to adopt VPI to eliminate voids that spark partial discharge. The European Ecodesign Directive requires IE3 efficiency for ≥0.75 kW motors, while China’s GB 18613-2020 is aligned with IEC 60034-30-1 efficiency classes. Slot-fill factors above 70% and concentrated permanent-magnet hot spots are pushing resin performance toward glass-transition temperatures of 180 °C. Compliance with IEC 60034-18-41 partial-discharge testing embeds VPI as a prerequisite, locking in long-term resin consumption as global motor fleets shift to IE4 and IE5.

OEM Shift toward Solvent-Free Impregnation Processes

Metal HAP ceilings of 0.0079 grains per dry standard cubic foot for new U.S. coating facilities make solvent-based varnishes uneconomical unless paired with thermal oxidizers. Europe’s Industrial Emissions Directive and China’s Blue-Sky Action Plan mirror these caps. New solventless chemistries cut cure cycles from six hours to under ninety minutes on automated trickle-impregnation lines. Wacker Chemie’s SILRES H62 C cures at room temperature within twenty-four hours, removes post-bake ovens, and slashes plant energy use by roughly 40%.

Grid-Scale Wind-Turbine Installation Growth

Global wind additions hit 117 GW in 2024, and cumulative capacity is expected to top 1,200 GW by 2030. Modern 8-15 MW offshore generators operate at up to 6.6 kV, demanding Class H or Class C epoxy or polyester-imide insulation. Retrofits of 15- to 20-year-old onshore units across Europe and North America extend service life, creating a secondary market for on-site impregnation services that can requalify generators without lifting rotors, accelerating resin demand beyond new-build volumes[1]Global Wind Energy Council, “Global Wind Report 2025,” gwec.net.

EV Traction-Motor Production Acceleration

Pulse-width-modulated inverters induce voltage spikes near 1,200 V and high switching frequencies, intensifying insulation stress. Federal incentives under the U.S. Inflation Reduction Act, combined with China’s dual-credit scheme, are co-locating traction-motor assembly with domestic impregnation capacity. Distributed windings that rely on full VPI are displacing hairpin designs in several vehicle platforms, cementing epoxy and polyester-imide requirements for Class H performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VOC and HAP Regulatory Tightening | –0.9% | North America, EU, China, India | Short term (≤ 2 years) |

| Price Volatility of Bisphenol-A and Styrene Feedstocks | –0.7% | Asia-Pacific, Europe, global spot markets | Medium term (2-4 years) |

| Capital-Intensive Vacuum-Pressure Equipment | –0.4% | India, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

VOC and HAPS Regulatory Tightening

Compliance with updated U.S. EPA and EU emission standards obliges legacy plants to install oxidizers that cost USD 0.8–1.5 million each, squeezing margins and delaying expansions. Small motor shops lacking in-house formulation expertise face high validation costs to switch to solventless systems, often resorting to contract impregnation that inflates unit costs. European anti-dumping duties of up to 40.8% on Chinese epoxy imports further elevate raw-material prices, adding complexity for regional OEMs[2]European Commission, “Anti-Dumping Duties on Epoxy Resins,” ec.europa.eu.

Price Volatility of Bisphenol-A and Styrene Feedstocks

Bisphenol-A spot prices in Asia oscillated by nearly 50% during 2024-2025 as phenol oversupply combined with outages at epichlorohydrin facilities. Contract styrene prices on the U.S. Gulf Coast swung by USD 550 per ton over the same period. Such variability can erase 150-200 basis points of profitability for motor OEMs and discourages long-term resin supply agreements, postponing capacity expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solventless Formulations Extend Compliance Leadership

Solventless resins captured 64.23% of the impregnating resins market share in 2025 and are forecast to grow at 5.15% through 2031. Their exothermic cure eliminates solvent evaporation, shortens cycle time, and bypasses multi-million-dollar thermal oxidizers mandated under 40 CFR Part 63, Subpart HHHHH. Energy savings reach 40% compared with conventional bake-and-cure lines, making solventless systems attractive even in geographies with modest electricity tariffs. Trickle-impregnation machines that marry solventless chemistry with automated winding handling are spreading from large motor OEMs to contract shops, compressing takt times to under ninety minutes.

Solvent-based varnishes persist in retrofit lines and developing markets where emission enforcement is patchy. An installed base of legacy tanks and ovens, often amortized years ago, cushions operating budgets. Yet, as imported replacement solvents face tighter customs checks and rising taxes, converters are budgeting capex for solventless upgrades in the 2027-2029 window, aligning with planned motor model changes.

By Resin Type: Epoxy Poised for Fastest Growth on Electronics Uptake

Epoxy volumes are projected to rise at a 5.12% CAGR, the highest among resin types, even though Other Resins commanded 38.67% share in 2025. Low dielectric loss, robust adhesion to copper, and compatibility with automated dispensing make epoxy the preferred choice for fine-pitch windings and semiconductor underfill. Emerging 48-V mild-hybrid vehicles further amplify demand for Class H epoxy insulation that survives inverter-induced spikes.

Polyester resins remain entrenched in cost-sensitive appliance motors, while polyester-imides address high-voltage wind-turbine and traction-motor duty cycles. Silicone systems are gaining ground in battery encapsulation, owing to flame-retardant chemistry and resistance to thermal cycling. Polyurethanes occupy a niche in outdoor generators that face moisture ingress, offering flexibility that mitigates delamination under thermal shock.

By Application: Motors and Generators Retain Volume Leadership

Motors and generators accounted for 68.98% of the impregnating resins market share in 2025 and are expected to advance at a 5.06% CAGR to 2031. Higher slot-fill factors in IE4 and IE5 machines, combined with thinner air gaps, raise winding temperatures and accelerate the adoption of Class H and Class C systems. Electric-vehicle traction motors intensify these requirements with inverter-driven voltages up to 1,200 V and switching frequencies above 10 kHz, making full VPI indispensable.

Transformers, especially dry types for urban substations, represent a steady growth avenue as utilities seek fire-safe alternatives to oil-filled units. Appliance motors, from refrigerator compressors to washing-machine drives, continue to transition from dip-and-bake to trickle impregnation to meet U.S. Department of Energy efficiency thresholds. Inductors, solenoids, and other electronics components consume low-viscosity epoxy grades capable of penetrating sub-0.1 mm gaps, supporting the miniaturization of consumer devices.

Geography Analysis

Asia-Pacific held 41.24% impregnating resins market share in 2025 and is set to grow at a 5.14% CAGR through 2031. China’s dual-credit policy yielded 10.2 million new-energy vehicles in 2024 and targets a 50% NEV sales mix by 2035, anchoring large-scale traction-motor demand. India’s Production-Linked Incentive schemes earmark USD 2.3 billion for electronics and USD 10 billion for semiconductor fabs, catalyzing local consumption of polyester-imide and epoxy grades. Japan’s subsidy program covers up to 50% of fab construction costs, building a domestic supply chain for low-chloride epoxy underfill compatible with advanced packaging. South Korean chipmakers are standardizing fast-cure epoxy for system-in-package modules, while Thailand and Vietnam offer multi-year tax holidays that attract contract impregnation houses, balancing regional capacity.

North America leverages USD 369 billion in clean-energy incentives under the Inflation Reduction Act, which ties consumer tax credits to domestic content thresholds. Automakers have announced tens of billions in capex for traction-motor assembly lines in Michigan, Kentucky, and Tennessee, all specifying solventless epoxy formulations that satisfy the U.S. EPA’s HAP ceiling. Canada’s Strategic Innovation Fund and Mexico’s near-shoring inflows round out a regional corridor that localizes resin sourcing under USMCA’s 75% regional-value rules.

Europe is guided by the Green Deal’s 2035 zero-emission target and Euro 7 standards, accelerating Class H traction-motor insulation in Germany, France, and Italy. Offshore wind build-outs in the North Sea and Baltic Sea are driving Class C epoxy adoption for 15 MW generators. Anti-dumping duties on Asian epoxy imports open share for domestic formulators, though recent plant closures constrain near-term solventless supply. Eastern Europe and Russia maintain polyester demand for rail and oil-field motors, despite geopolitical headwinds.

South America’s growth centers on Brazil’s 2.3 million-unit automotive output, which is pivoting to flex-fuel hybrids. Chile’s electrified copper mines and Colombia’s renewable auctions are introducing Class H requirements for heavy-duty generators. The Middle East and Africa add incremental demand via megaprojects such as Saudi Arabia’s NEOM and South Africa’s grid-modernization, though currency volatility impacts import economics for specialty resins.

Competitive Landscape

The impregnating resins market is moderately consolidated. Innovation pipelines focus on ambient-cure epoxy-silicone hybrids, flame-retardant silicones with thermal conductivity above 1.5 W/m-K for EV battery packs, and ultra-low-viscosity epoxies for 5G power modules. Quality consistency remains a barrier for low-cost entrants: chloride contamination above 100 ppm disqualifies many formulations from automotive qualification. European anti-dumping tariffs shift cost advantages but also spur local capacity expansions from incumbents.

Impregnating Resins Industry Leaders

ALTANA (ELANTAS)

Von Roll

Axalta Coating Systems, LLC

Henkel AG and Co. KGaA

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Momentive launched a flame-retardant silicone resin for EV battery encapsulation that delivers thermal conductivity above 1.5 W/m-K and dielectric strength of 20 kV/mm.

- May 2024: Wacker Chemie introduced SILRES H62 C, a silicone-modified epoxy that cures at room temperature within twenty-four hours, removes post-bake ovens, and meets IEC 60085 Class F requirements.

Global Impregnating Resins Market Report Scope

Impregnating resins are liquid substances, frequently based on epoxy or polyester, crafted to permeate and saturate porous materials like paper or fabric, aiming to improve mechanical and electrical characteristics. They are commonly utilized in various industries, including electrical components, transformers, and printed circuit boards, for insulation, protection, and structural reinforcement.

The impregnating resin market is segmented by technology, resin type, application, and geography. By technology, the market is segmented into solventless resins and solvent-based resins. By resin type, the market is segmented into epoxy, polyester, polyester-imide, and other resin types (polyurethane, silicone, and others). By application, the market is segmented into motors and generators, home appliances, transformers, electrical and electronic components, automotive components, and other applications. The report also covers the market size and forecast for the impregnating resin market in 26 countries across major regions. For each segment, the market sizing and forecast have been done on the basis of value (USD).

| Solventless Resins |

| Solvent-based Resins |

| Epoxy |

| Polyester |

| Polyester-imide |

| Other Resin Types (Polyurethane, silicone, etc.) |

| Motors and Generators |

| Home Appliances |

| Transformers |

| Electrical and Electronic Components |

| Automotive Components |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Technology | Solventless Resins | |

| Solvent-based Resins | ||

| By Resin Type | Epoxy | |

| Polyester | ||

| Polyester-imide | ||

| Other Resin Types (Polyurethane, silicone, etc.) | ||

| By Application | Motors and Generators | |

| Home Appliances | ||

| Transformers | ||

| Electrical and Electronic Components | ||

| Automotive Components | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the impregnating resins market by 2031?

The impregnating resins market is projected to reach USD 2.50 billion by 2031.

Which technology segment leads the global market?

Solventless formulations dominated with a 64.23% share in 2025 and maintain the highest growth outlook to 2031.

Why are epoxy resins growing faster than other types?

Low dielectric loss, strong copper adhesion, and compatibility with automated trickle lines position epoxy for the fastest 5.12% CAGR to 2031.

How do environmental regulations influence resin selection?

VOC and metal-HAP ceilings in the U.S., EU, and China effectively force OEMs to adopt solvent-free resins or install costly abatement systems.

Which region is expected to contribute the largest incremental demand?

Asia-Pacific, led by China, India, and Japan, is projected to add the most volume, aided by EV mandates and semiconductor investment.

What capital hurdle limits new entrants?

A full VPI line costs more than USD 5 million and requires extensive IEC 60085 testing, concentrating capacity among financially strong incumbents.

Page last updated on: