Packaging Resins Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

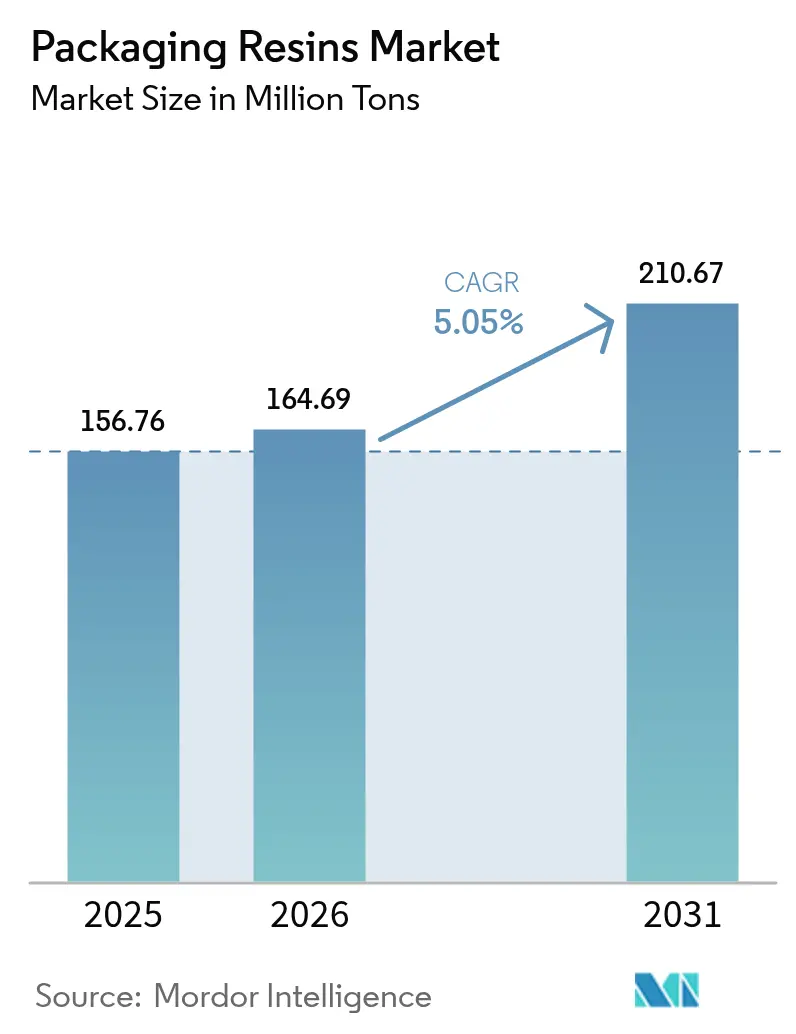

| Market Volume (2026) | 164.69 Million tons |

| Market Volume (2031) | 210.67 Million tons |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

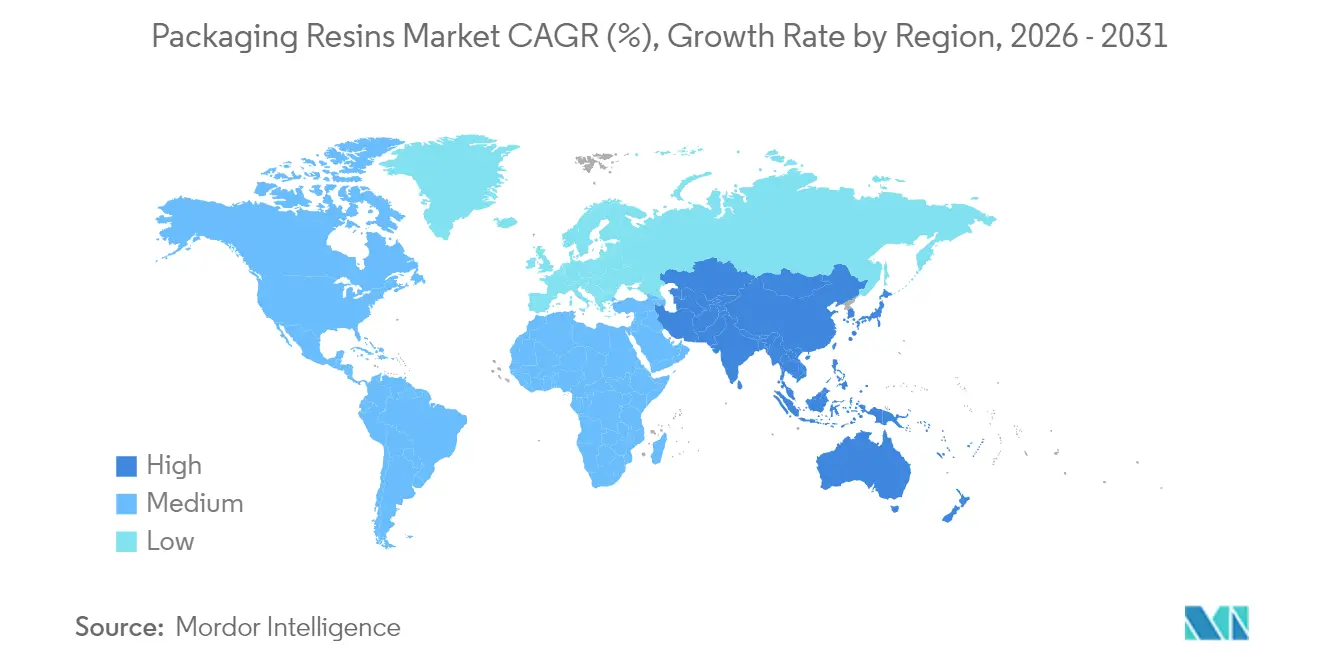

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Resins Market Analysis by Mordor Intelligence

Packaging Resins market size in 2026 is estimated at 164.69 Million tons, growing from 2025 value of 156.76 Million tons with 2031 projections showing 210.67 Million tons, growing at 5.05% CAGR over 2026-2031. This steady expansion reflects resilient demand across food, beverage, healthcare, and e-commerce channels, ongoing material substitutions toward lighter structures, and accelerating investments in advanced recycling. Supply-side efficiencies—especially in Asia-Pacific—temper unit cost escalation even as feedstock volatility rises. Tighter global rules on recycled content stimulate resin modification work, while corporate decarbonization commitments push converters to secure low-carbon and bio-based feedstocks. M&A activity targeting synergy capture and circular-economy capabilities continues, indicating that scale and technology breadth now matter as much as geographic reach.

Key Report Takeaways

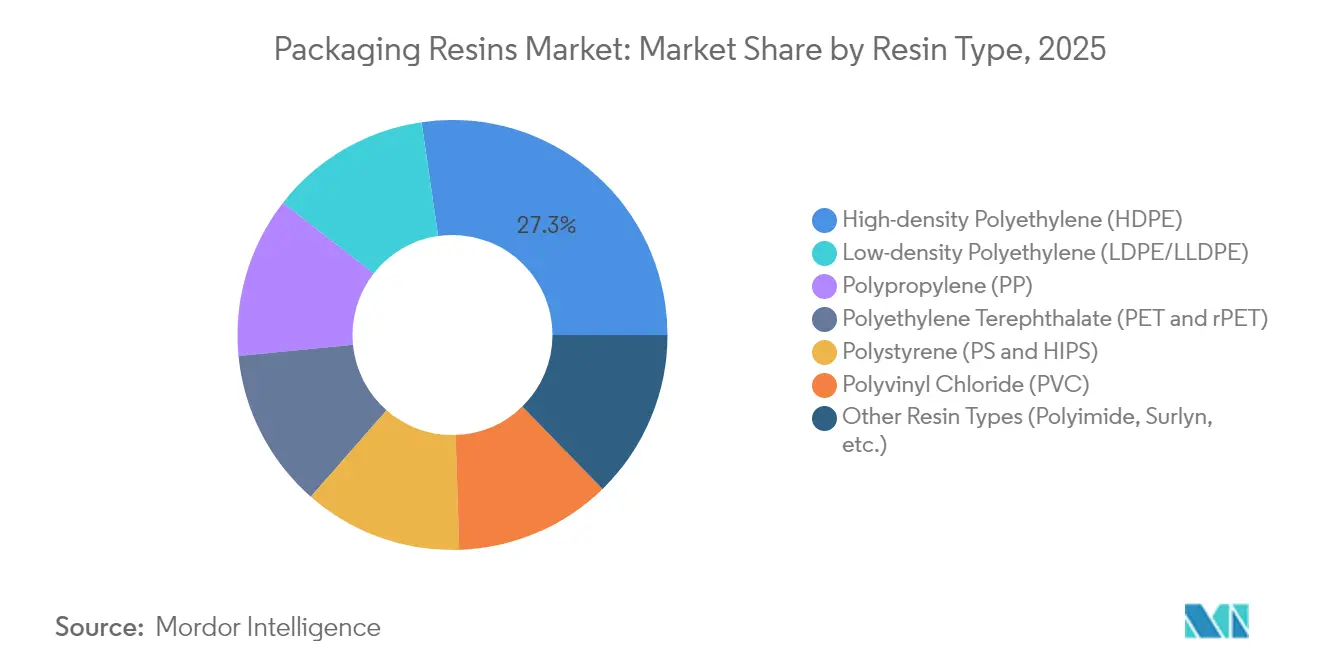

- By resin type, high-density polyethylene captured 27.30% of the packaging resins market share in 2025, while the “Other Types” category is forecast to expand at 6.32% CAGR through 2031.

- By application, food and beverage commanded 47.10% of the packaging resins market share in 2025; “Other Applications” are projected to grow fastest at 6.18% CAGR to 2031.

- By geography, Asia-Pacific held a 53.10% share of the packaging resins market size in 2025 and is advancing at a 5.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Packaging Resins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effectiveness & longer shelf-life | +1.20% | Global, with stronger impact in emerging markets | Medium term (2-4 years) |

| Booming e-commerce fulfilment volumes | +1.80% | North America & APAC core, spill-over to EU | Short term (≤ 2 years) |

| Increasing demand from food and beverage industry | +1.10% | Global, particularly APAC and Latin America | Long term (≥ 4 years) |

| Rise in phramaeuctical and healthcare packaging demand | +0.90% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Shift to mono-material packs for recyclability | +0.70% | EU core, expanding to North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-effectiveness & Longer Shelf-life

Packaging resins extend product freshness, cut waste, and reduce logistics losses by combining oxygen barriers with moisture resistance. Recent smart-packaging prototypes embed polyaniline and carbon nanodot sensors that detect ethanol and methanol generated during spoilage, delivering real-time condition alerts for perishable goods[1]Ahmed Maruf, “IoT-Enabled Biosensors in Food Packaging,” MDPI, mdpi.com . Industrials are scaling these resins for temperature-sensitive pharmaceuticals and functional food channels. AI-guided extrusion planning now tunes layer thickness to millimeter tolerances, curbing raw-material overuse and trimming unit cost. As high-value active ingredients increase, converters recast resin choice as a risk-mitigation lever rather than a commodity input. The resulting cost-of-ownership advantage sustains premium acceptance even when feedstock swings pressure margins.

Booming E-commerce Fulfillment Volumes

Online retail volumes drive structural shifts toward lighter, more protective packaging. Dimensional-weight shipping fees incentivize thin-wall pouches, while automation demands predictably stretch-resistant films. Resin formulators answer with higher-strength LLDPE blends and impact-modified polyolefins able to survive conveyor drops. Growth of paper mailers creates substitution risk, yet barrier-coating grades of polyolefin and EVOH preserve plastic usage even inside fiber-based formats. Single-serve portion packs flourish as consumers seek convenience, intensifying demand for resealable closures and peelable seals. The net impact is a broader mix of micro-applications, each requiring specific melt index and toughness profiles, sustaining volume momentum across diverse resin families.

Increasing Demand from Food & Beverage Industry

Regulations such as the EU Packaging and Packaging Waste Regulation and extended producer responsibility schemes force brand owners to back designs that combine recyclability with uncompromised barrier performance[2]Food Packaging Forum, “European Council Adopts Final PPWR Provisions,” foodpackagingforum.org . Investments like Tetra Pak’s USD 270 million aseptic technology upgrade demonstrate the capital intensity of staying compliant while leveraging ultra-high-temperature systems for shelf-stable dairy. Biodegradable and compostable resin innovations gain traction, yet require precise moisture management to avoid premature degradation. Smart-label integration—linking freshness indicators with cloud dashboards—creates incremental resin demand for electronics-compatible structures. Together, these shifts anchor steady volume growth despite saturated mature markets.

Rise in Pharmaceutical & Healthcare Packaging Demand

Moisture-resistant HDPE bottles, cyclic olefin copolymer vials, and blister films with desiccant layers protect high-value biologics and personalized therapies. North America sets sterile-pack trends as FDA guidelines tighten water-vapor-transmission thresholds, spurring upgrades across Asian supply chains. Sustainability goals run parallel: firms test recycled HDPE for non-contact secondary packs and evaluate bio-PE where traceability permits. Serialization mandates drive machine-readable printing on laminates, influencing resin surface-energy specifications. These combined technical hurdles underpin a robust growth premium for medical-grade polymers through the decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening regulations on plastic waste | -1.40% | EU core, expanding to North America and APAC | Medium term (2-4 years) |

| Feed-stock (naphtha/ethylene) price volatility | -0.80% | Global, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| PFAS scrutiny on fluorinated HDPE containers | -0.60% | EU core, expanding to North America, with early adoption in California and select US states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Regulations on Plastic Waste

The EU’s August 2026 cap of 25 ppb for individual PFAS in food packaging compels rapid material reformulation. Parallel state-level bans in California and New Mexico layer complexity on multinational supply chains, while India’s 30% recycled-PET mandate triggers 30% cost inflation for beverage fillers who struggle with limited r-PET supply. Extended producer responsibility statutes rolling out across the United States in 2025 will accelerate post-consumer take-back fees. Compliance spending diverts cash from expansion projects and narrows short-term margins, even as it catalyzes long-run innovation.

Feed-stock (Naphtha/Ethylene) Price Volatility

Naphtha and propylene swings distort resin cash-cost curves; unplanned cracker outages coupled with prospective 25% tariffs on Canadian and Mexican imports drove a March 2025 spike in PE and PP contract prices. U.S. polymer-grade propylene is projected to rise further as LyondellBasell’s refinery exit tightens supply. In Asia, sub-economic spreads forced several Southeast Asian crackers offline, demonstrating margin fragility when crude tracks upward. Hedging programs and flexible sourcing partially cushion volatility, yet converters still face quoting challenges on multi-year supply contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: HDPE Leadership Amid Specialty Growth

High-density polyethylene sustained the largest 27.30% packaging resins market share in 2025, with demand anchored in blow-molded food containers, jerrycans, and pharma bottles. Growth persists as recyclate availability improves, aligning with corporate recycled-content pledges. “Other Types” register the fastest 6.32% CAGR, reflecting scaling of polyimide, ionomer, and cyclic-olefin copolymer lines tailored to high-barrier, retortable, and easy-seal formats. Polypropylene extends penetration in caps and medical devices, while PET faces mixed fortunes—benefiting from recycling infrastructure yet constrained by bottle-to-bottle mandates that divert supply. Polyvinyl chloride remains niche in non-food blister packs due to chlorine-related disposal issues. Bio-PE capacity, expanded 30% by Braskem to 260,000 tons, affirms commercial-scale renewable feedstock pathways. Advanced recycling plants such as ExxonMobil’s Baytown unit, targeting 1 billion lb/year by 2027, promise new circular feedstreams.

The packaging resins market for HDPE-based rigid packs demonstrates steady growth potential, supported by increasing demand across high-value applications. Product developers couple multi-layer downgauging with compatibilizers that enable mono-material recovery, an approach boosting post-consumer recycling rates and ensuring compliance with 2030 recyclability pledges. Equipment retrofits unlock run-rate flexibility, and the migration to all-electric injection presses cuts energy use, strengthening HDPE cost leadership. Specialty grades command premium pricing that offsets lower volumes; niche opportunities in odor-barrier and radiation-resistant films lift gross margins for innovators.

By Application: Food & Beverage Dominance with E-commerce Surge

Food and beverage maintained a commanding 47.10% packaging resins market share in 2025, safeguarded by indispensable requirements for hygiene and regulatory adherence. Shelf-stable dairy, ready-to-eat meals and carbonated beverages rely on precise oxygen- and CO₂-barrier properties that favor multilayer PET and EVOH-lined PE.

“Other Applications” encompassing e-commerce fulfillment, protective industrial wraps and returnable transport packaging will grow at 6.18% CAGR, fueled by omnichannel retail logistics and automation trends. Dimensional-weight fee structures push designers toward tear-resistant thin films and bubble-cushion laminates based on tougher LLDPE. Smart labels equipped with NFC chips to authenticate cosmetics and personal-care packs stimulate demand for resins that accept stable conductive inks. Healthcare maintains steady up-trend as biologics pipelines expand, while industrial chemical drums adopt cross-linked HDPE to satisfy UN dangerous-goods norms. Growing adoption of hybrid paper-plus-barrier-resin designs underscores the shift from primary plastic pack to functional coating layer, further diversifying application pathways.

Geography Analysis

Asia-Pacific controlled 53.10% of global demand in 2025 and will accelerate at 5.95% CAGR through 2031, a dual dominance rooted in cost-effective manufacturing and swelling domestic consumption. China’s 362 million-ton virgin resin output in 2022 cemented its global supply influence, yet profitability has thinned, prompting several crackers to idle or defer expansion. India’s rigid-pack boom—serving food, beverage and personal care—is propelled by urbanization and rising income, though extended-producer-responsibility rules push brand owners toward recyclable laminates. Southeast Asian makers grapple with negative spreads, but long-term fundamentals remain intact due to proximity to growth markets.

North America shows moderate growth but high innovation density. Analysts forecast headwinds for polyethylene and polypropylene until 2026 because of capacity overhang and feedstock uncertainty. Investments such as ExxonMobil’s advanced-recycling expansion and LyondellBasell’s 400,000-t propylene unit reflect strategic bets on differentiation rather than volume plays. Canada and Mexico face potential tariff disruptions that would recalibrate continental trade flows.

Europe balances tight regulation with technology leadership. The Packaging and Packaging Waste Regulation drives mono-material adoption, while high recycling rates in Denmark and Austria reinforce downstream demand for washed flakes. SABIC’s 135 product launches in 2024 and pilot chemical-recycling ventures show incumbents aligning portfolios with circular-economy policy. The Netherlands targets fossil-free packaging by 2050, intensifying R&D in bio-polymers. South America and Middle East & Africa collectively record rising demand from urbanization and e-commerce penetration; Brazil leads regional uptake, and Saudi Arabia leverages feedstock advantage for export-oriented PE and PP.

Competitive Landscape

The packaging resins market is moderately fragmented but moving toward consolidation. Q2 2024 logged 60 M&A deals, up 9.10% YoY, signaling renewed appetite for bolt-on acquisitions even as total invested capital fell 85% to USD 0.38 billion amid higher funding costs. Competitive intensity varies across sub-sectors. Pharmaceutical and healthcare grades enjoy margin insulation due to stringent qualification barriers; ExxonMobil’s Exact resin series and Borealis’ BorPure range command price premiums.

Commodity film markets remain price sensitive, with Asian overcapacity weighing on spot quotes. Strategic differentiation now centers on circular offerings: SABIC’s Trucircle PCR-based PP, Braskem’s I'm Green bio-PE, and Dow’s bio-ethylene supply pact with New Energy Blue are high-profile initiatives. Technology adoption is another lever—IoT-enabled smart packaging alliances create novel revenue streams beyond resin tonnage, and early movers in chemical recycling expect license fees as a future profit pool.

Packaging Resins Industry Leaders

China Petrochemical Corporation. (Sinopec)

Dow

Exxon Mobil Corporation

LyondellBasell Industries Holdings B.V.

SABIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: LyondellBasell plans to expand propylene production at its Channelview Complex near Houston. Construction is scheduled to begin in Q3 2025, with operations starting by late 2028. The unit will produce approximately 400 thousand metric tons of propylene annually, strengthening the company's position in the market through its use in food packaging.

- May 2023: Dow and New Energy Blue have signed a long-term supply agreement in North America. New Energy Blue will produce bio-based ethylene from renewable agricultural residues, which Dow will purchase to lower carbon emissions in plastic production and support recyclable packaging applications.

Global Packaging Resins Market Report Scope

The packaging resins market is segmented by resin type, application, and geography. By resin type, the market is segmented into high-density polyethylene, low-density polyethylene, polyethylene terephthalate, polypropylene, polystyrene, polyvinyl chloride, and other resin types. By application, the market is segmented into food and beverage, consumer goods, cosmetics and personal care, healthcare, industrial, and other applications. The report also covers the market size and forecasts for the packaging resins market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (million metric tons).

| High-density Polyethylene (HDPE) |

| Low-density Polyethylene (LDPE/LLDPE) |

| Polyethylene Terephthalate (PET and rPET) |

| Polypropylene (PP) |

| Polystyrene (PS and HIPS) |

| Polyvinyl Chloride (PVC) |

| Other Resin Types (Polyimide, Surlyn, etc.) |

| Food and Beverage |

| Consumer Goods |

| Cosmetics and Personal Care |

| Healthcare |

| Industrial |

| Other Applications (E-commerce Mailers and Protective Wrap, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin Type | High-density Polyethylene (HDPE) | |

| Low-density Polyethylene (LDPE/LLDPE) | ||

| Polyethylene Terephthalate (PET and rPET) | ||

| Polypropylene (PP) | ||

| Polystyrene (PS and HIPS) | ||

| Polyvinyl Chloride (PVC) | ||

| Other Resin Types (Polyimide, Surlyn, etc.) | ||

| By Application | Food and Beverage | |

| Consumer Goods | ||

| Cosmetics and Personal Care | ||

| Healthcare | ||

| Industrial | ||

| Other Applications (E-commerce Mailers and Protective Wrap, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the packaging resins market?

The packaging resins market size reached 164.69 million tons in 2026 and is projected to grow to 210.67 million tons by 2031.

Which region leads the packaging resins market?

Asia-Pacific leads with 53.10% share in 2025 and is also the fastest-growing region at 5.95% CAGR through 2031.

Which resin type dominates global demand?

High-density polyethylene holds the largest packaging resins market share at 27.30% thanks to its versatility across rigid and flexible formats.

How are regulations influencing material choices?

Mandated recycled-content thresholds, PFAS restrictions and extended producer responsibility laws are steering converters toward mono-material, recyclable and bio-based resins, accelerating innovation.

What drives growth in pharmaceutical packaging resins?

Strict sterility standards, serialization requirements and the rise of personalized medicines are boosting demand for moisture-barrier and traceable resin grades in healthcare packaging.

How is e-commerce affecting resin demand?

Online retail increases volume needs for lightweight, impact-resistant packaging and spurs development of smart films compatible with high-speed automation, pushing specialty resin consumption upward.

Page last updated on: