Resin Capsule Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

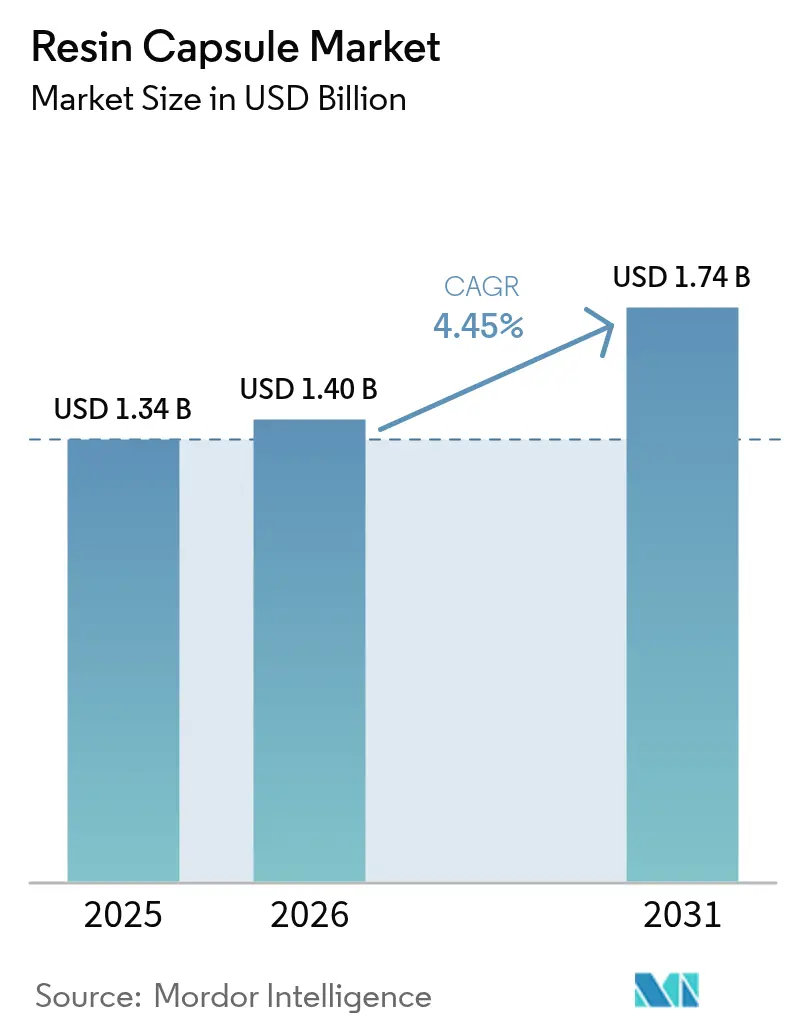

| Market Size (2026) | USD 1.4 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resin Capsule Market Analysis by Mordor Intelligence

The Resin Capsule Market size was valued at USD 1.34 billion in 2025 and estimated to grow from USD 1.4 billion in 2026 to reach USD 1.74 billion by 2031, at a CAGR of 4.45% during the forecast period (2026-2031). Rising mechanized underground mining, rapid metro-rail tunnel construction, and stricter anchorage standards in high-rise retrofits continue to fuel adoption of resin-anchored rock bolts and post-installed rebar. Automated drilling platforms that impose heavier dynamic loads than manual operations, expanding metro networks in Asia and Europe, and tighter seismic design codes together reinforce demand for chemical anchoring solutions that distribute stress more evenly than expansion fasteners. Environmental policy is an additional growth lever, accelerating the shift from high-VOC styrene capsules toward water-based or bio-based systems. Competitive rivalry is intensifying as leading multinationals consolidate regional players to broaden product portfolios and geographic reach.

Key Report Takeaways

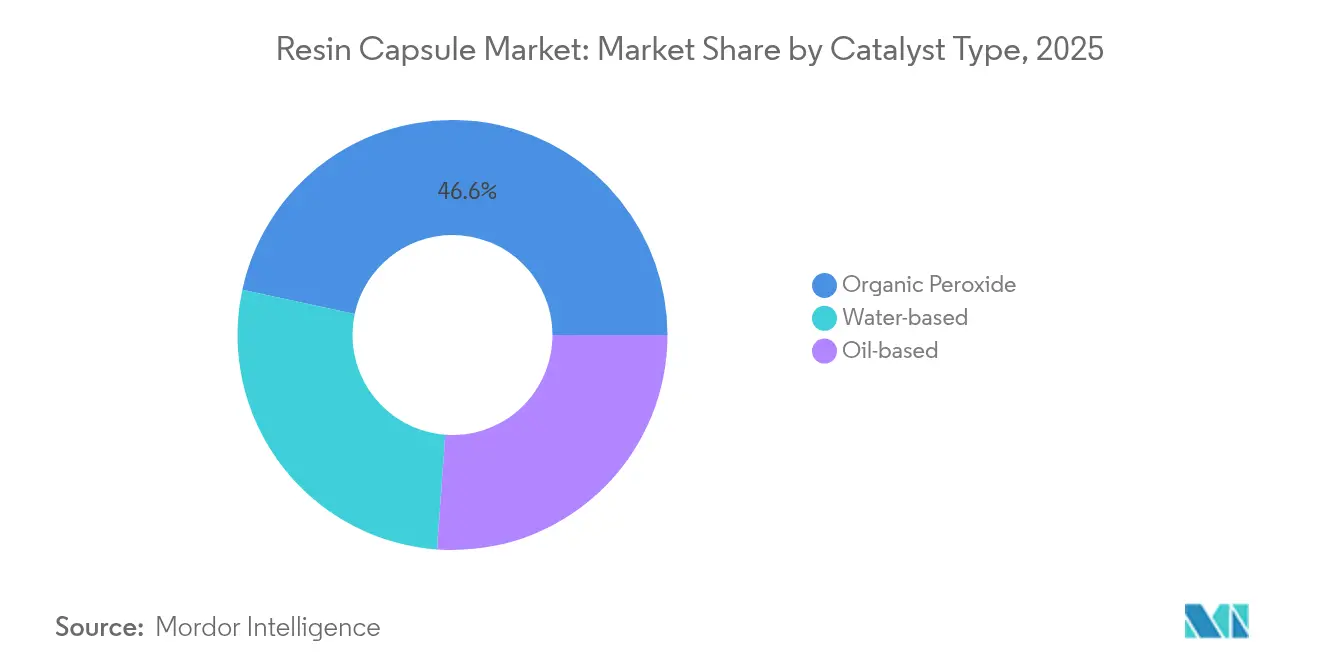

- By catalyst type, organic peroxide systems retained 46.62% share in 2025, whereas water-based catalysts are growing at 4.78% CAGR.

- By resin type, polyester held 39.92% revenue in 2025, while bio-based and other alternatives are forecast to rise at 4.83% CAGR.

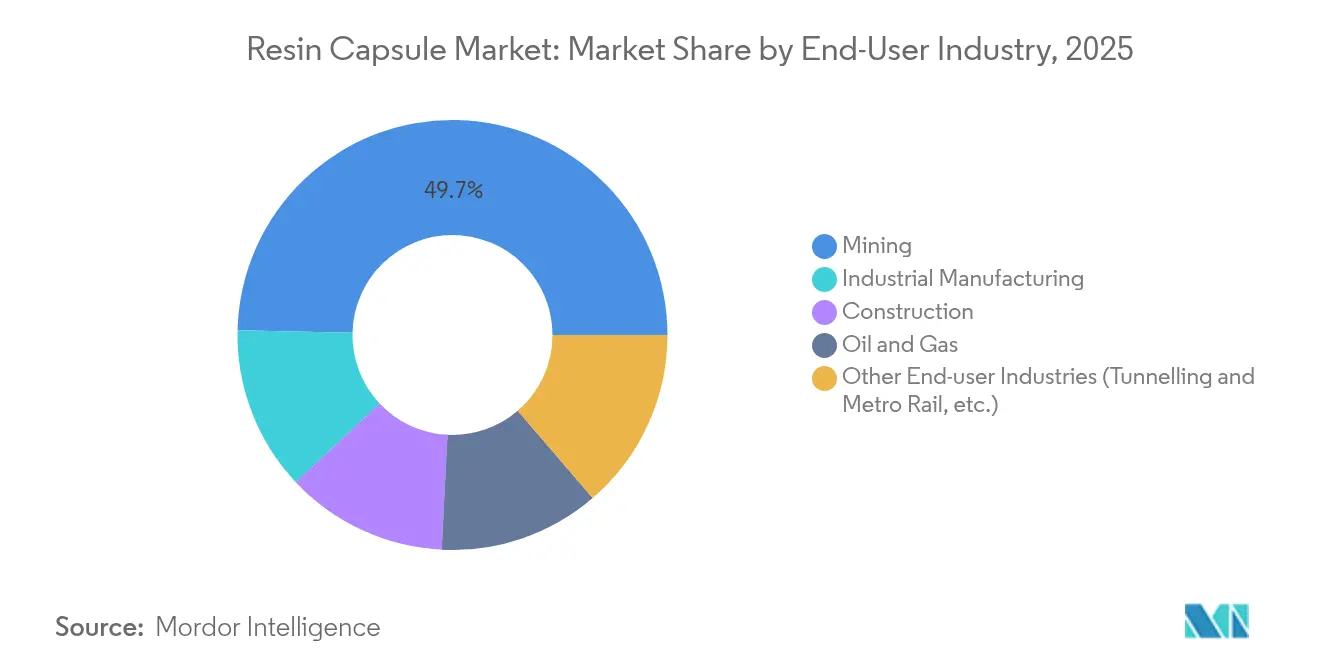

- By end-user industry, mining accounted for 49.65% of resin capsule market share in 2025, while tunnelling and metro rail is projected to expand at 5.03% CAGR through 2031.

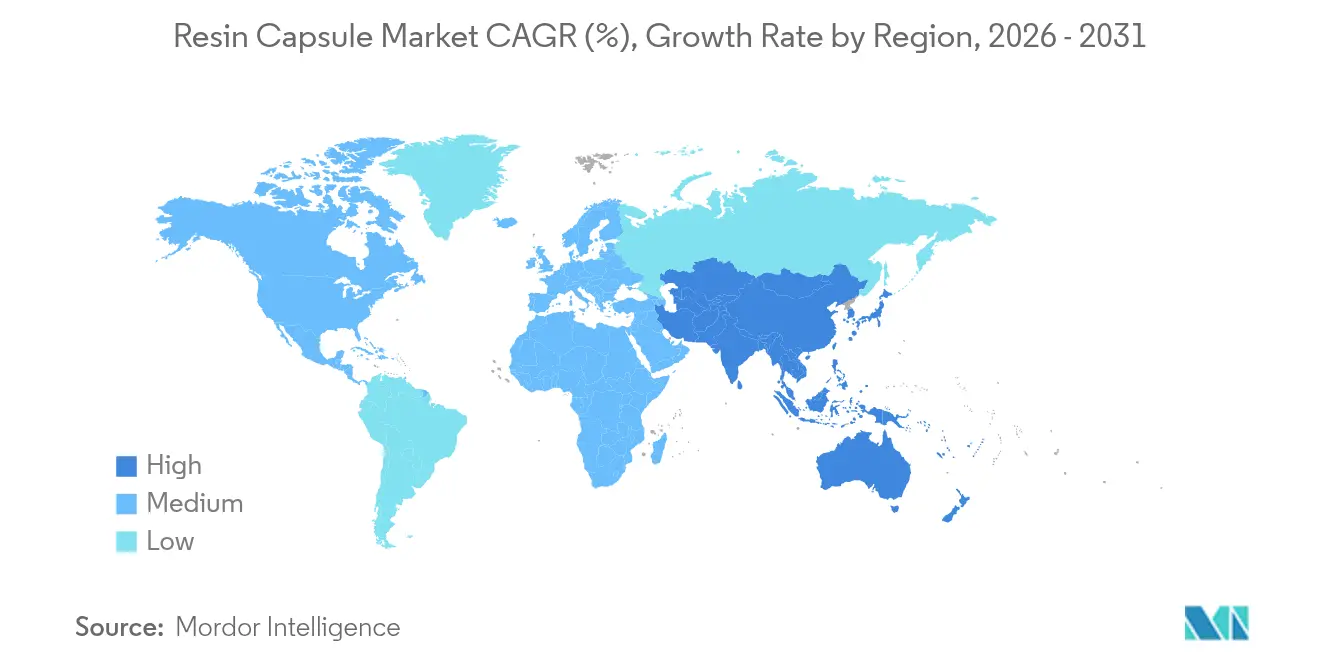

- By geography, Asia-Pacific commanded 45.12% revenue share in 2025; the same region is advancing at the fastest 4.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Resin Capsule Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mechanised underground mining | +1.2% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Tighter anchorage standards in high-rise and bridge retrofits | +0.8% | North America & EU, expanding to APAC urban centers | Long term (≥ 4 years) |

| Rapid metro rail tunnel construction in Asia and Europe | +0.9% | APAC core, spill-over to MEA and South America | Short term (≤ 2 years) |

| Digital mine planning enabling thinner pillar designs | +0.6% | Global, early adoption in developed mining regions | Medium term (2-4 years) |

| Shift to low-exotherm bio-based catalysts reducing downtime | +0.4% | EU and North America leading, gradual APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Mechanized Underground Mining

Automated coal, copper, and hard-rock operations increasingly rely on resin-anchored bolts that withstand higher cyclical loads than mechanical alternatives. Sandvik’s intelligent long-hole rigs integrate real-time torque monitoring, optimizing bolt placement and capsule usage[1]“Sandvik Drills Reach New Depths,” Mining Weekly, miningweekly.com . Battery-electric loaders further tighten excavation cycles, raising instantaneous roof stress that chemical anchors accommodate through homogeneous bond lines. As capital-intensive mines target deeper seams, end-users prioritize fast-curing resins that minimize development downtime.

Tighter Anchorage Standards in High-Rise and Bridge Retrofits

Post-installed rebar design guides now specify adhesive connections for seismic and wind-load resistance, citing 120-year service-life certifications for many epoxy systems. Updated bridge codes emphasize load distribution over larger concrete volumes, favoring chemical anchors that mitigate progressive pull-out failures. Regulatory authorities in the United States and European Union publish acceptance criteria that limit expansion fasteners for high-consequence retrofit work, translating directly into higher resin capsule demand.

Rapid Metro Rail Tunnel Construction in Asia and Europe

Chengdu’s Metro Line 6 pipe-jacking under existing shield tunnels illustrates the complex loading environments that push project specifiers toward resin capsules capable of curing in water-filled holes. GIS-aided alignment planning enables precise anchor layout, maximizing segment stability with fewer bolts. European city tunnels increasingly mandate styrene-free capsules to protect confined-space workers, accelerating the uptake of water-based catalyst systems.

Digital Mine Planning Enabling Thinner Pillar Designs

Modern CAD-GIS suites model rock deformation with high fidelity, allowing engineers to shrink pillar width while preserving safety through denser resin-anchored support grids. Closer bolt spacing increases capsule consumption per meter of advance, converting design sophistication into material demand. Temporary robotic support systems coordinate with digital plans, placing bolts rapidly in pre-programmed patterns that favor capsule consistency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in epoxy and polyester feedstock prices | -0.7% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Strict VOC limits on styrene-based capsules | -0.5% | EU and North America, expanding to APAC | Medium term (2-4 years) |

| Skilled-installer shortage driving anchor failures | -0.3% | Global, particularly acute in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Epoxy and Polyester Feedstock Prices

Antidumping duties on Asian epoxy resin imports into the United States amplify price swings and extend lead times for capsule producers[2]“Epoxy Resin From Korea, Taiwan and Thailand,” U.S. International Trade Commission, usitc.gov. Disruptions at upstream petrochemical plants ripple through polyester supply, prompting contractors to hedge inventory or negotiate escalation clauses. Small and mid-size applicators face liquidity strain when input costs spike without immediate pass-through.

Strict VOC Limits on Styrene-Based Capsules

Regional air-quality rules cap construction chemical emissions at progressively lower thresholds, effectively phasing out high-styrene formulations in many states and EU nations. Compliance requires reformulation toward epoxy-acrylate or pure epoxy chemistries, raising R&D expenses. Installers must adopt new handling protocols, adding indirect costs that temper near-term uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Catalyst Type: Water-Based Systems Gain Environmental Edge

Organic peroxide products kept 46.62% revenue in 2025 on legacy adoption within hard-rock and infrastructure applications. Water-based catalysts, however, are rising at 4.78% CAGR, propelled by REACH compliance and confined-space safety mandates. Silver- and bismuth-activated blends shorten cure cycles at lower exotherm, supporting higher advance rates in tunneling operations. Oil-based variants continue serving general construction but show minimal share shift.

Innovation across all families aims to widen temperature windows and extend shelf life. Suppliers are integrating QR-code traceability that links capsule production data to installation logs, aligning with digital quality-assurance workflows.

By Resin Type: Bio-Based Alternatives Challenge Polyester Dominance

Polyester maintained 39.92% revenue in 2025 owing to cost advantages across standard applications. Yet bio-based epoxy and acrylic systems are growing 4.83% CAGR as asset owners apply embodied-carbon reporting to procurement. Commercial launches such as Henkel LOCTITE HB S ECO cut CO₂ emissions by 60% while retaining structural integrity. Cardanol-derived vitrimers add self-healing benefits and recyclability, aligning with circular-economy targets.

Epoxy remains indispensable for extended-service anchors in marine and seismic zones, though supply volatility encourages dual-sourcing with vinyl ester or acrylics. Resin formulators are experimenting with flame-retardant bio-fillers to broaden tunnel applications subject to stringent fire codes.

By End-User Industry: Tunnelling Segment Accelerates Past Mining

Mining dominated 49.65% revenue in 2025 as deep coal and metal operations require dense resin-anchored support. The tunnelling and metro-rail niche, however, is climbing 5.03% CAGR on record project backlogs in Asia and Europe. Complex shield excavations under urban utilities demand capsules that cure in water and accommodate cyclic train vibrations.

Industrial construction and oil-and-gas remain steady consumers, prioritizing corrosion-resistant formulations for chemical plants and offshore jackets. Infrastructure-heavy economies directing stimulus toward subways and bridges will continue to tip demand toward tunnelling anchors through 2031.

Geography Analysis

Asia-Pacific’s 45.12% command in 2025 reflects heavy infrastructure pipelines and rapid mechanization across Chinese and Indian underground mines. Adoption of 3D geological mapping allows precision anchor layouts that optimize resin usage. Japan’s stringent quality codes spur higher-value epoxy capsule demand, whereas ASEAN nations represent volume growth through metro rail and hydropower tunneling.

North America is a mature resin capsule market driven by bridge rehabilitation and high-rise seismic upgrades, both of which value long-life epoxy systems certified for 120 years. The antidumping verdict on Asian epoxy imports has tightened domestic supply, raising prices but accelerating R&D into alternative resin chemistries.

Europe balances retrofit demand with green-chemistry adoption. REACH restrictions push contractors toward water-based catalysts, stimulating supplier innovation. The region’s high share of mechanized tunneling under historic city centers further elevates capsule volumes.

South America and Middle East & Africa show uneven spending cycles yet present upside where large mining or mega-project activity coincides with international financing tied to performance-based anchor specifications. Building local installer competence remains a prerequisite for sustained demand.

Regulatory Landscape

The regulatory environment for resin capsules is tightening around chemical safety, emissions, and verified anchor performance in mining and civil construction. In the European Union, Commission Regulation (EU) 2026/1168 amended REACH (Regulation (EC) No 1907/2006) to further restrict synthetic polymer microparticles in mixtures and products, strengthening formulation and documentation requirements for capsule chemistries and additives. In parallel, civil-engineering chemical anchors often rely on third-party approvals such as European Technical Assessments (for example, ETA-05/0164 and ETA-21/0948 for systems used in cracked and non-cracked concrete), which increases lot traceability, defined cure behavior, and standardized test evidence at the project-spec level.

Mining jurisdictions are also codifying resin-anchored rock support requirements through national and group standards. China issued MT/T 146-2025 for resin-anchor bolts (effective 30 December 2025), and group standard T/HEBQIA 530-2026 sets technical specifications for mine-resin rock bolt anchors, including chemical composition and setting-time requirements. India references mine safety guidance (DGMS) that uses performance thresholds such as achieving compressive strength above 40 MPa within 24 hours for roof-bolting integrity, raising the role of certified testing and installation quality controls alongside product compliance.

Value Chain Analysis

The resin capsule value chain begins with upstream petrochemical and specialty-chemical inputs, primarily polyester, epoxy, and acrylic resins, together with catalysts (organic peroxide, oil-based, and water-based systems) and performance additives that control thixotropy, temperature window, and exotherm. These materials are compounded into two-compartment capsules (resin mastic and catalyst) within a frangible sheath, paired with external packaging materials (commonly polythene), and then subjected to in-process QC for viscosity, fill ratio, gel time, and shelf-life stability.

Midstream production and downstream delivery are shaped by hazardous-material handling and the need for consistent field performance in mechanized bolting and post-installed rebar. Manufacturers and integrated solution providers, including mining and tunneling consumables suppliers and equipment OEM ecosystems, distribute through direct contracts with mines and large infrastructure contractors, as well as through construction-channel distributors for civil anchoring. Key bottlenecks include feedstock price volatility in epoxy and polyester, plus logistics constraints for regulated chemicals, so regional manufacturing footprints and tightly managed inventory programs are used to reduce lead-time risk, especially for high-turn mining operations and metro-rail tunneling projects where curing windows and installation repeatability are contract-critical.

Competitive Landscape

The resin capsule market is moderately concentrated. Sika’s USD 5.5 billion acquisition of MBCC Group broadened its product family into specialty underground resins and expanded presence in North America and Asia.

Hilti pushes adoption of its SafeSet system, integrating volume calculators and smart dispensers that reduce installation variability. Sandvik embeds anchor-validation sensors into drilling cycles, bundling consumables with equipment to lock in recurring revenue. Regional manufacturers differentiate through custom curing windows and lower price points, particularly in India and China.

Technology partnerships emerge around bio-based feedstocks and low-exotherm catalysts, with universities and start-ups supplying novel polymers. Intellectual-property barriers remain moderate, prompting frequent licensing and joint-development agreements.

Resin Capsule Industry Leaders

Hilti

Koelner Rawlplug IP

Minova

Sandvik AB

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product whitespace is concentrated in low-emission and worker-safety formulations that still meet demanding anchor performance in confined spaces and water-bearing drill holes. Styrene-free and water-based catalyst systems align with REACH-driven chemical scrutiny and tunnel jobsite requirements, and they also support procurement criteria that increasingly call for documented exposure reduction and standardized test evidence rather than supplier self-declaration. Technical differentiation opportunities are also visible in formulations engineered for mechanized installation, including thixotropic compounds for overhead use and controlled low-exotherm curing to reduce downtime in high-cycle mining and metro-rail tunneling.

Manufacturing and installation automation creates another opportunity layer because capsule consistency and digital QA fit the shift toward automated drilling and bolting platforms. Sandvik has commercialized automation around resin handling and installation (including Automatic Resin Injection, alongside styrene-free capsule introductions), while suppliers such as Sinostone market fully automatic resin capsule production lines that target standardized, high-throughput output. At the same time, upgrades in acceptance and third-party testing practices for structural fixings, including expanded pull-out testing protocols used in transportation infrastructure oversight, favor suppliers that can provide traceable batches, documented cure profiles, and application-specific approvals for cracked concrete, seismic retrofit, and heavy-load anchoring.

Recent Industry Developments

- January 2026: Sika launched its Fast Forward investment and efficiency program focused on production network optimization and digital value chain transformation, with a CHF 80 million savings target for 2026. The initiative supports competitiveness for chemical anchoring and construction-chemicals portfolios by improving manufacturing efficiency and enabling more standardized, traceable production and supply planning across regions.

- March 2025: Minova completed the acquisition of Platipus Anchors, adding a portfolio that includes resins, grouts, and membranes. The combination broadens Minova's ground-support offering and provides cross-selling potential in mining and civil anchoring applications where chemical bonding systems are specified alongside mechanical anchoring solutions.

- September 2024: Sandvik introduced new underground ground-support solutions including the Fasloc SF styrene-free resin capsule and an updated ARI (Automatic Resin Injection) system for automated resin capsule installation. The styrene-free launch addresses confined-space health requirements while the ARI update strengthens Sandvik's equipment-plus-consumables workflow, reinforcing repeatable installation quality in mechanized mining operations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the resin capsule market covers pre-measured, encapsulated resin systems used to anchor bolts, rebars, and similar supports in drilled holes across construction, mining, and related industrial installations. The sizing captures sales value at the market level across key resin and catalyst systems used for this purpose.

Scope exclusions: We exclude non-capsule chemical anchoring formats (such as bulk cartridges and injection grouts), along with mechanical anchors and pure cement-based anchoring materials.

Segmentation Overview

- By Catalyst Type

- Organic Peroxide

- Oil-based

- Water-based

- By Resin Type

- Polyester

- Epoxy

- Acrylic

- Other Resin Types (Vinyl Ester, Bio-based, etc.)

- By End-User Industry

- Mining

- Industrial Manufacturing

- Construction

- Oil and Gas

- Other End-user Industries (Tunnelling and Metro Rail, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with setting clear counting rules for what qualifies as a resin capsule sale in each end use, then building a demand view that can be defended country by country. We rely on public and official references, including mining production releases from agencies such as USGS, construction output indicators from sources such as the World Bank, customs trade statistics where available, and standards and guidance notes from bodies such as ISO and OSHA that shape anchoring practices.

Next, we cross-check market structure using company annual reports, investor presentations, product catalogs, and credible press coverage to understand where demand comes from. To reduce blind spots in cross-border flows, we also review import and export shipment-level records through a paid database subscription, and patent databases are used to confirm resin chemistry direction and curing system trends. These desk sources are illustrative only, and many other references were also used for collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with manufacturers, distributors, contractors, mine operators, and engineering teams that specify anchoring systems. Because demand ties to project cycles, we tested capsule usage per installation with respondents across APAC, EMEA, and the Americas, and we also checked resin type preferences and how pricing changes get passed through to downstream buyers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 42% |

| Mid tier: 45% | Functional/Unit leaders: 30% | EMEA: 34% |

| Smaller Players: 16% | Managers: 54% | Americas: 24% |

Market-Sizing & Forecasting

The core sizing logic is built top-down by reconstructing the demand pool from underground and surface mining activity, tunneling and metro build-outs, and construction anchoring intensity, then applying resin capsule penetration rates where this format is commonly specified. After the demand spine is set, the totals are corroborated with selective bottom-up approximations, including sampled price per capsule and consumption per installation, distributor channel checks, and partial supplier roll-ups in priority countries.

Inputs used in the model include mining development and production trends, tunnel project pipelines, construction and infrastructure spending direction, typical bolt and rebar anchoring patterns by application, and observable price movements tied to resin and catalyst systems that influence selling prices. When a country has limited direct visibility, we fill the gap using proxy indicators such as project counts and mining output mixes, then adjust with interview-backed conversion factors so the estimates stay practical.

For forecasting, scenario analysis is used around mining capex cycles and infrastructure project timing, and it is combined with simple regression relationships between activity indicators and resin capsule consumption. Assumptions on penetration and pricing are refreshed using primary feedback so the outlook reflects how specifications and procurement behavior are expected to evolve.

Data Validation & Update Cycle

Validation is handled through multiple checks that look for consistency across geography, end use, and pricing. We compare model outputs against independent signals such as mining output trends, major tunneling project pipelines, and trade patterns, and then investigate variances that fall outside reasonable ranges before the numbers are finalized.

A second analyst review is completed for key assumptions such as penetration rates, application splits, and price progression, so calculation errors and logic breaks are caught early. Reports are refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major mining slowdowns, sharp resin feedstock moves, or large infrastructure program changes. Before delivery, an analyst performs a fresh review pass so clients receive an up-to-date view aligned to the latest available indicators.

Mordor Intelligence's Resin Capsule Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for resin capsules because publishers do not always count the same product forms, end uses, and timing of pricing, even when the market name looks identical. Differences also come from the year selected as the reference point and whether the estimate leans toward conservative or aggressive adoption assumptions.

Some published figures can look higher when bulk chemical anchoring formats or closely related adhesives are included alongside capsules, or when pricing is carried forward using broad chemical inflation without application-level checks. For Mordor Intelligence, only encapsulated resin capsule systems are counted, and the yearly values are tied back to mining development, tunneling starts, and construction anchoring activity that were rechecked through recent interviews.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.34 B (2025) | |

| Global Consultancy A | USD 1.20 B (2024) | Uses a different base year and may not fully reflect the 2025 shift in mining development and tunneling starts, which changes the implied mix and realized pricing used in the total. |

| Industry Publisher B | USD 1.05 B (2024) | Lower total is consistent with narrower end-use capture and conservative penetration assumptions for capsule anchoring in construction retrofits, plus limited adjustment for application-level price differences. |

Taken together, the spread is mainly explained by year alignment, what is counted as a resin capsule sale versus adjacent chemical anchors, and how adoption is translated from activity into volumes. When these drivers are made explicit and then checked with real-world usage patterns, the final number becomes easier to trace and update without reworking the full model.

Key Questions Answered in the Report

What is the projected size of the resin capsule market by 2031?

The resin capsule market size is expected to reach USD 1.74 billion by 2031.

Which region leads the resin capsule market in both share and growth?

Asia-Pacific leads with 45.12% revenue in 2025 and posts the fastest 4.92% CAGR through 2031.

Why are water-based catalyst systems gaining popularity in resin capsules?

Environmental regulations that cap VOC emissions and safety requirements in confined spaces drive adoption of water-based catalysts growing at 4.78% CAGR.

Which end-user segment is expanding the fastest?

Tunnelling and metro rail applications show the highest 5.03% CAGR due to urban subway expansions.

Page last updated on: