Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

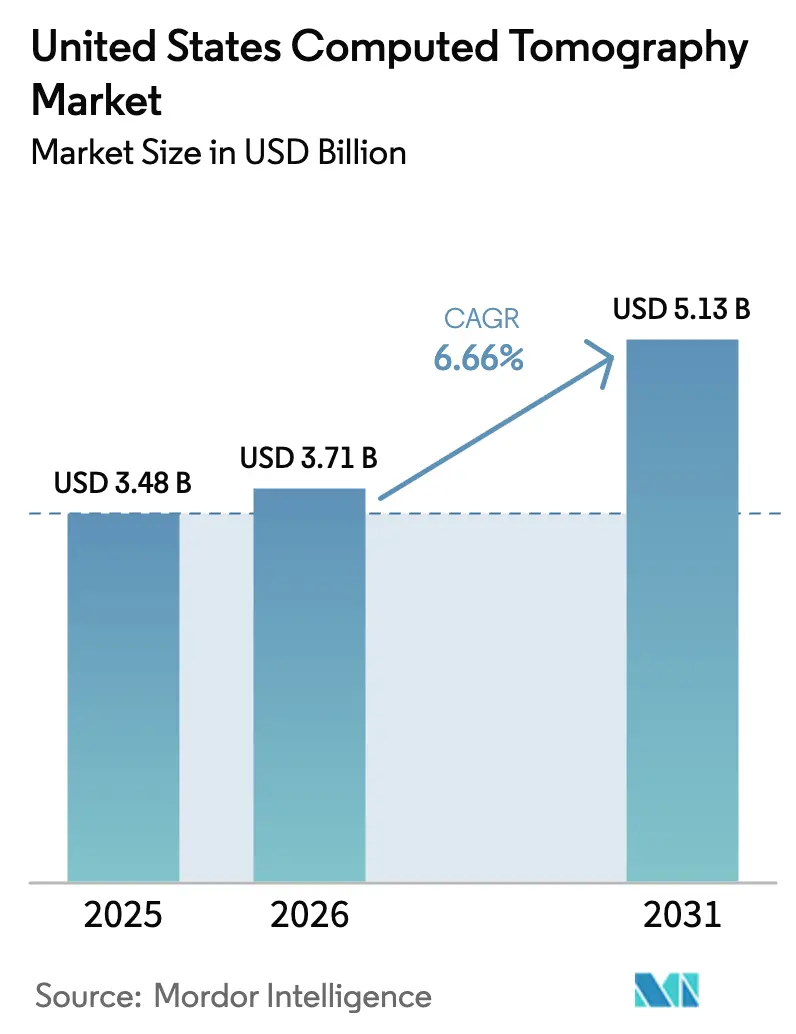

| Base Year Market Size (2025) | USD 3.48 Billion |

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 5.13 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Computed Tomography Market Analysis by Mordor Intelligence

The United States computed tomography market size is expected to grow from USD 3.48 billion in 2025 to USD 3.71 billion in 2026 and is forecast to reach USD 5.13 billion by 2031 at 6.66% CAGR over 2026-2031. A sharp rise in multimorbidity, continuous breakthroughs in detector design, and swift outpatient migration are combining to elevate scanner utilization across hospitals and freestanding imaging centers [1]Centers for Disease Control and Prevention, “Behavioral Risk Factor Surveillance System,” cdc.gov . Photon-counting platforms are moving from pilot deployments to routine service, while mobile units are becoming integral to trauma and critical-care workflows. Competitive intensity is climbing as original-equipment manufacturers embed artificial intelligence in scanners and reporting software to offset staff shortages and reimbursement pressures. Providers are also pursuing regional growth in the Sun Belt and Mountain West, where population inflows of older adults are heightening demand for advanced cardiac and oncologic imaging.

Key Report Takeaways

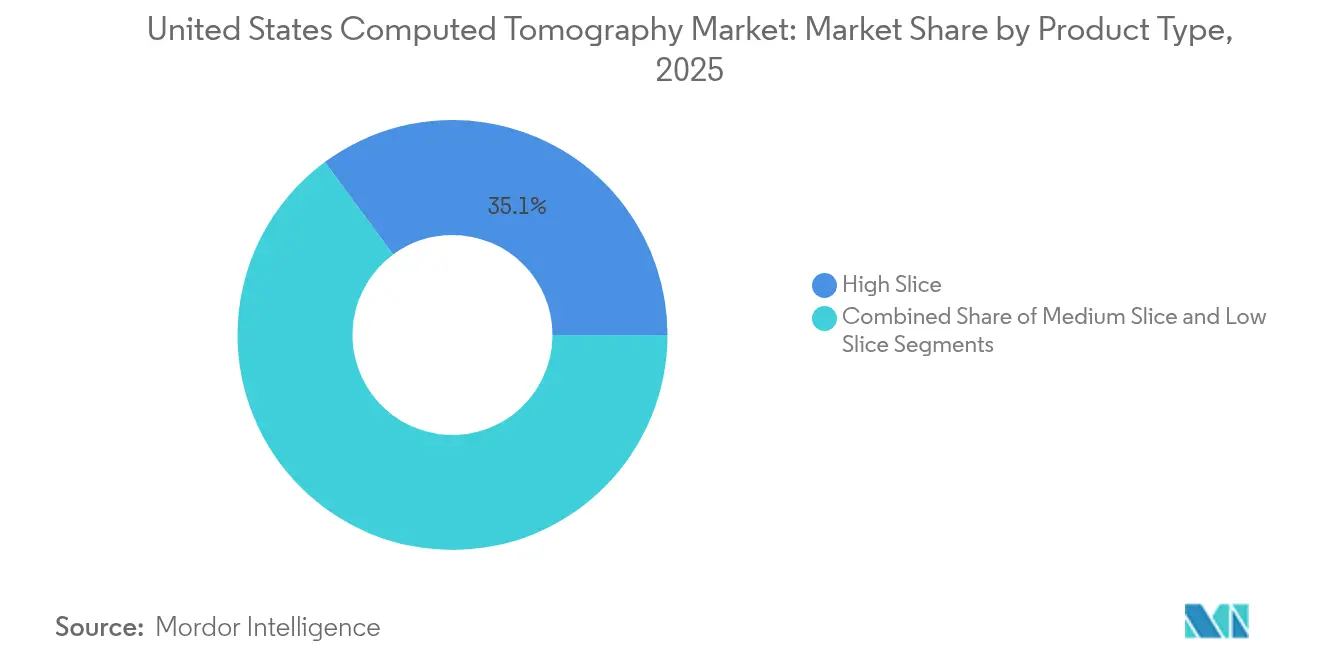

- By product type, high-slice systems led with 35.12% of the computed tomography market share in 2025, whereas medium-slice systems are poised for the fastest expansion at 7.53% CAGR through 2031.

- By application, oncology dominated with 33.05% revenue share in 2025; neurology is projected to rise at a 7.44% CAGR to 2031.

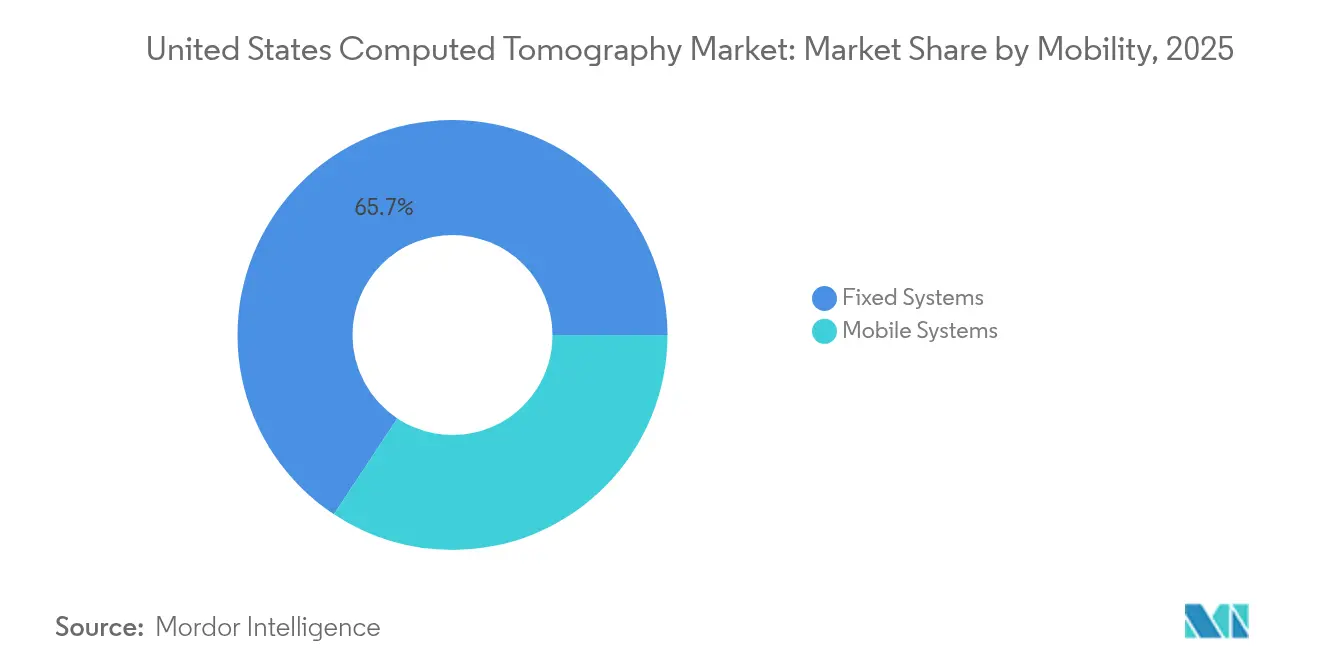

- By mobility, fixed platforms accounted for 65.70% of the computed tomography market size in 2025, yet mobile systems are advancing at a 7.46% CAGR.

- By end user, hospitals held 48.60% of the computed tomography market size in 2025, while diagnostic imaging centers are set for a 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Computed Tomography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +1.8% | Global, concentrated in aging metropolitan areas | Long term (≥ 4 years) |

| Growing geriatric population | +1.5% | National, with early gains in Sun Belt states | Long term (≥ 4 years) |

| Continuous technological advancements in CT | +1.2% | National, led by academic medical centers | Medium term (2-4 years) |

| Expanded CMS reimbursement for low-dose lung cancer screening | +0.9% | National, particularly rural and underserved areas | Short term (≤ 2 years) |

| Adoption of mobile CT in outpatient & trauma settings | +0.7% | Regional, focused on emergency departments and ASCs | Medium term (2-4 years) |

| Rapid AI-based workflow & image-quality upgrades | +0.6% | National, early adoption in large health systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Drives Imaging Demand

Cardiovascular disease is projected to affect 45 million U.S. adults by 2050, and hypertension prevalence is forecast to climb from 51.2% in 2020 to 61.0% in 2050. Parallel increases in obesity, depression, and hyperlipidemia have lifted multimorbidity from 52.5% to 59.5% among younger adults between 2013 and 2023. Greater clinical complexity translates into higher examination volumes; CT utilization is expected to rise 25.1% through 2055 [2]GE HealthCare, “Revolution Vibe Launch Details,” gehealthcare.com . Hospitals are expanding cardiac CT programs in anticipation of a 175% surge in procedures per site by 2030. Medicare’s decision to cover virtual CT colonography is another signal that policymakers see preventive imaging as a cost-saving strategy.

Growing Geriatric Population Accelerates Advanced Imaging Adoption

Adults aged 65+ represent the fastest-growing cohort and prefer outpatient settings that offer faster appointments and easier parking. Hospital spending rose 10.4% in 2023 due in part to geriatric diagnostic complexity. Vizient projects a 13% advance in outpatient advanced imaging volumes over the next decade, led by CT and PET. The shift favors the computed tomography market because ambulatory centers often adopt mid-tier scanners that combine cardiac capability with lower capital cost. Workforce attrition complicates this growth: male radiologists face a 13.5% exit rate, intensifying staffing gaps.

Continuous Technological Advancements Transform Clinical Workflows

Photon-counting devices such as Siemens NAEOTOM Alpha.Prime provide 0.2 mm spatial resolution and spectral data in a single, radiation-efficient acquisition [3]Siemens Healthineers, “Photon-Counting CT: A New Era,” siemens-healthineers.com . Ten-year economic models show savings of USD 794.5 per patient due to fewer secondary tests. Northwestern Medicine reported a 15.5% gain in report throughput after integrating generative AI for dictation and decision support. The FDA has green-lit more than 750 radiology-focused AI tools, signaling regulatory comfort with the technology.

Expanded CMS Reimbursement Enhances Access to Preventive Screening

Medicare now reimburses AI-enabled coronary plaque quantification for symptomatic patients with no known disease, broadening access to coronary CT angiography. Lung screening eligibility moved to ages 50-77 and removed patient cost-sharing. CMS estimates these changes will avert 13,982 cancers among beneficiaries annually. Doubling of coronary CTA reimbursement rates further stimulates equipment upgrades at outpatient sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment acquisition & maintenance costs | -1.1% | National, acute in rural and community hospitals | Long term (≥ 4 years) |

| Stringent FDA regulatory pathway & 510(k) backlog | -0.8% | National, affecting all market participants | Medium term (2-4 years) |

| Radiation-dose related patient safety concerns | -0.6% | National, heightened in pediatric centers | Medium term (2-4 years) |

| Radiology workforce shortages constraining scanner utilization | -0.9% | National, severe in rural and secondary markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Equipment Acquisition Costs Constrain Market Penetration

Upfront scanner prices exceeding USD 1 million strain rural balance sheets; 20% of Americans live in counties now lacking local CT access after hospital closures. Managed service agreements and cash-flow-neutral financing have gained traction as providers seek to match payments with revenue cycles. Siemens’ SOMATOM Pro.Pulse reduces energy draw by 20%, lowering total cost for small facilities.

Radiology Workforce Shortages Limit Scanner Utilization Potential

There are more than 1,400 open radiologist positions nationwide, and CT technologist vacancies have reached 18.1%, up from 6.2% three years earlier. The American College of Radiology warns that yearly demand is rising 3-5% despite static residency caps set in 1997. Providers turn to teleradiology, projected to expand from USD 4.4 billion in 2024 to USD 6.7 billion by 2027, to cope with reading backlogs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medium-Slice Systems Gain Momentum

High-slice platforms held 35.12% of the computed tomography market share in 2025, reflecting their dominance in cardiac, trauma, and oncology imaging where rapid temporal resolution is critical. Medium-slice systems are forecast to deliver a 7.53% CAGR and are increasingly selected by outpatient centers seeking cardiac capability without the cost of 256-slice flagships. GE Healthcare’s Revolution Vibe offers single-heartbeat imaging at a mid-tier price, illustrating the market’s pivot toward value-centric upgrades. Low-slice scanners remain relevant for pediatric follow-up and basic trauma studies when dose minimization is paramount. Constrained capital budgets, especially in non-urban facilities, favor mid-range replacements, encouraging suppliers to expand configurable options and AI bundles.

An installed-base shift is under way as providers retire 16-slice workhorses introduced in the early 2000s. Refurbishment programs target safety-net hospitals, whereas private equity-backed imaging chains prefer new installations to capture capacity incentives from payers. The computed tomography market benefits as medium configurations deliver robust ROI in outpatient corridors competing with hospital-owned centers. Vendor neutrality in post-processing has also reduced lock-in, further supporting mid-range adoption. Overall, budget alignment and throughput requirements make medium-slice technology the segment to watch through 2031.

By Application: Neurology Workflows Accelerate with AI

Oncology captured 33.05% of the computed tomography market size in 2025, supported by expanding immunotherapy protocols that require serial monitoring. Neurology, however, will be the fastest climber at 7.44% CAGR because AI triage tools cut scan-to-treatment time for stroke. RapidAI’s Lumina 3D slashes head-and-neck CTA reconstructions from hours to minutes, allowing technologists to move more patients per shift. Cardiovascular volumes also rise as CMS broadens coronary CTA reimbursement, prompting providers to install scanners with ≥128 slices for plaque analytics.

Photon-counting detectors are opening new musculoskeletal horizons by resolving trabecular microarchitecture, valuable in osteoporosis management. Emergency departments still rely on whole-body trauma protocols, yet dose-optimized iterative reconstruction helps comply with ALARA guidelines in pediatric workups. The net effect is a demand mix that encourages vendors to ship multipurpose scanners configurable per clinical service line.

By Mobility: Point-of-Care Adoption Expands

Fixed rooms dominated with 65.70% share in 2025 because high-volume radiology departments rely on broad-bore gantries, power injectors, and fully shielded suites. Mobile systems are climbing 7.46% per year, aided by intensive care demand and rural outreach programs. Prospective trials show bedside head CT produces near-equivalent diagnostic accuracy for intracranial hemorrhage, which is pivotal in neuro-ICU environments. Manufacturers now emphasize battery life, wireless data upload, and compact footprints to navigate narrow hallways.

Mobile stroke units illustrate the growth vector: integrated CT lets paramedics confirm large-vessel occlusion curbside, shaving 30 minutes off door-to-needle time. During the COVID-19 pandemic, pop-up triage tents leveraged self-shielded mobile scanners to reduce cross-contamination risk. These successes persuaded many systems to retain mobile capacity permanently. Federal grants targeting critical-access hospitals further support deployments, broadening the computed tomography market footprint.

By End User: Outpatient Imaging Centers Capture Market Momentum

Hospitals accounted for 48.60% of 2025 revenue owing to complex case mix and emergency demand. Diagnostic imaging centers will grow 7.61% annually as insurers steer routine studies away from high-cost inpatient sites. RadNet’s 21-center expansion and US Radiology Specialists’ plan for 12 new facilities underline this migration. Outpatient operators leverage Saturday scheduling and bundled cash prices to compete for self-pay and high-deductible volumes.

Ambulatory surgery centers add scanners to enable same-day lumbar CT myelograms or postoperative checks, reducing patient transfers. Urgent-care chains also seek compact scanners to shorten orthopedic workups. The computed tomography industry’s modular service contracts, which bundle AI reconstruction and teleradiology reporting, are making technology adoption easier for these lean enterprises.

Geography Analysis

The computed tomography market reveals stark regional contrasts. Large coastal academic hubs in California, Massachusetts, and New York lead adoption of photon-counting platforms due to research grants and complex patient populations. California’s market enjoys additional lift from GE Healthcare’s seven-year deal with Sutter Health covering 300 sites and 3.5 million patients. These agreements tie hardware replacement cycles to staff development programs, accelerating technology refresh

Sun Belt states are experiencing double-digit scanner growth as retirees flock to Arizona, Texas, and Florida. Cardiac CT capacity expansion is most pronounced in these markets because older patients present high coronary risk. Texas gained a boost when RadNet opened its Houston hub, signaling confidence in the region’s reimbursement environment. Certificate-of-need reform in Georgia and South Carolina is attracting new outpatient entrants, enhancing competition.

Rural America faces the opposite trend. One in five residents lives in a county lacking immediate CT access after recent hospital closures. Mobile fleets and teleradiology partnerships are plugging gaps, yet long drive times persist in parts of the Midwest and Appalachia. Federal infrastructure funds earmarked for critical-access hospitals should relieve some disparities, but capital cost remains a barrier. The computed tomography market size attributable to rural catchment areas therefore grows more slowly, although targeted grant programs may unlock latent demand over the forecast horizon.

Competitive Landscape

The United States computed tomography market is moderately concentrated around five multinational vendors that combine equipment, software, and lifecycle services. GE Healthcare’s 2024 acquisition of MIM Software brings advanced contouring and fusion algorithms under its umbrella, positioning the company to offer an end-to-end oncology workflow. Siemens Healthineers is deploying USD 0.67 billion from its broader USD 27.38 billion MedTech fund specifically to extend photon-counting into mainstream price tiers. Canon Medical pursues a training-led strategy through its Cleveland academy, hoping to foster brand loyalty among technologists and biomeds.

Strategic partnerships with cloud and semiconductor firms are reshaping software roadmaps. GE is collaborating with NVIDIA to embed generative AI that automates protocol selection and dose optimization, a response to technologist scarcity. Philips emphasizes spectral CT for interventional guidance, leveraging its catheter portfolio for cross-selling opportunities. Disruptive entrants such as RapidAI carve a niche by integrating vendor-neutral AI that overlays on legacy scanners, threatening to commoditize proprietary workstation sales.

Rural market penetration remains an untapped battleground. Siemens introduces lower-power scanners that can run on community-hospital electrical infrastructure, while GE pilots mobile turnkey suites bundled with teleradiology. Pricing creativity, from subscription scanning models to outcome-based payments, is emerging as the primary lever for winning first-time buyers.

United States Computed Tomography Industry Leaders

Canon Medical Systems Corporation (Toshiba Corporation)

GE Healthcare

Koninklijke Philips NV

Siemens Healthineers AG

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare launched the Revolution Vibe CT system featuring Unlimited One-Beat Cardiac imaging and AI workflow orchestration.

- January 2025: GE HealthCare and Sutter Health entered a seven-year agreement covering 300 facilities and 3.5 million patients to deploy AI-powered CT, MRI, and nuclear medicine technologies.

- September 2024: Canon Medical Systems opened Canon Medical Academy in Cleveland to train customers on CT and other modalities.

- February 2024: Royal Philips introduced the CT 5300 system with integrated AI for diagnostic, interventional, and screening applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the United States computed tomography (CT) market as the revenue generated from the sale or long-term lease of new, factory-built medical CT scanners, fixed or mobile, across all detector slice counts and specialized photon-counting variants. Ancillary service contracts that are bundled at the point of sale are included; aftermarket parts, refurbished units, and veterinary or industrial CT systems are not.

Scope exclusion: Dental-only cone-beam CT devices sold to stand-alone dental clinics fall outside this scope.

Segmentation Overview

- By Product Type

- Low Slice

- Medium Slice

- High Slice

- By Application

- Oncology

- Neurology

- Cardiovascular

- Musculoskeletal

- Other Applications

- By Mobility

- Fixed Systems

- Mobile Systems

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed radiology department heads, imaging-center procurement leads, OEM service managers, and reimbursement policy experts across the Northeast, Midwest, South, and West. These discussions verified slice-mix adoption curves, clarified mobile-fleet penetration, and pressure-tested average selling price (ASP) assumptions surfaced during desk work.

Desk Research

We began with authoritative public datasets, such as FDA 510(k) clearances, CMS procedure volumes, U.S. Census age-cohort projections, and CDC chronic disease prevalence tables, which ground our demand pool. Financial details were obtained from SEC 10-Ks and quarterly filings of the leading CT manufacturers, while import-export codes from the U.S. International Trade Commission clarified cross-border unit flows and revealed average declared values. Supplementary context came from peer-reviewed radiology journals, American College of Radiology guidelines, and position papers from the Medical Imaging & Technology Alliance.

To enrich the competitive lens, analysts drew on Dow Jones Factiva for deal flow and product launch tracking, and D&B Hoovers for company-level revenue splits. The sources named here illustrate, not exhaust, the desk-research corpus consulted.

Market-Sizing & Forecasting

We employ a top-down model that starts with hospital and imaging-center CT installation bases, layers in replacement cycles, and adjusts for new capacity driven by procedure growth. Results are cross-checked through selective bottom-up snapshots, sampled OEM unit shipments times confirmed ASPs, to refine totals. Key variables include annual CT scan volumes, geriatric population growth, average detector slices per scanner, capital budget sentiment indices, and CMS reimbursement shifts for lung cancer screening. A multivariate regression, incorporating these drivers, produces the 2025-2030 forecast; scenario analysis moderates extremes when policy shocks arise.

Data Validation & Update Cycle

Outputs undergo three-step variance checks, senior analyst review, and reconciliation against external equipment sales tallies. The model refreshes annually, with interim updates triggered by FDA approvals of disruptive technologies or reimbursement revisions, ensuring clients receive the latest vetted view.

Why Mordor's United States Computed Tomography Baseline Earns Trust

Published U.S. CT market values seldom match because firms diverge on slice count inclusion, ASP inflation methods, refresh cadence, and whether service contracts are counted.

Key gap drivers center on scope breadth and pricing mechanics. Some publishers exclude premium photon-counting units, others lock ASPs to historic lists, and a few report only initial hardware sales, ignoring bundled multi-year service revenue. Mordor's approach, by contrast, blends unit-level insight with real contract values and is updated each year, which tempers both over-optimism and under-counting.

In sum, our disciplined scope choices, current-year ASP tracking, and balanced top-down/bottom-up reconciliation give decision-makers a dependable midpoint that is transparent, repeatable, and readily defendable on client calls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.48 B (2025) | Mordor Intelligence | - |

| USD 2.40 B (2023) | Regional Consultancy A | Relies on hospital procurement survey from 2022; excludes refurbished unit replacements and premium-slice ASP uplift |

| USD 1.40 B (2024) | Research Publisher B | Counts only hardware purchase, omits bundled service contracts and mobile fleet deployments |

In sum, our disciplined scope choices, current-year ASP tracking, and balanced top-down/bottom-up reconciliation give decision-makers a dependable midpoint that is transparent, repeatable, and readily defendable on client calls.

Key Questions Answered in the Report

What is the current size of the United States computed tomography market?

The market stands at USD 3.71 billion in 2026 and is projected to reach USD 5.13 billion by 2031.

Which product segment is growing fastest in the computed tomography market?

Medium-slice scanners are expanding at a 7.53% CAGR due to their balance of cardiac capability and manageable capital cost.

Why are outpatient imaging centers attracting CT investments?

Insurers push routine scans to lower-cost sites, and operators gain patients through faster scheduling, driving a 7.61% CAGR for this end-user group.

How are mobile CT solutions impacting rural healthcare?

Mobile units supply point-of-care imaging where fixed installations are unaffordable, reducing transfer times and widening access.

What technology trend will most alter CT workflows by 2031?

Photon-counting detectors coupled with AI reconstruction will deliver higher spatial resolution at lower dose, enabling new cardiac and orthopedic applications.

How big is the workforce gap in U.S. radiology?

More than 1,400 radiologist positions remain unfilled, while CT technologist vacancies have reached 18.1%, encouraging adoption of AI and teleradiology.

Page last updated on: