Alzheimers Diagnosis And Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.56 Billion |

| Market Size (2031) | USD 11.06 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alzheimers Diagnosis And Drugs Market Analysis by Mordor Intelligence

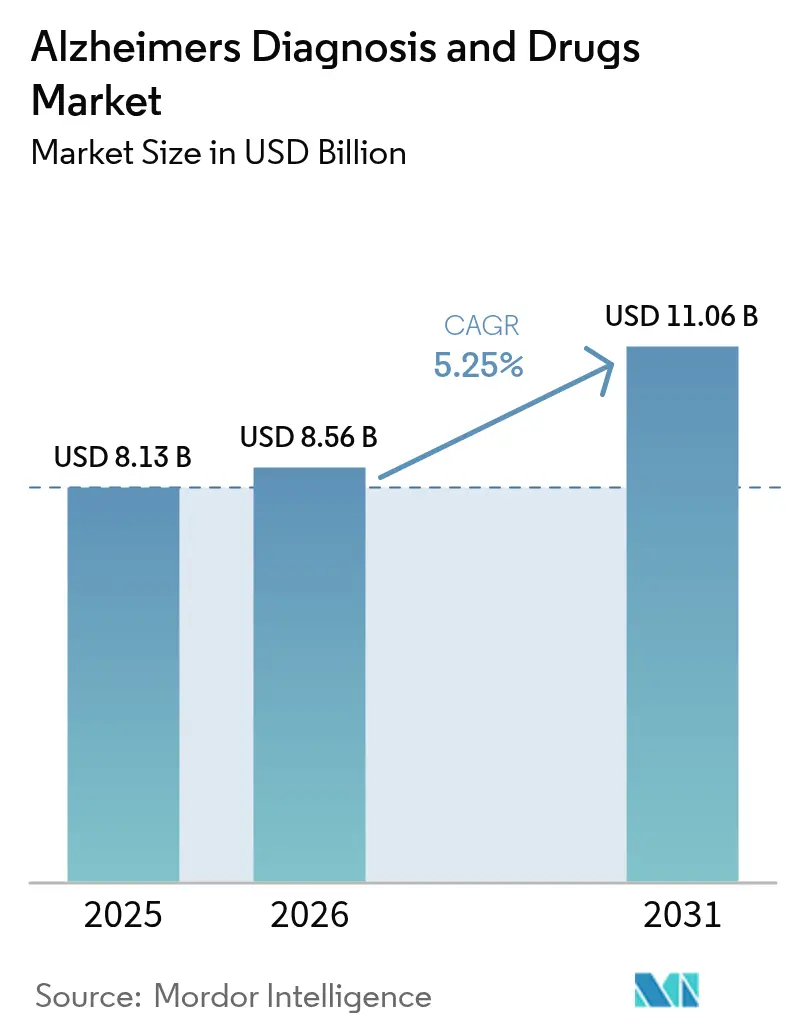

The Alzheimers Diagnosis And Drugs Market size is expected to increase from USD 8.13 billion in 2025 to USD 8.56 billion in 2026 and reach USD 11.06 billion by 2031, growing at a CAGR of 5.25% over 2026-2031.

Growth stems from the first wave of disease-modifying antibodies, widening biomarker reimbursement, and AI-enabled imaging platforms that shorten diagnostic timelines. Anti-amyloid monoclonal antibodies have re-energized investor sentiment, while blood-based tests are solving capacity bottlenecks created by limited PET scanners and cerebrospinal fluid labs. Governments in North America and parts of Europe are adding value-based payment rules that link reimbursement to real-world outcomes, a step that should reduce payer push-back on expensive biologics. Asia-Pacific health systems are spending heavily on neurology training and telehealth, positioning the region for double-digit gains. Meanwhile, venture funding is gravitating toward AI-driven diagnostic start-ups and combination-therapy programs that hedge the historically high Phase III failure rate.

Key Report Takeaways

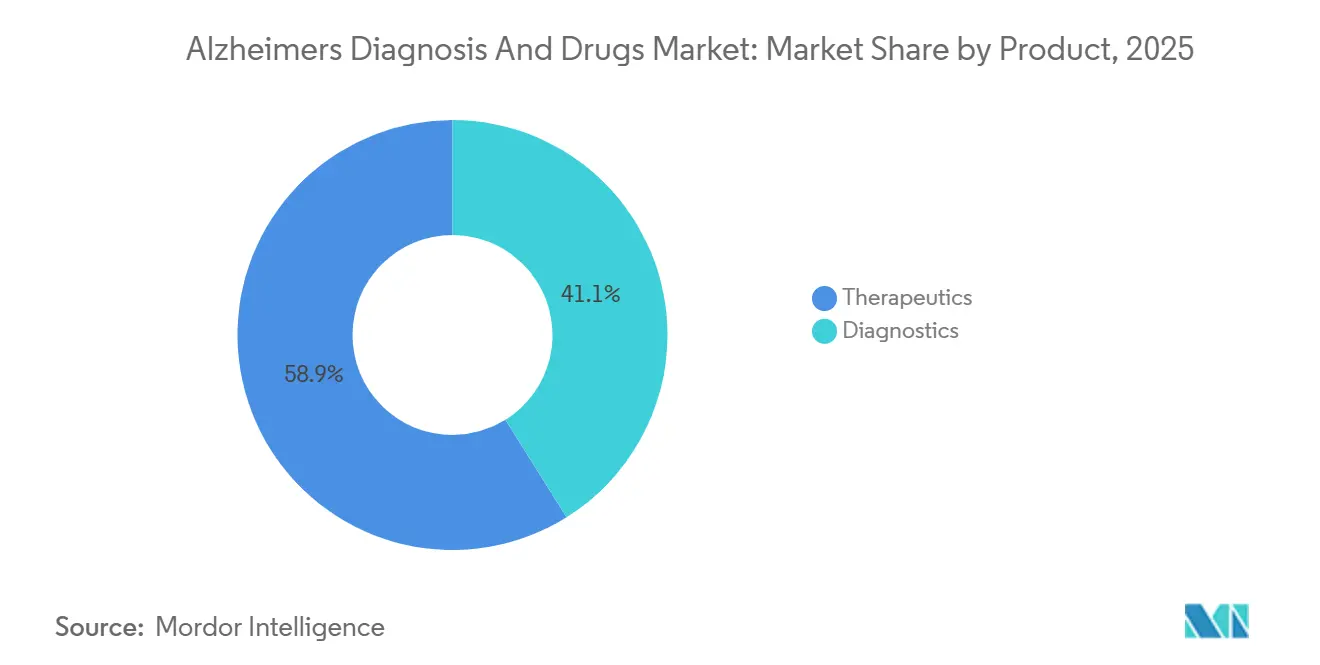

- By product category, therapeutics accounted for 58.90% of the Alzheimer's diagnosis and drugs market share in 2025, while diagnostics are advancing at a 11.95% CAGR through 2031.

- By end user, hospitals and specialty clinics controlled 54.85% of the 2025 revenue pool, but home-care and remote testing providers are expanding at a 13.75% CAGR through 2031.

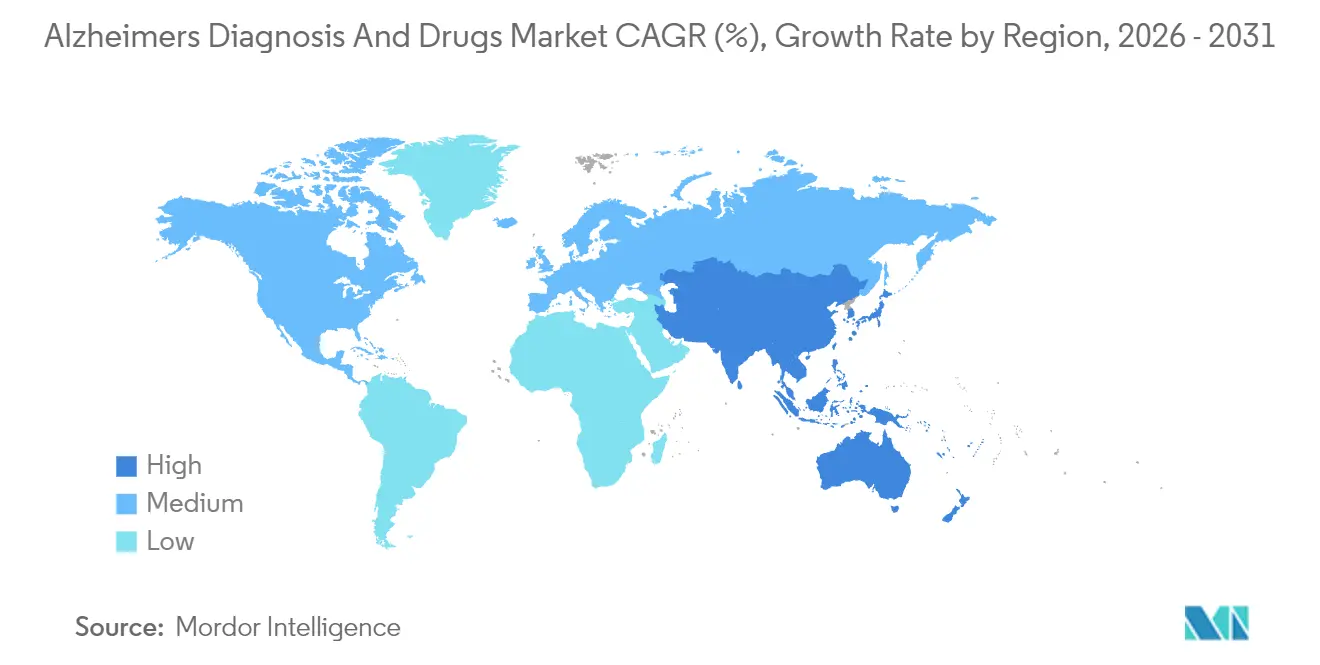

- By geography, North America dominated with 45.10% revenue share in 2025; Asia-Pacific is set to grow the fastest at 10.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Alzheimers Diagnosis And Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising biomarker-based early diagnosis uptake | +1.2% | North America, EU leading | Medium term (2-4 years) |

| Accelerating approvals of anti-amyloid monoclonal antibodies | +1.8% | North America, EU primary; APAC emerging | Short term (≤2 years) |

| Growing geriatric population and disease prevalence | +1.5% | Global; APAC highest growth | Long term (≥4 years) |

| Expansion of blood-based diagnostic test reimbursement | +0.9% | North America leading | Medium term (2-4 years) |

| AI-enabled neuro-imaging workflow efficiencies | +0.7% | Developed markets | Medium term (2-4 years) |

| Regional public-private consortia for dementia R&D | +0.6% | North America, EU, select APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Approvals of Anti-Amyloid Monoclonal Antibodies

Full FDA approval of lecanemab in July 2024 and conditional EMA authorization two months later established a commercial pathway for disease-modifying therapy, prompting Medicare to relax access rules through coverage with evidence development.[1]“FDA Grants Accelerated Approval for Alzheimer’s Disease Treatment,” FDA, fda.gov Donanemab’s FDA nod in August 2024 intensified competition, forcing manufacturers to engage in value-based pricing discussions earlier in the product life cycle. Hospital networks are already expanding infusion suites, while specialty pharmacies negotiate risk-sharing agreements that tie discounts to cognitive-score maintenance. The approvals have also raised the regulatory bar, with future candidates expected to demonstrate plaque removal plus clinically meaningful slowing of decline. Asia-Pacific agencies are mirroring Western regulators, with Japan granting lecanemab priority review within 6 months of the U.S. decision, reinforcing global momentum behind disease-modifying biologics.

Rising Biomarker-Based Early Diagnosis Uptake

The FDA’s 2024 breakthrough-device designations for plasma phospho-tau assays capped a decade-long quest for minimally invasive screening, shrinking dependence on PET and lumbar puncture.[2]Heather Snyder, “Revised Diagnostic Guidelines for Alzheimer’s Disease,” Alzheimer’s Association, alz.org Updated clinical guidelines now recommend blood biomarkers as first-line tests, which has multiplied testing volumes at Quest Diagnostics and LabCorp. Primary-care physicians are adopting screening workflows that add just five minutes to routine visits, enabling earlier therapeutic intervention. Health-plan actuaries are recalculating cost-offsets, noting that each year of delay in institutional care saves USD 17,000 per patient in U.S. Medicaid outlays. Emerging economies are piloting mobile phlebotomy vans that collect samples in rural areas, broadening diagnostic reach without significant investment in bricks-and-mortar infrastructure.

Growing Geriatric Population & Disease Prevalence

The UN projects the global 65-plus cohort to reach 95 million by 2030, with APAC accounting for over half of that growth. Alzheimer’s prevalence will hit 7.1 million in the United States alone, raising the economic burden to USD 360 billion per year. Governments are embedding dementia strategies into broader healthy-aging agendas, allocating funds for memory clinic networks and specialist training slots. China’s five-year dementia program mandates biomarker capacity in every tier-2 hospital, while India is rolling out community health worker curricula that include cognitive screening modules. Venture investors view these demographics as a structural tailwind, justifying larger Series B rounds for platform biotech and digital therapeutics aimed at early-stage disease.

Expansion of Blood-Based Diagnostic Test Reimbursement

Medicare assigned national coverage for amyloid and tau blood tests in January 2024, triggering commercial payer adoption by Aetna, Humana, and Blue Cross plans by mid-2024. Germany’s G-BA granted provisional coverage at EUR 320 per test in September 2024 and demanded 24-month real-world evidence submissions. NICE draft guidance in October 2024 limited biomarker use to patients with CDR scores of 0.5-1.0 pending asymptomatic validation. This staggered adoption pattern positions diagnostics suppliers to capture revenue sooner in the United States while lobbying European agencies for broader inclusion, creating regional tailwinds for the Alzheimer's diagnosis and drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Late-stage drug failure rates and sunk R&D costs | -0.8% | Global | Long term (≥4 years) |

| Limited specialist workforce for therapy monitoring | -0.6% | Global; acute in rural markets | Medium term (2-4 years) |

| Diagnostic biomarker performance variability across ethnicities | -0.4% | Diverse populations | Medium term (2-4 years) |

| Payer hesitancy on high-cost biologics | -0.9% | North America, EU | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Late-Stage Drug Failure Rates & Sunk R&D Costs

Phase III attrition above 90% continues to discourage big-ticket bets, underscored by Roche’s 2024 exit from gantenerumab after USD 2 billion in spend. Investors price higher risk, upping demanded equity stakes and milestone contingencies. Mid-cap biotech is turning to platform approaches, aiming to recycle failed assets into combination regimens rather than scrapping them outright. Policy makers fear innovation droughts and are experimenting with tax credits that trigger only on successful proofs of concept, thereby sharing downside risk. Academic consortia are lobbying for dedicated NIH lines that cover “bridge-to-pivot” studies, extending the life of promising molecules that miss single-endpoint trials.

Limited Specialist Workforce for Disease-Modifying Therapy Monitoring

At USD 26,500 per year, lecanemab forces payers to reckon with stretched neurology budgets; NICE withheld full UK coverage pending real-world data, reflecting a broader European skepticism.[3]“Lecanemab Health Technology Assessment,” NICE, nice.org.uk Private U.S. insurers require amyloid positivity plus mild cognitive impairment staging, trimming the eligible pool by an estimated 30%. Coverage with Evidence Development compels physicians to upload cognitive-outcome metrics, creating administrative drag that deters smaller clinics. Some payers are trialing subscription models modeled on hepatitis-C contracts, but uptake remains limited. Delayed reimbursement cycles strain specialty pharmacies' cash flow, nudging them to demand higher wholesaler discounts or abandon the category. Patient advocacy groups fear a two-tier system in which only large urban centers provide disease-modifying biologics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostics Outpace Therapeutics on Reimbursement Momentum

Diagnostics revenue is forecast to compound 11.95% yearly through 2031, more than double the Alzheimer's diagnosis and drugs market CAGR, as blood biomarker tests supplant imaging and CSF taps. Declining CSF volumes down 2.1% per year reflect patient preference and faster blood-test turnarounds. AI-driven MRI post-processing further reduces dependence on costly PET scans.

Therapeutics retained 58.90% of 2025 sales, driven by generic cholinesterase inhibitors, which accounted for USD 2.8 billion. Anti-tau agents lag: TauRx’s hydromethylthionine missed its phase 3 endpoint in September 2024, delaying launch to 2027. Roche’s semorinemab entered phase 3 in January 2024, with results expected in 2027, signaling a second wave of innovation beyond amyloid clearance. The Alzheimer's disease diagnosis and therapeutics market is projected to grow modestly at 5.25% per year, as diagnostics capture a rising share of new spending.

By End User: Home-Care Providers Gain as Point-of-Care Tests Proliferate

Hospitals and specialty clinics generated 54.85% of 2025 revenue by controlling infusion suites and MRI scanners. Their dominance will erode as subcutaneous dosing and portable blood-test kits move treatment to lower-cost sites.

Home-care and remote testing providers are forecast to expand 13.75% annually through 2031, the fastest pace among end users. Eisai’s at-home lecanemab autoinjector, filed for FDA priority review in January 2025, exemplifies the shift. Rural patients gain access without traveling to memory centers, broadening geographic penetration and diversifying revenue streams inside the Alzheimer's diagnosis and drugs market.

Geography Analysis

North America retained 45.10% revenue in 2025, propelled by early access to FDA-cleared biologics and CMS reimbursement for blood biomarkers. Canadian provinces align benefits, though Quebec negotiates independent price caps that shave average antibody prices by 12%. Mexico leverages medical tourism, drawing Latin American patients for PET scans and tapping cross-border insurance partnerships that package lodging with diagnostic bundles. Canada’s provincial formularies added lecanemab during 2024, contingent on amyloid confirmation and APOE genotyping. Sustained payer backing underpins a steady 5.8% regional CAGR through 2031.

Asia-Pacific is the fastest-growing bloc, charting a 10.55% CAGR. China’s dementia plan mandates that amyloid-PET and blood-biomarker testing be available at every prefecture-level hospital by 2028. The Alzheimer's disease and drug market share in APAC could reach 28.60% by 2031 as Japan accelerates reimbursement for AI imaging and South Korea rolls out nationwide cognitive-screening programs at community clinics. Australia’s expedited-review pathway shaves six months off regulatory timelines, making the country a beachhead for Western firms entering Asia. India is piloting public-private elder-care hubs that combine day care, telehealth, and diagnostics under a single roof, financed by municipal bonds.

Europe offers a mature yet fragmented landscape. Germany’s sickness funds cover blood-biomarker tests ahead of most EU peers, but France still ties reimbursement to PET confirmation, slowing routine uptake. The Horizon Europe program injects USD 350 million into dementia consortia, widening the R&D pool for mid-sized biotech. Eastern European members lag in therapeutic adoption due to constrained specialty-care budgets, though they gain from EU structural funds that upgrade imaging infrastructure.

Regulatory Landscape

Regulation in Alzheimer’s diagnosis and therapeutics is being shaped by tighter evidentiary expectations for disease-modifying drugs and clearer pathways for biomarker tests and drug-device combinations. In the United States, the FDA’s March 2024 draft guidance on Early Alzheimer’s disease drug development clarified trial design and endpoint considerations for early-stage populations, reinforcing the need to link biomarker effects to clinically meaningful outcomes. The FDA also continues to steer combination products through early sponsor engagement, including pre-IND interactions, when delivery devices, companion diagnostics, or integrated workflows are part of the therapy and monitoring model.

In Europe, EMA guidance for clinical investigation in Alzheimer’s disease (consultation activity spanning 2025-2026) and EU device rules are shaping how blood-based tests and integrated drug-device offerings are brought to market under MDR/IVDR expectations. The EMA established the Combination Products Operational Group (COMBO) in December 2025, highlighting interface topics such as MDR Article 117 requirements for medicinal products that incorporate devices. These regulatory signals are also reflected in approvals that expand care models, including the FDA approval in July 2026 of LEQEMBI IQLIK (lecanemab-irmb) subcutaneous injection as an initiation dose for early Alzheimer’s disease, which affects post-market monitoring, labeling, and payer evidence requirements for broader use.

Competitive Landscape

Competition intensified once lecanemab and donanemab demonstrated that plaque clearance yields clinical benefit. Biogen and Eisai co-promote Leqembi, leveraging Biogen’s U.S. neurology sales force and Eisai’s global manufacturing. Eli Lilly, facing capacity bottlenecks, signed a contract-manufacturing pact with Samsung Biologics to double antibody output by 2026. Roche redirects resources to a tau-targeted small-molecule after its antibody setback, while Novartis invests in gene-editing spin-outs exploring APOE4 knock-down strategies. C2N Diagnostics and Quanterix engage in cross-licensing of antibody clones to broaden assay menus and secure hospital-lab stickiness.

Digital entrants complicate the field. Google’s DeepMind teams up with the University of Oxford to develop multimodal AI that integrates speech pattern analytics with MRI, inching toward a software-as-medical-device submission for 2026. Apple embeds cognitive-assessment modules into watchOS, signaling a future in which consumer electronics feed clinical decision support. Patents around phospho-tau epitopes form a dense thicket; USPTO filings related to Alzheimer’s biomarkers jumped 28% in 2024. Mid-tier players hedge risk through option-based partnerships: Alector grants AbbVie regional marketing rights for a TREM2 agonist contingent on reaching Phase II endpoints. Overall, intellectual-property strength, AI enablement, and manufacturing scalability form the three pillars of durable advantage.

Alzheimers Diagnosis And Drugs Industry Leaders

AstraZeneca PLC

Eli Lilly and Company

F. Hoffmann-La Roche AG

Johnson &Johnson Services, Inc.

Bristol-Myers Squibb Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Care delivery is shifting toward scalable, decentralized diagnosis and lower-burden administration, which creates whitespace for blood-based biomarker workflows, high-throughput lab platforms, and services that link testing to treatment eligibility and safety monitoring. In diagnostics, multiple 2026 milestones support commercialization and adoption of standardized blood assays across geographies: Roche announced CE marking in May 2026 for its Elecsys plasma pTau217 test, and Beckman Coulter Diagnostics received a CE Mark under IVDR in July 2026 for an Access p-Tau217 assay, supporting regulated, routine-lab options beyond PET and CSF. In the United States, FDA action to codify special controls for an Alzheimer’s disease pathology assessment test into class II in April 2026 sets clearer expectations for performance, labeling, and quality systems, which helps manufacturers and laboratories scale testing menus with less regulatory uncertainty.

On the therapeutics side, opportunities increasingly depend on improving the practicality of disease-modifying therapy (DMT) delivery and expanding access in new geographies. The FDA approval in July 2026 of LEQEMBI IQLIK as a subcutaneous initiation dose strengthens at-home or non-infusion-site care pathways, aligning with the broader shift toward home-care and remote testing providers. Active clinical programs are also broadening beyond amyloid-only approaches: UCSF launched the Alzheimer’s Tau Platform (ATP) trial in July 2026, a multi-site study designed to evaluate combination regimens, which supports a pipeline and partnering environment for companion diagnostics, combination-therapy development, and longitudinal monitoring solutions that integrate blood biomarkers, imaging, and digital assessments.

Recent Industry Developments

- July 2026: The FDA approved LEQEMBI IQLIK (lecanemab-irmb) subcutaneous injection as an initiation dose for early Alzheimer’s disease. The decision expands dosing options beyond infusion-centered pathways and supports more decentralized care models when paired with biomarker confirmation and ongoing monitoring.

- July 2025: The FDA approved a titration-dose label update for donanemab, aimed at reducing ARIA-E incidence while maintaining amyloid clearance. This change improves real-world usability for anti-amyloid therapy programs and influences how providers plan monitoring protocols and infusion-suite capacity.

- May 2024: Medicare assigned national coverage for amyloid and tau blood tests, accelerating payer adoption of blood-based biomarker workflows. Wider reimbursement improves test throughput versus PET and CSF pathways and increases diagnostic laboratory participation in the Alzheimer’s care continuum.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from products used to diagnose Alzheimer disease and to treat it with prescription therapies, counted at the global level across major regions.

Scope exclusions: We exclude non-Alzheimer dementias, non-medical care services, and supportive non-drug interventions that do not directly diagnose or treat Alzheimer disease.

Segmentation Overview

- By Product

- Therapeutics

- Cholinesterase Inhibitors

- NMDA Receptor Antagonists

- Anti-amyloid mAbs

- Anti-tau & other DMTs

- Diagnostics

- Brain Imaging

- CSF Biomarker Tests

- Blood-based Biomarker Tests

- Genetic Testing

- Therapeutics

- By End User

- Hospitals & Specialty Clinics

- Diagnostic Laboratories

- Research & Academic Institutes

- Home-care / Remote Testing Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market, define what qualifies as an Alzheimer diagnostic or drug, and map where demand is likely to sit by region. Public sources were reviewed for the disease burden, testing pathways, and treatment access patterns, which then shaped the demand pool we modeled.

Key inputs were taken from sources such as the World Health Organization, the US FDA, the US CDC, OECD health statistics, and publications indexed in PubMed, then cross-checked with company filings, earnings material, and credible press coverage. Where needed, we also used paid subscriptions for company financials and intelligence, patents, and news and financials to confirm product activity and keep assumptions grounded. These sources are illustrative and not exhaustive, and many other references were used to collect data, validate totals, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how diagnosis volumes are moving, how therapy uptake differs by stage of disease, and what pricing and access changes are being seen in practice. We spoke with a mix of clinicians, diagnostic lab stakeholders, and industry-facing experts across APAC, EMEA, and the Americas, so gaps from desk findings could be closed and key assumptions could be stress-tested before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 41% | EMEA: 31% |

| Smaller Players: 16% | Managers: 43% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic, where epidemiology and care-pathway math set the demand pool first, followed by reality checks using selective supplier and channel signals. In practice, prevalence and diagnosed population were translated into testing and treatment cohorts, which were then converted to value using typical test frequency, therapy duration, and average selling prices.

Key model inputs included Alzheimer prevalence and aging population share, diagnosis rates and testing mix (imaging, CSF, blood-based biomarkers, and genetic tests), treatment initiation and persistence by disease stage, retail and hospital channel mix, and region-level reimbursement or access signals that affect uptake. Forecasting relied on scenario analysis supported by expert feedback, since adoption curves for newer modalities and therapy classes can shift with guideline updates and payer behavior. When bottom-up inputs were incomplete in smaller countries, proxy ratios were applied from similar health-system peers, then adjusted through expert checks to avoid overstating penetration.

Data Validation & Update Cycle

Outputs were validated by comparing implied patient counts, testing volumes, and therapy-treated cohorts against independent signals from public health statistics and published clinical practice patterns. Large variances were flagged, reworked, and reviewed in more than one analyst pass before sign-off, with follow-up calls triggered when pricing, uptake, or access assumptions looked inconsistent.

The model is refreshed annually, and interim updates are made when material events occur, such as major regulatory decisions, guideline changes, or step-changes in reimbursement. Before delivery, a final review pass is done so clients receive the most current set of assumptions and the resulting market numbers.

Mordor Intelligence's Alzheimers Diagnosis and Drugs Market Size Compared With Other Published Estimates

Published market sizes for Alzheimer diagnosis and drugs often do not match because the included test types, therapy boundaries, and the timing of price and uptake assumptions are not consistent. Differences can also come from whether the estimate uses a treated-patient build or a broad spending pool that includes adjacent dementia care activity.

The biggest gap drivers in this market are usually whether imaging is counted as Alzheimer-specific diagnosis revenue, whether blood-based biomarker testing is included as it scales, and whether drug revenues include only Alzheimer-labeled use or also off-label symptomatic prescribing. Some studies also apply aggressive uptake for newer therapies without tying it back to diagnosis capacity and payer coverage, which can inflate near-term values, and currency timing can further widen the spread when exchange rates move.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.13 B (2025) | |

| Industry Research Publisher A | USD 7.80 B (2025) | Often treated as a combined diagnostics and therapeutics view but with a different diagnostic scope mix, which can undercount newer biomarker-led pathways or apply lower near-term test and therapy adoption assumptions. |

| Industry Research Publisher B | USD 9.70 B (2024) | Can emphasize biomarker tests while excluding several structural imaging approaches, and it may also use a higher growth base case for therapy uptake and pricing, which pushes the total upward when rolled into one global number. |

The table shows that most of the spread is explained by what is counted as Alzheimer-specific diagnosis revenue, plus how quickly therapy uptake is assumed to expand versus real-world diagnosis capacity. By linking tested and treated cohorts to practical access and pricing signals, and by keeping imaging and biomarker categories consistently classified year to year, the estimate stays more traceable for planning purposes, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the forecast revenue for the Alzheimers diagnosis and drugs market by 2031?

It is projected to reach USD 11.06 billion, reflecting a 5.25% CAGR over 2026-2031.

Which product class is growing the fastest?

Diagnostics, especially blood-based biomarker assays, are expanding at a 11.95% CAGR through 2031.

Which region will post the highest growth rate?

Asia-Pacific is on track for a 10.55% CAGR, driven by aging demographics and increased healthcare spending.

What share did hospitals and specialty clinics hold in 2025?

They captured 54.85% of global revenue thanks to infusion and imaging infrastructure.

Which companies dominate disease-modifying therapy?

Biogen, Eisai, and Eli Lilly lead with approved or near-approved anti-amyloid antibodies.

Page last updated on: