Aluminum Cans Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 58.13 Billion |

| Market Size (2031) | USD 70.72 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

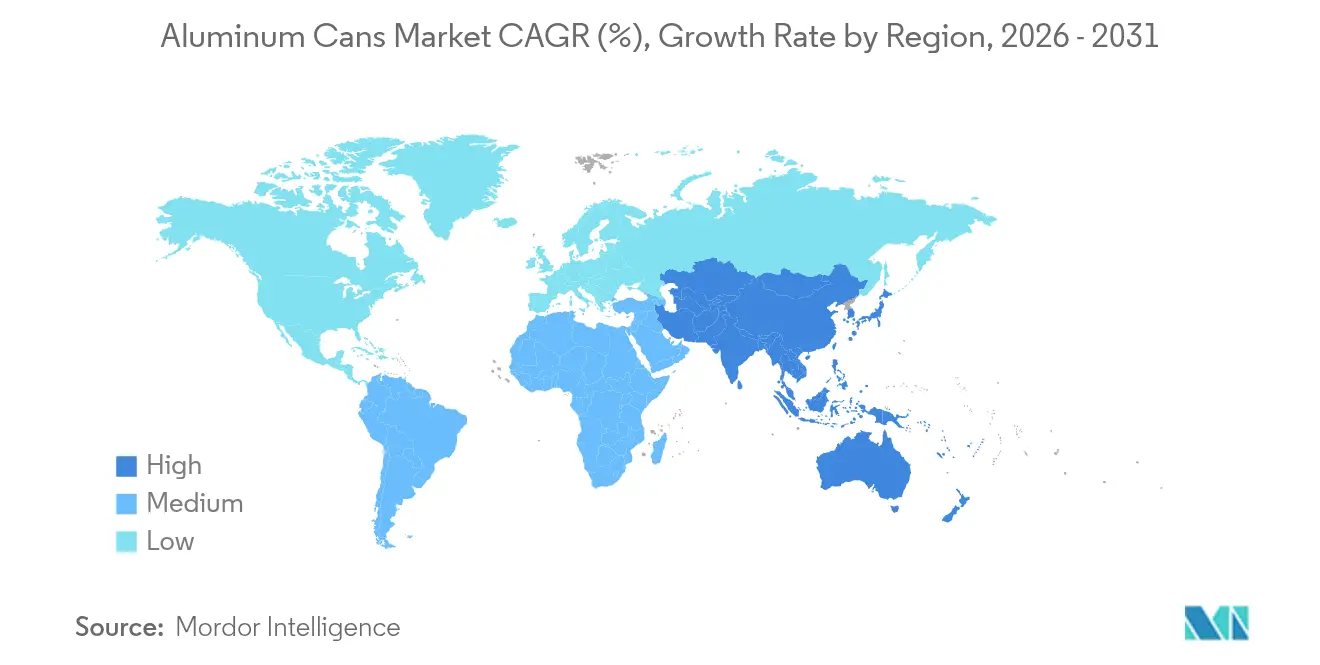

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

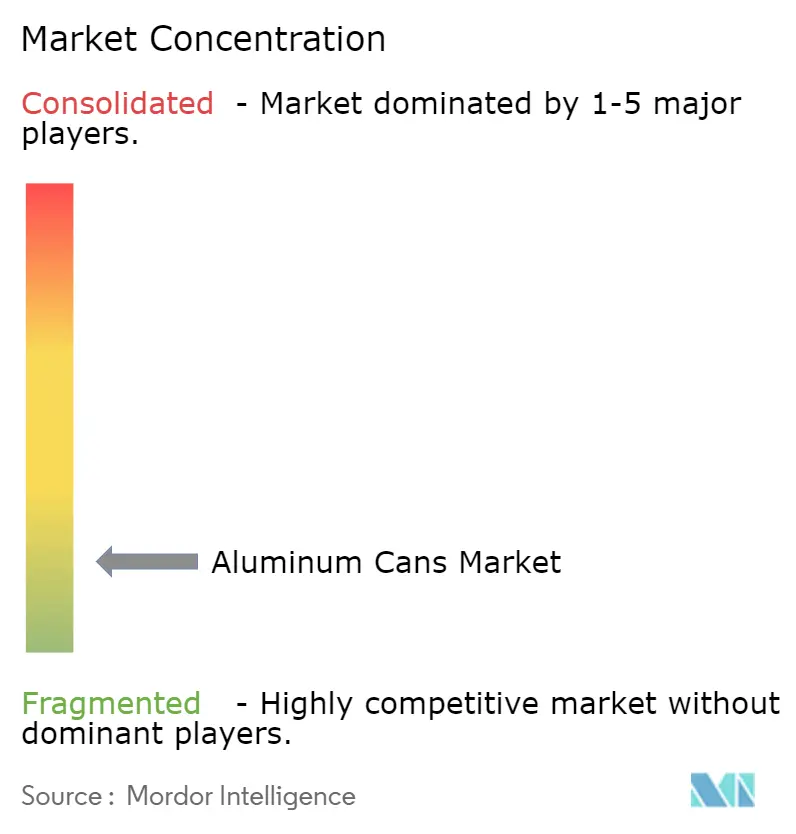

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminum Cans Market Analysis by Mordor Intelligence

The global aluminum cans market size in 2026 is estimated at USD 58.13 billion, growing from 2025 value of USD 55.89 billion with 2031 projections showing USD 70.72 billion, growing at 4.01% CAGR over 2026-2031. Sustained policy pressure favoring circular packaging, rapid adoption by beverage producers shifting away from PET and glass, and capacity additions in high-growth regions collectively underpin this steady expansion. Deposit return systems that guarantee 90% collection by 2029 across the European Union sharply improve recycling economics, prompting brand owners and converters to accelerate investments in closed-loop can manufacturing. Asia Pacific retains its leadership position thanks to rising urban disposable incomes, while North America and Europe leverage premiumization and evolving sustainability mandates to support value growth. Capacity bottlenecks persist, yet recent acquisitions and greenfield builds point to a gradually improving supply balance. At the same time, premium beverage launches, wine-in-can initiatives, and e-commerce demand for dent-resistant formats create additional tailwinds that lift the aluminum cans market well beyond traditional carbonated soft drink applications.

Key Report Takeaways

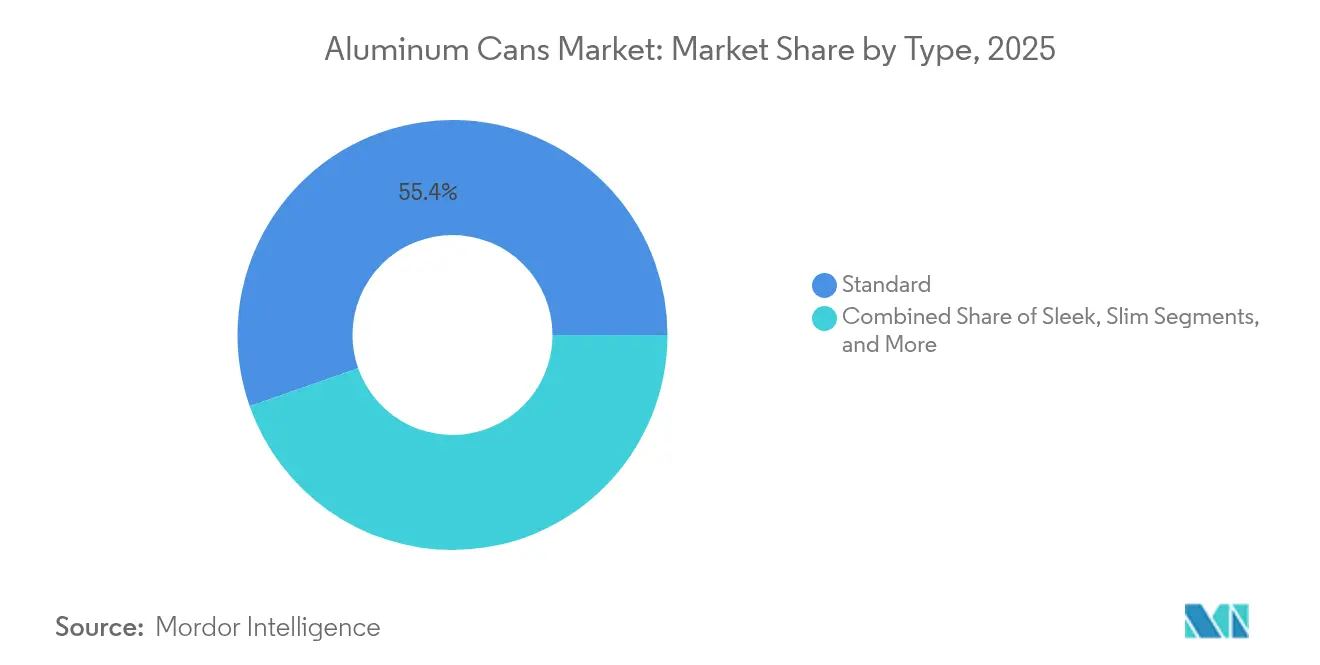

- By type, standard formats controlled 55.38% revenue in 2025, whereas sleek variants are set to advance at a 4.06% CAGR through 2031.

- By end-user industry, beverages captured 48.35% of the aluminum cans market share in 2025, while aerosol applications exhibit the highest projected CAGR of 5.21% over the same period.

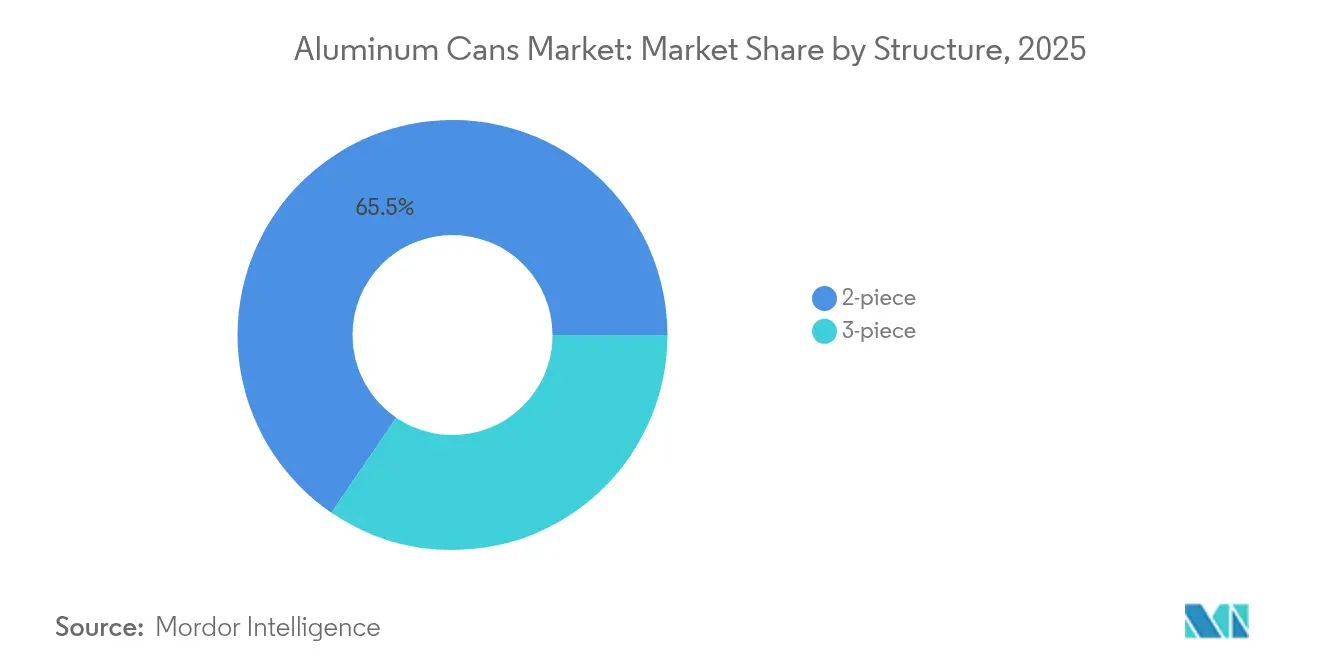

- By structure, 2-piece technology held 65.48% share of the aluminum cans market size in 2025 and should grow 4.48% annually to 2031.

- By capacity, the 251-500 mL range accounted for 52.57% of 2025 revenues, yet up-to-250 mL formats are forecast to outpace at 4.16% CAGR through 2031.

- By geography, Asia Pacific led with 40.74% market share in 2025, and its aluminum cans market size is primed to rise 5.52% annually between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aluminum Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High recyclability and closed-loop recovery systems | +1.20% | Global, early leadership in the EU & North America | Long term (≥ 4 years) |

| Shift from PET/glass to aluminum amid EPR and plastics-tax mandates | +1.50% | Europe & North America, spreading to APAC | Medium term (2-4 years) |

| Boom in RTD, craft, and functional beverages | +0.90% | North America & Europe, spill-over to APAC | Short term (≤ 2 years) |

| Rapid growth of can-friendly wine and spirits packaging | +0.30% | North America, Europe, Australia | Medium term (2-4 years) |

| E-commerce’s need for dent-resistant primary packaging | +0.20% | Global urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Recyclability and Closed-Loop Recovery Systems

Aluminum retains its metallurgical properties indefinitely, enabling genuine material circularity that plastic and glass cannot match. The Can Manufacturers Institute notes that 75% of all aluminum ever produced remains in active use today, and remelting secondary aluminum consumes 95% less energy than primary smelting.[1]Can Manufacturers Institute, “Aluminum Beverage Can Remains Most Recycled Drinks Package,” canc entral.com European smelters Constellium, Elval, Novelis, and Speira harmonized alloy specifications in April 2024 to allow beverage cans with up to 100% recycled content, cutting carbon emissions by 2.6 tons of CO₂ per ton of metal and lowering operating costs for fillers committed to science-based climate targets. U.S. recycling rates slipped to 43% in 2023, but industry-backed investments aim to lift recovery to 70% by 2030 and 90% by 2050, ensuring long-term feedstock security for can plants. Deposit return programs covering more than 40 billion containers annually in Europe, Canada, and select U.S. states materially raise collection volumes, translating into lower scrap premiums and stronger margins for integrated can makers. These structural advantages collectively add 1.2 percentage points to forecast CAGR, cementing aluminum’s reputation as the definitive circular beverage package.

Shift from PET/Glass to Aluminum Amid EPR and Plastics-Tax Mandates

Extended Producer Responsibility schemes fundamentally reshape material cost hierarchies. The United Kingdom’s 2025 base EPR fee is set at GBP 266 per tonne for aluminum, far below levies applied to PET, multilayer pouches, or difficult-to-recycle flexibles. California expanded its Container Redemption Value program to wine and spirits in January 2024, immediately widening the addressable beverage can universe by 400 million units a year. Meanwhile, EU rules compel 90% collection of single-use beverage containers by 2029, a benchmark that heavily favors aluminum due to its high post-consumer scrap value. Australia will require 80% recycled content in food-grade aluminum by 2040, again reinforcing demand visibility along the entire Pacific Rim. These converging policies collectively boost aluminum’s attractiveness and inject an additional 1.5 percentage point lift into medium-term growth forecasts.

Boom in RTD, Craft, and Functional Beverages

Canned juice revenues jumped 8.5% to USD 1.43 billion in 2024, even as broader beverage volumes stagnated. Crown Holdings reports that 75% of new drink launches now choose cans for North American rollouts, citing oxygen-barrier performance and full-body branding real estate as decisive factors. Energy drinks, spiked seltzers, and adaptogen-infused functional beverages deeply value aluminum’s light weight and quick-chill properties, allowing cold-chain efficiency that glass cannot deliver. Mexico’s beer market reached 80% can penetration in 2024, while Brazil is tracking for 64% by 2026, validating can momentum across Latin America. The swift rise in performance beverages enriches product mix and lifts filling line utilization, adding roughly 0.9% to global CAGR during the first half of the forecast period.

Rapid Growth of Can-Friendly Wine and Spirits Packaging

California wineries introduced 90-gram aluminum bottles that slash transport-phase carbon versus 500-gram glass, winning shelf listings at major grocery chains seeking sustainable premium SKUs. The U.S. Alcohol and Tobacco Tax and Trade Bureau removed fill-size barriers in January 2025, formally legalizing a wide variety of can volumes for wine and distilled spirits. Portion-control trends align neatly with 187-mL and 250-mL formats, expanding aluminum’s presence in single-serve hospitality channels. Technical hurdles, such as aluminum ion migration in high-strength spirits, are being mitigated by FDA-approved epoxy-free internal liners, enabling safe multi-year shelf life. Although the current driver impact is modest, accelerating brand adoption adds 0.3% to CAGR potential in medium-term horizons.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from flexible PET and carton formats | -0.80% | Global, most severe in cost-sensitive markets | Short term (≤ 2 years) |

| Price and supply volatility of primary aluminum | -0.60% | Global, import-dependent regions hit hardest | Medium term (2-4 years) |

| Regional can-making capacity bottlenecks | -0.40% | North America, Europe, and selective APAC zones | Medium term (2-4 years) |

| Rising Scope-3 decarbonization compliance costs | -0.30% | Europe & North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Flexible PET and Carton Formats

Multilayer cartons and lightweight PET bottles continue to dominate price-sensitive segments, especially for private-label juices, dairy drinks, and shelf-stable water, where brand owners prioritize unit cost over recyclability. New glycol-modification techniques have extended PET shelf life for carbonation and sensitive nutrient blends, narrowing aluminum’s functional advantage. In developing economies, consumer willingness to pay sustainability premiums remains low, restraining penetration in commoditized categories. However, upcoming bans on non-recyclable plastic formats across the EU and Canada, alongside hard-to-reach EPR thresholds, will gradually erode the competitive edge of flexibles. Net effect is a temporary 0.8% drag on the aluminum cans market CAGR from 2025-2027.

Price and Supply Volatility of Primary Aluminum

London Metal Exchange prices oscillated between USD 2,100-2,300 per tonne throughout 2024 amid geopolitical tensions and energy cost spikes.[2]Aluminium Journal, “LME Price Volatility Commentary 2024,” aluminiumjournal.com Boston Consulting Group projects a 16-million-ton deficit by 2030 without USD 60-90 billion in new smelting capacity, raising cost-of-capital hurdles for downstream converters. Small and mid-tier can makers lack financial instruments to hedge price swings, slowing greenfield projects in Africa and Southeast Asia. On the flip side, secondary aluminum now represents over 70% of beverage-can body sheet in mature regions, cushioning volatility. Overall, metal cost uncertainty still subtracts 0.6% from mid-term growth forecasts until additional recycling capacity or energy-efficient smelters come online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Standard Formats Dominate, Sleek Designs Accelerate

Standard 330-mL and 355-mL bodies retained 55.38% of 2025 revenue, a share underpinned by filling-line compatibility, the highest line speeds, and optimal pallet density. The segment also capitalizes on broad end-user familiarity, which reduces changeover costs for global bottlers. Nevertheless, sleek cans, typified by 250-mL and 310-mL footprints, are advancing swiftly at a 4.06% CAGR thanks to their premium visual ratio and enhanced billboard effect in crowded retail aisles. Beverage formulators serving functional, low-calorie, and alcohol-ready-to-drink segments prize the elongated profile for differentiated shelf blocking and cold-box visibility. Ball’s Dynamark variable-graphics platform lets marketers design limited-run art across both standard and sleek formats without line-stopovers, trimming inventory risk and fostering campaign agility. As printing technology lowers per-unit cost, sleek cans should secure incremental penetration in higher-margin SKUs. Specialty shapes and tactile embossing remain nascent but reflect ongoing innovation that further enriches consumer experience. Altogether, the aluminum cans market expects continued coexistence of standard mass-volume formats and sleek premium variants, with the latter responsible for outsized revenue gains relative to capacity installed.

Standard bodies still benefit from superior logistics economics: a 24-count case of 355-mL cans weighs 20% less than an equivalent glass pack, cutting freight emissions and reducing shelf-stack injuries for retailers. Their thicker gauge, tooled since the 1990s, affords converters a stable margin capture even at high metal premiums. Yet brand owners are willing to absorb a slight cost uplift for sleek cans targeting lifestyle positioning where visual disruption and perceived health cues trump per-ounce value. By 2030, sleek units are likely to reach double-digit market share, adding breadth to packaging portfolios while maintaining backward compatibility with legacy line equipment. As such, type diversification reinforces the broader aluminum cans market’s resilience and keeps switching costs low for bottlers contemplating entry into niche beverage sub-categories.

By End-User Industry: Beverages Predominate, Aerosols Surge

Beverages claimed 48.35% of global revenues in 2025, mirroring a century-long symbiosis between carbonated drinks and lightweight metal containers. Carbonated soft drinks, energy shots, and sports hydration products remain workhorse volumes that secure economies of scale for can-sheet rolling mills. Sustained double-digit launches of spiked seltzers, CBD-infused tonics, and nitro-coffee further widen beverage category breadth, allowing can lines to run at near-full utilization even during off-season contractions for mainstream sodas. Meanwhile, aerosol fillings from deodorants to cooking sprays are forecast to post a 5.21% CAGR, marking them the fastest mover within the aluminum cans market. Brand owners appreciate aluminum’s corrosion resistance for formulations containing oils, propellants, or alcohols that degrade tinplate alternatives. Enhanced wall ironing processes enable pressure ratings up to 18 bar, paving the way for mousse, paint, and whipped-cream formats as well.

Pet food and human canned foods hold a smaller slice but deliver stable year-round demand anchored in inventory rotation and emergency-stock purchasing behaviors. Silgan Holdings witnessed double-digit pet food can revenue growth in 2024, illustrating premium pet nutrition’s alignment with metal’s oxygen-barrier features. Pharmaceutical and nutraceutical applications occupy an emerging frontier, leveraging tamper-evidence and precise metering features of small-volume aluminum vials. Collectively, end-user diversification further insulates the aluminum cans market against single-category downturns while providing multiple growth vectors that absorb manufacturing overhead and accelerate asset payback.

By Structure: 2-Piece Technology Commands Efficiency

The aluminum cans market size for 2-piece bodies represented 65.48% of global revenues in 2025 and will expand at 4.48% through 2031 as draw-and-wall-iron lines run above 2,000 cans per minute with minimal scrap rates. Removing a longitudinal seam eliminates an entire weld and inspection step, slashing energy consumption and lowering inclusion defects. Continuous lightweighting cuts can body thickness by 35% relative to 2000-era gauges, producing significant metal savings without sacrificing top-load strength. Crown’s 2024 deployment of high-speed two-piece lines in Brazil illustrates a large-scale commitment to the platform [CROWNCORK.COM]. While 3-piece constructions remain useful for oversize formats or intricate shapes, they experience sub-3% growth as beverage brands increasingly standardize on 2-piece bodies for CAPEX optimization.

Emerging draw-redraw (DRD) and impact-extrusion processes open additional avenues for shaped aerosol, wine, and spirits bottles where brand identity commands premium shelf prices. Ball’s acquisition of Spain-based Alucan adds DRD expertise that dovetails with aspirational personal-care and household categories. Over the forecast period, structural innovations look set to consolidate around 2-piece tactility complemented by niche extruded offerings, a mix that preserves efficiency while satisfying brand-driven differentiation demands. Consequently, production planners maintain high asset turnover, while suppliers of compounds, rings, and ends anchor MRO ecosystems that support sustained equipment uptime.

By Capacity: Mid-Size Leads, Small-Format Grows Fastest

Cans ranging from 251-500 mL accounted for 52.57% of global revenue in 2025, cementing their role as the universal single-serve drink size across most cultures. Their geometry perfectly balances refreshment volume, brand artwork surface area, and pack out density on standard pallets. Even so, sub-250 mL formats, including 150 mL mini-sodas and 187 mL wine spritzers, are witnessing the steepest climb at 4.16% CAGR through 2031. Health-conscious consumers perceive smaller servings as portion-controlled and calorie-responsible, enabling premium price points on a per-ounce basis. Craft cocktail brands exploit mini-cans for mix-and-match variety packs that encourage trade-up and exploration.

Conversely, cans above 500 mL serve large family or value-seeking segments, yet they wrestle with cooler-door real estate and incremental taxation in markets assessing volumetric alcohol duties. Still, 568 mL “tall-boys” remain culturally entrenched in several European beer segments, offering opportunistic volume growth aligned with sporting events and festival seasons. On the manufacturing front, one format does not cannibalize another; modern body makers can swap tooling within a shift, allowing plants to flex output in line with regional merchandising programs. Hence, diversified capacity enables the aluminum cans market to accommodate both premium micro-serves and mainstream thirst-quenchers.

Geography Analysis

Asia Pacific contributes 40.74% of global sales, and its aluminum cans market size is projected to advance 5.52% annually to 2031, underwritten by rising middle-class disposable incomes, urban convenience culture, and authoritative restrictions on single-use plastics in China, India, and Japan. China retains pole position with in-house rolling capacity and a vibrant domestic beverage sector that collectively eclipses import dependence. Hindalco’s USD 10 billion expansion amplifies India’s domestic metal supply in anticipation of can adoption by local cola, energy drink, and alcopop producers. Japan’s mature beverage environment spurs innovation in premium tea and craft coffee cans, aided by Asahi Group’s net-zero pledges driving procurement switch-overs. Southeast Asia is equally dynamic; NS-Siam United Steel allocated USD 58.5 million to bolster tinplate output, yet concurrently partners with foreign can-sheet suppliers, signaling blended development paths for both ferrous and aluminum supply chains.

North America ranks second in absolute size, though its unit volumes plateau. Instead, the region focuses on trading up to sleek, slim, and specialty thermochromic cans that fetch higher margins. Ball shipped roughly 49 billion containers in 2023, representing 36% regional aluminum cans market share and delivering significant recycled content progress as reclamation systems scale. U.S. state-level container deposit expansions plus Canada’s EPR rollouts strengthen secondary scrap supply, raising recycled content in can body sheet to record highs and lowering metal purchase costs for converters.

Europe, while mature, leans heavily on regulatory levers to accelerate modal shift from PET to aluminum. With the EU’s 90% collection target looming, brand owners pre-pay for compliance by booking multi-year aluminum can supply contracts that stabilize converter order books. The United Kingdom’s upcoming deposit return program will funnel 14 billion metal containers into closed-loop paths yearly, solidifying feedstock security. Germany and France aggressively promote wine-in-can pilots, expanding beyond beer’s established foothold. These factors allow European producers to deploy new capacity while raising line speeds and integrating on-site renewable energy, ensuring that the aluminum cans market in the bloc grows in value even where volumes edge upward modestly.

Regulatory Landscape

Policy is increasingly shaping aluminum can demand through packaging EPR rules, deposit-return systems, and recyclability requirements. In Europe, Regulation (EU) 2025/40 on packaging and packaging waste (PPWR) generally applies from August 12, 2026, reinforcing design-for-recyclability and labeling expectations and linking market economics to collection performance, including the 90% collection target for metal beverage cans by 2029 referenced in EU guidance.

In the United Kingdom, the Producer Responsibility Obligations (Packaging and Packaging Waste) (Amendment) Regulations 2025 came into force on January 1, 2026, and they operate alongside DEFRA-administered EPR obligations (including PRN-based compliance), with a 2026 aluminum recycling business target set at 62%. In the United States, supply-chain and recycling-flow visibility gained legislative attention in 2026 through House-introduced bills including the Counting Aluminum Net Surplus (CANS) Act (H.R. 7992), which mandates ongoing study of aluminum landfill waste and scrap market flows, and the Secure Aluminum Supply Chains Act, which directs the USITC to investigate risks tied to aluminum scrap exports to nations of concern.

Value Chain Analysis

The aluminum can value chain runs from upstream bauxite and alumina to primary aluminum smelting, then into rolling mills producing can body, end, and tab stock. Can makers form cans, predominantly via two-piece drawing and wall ironing, before supplying brand owners for filling and distribution, with downstream performance tied to line speed, decoration and printing capability, and quality-control systems.

Secondary aluminum is a key linkage in the chain, especially Used Beverage Cans (UBCs), which are remelted and cast into rolling ingot to support closed-loop can-to-can supply. Facilities such as Constellium’s Muscle Shoals operation are positioned around this recycling-to-rolling interface. Industry coordination also helps stabilize circular feedstock: the Global Beverage Can Circularity Alliance (GBCCA), founded during COP28 with members including the International Aluminium Institute, the Can Manufacturers Institute, and the Aluminum Association, targets 80% global recycling by 2030 and near 100% by 2050, aligning brands, recyclers, and sheet suppliers around higher recovery and recycled-content availability.

Competitive Landscape

The aluminum cans market shows high concentration; Ball Corporation, Crown Holdings, and Ardagh Metal Packaging together hold about 60% of global revenues, enabling economies of scale in can-sheet sourcing, end-manufacturing, and logistics. Ball commands roughly 36% of North America, shipping 49 billion units in 2023 via 13 regional plants that offer just-in-time deliveries to the continent’s largest fillers. Crown Holdings leverages geographic diversification, deriving more than 40% of segment income from Latin America after recent plant expansions in Brazil. Ardagh maintains long-term sheet supply agreements, most recently extending a North American pact with Novelis in January 2024, signaling buyer strength in upstream metal procurement.

Consolidation continues: Sonoco acquired Eviosys for USD 3.9 billion in December 2024, instantly combining Europe’s second-largest food-can network with Sonoco’s North American base, unlocking USD 100 million synergy potential. Ball purchased Florida Can Manufacturing and Spain-based Alucan to fortify regional supply networks and obtain extruded aerosol technology, respectively. Smaller regional players seek competitive footholds through specialty printing, quick-changeover capability, or local-government incentives that offset higher scrap premiums. Technology races center on bisphenol-free internal coatings, hydrogen-ready annealing furnaces, and AI-enabled vision inspection that together drive down defect rates and bolster sustainability credentials. With brand owners tightening Scope-3 accounting, suppliers that demonstrate high recycled content and low carbon footprints enjoy preferred-vendor status.

Overall, the aluminum can industry balances economies of scale with targeted innovation, ensuring that even as top players consolidate, niches remain open for agile entrants focusing on design, sustainability, or regional service niches. Anti-trust regulators in major jurisdictions maintain watchful eyes on M&A trends, but to date, plant divestitures and contract manufacturing partnerships have kept market contestability intact.

Aluminum Cans Industry Leaders

Ball Corporation

Crown Holdings, Inc.

Silgan Holdings Inc.

Ardagh Group S.A.

CAN-PACK S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions in emerging beverage markets are creating whitespace as can penetration rises and local supply remains constrained. In India, Crown Holdings announced in April 2026 a state-of-the-art, two-line beverage can facility in Northern India with estimated annual capacity of 2.2 billion cans, while AGI Greenpac commenced construction in May 2026 on an aluminum beverage can plant in Hathras, Uttar Pradesh, with planned annual capacity of 1.6 billion cans. Together, these moves point to faster localization of can-making near fast-growing filling ecosystems.

Recycling and can-to-can conversion also offer a practical opportunity set, supported by measured collection performance and named projects. European Aluminium and Metal Packaging Europe reported a 76.3% aluminum beverage can recycling rate across the EU, UK, Switzerland, Norway, and Iceland for 2023, indicating a large, bankable UBC stream. Novelis is expanding its Latchford, UK, recycling plant to more than double beverage can recycling capacity to 85,000 tonnes per year by late 2026, and the gap between collection and true can-to-can recycling, where only a minority of recycled cans return to can sheet, still leaves room for investment in sorting, de-coating, and specification alignment with rolling mills alongside policy targets such as the EU’s 2029 collection benchmark.

Recent Industry Developments

- May 2026: Ball Corporation confirmed that its Millersburg, Oregon, beverage can facility is planned to be commissioned in late 2026, with capacity committed through long-term customer offtake agreements. The announcement points to how new North American can-making capacity is being underwritten by contracted demand as suppliers manage high utilization and reduce exposure to spot-volume swings.

- May 2025: Crown added a high-speed beverage can line in Ponta Grossa, Brazil, to support expanding can demand across Latin America. The additional line improves regional responsiveness for beverage customers and supports Crown’s strategy of using Latin American expansions to balance its global capacity footprint.

- October 2024: Ball launched Dynamark Advanced Pro variable graphics across EMEA lines to expand personalization and shorter-run design capability for beverage brands. The upgraded decoration flexibility gives converters more room to capture premium and promotional volumes without requiring large inventory builds, supporting brand experimentation across standard and sleek formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The aluminum cans market is defined as the value generated from manufacturing and selling aluminum can bodies and ends used to pack beverages, food, aerosols, and other consumer or industrial products, across global trade and domestic supply.

Scope exclusions: this sizing excludes non-can aluminum packaging formats such as foil-based packs, trays, and flexible laminates, and it also excludes steel cans unless the item is an aluminum can.

Segmentation Overview

- By Type

- Standard

- Sleek

- Slim

- Other Types

- By End-user Industry

- Beverage

- Alcoholic Beverages

- Non-alcoholic Beverages

- Food

- Canned Food

- Pet Food (Wet and Treats)

- Aerosol

- Other End-user Industries

- Beverage

- By Structure

- 2-piece

- 3-piece

- By Capacity

- Up to 250 ml

- 251 - 500 ml

- More than 500 ml

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Malaysia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand and supply setting using public statistics that are easy to trace. We referred to sources such as UN Comtrade for trade flows of aluminum packaging and related inputs, USGS for aluminum industry context, World Bank and IMF macro indicators for consumption and inflation context, and government environment agencies for recycling targets and packaging rules that impact can adoption.

After that, company filings, investor presentations, press releases, and packaging association publications were used to map capacity additions, regional production footprints, and typical can formats in circulation. When needed, paid subscriptions that consolidate company financials and news were used to cross-check production changes, while an import and export shipment-level database was used selectively to validate directional trade patterns for cans and input movements. The desk sources listed here are illustrative, and we checked other public documents for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys across can makers, can-end suppliers, beverage and food packers, and packaging procurement teams, followed by discussions with recyclers and industry bodies to keep recovery-rate assumptions realistic. Because this is a global market, we balanced perspectives across APAC, EMEA, and the Americas so regional differences in can penetration and pricing could be reflected, then cross-checked back to the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 20% | APAC: 41% |

| Mid tier: 40% | Functional/Unit leaders: 26% | EMEA: 34% |

| Smaller Players: 21% | Managers: 54% | Americas: 25% |

Market-Sizing & Forecasting

The core sizing uses a top-down build where packaging demand is reconstructed from end-use consumption pools and then filtered through aluminum can penetration by region and product category. To keep the totals realistic, we corroborate with selective bottom-up approximations, such as sampled can-line capacity signals, can format mix checks, and price-per-thousand-can sanity checks discussed with industry participants.

Key inputs include beverage volume trends (carbonated drinks, beer, and ready-to-drink segments), shifts in packaging preferences from plastic to metal, average can weight and lightweighting pace, recycling rates and recycled content commitments, and regional capacity utilization patterns that affect availability and pricing. When bottom-up signals were incomplete for smaller countries, we used proxy ratios based on beverage output and import dependence, and then rechecked the implied per-capita can usage so the outcome stays plausible.

For forecasting, scenario analysis was used with a central case anchored to expected beverage growth and policy-led recycling improvements, then adjusted with expert views on can-price movement and capacity additions. Assumptions were kept in USD terms with consistent currency timing so year-to-year changes reflect market movement rather than conversion noise.

Data Validation & Update Cycle

Validation is handled through multiple passes of triangulation across demand indicators, supply capacity signals, and trade direction checks, followed by variance reviews at regional and global totals. If pricing or volume outputs move outside expected bands, we re-test the drivers, and we trigger targeted re-contacts with interviewees to confirm whether the shift is real or model-driven.

Before sign-off, the model and assumptions go through analyst review steps that include anomaly checks, unit consistency checks, and cross-year continuity checks so spikes are explained and documented. Reports are refreshed annually, with interim updates made when material events occur, and a final pre-delivery check is completed so clients receive the latest updated view.

Mordor Intelligence's Aluminum Cans Market Sizing Compared With Other Published Estimates

Published market values for aluminum cans can differ across sources, even when the topic name is the same, because the scope and the counting logic are not always aligned. The benchmark table highlights how the base year timing, what is included as an aluminum can, and how pricing is treated can move the number up or down.

A common gap driver is whether the estimate is centered on complete aluminum can systems across beverage, food, and aerosol uses, or whether it leans more heavily toward beverage-only demand signals and then scales to other uses with broad ratios. Another driver is the pricing path, where some estimates assume faster can price inflation or do not normalize for lightweighting, recycled content, and regional mix shifts, which can change the value outcome even if unit volumes are similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 58.13 B (2026) | |

| Industry Publisher A | USD 63.20 B (2025) | Uses a 2025 base year and a broader value build that can pull forward inflation and mix effects, which makes direct comparison to a 2026 starting point sensitive to pricing and currency timing. |

| Global Publisher B | USD 53.70 B (2025) | Leans on a different base-year anchor and may apply a tighter interpretation of which non-beverage can applications are counted, which can compress the value total in early years. |

The table shows a spread that is largely explained by base-year choice and how adjacent packaging formats and non-beverage uses are treated. In Mordor Intelligence's model, the 2026 value is tied to aluminum can demand across beverage, food, aerosol, and other end uses, with pricing normalized for regional mix and lightweighting so the total stays traceable to clear volume and price drivers.

Key Questions Answered in the Report

What is the projected value of the aluminum cans market by 2031?

It is forecast to reach USD 70.72 billion by 2031, growing at a 4.01% CAGR.

Which region leads demand growth for aluminum beverage cans?

Asia Pacific tops both current share and forecast growth, expanding at a 5.52% CAGR through 2031.

Why are sleek cans gaining popularity among beverage brands?

Sleek formats support premium positioning, deliver distinctive shelf presence, and are expected to grow 4.06% annually.

How do deposit return systems influence aluminum can demand?

Mandated 90% collection rates raise recycled content, lowering material costs and strengthening preference for aluminum containers.

What is the biggest restraint facing can makers today?

Volatility in primary aluminum prices, coupled with supply deficits forecast for 2030, poses the greatest cost pressure.

Which end-user segment is expected to expand fastest?

Aerosol applications lead with a 5.21% CAGR as personal care and household brands pursue recyclable metal packaging.

Page last updated on: