Aluminium Forging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

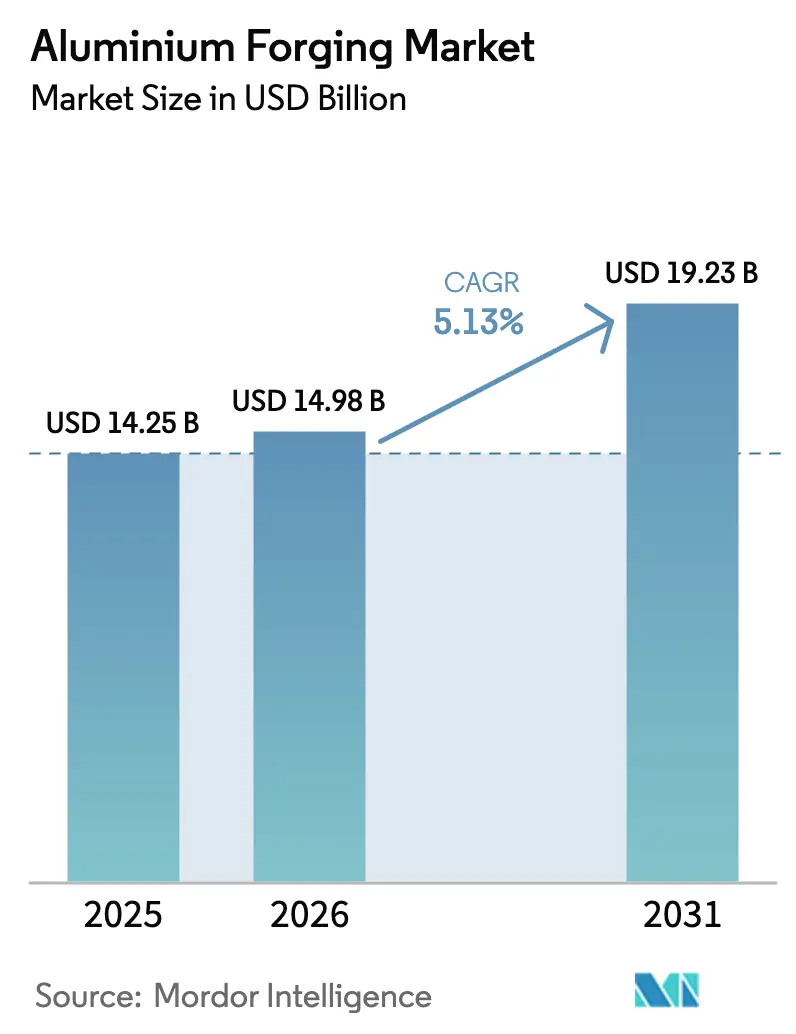

| Market Size (2026) | USD 14.98 Billion |

| Market Size (2031) | USD 19.23 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminium Forging Market Analysis by Mordor Intelligence

aluminium forging market size in 2026 is estimated at USD 14.98 billion, growing from 2025 value of USD 14.25 billion with 2031 projections showing USD 19.23 billion, growing at 5.13% CAGR over 2026-2031. Rising demand for lighter vehicles, stricter emission standards, and the material’s compatibility with existing press lines underpin this outlook, giving the aluminium forging market a structural edge over steel. OEMs are integrating forged aluminium suspension arms, control arms, and power-dense aerospace components to cut vehicle curb weight, extend EV range, and lower life-cycle emissions. Regional supply chains are also shifting as policymakers implement carbon taxes and local-content rules, prompting onshore capacity additions that tighten the aluminium forging market and open new revenue streams for certified suppliers. Price volatility on the London Metal Exchange and rising energy costs are compressing unhedged margins, yet forward-integration moves by top players are mitigating the impact.

Key Report Takeaways

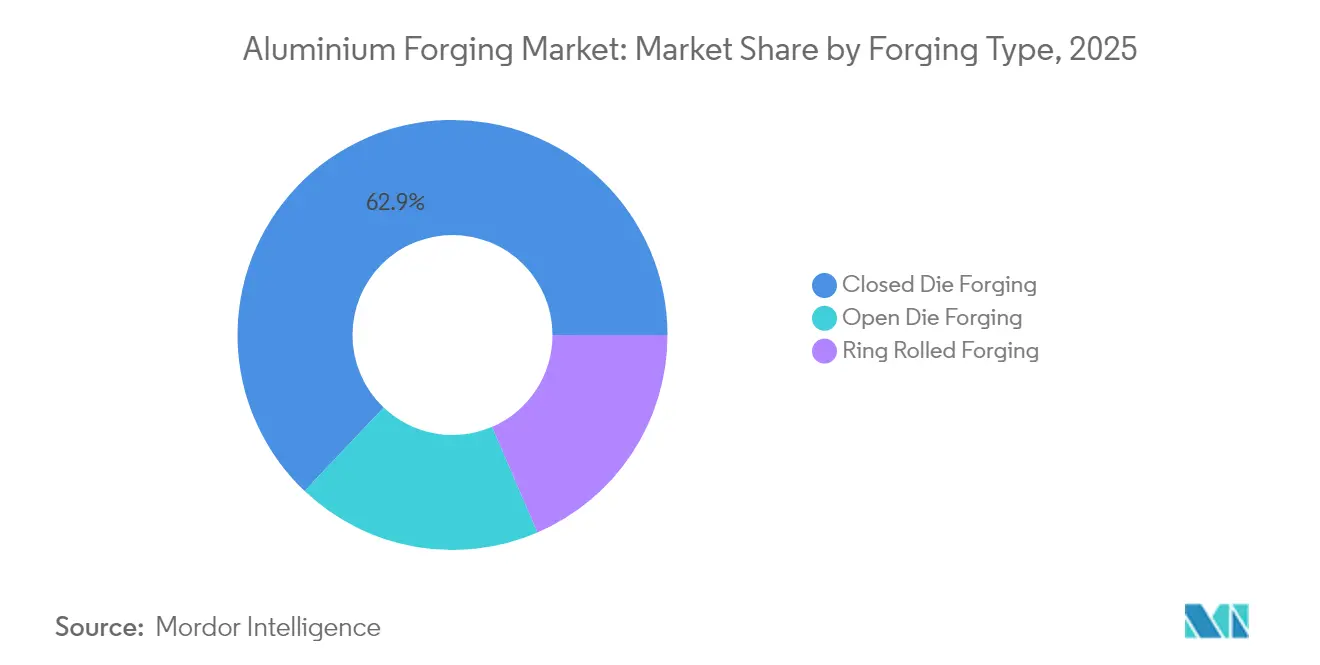

- By forging type, closed-die captured 62.93% of the aluminium forging market share in 2025, and is projected to expand at a 5.24% CAGR through 2031.

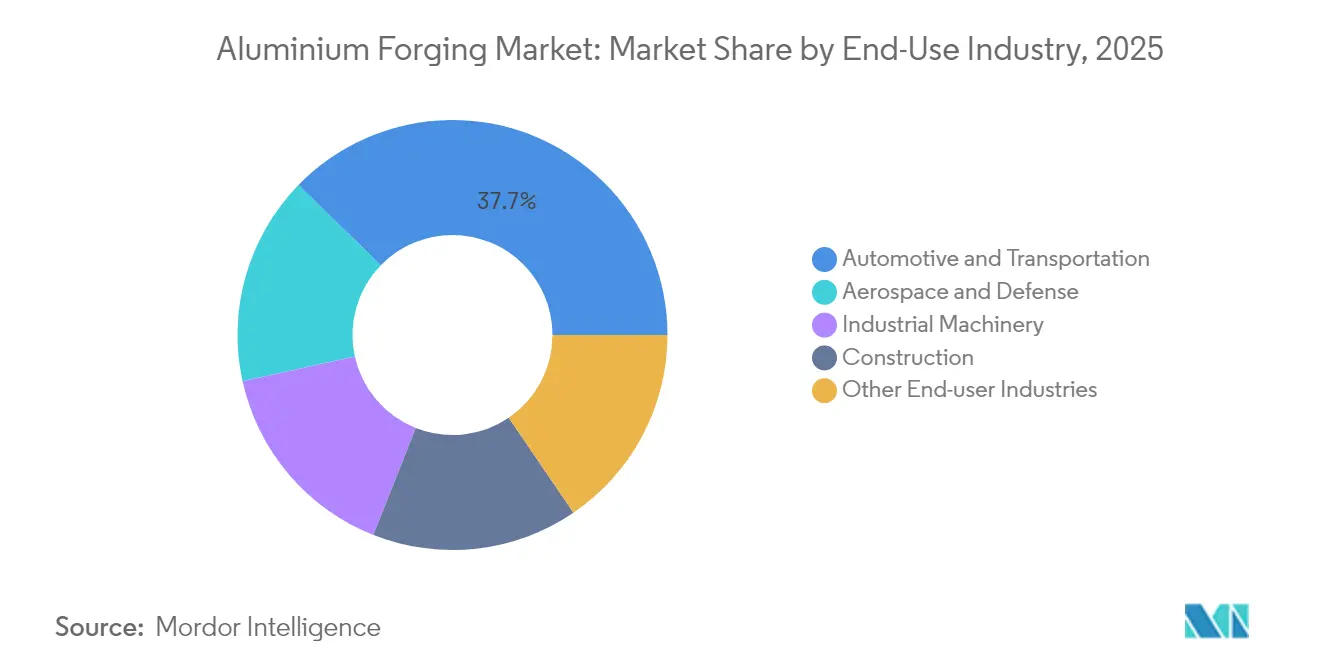

- By end-use industry, the automotive and transportation sector led with a 37.71% share of the aluminium forging market size in 2025; the aerospace and defense sector is advancing at a 5.47% CAGR to 2031.

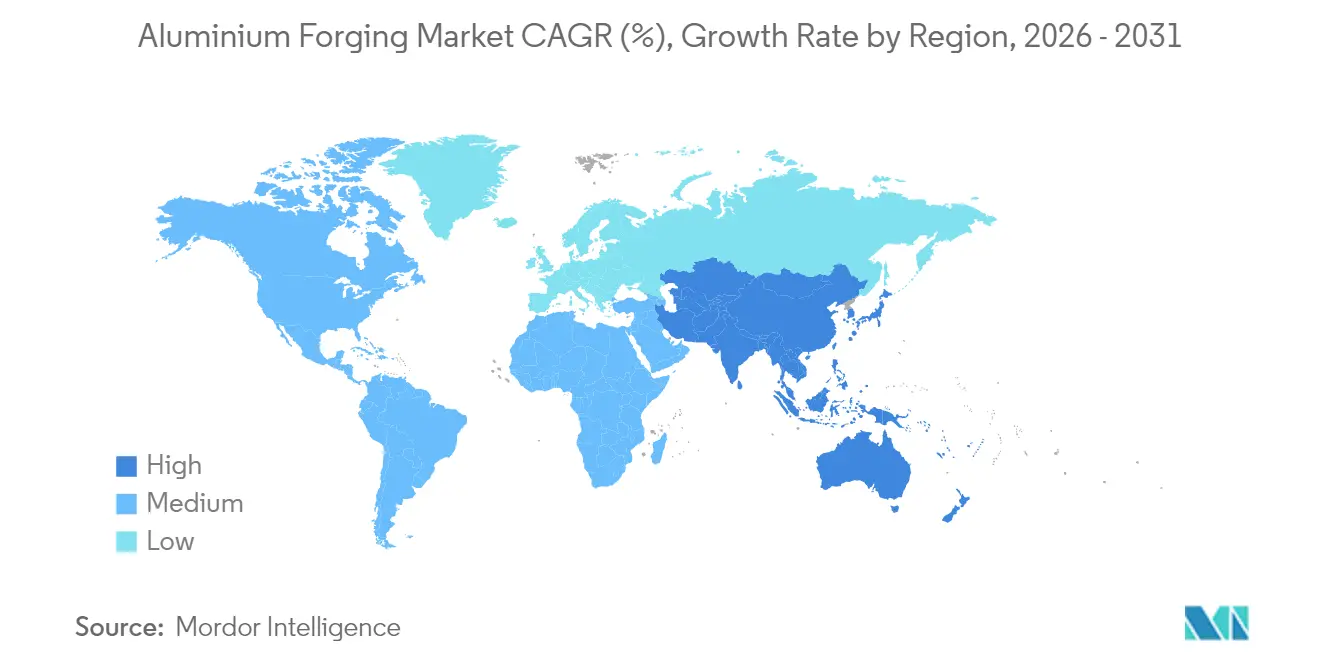

- By geography, the Asia-Pacific region commanded 37.97% of 2025 revenue and is forecast to post a 6.35% CAGR through 2031, the fastest regional expansion in the aluminium forging market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aluminium Forging Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing use of lightweight materials | +1.2% | Global, concentrated in North America, Europe, and China | Medium term (2-4 years) |

| Surging EV-oriented automotive demand | +1.5% | APAC core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Rising aero-engine backlog | +0.9% | North America, Europe, emerging in India and Turkey | Long term (≥ 4 years) |

| Hydrogen-ready gas-turbine build-out | +0.4% | Europe, Middle East, Japan | Long term (≥ 4 years) |

| Local-content mandates | +0.7% | India, Southeast Asia, Middle East, Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Use of Lightweight Materials Across Industrial Sectors

Automotive and aerospace OEMs report a 40-50% reduction in component weight when aluminium forgings replace steel, resulting in a 6-8% range extension on 75 kWh EV packs[1].Ramkrishna Forgings, “Investor Presentation 2024,” ramkrishnaforgings.com Even advanced high-strength steel grades remain 2.9 times denser than aluminium, forcing trade-offs between payload and fuel economy. Industrial robotics firms are adopting forged aluminum manifolds and joints to reduce arm inertia, thereby shortening pick-and-place cycles by 200 ms and increasing throughput over three shifts. Construction equipment manufacturers specify forged aluminum for booms and jibs to comply with axle-load limits, thereby unlocking higher legal payloads without incurring highway permit penalties. Aerospace remains the most weight-sensitive user; each kilogram trimmed from an airframe saves about USD 3,000 in fuel during a 20-year life, making aluminium-lithium forgings preferable to composites for cryogenic tank domes and fuselage frames.

Surging Demand from EV-Oriented Automotive and Transportation OEMs

Ramkrishna Forgings invested INR 57.5 crore (approximately USD 6.9 million) in 2024 to create a 3,000 tpa aluminium forging capacity for EV suspension arms and battery-tray brackets. ILJIN’s USD 100 million Alabama greenfield plant, announced in October 2024, will supply forged control arms to General Motors and Stellantis by Q3 2026. Mass reduction remains a key selling point; a 20 kg weight cut in unsprung parts yields an 8 km range gain on a 400-km EV, a critical margin in consumer purchase decisions. Fleet operators see analogous savings in commercial-vehicle electrification, as forged aluminium wheel hubs and steering knuckles lower rolling resistance and total cost per tonne-kilometer.

Rising Aero-Engine Backlog Driving Closed-Die Orders

Safran’s 2024 contract with Hindustan Aeronautics covers aluminium fan blades and casings for LEAP turbines, highlighting supply constraints in closed-die capacities. Turkish Aerospace reported 18-month lead times for critical aluminum forgings, compared to a historic 10-month norm, which delayed trainer-aircraft deliveries. Bharat Forge’s October 2025 Rolls-Royce deal adds Indian capacity for Pearl 10X business-jet fan blades, underscoring the OEM's willingness to qualify new AS9100D vendors. Aluminium-lithium alloys with 7-10% lower density than 2000-series alloys enable 150 kg of engine weight savings and a 2% reduction in fuel burn over 3,000 hours.

Hydrogen-Ready Gas-Turbine Build-Out

The EU-funded H2AL project is refining heat-treatment routes that maintain the stability of 6000-series aluminium above 300 °C, a requirement for hydrogen combustor liners. Siemens Energy and General Electric test hydrogen-capable turbines in Germany and the Netherlands, specifying forged aluminium casings that lower foundation costs by 10-15%. NEOM in Saudi Arabia and Japan’s ammonia co-firing push create parallel demand for corrosion-resistant valve bodies and actuator housings.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminium LME price volatility | -0.8% | Global, acute in Southeast Asia and Latin America | Short term (≤ 2 years) |

| Stringent aerospace defect-detection norms | -0.5% | North America, Europe, expanding to India and Turkey | Medium term (2-4 years) |

| Energy-intensive operations facing carbon tax | -0.4% | EU, UK, future CBAM regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aluminium LME Price Volatility and Hedging Costs

LME prices fell 20% from USD 2,600 per tonne in early 2024 to USD 2,080 in December, squeezing margins for spot-exposed forgers. Options premiums on 12-month collars widened to 4.5% of notional in 2024 versus 2.8% a year earlier, while the U.S. Midwest premium spiked to USD 1,323 per tonne in June 2025 on tariff-driven logistics snarls. Smaller Southeast Asian and Latin American suppliers lack access to sophisticated hedges and forfeit 8-12% of their margin to tolling structures. Japan’s quarterly premium jumped 30% to USD 228 per tonne in Q1 2025 on scrap scarcity and LNG-linked power costs.

Stringent Defect-Detection Standards in Aerospace Supply Chains

AS9100D compliance mandates the ultrasonic detection of subsurface voids greater than 1.5 mm, along with X-ray and full traceability, which raises capital expenditures by USD 2–5 million for mid-tier entrants. OEMs tightened sampling after Pratt & Whitney’s 2024 powder-metal recall, with some requiring 100% volumetric inspection FT.COM. Billet chemistry certificates must be archived for 20 years, which prolongs qualification to 24–36 months and delays revenue for new suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Forging Type: Closed-Die Dominance Reflects Near-Net-Shape Economics

Closed-die processes held a 62.93% share of the aluminium forging market in 2025 and are projected to expand at a 5.24% CAGR, driven by ±0.5 mm tolerances that eliminate secondary machining in high-volume automotive and aerospace parts. Investments such as Aubert & Duval’s EUR 75 million 60-MN press, due online in 2027, underline expectations of a sustained aero-engine backlog.

Ring-rolled forging retains niche status for bearings and pressure-vessel rings where weld-free geometry is indispensable. Open-die forging remains the preferred method for producing ultra-large parts exceeding 50 kg; China’s 16,500-tonne Tai’an press underscores the state's support for the nuclear and petrochemical markets. Digital simulation platforms, such as FORGE NxT 4.1, reduce prototype cycles from five to two, thereby reducing scrap and energy costs across all forging types.

By End-Use Industry: Aerospace Grows Fastest Despite Automotive’s Volume Lead

Automotive and transportation, at 37.71% of 2025 volume, remain the largest slice of the aluminium forging market. However, the aerospace and defense sector is the fastest-growing end-use, posting a 5.47% CAGR to 2031, driven by demand for engines and airframes. Aerospace’s price premia—USD 8,000–12,000 per forged fan blade—raise the aluminium forging market size for the segment, even at modest unit counts. The aluminium forging market share for the aerospace industry is therefore projected to rise by 2.1 percentage points by 2031.

Industrial machinery users prefer forged aluminium hydraulic manifolds due to their higher thermal conductivity of 237 W/mK, compared to 50 W/mK for steel, which enables air cooling in high-duty cycles. Construction equipment builders specify forged aluminium booms to meet axle-load caps, while oil-and-gas players apply ring-rolled closures for 10,000 psi wells.

Geography Analysis

The Asia-Pacific region dominated the aluminium forging market with a 37.97% share in 2025, a position expected to widen at a 6.35% CAGR through 2031. China’s withdrawal of its 13% aluminium semi-finished products rebate in December 2024 increased landed costs for ASEAN buyers, prompting them to consider long-term tolling deals. India’s aluminium forging market is gaining momentum, driven by a per-capita consumption that lags behind the global average by a factor of four. A USD 40 billion investment in smelting expansion is needed to meet a demand of 10 million tonnes per annum by 2030.

North America’s outlook improves with ILJIN’s USD 100 million Alabama plant, which will supply EV control arms starting in Q3 2026, recapturing volume lost to Mexico. Europe consolidates around aerospace; Aubert & Duval’s new press and EGA’s 30,000 tpa recycled billet line in Germany support local circular-economy mandates. South America and the Middle East remain import-led for complex, closed-die parts, although Saudi Arabia’s NEOM and Brazil’s defense offsets are expected to foster joint ventures that will increase in-region share post-2026.

Competitive Landscape

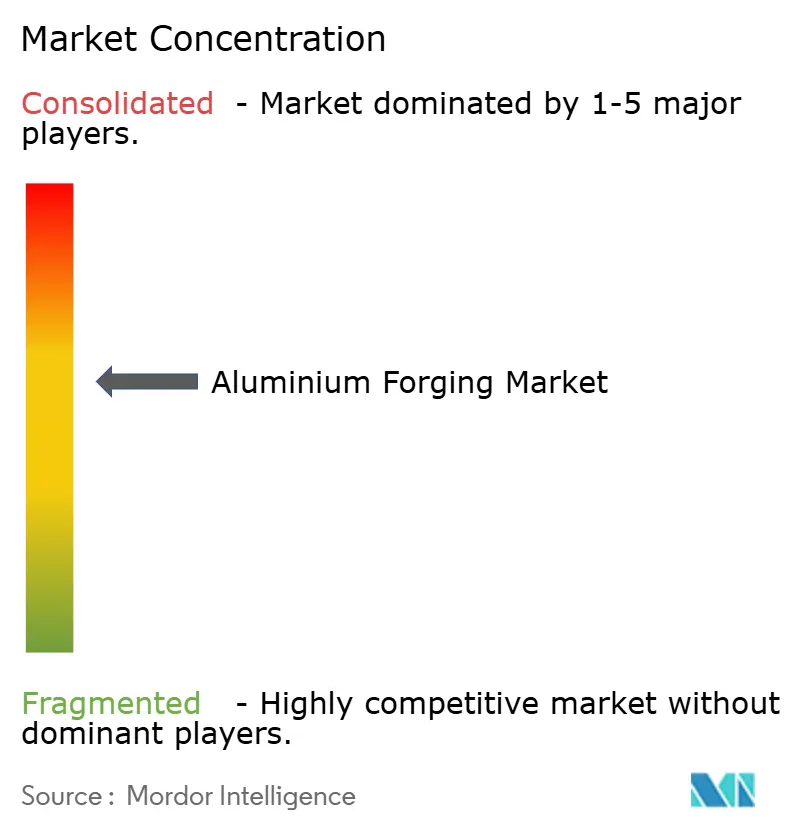

The global aluminium forging market is moderately fragmented. The top five forgers hold a significant share of the global market, while regional specialists compete through proximity and shorter lead times. Technology adoption differentiates leaders; predictive-maintenance software reduces unscheduled downtime to 3% from 8%, thereby increasing utilization. Aluminium-lithium forgings for space launchers represent white-space growth, with third-generation alloys offering 7-10% density reductions. Indian and Turkish disruptors leverage 40% lower overhead and AS9100D compliance to underbid Western incumbents by 15-20% on aero-engine parts.

Aluminium Forging Industry Leaders

Howmet Aerospace

Bharat Forge

Nippon Steel Corporation

Thyssenkrupp AG

Aluminum Precision Products

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Bharat Forge signed a multi-year Rolls-Royce deal to supply Pearl 10X forged aluminium fan blades, its first entry into business-aviation engines.

- October 2024: ILJIN Co., Ltd. announced a USD 100 million investment in a new aluminium forging facility in Alabama, creating 160 jobs and producing forged control arms for General Motors and Stellantis electric-vehicle platforms starting Q3 2026.

- June 2024: Bharat Forge invested USD 40 million in its U.S. aluminium subsidiary to install closed-die presses and machining centers, trimming lead times by seven weeks.

Global Aluminium Forging Market Report Scope

Aluminium forgings are produced by deforming wrought aluminium billets under compressive loads to achieve near-net structural shapes. The aluminium forging market is segmented by forging type, end-use industry, and geography. By forging type, the market is segmented into open die forging, closed die forging, and ring rolled forging. By end-use industry, the market is segmented into aerospace and defense, automotive and transportation, industrial machinery, construction, and other end-user industries. The report also covers the market size and forecasts for the aluminium forging market by geography, divided into five major regions, covering 32 countries worldwide. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Open Die Forging |

| Closed Die Forging |

| Ring Rolled Forging |

| Aerospace and Defense |

| Automotive and Transportation |

| Industrial Machinery |

| Construction |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Forging Type | Open Die Forging | |

| Closed Die Forging | ||

| Ring Rolled Forging | ||

| By End-Use Industry | Aerospace and Defense | |

| Automotive and Transportation | ||

| Industrial Machinery | ||

| Construction | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the aluminium forging market?

The aluminium forging market size is USD 14.98 billion in 2026.

How fast will demand grow through 2031?

Market revenue is projected to rise to USD 19.23 billion, equating to a 5.13% CAGR.

Which forging type holds the largest share?

Closed-die processes commanded 62.93% of 2025 revenue, benefiting from near-net-shape economics.

Which end-use segment is expanding the quickest?

Aerospace and defense is forecast to post a 5.47% CAGR through 2031 on engine and airframe backlogs.

Which region offers the fastest growth?

Asia-Pacific is projected to advance at 6.35% annually as China and India add capacity and consumption.

What is a key risk facing forgers?

Aluminium price volatility on the LME, with a 20% drop in 2024, threatens margins for unhedged suppliers.

Page last updated on: