Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

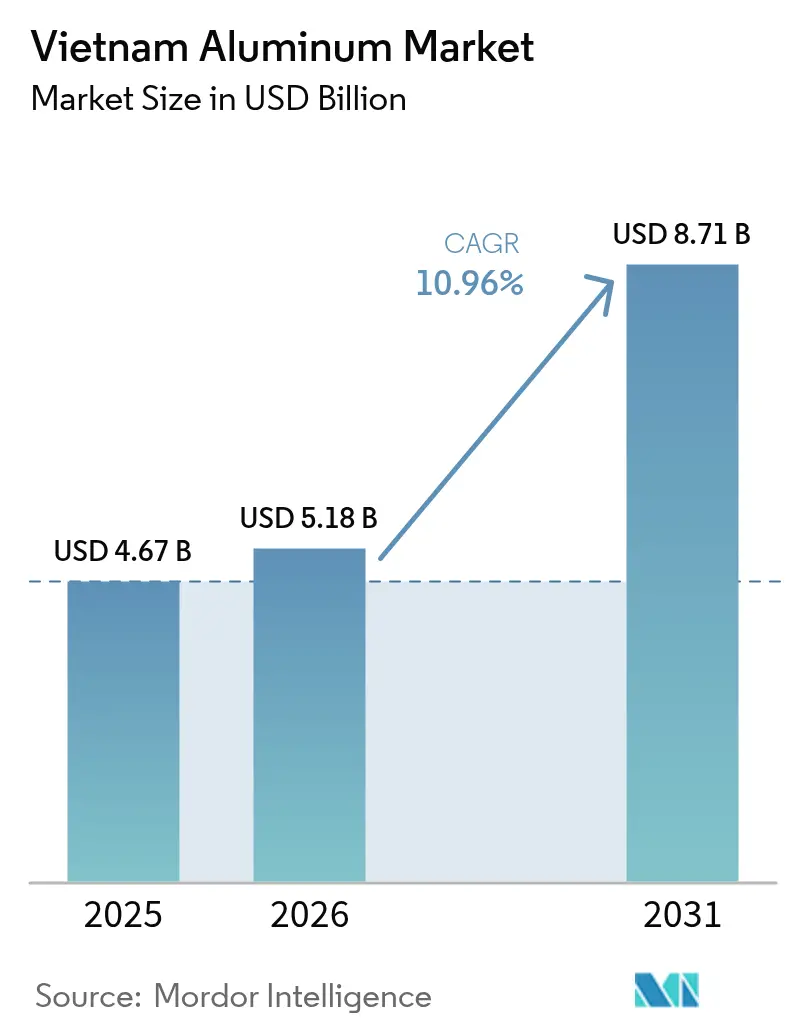

| Base Year Market Size (2025) | USD 4.67 Billion |

| Market Size (2026) | USD 5.18 Billion |

| Market Size (2031) | USD 8.71 Billion |

| Growth Rate (2026 - 2031) | 10.96% CAGR |

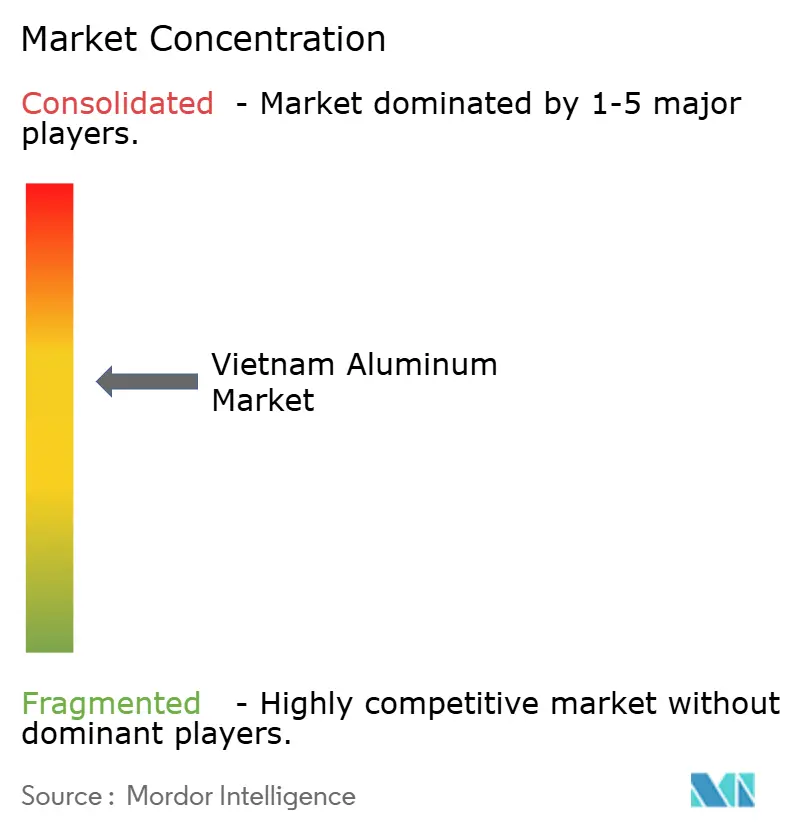

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Aluminum Market Analysis by Mordor Intelligence

The Vietnam Aluminum Market size is expected to grow from USD 4.67 billion in 2025 to USD 5.18 billion in 2026 and is forecast to reach USD 8.71 billion by 2031 at 10.96% CAGR over 2026-2031. This uptrend positions the Vietnam aluminum market among the fastest-growing value chains in Asia as abundant bauxite reserves, new alumina capacity, and demand from mobility and construction converge. Rising EV production, green-building mandates, and packaging circularity targets foster structural demand, while upstream security from 5.8 billion tonnes of bauxite supports long-term supply. Government Decision 866 authorizing eight processing facilities plus 19 exploration projects through 2030 further underpins growth, although capacity utilization still averages 70%, highlighting operational headroom.

Key Report Takeaways

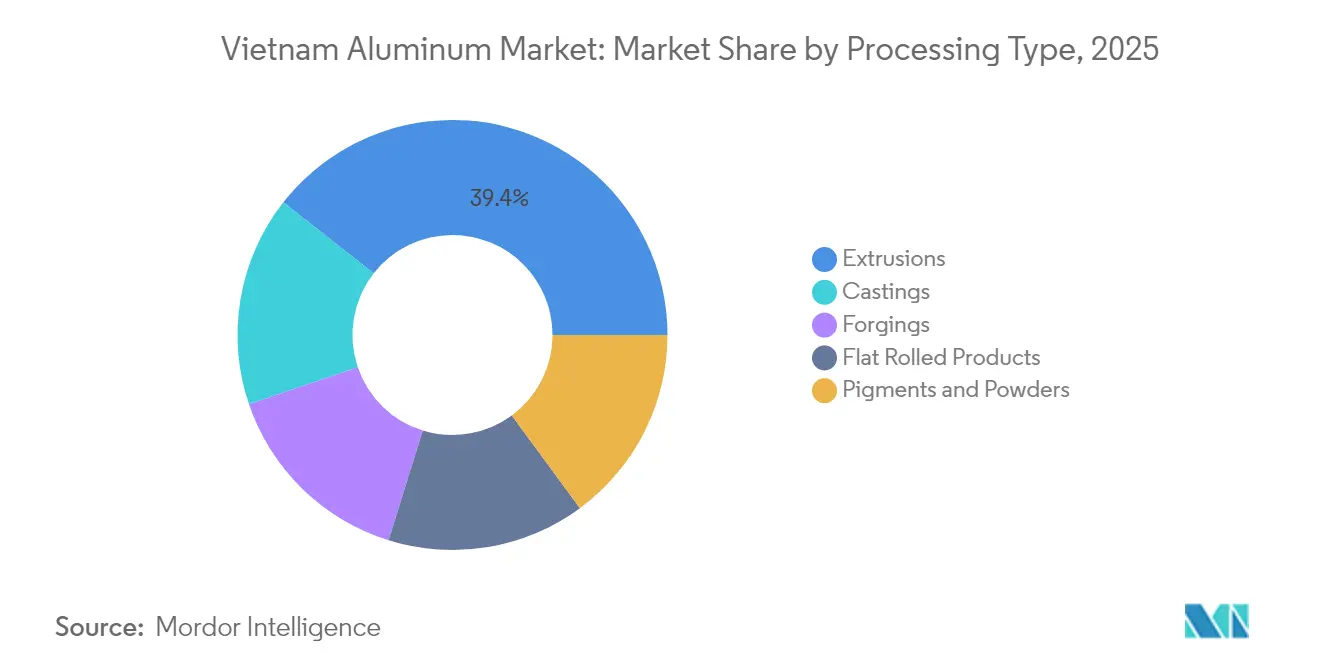

- By processing type, extrusions led with a 39.42% share of the Vietnam aluminum market in 2025, while castings are forecast to advance at a 13.62% CAGR to 2031.

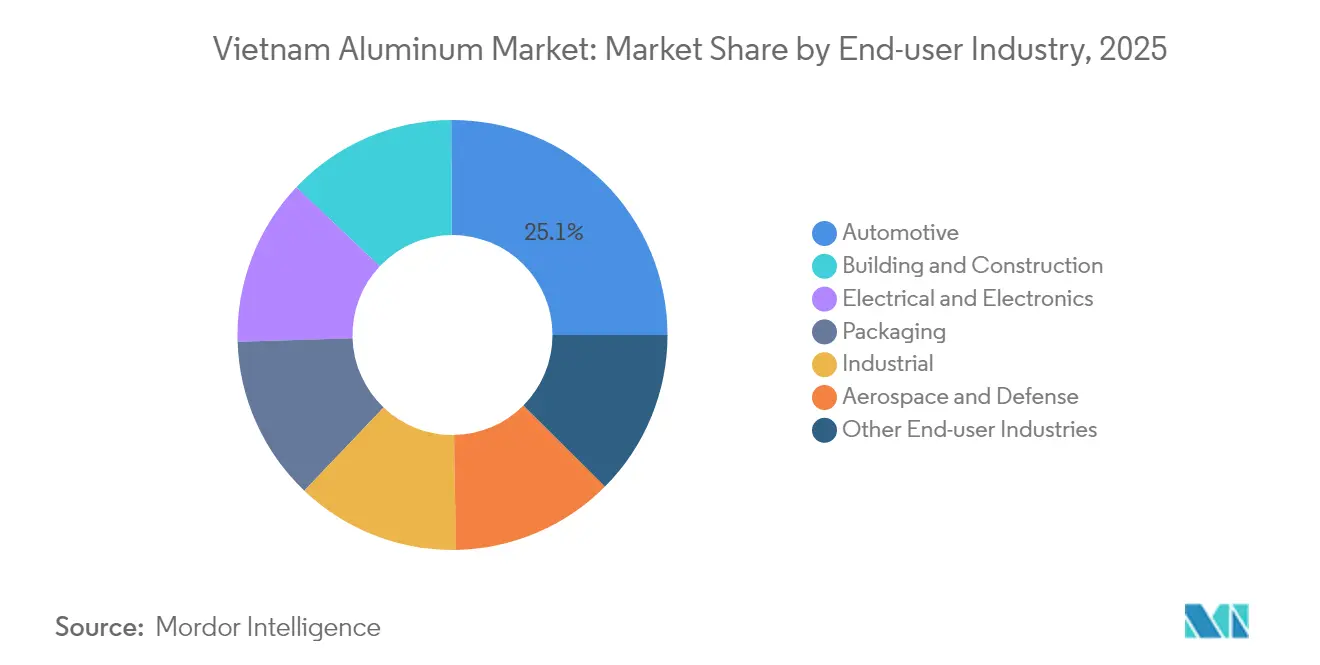

- By end-user industry, building and construction recorded a 12.74% CAGR outlook through 2031; automotive held 25.10% of the Vietnam aluminum market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Aluminum Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Auto-sector lightweighting push | +2.8% | Ho Chi Minh City and Hanoi automotive clusters | Medium term (2-4 years) |

| Booming public and green-building construction | +3.1% | National; early gains in Ho Chi Minh City, Hanoi, Da Nang | Short term (≤2 years) |

| Rebound in packaging demand | +1.4% | Industrial zones nationwide | Short term (≤2 years) |

| Expansion of bauxite and alumina projects | +2.9% | Central Highlands (Đắk Nông, Lâm Đồng) | Long term (≥4 years) |

| Rapid EV/battery-housing localization | +1.8% | Northern and southern manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Auto-sector Lightweighting Push

Automotive aluminum demand is reinforced by 858 IATF 16949-certified suppliers that integrate Vietnam into regional vehicle platforms. EV production uses nearly 30% more aluminum per unit than conventional models for battery enclosures and thermal systems, and Vietnam targets 50% electric urban vehicles by 2030. Local content policies fuel component outsourcing, while commercial fleets adopt aluminum parts to maximize payload and comply with emission norms. The World Bank estimates the EV transition could generate 6.5 million manufacturing jobs by 2050, a scenario that sustains metal demand across casting, extrusion, and flat-rolled supply chains. As OEMs expand capacity, the Vietnam aluminum market benefits from rising billet and ingot off-take, incentivizing new secondary smelters.

Booming Public and Green-Building Construction

Public spending of USD 30 billion in 2024 on transport and power facilities injected near-term demand for curtain walls, roofing, and structural extrusions. Green-certified buildings rose to 430 in Q1 2024, with EDGE and LEED accounting for 75.69% of certifications, favoring aluminum for its recyclability and thermal efficiency. Power Development Plan VIII earmarks USD 135 billion through 2030, driving aluminum demand for high-voltage structures and solar frames. Ho Chi Minh City’s USD 11.5 billion highway program and USD 1.2 billion of transport upgrades boost extruded profile consumption.

Rebound in Packaging Demand (Food-Drink and Pharmaceuticals)

Extended Producer Responsibility rules mandating 22% recycling of aluminum packaging from January 2024 create compliance-driven orders for can-sheet and foil. HEINEKEN Vietnam’s 850-tonne can-to-can pilot validated closed-loop recovery and spurred investment in rolling capacity. Beverage demand grows as per-capita consumption converges toward ASEAN averages, while pharma blister packs require high-barrier foil in an expanding healthcare sector. Vietnam’s 93% collection rate for beverage cans contrasts with only 1% domestic remelting into new cans, underscoring untapped value for the Vietnam aluminum market. Investors eye secondary smelters near industrial clusters to capitalize on scrap surpluses and CBAM-induced premium for low-carbon feedstock.

Expansion of Domestic Bauxite and Alumina Projects

Đắk Nông and Lâm Đồng contain 5.4 billion tonnes of reserves, or four times the aluminum resources of the U.S. and China combined. THACO’s USD 4 billion Tây Nguyên complex will raise alumina output by 4 million tonnes annually, while Hóa Chất Đức Giang’s USD 2.3 billion venture mines 14.4 million tonnes of ore per year. TKV plans to lift Lâm Đồng’s capacity to 2 million tonnes of alumina and build the country’s first 500,000-tonne primary smelter, closing a critical value-chain gap. Mastery of Bayer process technology and dry-red-mud handling reduces environmental risk and licensing costs. These projects will anchor feedstock security and decrease billet import dependence, bolstering the Vietnam aluminum market in the long run.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity tariffs and carbon pricing | −1.9% | Energy-intensive smelting regions nationwide | Medium term (2-4 years) |

| Cheap steel/plastics and composite substitutes | −1.2% | Construction and packaging markets | Short term (≤2 years) |

| Import dependence for primary metal and billets | −0.8% | Processing hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Electricity Tariffs and Carbon-Pricing Exposure

Aluminum smelting requires constant low-cost power, yet Vietnam’s average industrial tariff rose in 2024, compressing margins and limiting capacity use to 30-40% in some plants[1]Vũ Kim Ngan et al., “Border Carbon Adjustment Mechanisms and Impacts on Vietnam,” iisd.org. The EU’s Carbon Border Adjustment Mechanism affects USD 307.66 million of aluminum exports and could trim shipments by 4%, translating into USD 12 million revenue loss per year. Power Development Plan VIII calls for market-based pricing, pressuring electrolysis projects unless they secure renewables. Exporters must cut carbon intensity or pay CBAM fees that erode the Vietnam aluminum market’s cost advantage.

Import Dependence for Primary Metal and Billets

Vietnam performs five of six aluminum value-chain stages but lacks commercial-scale primary smelting, creating reliance on imported ingots from Malaysia, China, and the Middle East. Chinese alloy ingots accounted for 7.9% of imports, totaling 95,700 tonnes in 2024. U.S. investigations into Chinese transshipment through Vietnam resulted in antidumping duties of 14.15% on cooperative exporters and 41.84% on non-compliant firms[2]U.S. Department of Commerce, “Aluminum Extrusions From the Socialist Republic of Vietnam,” federalregister.gov. A 25% U.S. Section 232 tariff applies to USD 479 million of Vietnamese aluminum exports, eroding competitiveness and deterring billet importers. Until domestic smelting comes online, the Vietnam aluminum market remains vulnerable to external shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processing Type: Extrusions Drive Infrastructure Demand

Extrusions commanded 39.42% of the Vietnam aluminum market in 2025 on the back of sustained demand for window frames, curtain walls, and vehicle profiles. Rising infrastructure outlays valued at USD 95.8 billion through 2027 keep extrusion mills running at high throughput, while strict LEED and EDGE criteria reward anodized and thermally broken systems. Compliance with U.S. antidumping orders incentivizes process upgrades among cooperative exporters, reinforcing quality leadership. Castings are projected to grow at a 13.62% CAGR to 2031 as automakers localize lightweight components for EV platforms.

Certification under IATF 16949 remains a prerequisite for OEM supply and underpins Vietnam’s ranking as ASEAN’s second-largest certified base. Producers like Mien Hua Precision generate 60% of sales domestically and export the remainder to Japan, the U.S., and Australia, reflecting the country’s expanding mid-stream competitiveness.

By End-user Industry: Automotive Leads Market Transformation

The automotive sector accounted for 25.10% of 2025 demand, a share expected to expand as VinFast, THACO, and TC Group scale EV programs. Vietnam's aluminum market size for automotive applications is projected to outpace total growth as each electric two-wheeler requires 1.3 times the aluminum used in gasoline models. Building and construction is set to rise at a 12.74% CAGR to 2031, fueled by new highways, high-rise projects, and green-building policies that privilege recyclable materials.

Construction’s fast 12.74% CAGR signals a shifting demand mix toward long-cycle infrastructure. Pharmaceutical blister foil and beverage cans gain regulatory tailwinds from EPR compliance, raising the stakes for secondary smelters and foil mills. Extended use cases in marine, rail, and renewable energy broaden demand and hedge against cyclical shocks in any single sector.

Geography Analysis

Upstream resources cluster in the Central Highlands, where 5.4 billion tonnes of bauxite support alumina complexes at Lâm Đồng and Đắk Nông that shipped USD 1 billion of product in 2024. Northern industrial parks near Hanoi specialize in extrusions and flat-rolled products supplying electronics and auto plants, while southern hubs around Ho Chi Minh City house long-standing extrusion groups such as Long Vân.

Regional trade geopolitics influence flows: Vietnam supplied 7.9% of China’s secondary ingot imports in 2024 and benefited from supply diversification away from China in the U.S. market despite a 25% tariff. ASEAN neighbors create both competition and collaboration opportunities: Thailand boasts 1,947 certified auto suppliers, Malaysia dominates alloy ingot exports to China, and Indonesia is commissioning new smelters that could tilt regional supply dynamics.

Capacity utilization disparities persist: while mid-stream processors near Hanoi run close to 90%, some upstream plants in the Central Highlands averaged 70% utilization in 2024 due to power costs and logistics bottlenecks. Infrastructure improvements, including road and rail upgrades financed under Power Development Plan VIII, are expected to ease inland transport and unlock latent capacity by 2027, reinforcing growth prospects for the Vietnam aluminum market.

Competitive Landscape

The Vietnam aluminum market exhibits moderate fragmentation. Overseas majors such as Alcoa and Norsk Hydro leverage technology partnerships and alloy patents to serve OEMs but face tariffs on primary metal shipments. TKV’s expansion to 2 million tonnes of alumina plus a greenfield 500,000-tonne smelter aims to capture upstream value and reduce billet imports. Quality differentiation hinges on IATF 16949, ISO 14001, and CBAM-aligned decarbonization. More than 858 facilities now hold automotive certification, second only to Thailand in ASEAN, enabling fast-track approval for EV supply chains. Trade enforcement remains a strategic variable. The U.S. antidumping order of 14.15% for cooperative exporters and 41.84% for non-cooperating firms on extrusions forces compliance investments and encourages product diversification toward ASEAN and EU markets.

Vietnam Aluminum Industry Leaders

Daiki Aluminium Industry Co. Ltd

Global Vietnam Aluminum Co., Ltd (GVA)

Press Metal

Sapa Ben Thanh Aluminium Profiles Co., Ltd. (Sapa BTG)

Vietnam Coal and Mineral Industries Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Dak Nong People’s Committee disclosed nearly USD 1.2 billion in infrastructure upgrades to connect bauxite mines with ports, improving export logistics for alumina and future primary aluminum.

- January 2023: Vietnam Coal and Mineral Industries Group has announced the Dak Nong aluminum smelter, the country's first aluminum production project. Phase I operations are set to begin in Q2 2026, with an annual output of 450,000 metric tons.

Vietnam Aluminum Market Report Scope

Aluminum is a lightweight metal that resembles silver in color and can reflect light. Its properties include softness, non-magnetism, elasticity, and a lower density than other common metals, amounting to roughly one-third that of steel.

The Vietnamese aluminum market is segmented by processing type and end-user industry. By processing type, the market is segmented into castings, extrusions, forgings, flat-rolled products, and pigments and powders. The end-user industry segments the market into automotive, aerospace and defense, building and construction, electrical and electronics, packaging, industrial, and other end-user industries (marine, power, and others). The report also offers market size and forecasts based on volume (kilotons) and value (USD million).

By Processing Type

| Castings |

| Extrusions |

| Forgings |

| Flat Rolled Products |

| Pigments and Powders |

By End-user Industry

| Automotive |

| Aerospace and Defense |

| Building and Construction |

| Electrical and Electronics |

| Packaging |

| Industrial |

| Other End-user Industries |

| By Processing Type | Castings |

| Extrusions | |

| Forgings | |

| Flat Rolled Products | |

| Pigments and Powders | |

| By End-user Industry | Automotive |

| Aerospace and Defense | |

| Building and Construction | |

| Electrical and Electronics | |

| Packaging | |

| Industrial | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the forecast Vietnam aluminum market value by 2031?

The Vietnam aluminum market is expected to reach USD 8.71 billion by 2031.

How fast is the Vietnam aluminum market growing?

It is projected to post a 10.96% CAGR during 2026-2031.

Which processing type leads demand today?

Extrusions led with a 39.42% share in 2025, driven by construction and vehicle applications.

Which end-user segment is expanding the quickest?

Building and construction shows the fastest growth with a 12.74% CAGR outlook through 2031.

What challenge limits upstream capacity?

High electricity tariffs and carbon pricing lower smelter utilization to as low as 30-40% at times.

How many IATF 16949-certified suppliers operate in Vietnam?

There are 858 certified facilities, ranking second in ASEAN.

Page last updated on: