Europe Aluminium Composite Panel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

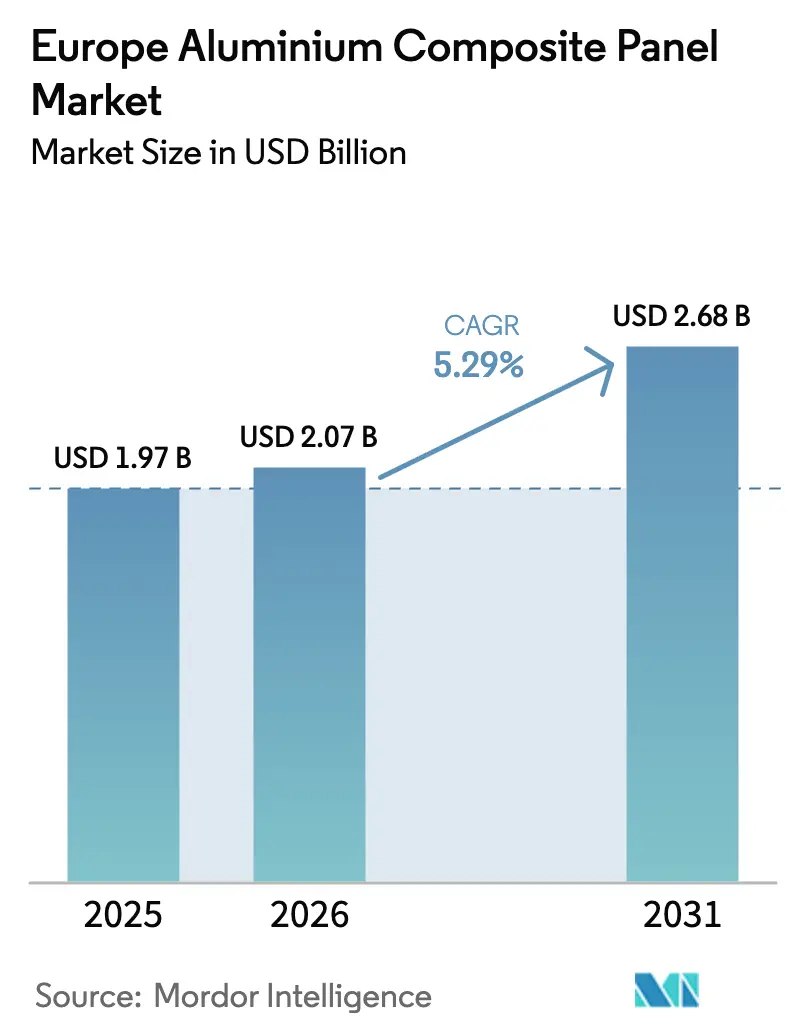

| Base Year Market Size (2025) | USD 1.97 Billion |

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aluminium Composite Panel Market Analysis by Mordor Intelligence

The European aluminium composite panel market size is expected to grow from USD 1.97 billion in 2025 to USD 2.07 billion in 2026 and is forecast to reach USD 2.68 billion by 2031 at 5.29% CAGR over 2026-2031. This growth is based on a pivot toward façade upgrade spending, stricter fire safety rules, and premium coating demand, which offset softer residential construction. Increased public-sector civil engineering work, the adoption of long-life PVDF finishes, and the phase-out of polyethylene cores combine to keep orders steady, even as overall building activity cools. Germany dominates the European aluminium composite panel market, driven by infrastructure programs that mitigate the impact of housing market challenges on suppliers. The transportation sector, particularly rail car manufacturers, is increasingly adopting lightweight aluminium skins that comply with EN 45545 standards, thereby unlocking new growth opportunities in the market.

Key Report Takeaways

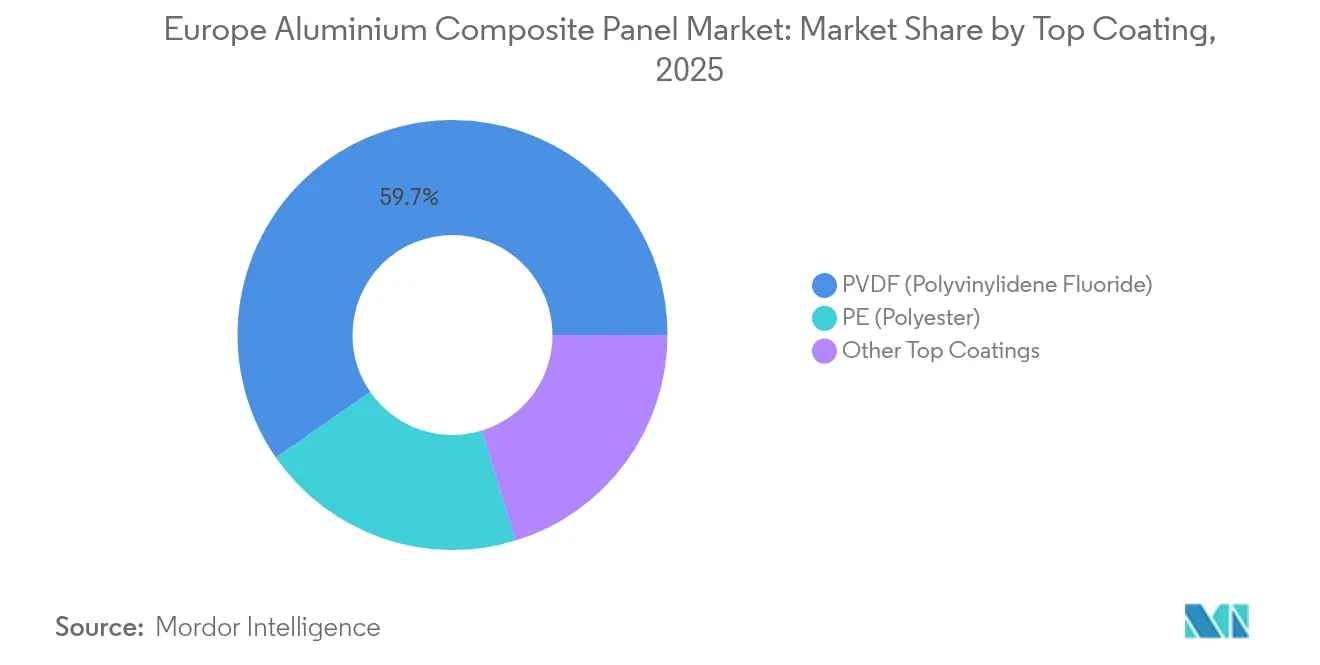

- By 2025, PVDF captured a 59.65% revenue share of the European aluminium composite panel market and is projected to accelerate at a 6.35% CAGR through 2031.

- By application, cladding held a 25.10% share of the European aluminium composite panel market in 2025 and is expected to expand at a 6.22% CAGR through 2031.

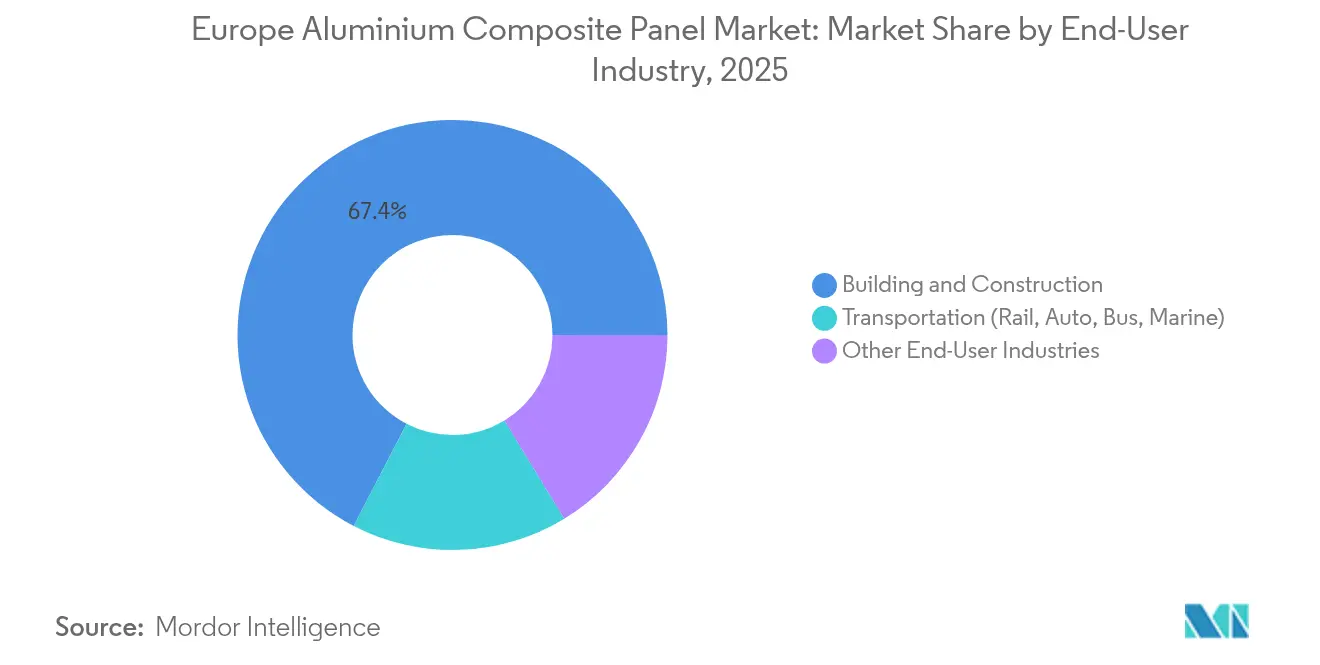

- By end-user industry, the building and construction sector accounted for 67.40% of the European aluminium composite panel market share in 2025, while the transportation sector is projected to record the highest CAGR at 6.05% through 2031.

- By geography, Germany led with 19.54% revenue share in 2025 and is growing at a 6.18% CAGR, outpacing the regional average.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on aluminum composite panel (acp) market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Aluminium Composite Panel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter EU fire-safety codes boosting A2 and FR cores | +1.2% | EU-wide, strongest in UK, Germany, France, Netherlands | Medium term (2-4 years) |

| Renovation wave under EU Green Deal needs lightweight cladding | +1.5% | EU-wide, most prominent in Germany, France, Italy, Spain | Long term (≥4 years) |

| Rapid uptake of PVDF coatings for durability and aesthetics | +0.8% | Western Europe premium projects | Medium term (2-4 years) |

| Growth of digitally printed ACPs for smart façades and DOOH ads | +0.5% | Major cities in UK, Germany, France, Spain, Italy | Long term (≥4 years) |

| Hydrogen-rail car lightweighting demand for ACP skins | +0.3% | Germany, France, UK, Netherlands | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stricter European Union Fire-Safety Codes Boosting A2 and FR Cores

Post-Grenfell regulations eliminated polyethylene-core panels from high-rise specifications across several member states. The UK banned combustible façades above 18 m in 2018, Germany adopted similar limits for buildings above 7 m, and France applied A2-s2,d0 rules on towers over 28 m. These measures have raised demand for mineral-filled cores despite a EUR 15–20 per m² price premium. National testing differences continue, yet a 2024 working group under EUMEPS signaled progress toward harmonization. Suppliers that already hold full-scale façade certifications are poised to benefit[1]UK Department for Levelling Up, Housing and Communities, “Building Safety Programme,” GOV.UK, gov.uk.

Renovation Wave Under EU Green Deal Needs Lightweight Cladding

The Renovation Wave aims to retrofit 35 million buildings by 2030, doubling the annual energy renovation rate. Lightweight ACP over-cladding adds only 5–7 kg per m², enabling installers to place new insulation without structural reinforcement. Poland, Germany, and Spain earmark Recovery and Resilience funds for such work, and performance standards in the recast Energy Performance of Buildings Directive kick in from 2028. The project flow depends on streamlined permitting and a trained installer base; however, the long-term horizon secures a demand floor through 2050[2]European Commission, “Renovation Wave Initiative,” EUROPA, ec.europa.eu.

Rapid Uptake of PVDF Coatings for Durability and Aesthetics

PVDF layers maintain color and gloss for 25 years, outperforming polyester finishes that typically require repainting within 15 years. Architectural specifications in coastal and industrial zones now default to PVDF, resulting in a 20–30% cost increase. Supply tightened in 2024 when battery makers diverted fluoropolymer feedstock, doubling coil-coating lead times. While some fabricators shifted to FEVE, most premium projects still pay the surcharge to secure longer warranties and lower lifecycle maintenance costs.

Growth of Digitally Printed ACPs for Smart Façades and DOOH Ads

UV-inkjet systems print 1,200 dpi graphics onto PVDF coils, reducing turnaround to 48 hours versus the six-week wait for screen prints. Programmatic DOOH in Europe reached 27% of campaigns in 2024, and printed backlit panels offer a lower energy draw than LED displays. Architects also embed QR codes and NFC tags to link users to building data. Adoption remains below 3% of volume, yet early movers earn 15–20% margin premiums thanks to design flexibility.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminium price volatility post-Ukraine war | –0.6% | Global, acute in Europe | Short term (≤2 years) |

| Re-cladding liabilities on combustible PE cores | –0.4% | UK, Germany, France, Netherlands | Medium term (2-4 years) |

| PVDF resin shortages due to battery-sector demand | –0.3% | Western Europe premium projects | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Aluminium Price Volatility Post-Ukraine War

Sanctions on Russian metal, high European energy tariffs, and freight premiums lifted LME aluminium to USD 2,400 per tonne in early 2024. Regional smelters curtailed output by 15% compared with 2019, and import duties rose further after the 2025 U.S. tariff round. Fabricators hedge three to six months of exposure but still face margin compression. Many now source recycled coils that carry a USD 200–300 discount and 95% lower embodied carbon, though surface-quality limits keep recycled content below 30% in architectural grades.

Re-Cladding Liabilities on Combustible PE Cores

The UK Building Safety Fund covers GBP 5.1 billion of remediation costs; however, owners must still finance most upgrades, which slows new high-rise approvals. Germany and France offered parallel grants, but the fear of future liability makes developers cautious. For suppliers, the switch to A2 panels increases unit margins but reduces volume, shifting production lines toward premium cores and consolidating demand among certified brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Top Coating: PVDF Maintains Leadership and Growth

PVDF finishes dominated the European aluminium composite panel market, accounting for a 59.65% share in 2025, and are on track for a 6.35% CAGR to 2031. The European aluminium composite panel market size for PVDF-coated products benefits from 25-year warranty norms and a proven track record in harsh climates. Architects in coastal regions of Germany, France, and Spain are increasingly viewing polyester as a lifecycle cost risk. Supply tightness in 2024 exposed vulnerabilities, yet substitution remained limited due to warranty requirements and color-retention policies.

PVDF’s premium of EUR 5–8 per m² equates to less than 1% of installed façade cost, making the upgrade decision straightforward for Class A offices, airports, and hospitality assets. Coil coaters that control their own fluoropolymer sourcing, such as 3A Composites, preserved delivery slots even during resin shortages, reinforcing their competitive edge. Polyester retains its share in interior decoration and temporary signage, but its growth lags the headline market.

By Application: Cladding Drives Demand Under Fire-Safety Mandates

Cladding secured 25.10% of the European aluminium composite panel market share in 2025 and is projected to advance at a 6.22% CAGR through 2031. New restrictions across the UK, Germany, and France eliminate combustible cores on tall buildings, steering specifications toward mineral-filled A2 products. The European aluminium composite panel market size for cladding applications is receiving an additional push from Green Deal renovation grants that favor over-cladding solutions with integrated insulation.

Interior decoration remains second in volume. PE-core panels, 3–4 mm thick, for speed installation of partition walls and ceiling modules. Signage and hoarding rely on digital printing, while insulation boards combine ACP skins with polyisocyanurate or mineral wool to deliver 20–30% energy savings. Rail carriers, although small, are the fastest-growing niche as rolling-stock builders seek weight savings. Column covers and beam wraps round out demand, especially in atria and transport hubs.

By End-User Industry: Construction Dominates, Transportation Speeds Ahead

Building and construction accounted for 67.40% of demand in 2025, reflecting ACP’s embedded role in façades and curtain walls. Weak housing starts trimmed overall construction spending by 2% in 2024, yet civil-engineering output rose 5.8%, sustaining orders for transport hubs and public buildings. Spain delivered a double-digit output jump thanks to Recovery Plan spending, while Italy shifted toward civil engineering to compensate for the end of its tax-credit boom.

Transportation holds a modest share but posts the fastest growth rate at 6.05% CAGR. Hydrogen and battery-electric trains utilize A2 panels to comply with EN 45545 fire safety regulations and offset the weight of the tank. Electric buses and lightweight marine craft also experiment with composite skins. Suppliers that tailor fire-rated sandwich panels for rolling-stock interiors are well-positioned for multi-year rail procurement cycles.

Geography Analysis

Germany led the European aluminium composite panel market with a 19.54% share in 2025 and is projected to grow at a 6.18% CAGR through 2031. Civil engineering budgets, linked to the EUR 25.6 billion NextGenerationEU allocation and a EUR 1 billion federal fire safety fund, underpin steady panel intake despite a 17% decline in housing permits. State codes now require non-combustible façades above 7 m, maintaining demand for A2 cores.

The United Kingdom experienced a contraction in 2024 due to the Building Safety Act, which tightened liability and halted many high-rise construction starts. Even so, the GBP 5.1 billion Building Safety Fund accelerates replacement of combustible panels, anchoring a refurbishment pipeline that supports certified suppliers. France balances moderate new-build activity with grants from ANAH that cover up to half of re-cladding costs in social housing.

Nordic countries set the pace on embodied-carbon limits. Denmark already mandates declarations, and Sweden will impose thresholds from 2025, pushing manufacturers to publish EN 15804 EPDs and shorten transport distances.

Competitive Landscape

The European aluminium composite panel market is moderately consolidated, with Global firms such as 3A Composites competing with regional specialists like Euramax. 3A Composites leverages vertical integration and introduced ALUCODUAL in late 2024, a dual-sided A2 panel that streamlines glass-curtain installation. Euramax differentiates through a digital configurator that speeds design approvals, while ALUCOIL leverages recently certified EPDs to win Nordic public projects. White-space opportunities center around digital printing, off-site prefabricated cassettes, and circular economy take-back schemes. Only around 10% of end-of-life panels are recycled today. Mechanical delamination pilots in Germany and the Netherlands recover up to 90% of aluminium content, suggesting a route to new revenue streams and compliance with tightening waste directives.

Europe Aluminium Composite Panel Industry Leaders

3A Composites

Arconic Inc.

ALUCOIL

Alubond USA

Mitsubishi Chemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: 3A Composites expanded its AXCENT line of prefabricated façade cassettes, integrating ALUCOBOND panels with subframes, insulation and glazing to cut on-site labor by 40%.

- November 2024: 3A Composites launched ALUCODUAL, a dual-sided A2 panel with PVDF finishes on both faces for transparent curtain walls.

Europe Aluminium Composite Panel Market Report Scope

| PE (Polyester) |

| PVDF (Polyvinylidene Fluoride) |

| Other Top Coatings |

| Interior Decoration |

| Hoarding and Signage |

| Insulation |

| Cladding |

| Railway Carrier |

| Column Cover and Beam Wrap |

| Building and Construction |

| Transportation (Rail, Auto, Bus, Marine) |

| Other End-User Industries |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDICS Countries |

| Rest of Europe |

| Top Coating | PE (Polyester) |

| PVDF (Polyvinylidene Fluoride) | |

| Other Top Coatings | |

| Application | Interior Decoration |

| Hoarding and Signage | |

| Insulation | |

| Cladding | |

| Railway Carrier | |

| Column Cover and Beam Wrap | |

| End-User Industry | Building and Construction |

| Transportation (Rail, Auto, Bus, Marine) | |

| Other End-User Industries | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDICS Countries | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the European aluminium composite panel market?

The market is valued at USD 2.07 billion in 2026.

How fast will demand for aluminium composite panels grow in Europe?

The market is projected to expand at a 5.29% CAGR to 2031.

Which coating type leads sales?

PVDF coatings dominated the market with a 59.65% share in 2025 and are forecasted to continue growing.

Why is Germany an attractive market for buyers?

Germany combines a large fire-safety retrofit pipeline with sustained civil-engineering outlays.

What is driving transportation demand for panels?

Hydrogen and battery-electric rail cars require lightweight, fire-rated aluminium skins to meet EN 45545.

How fragmented is supplier competition?

No firm holds more than 15%, and the top five together control roughly half of sales.

Page last updated on: