Alpha Olefins Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

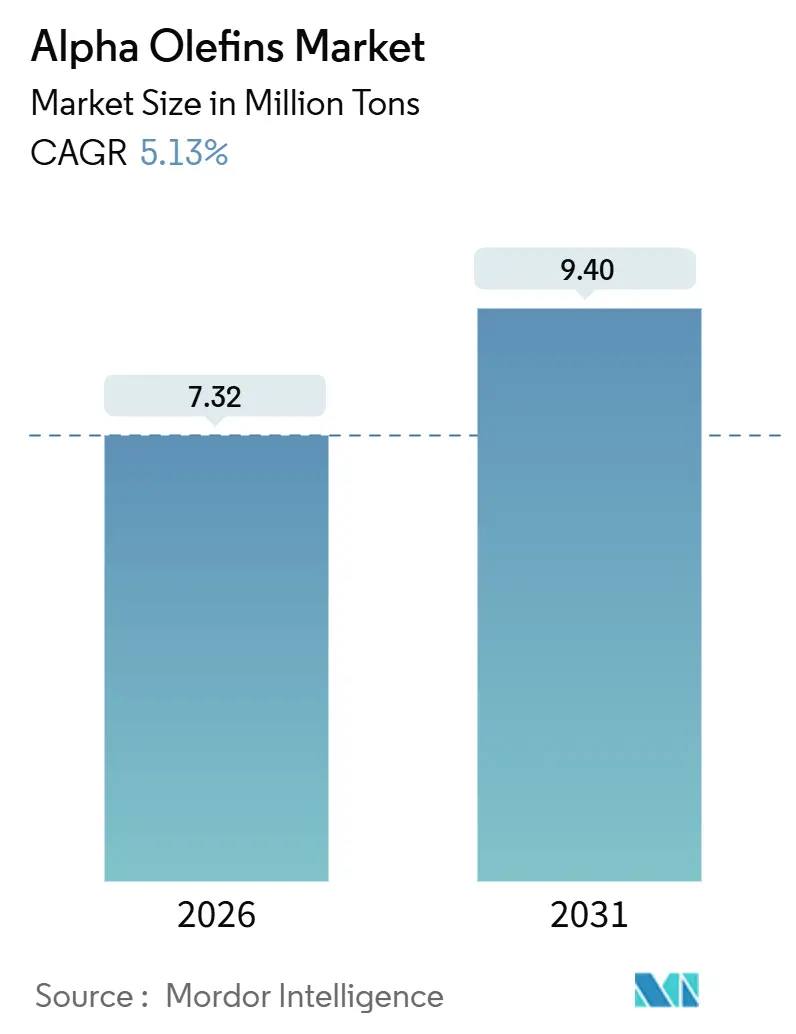

| Market Volume (2026) | 7.32 Million tons |

| Market Volume (2031) | 9.40 Million tons |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

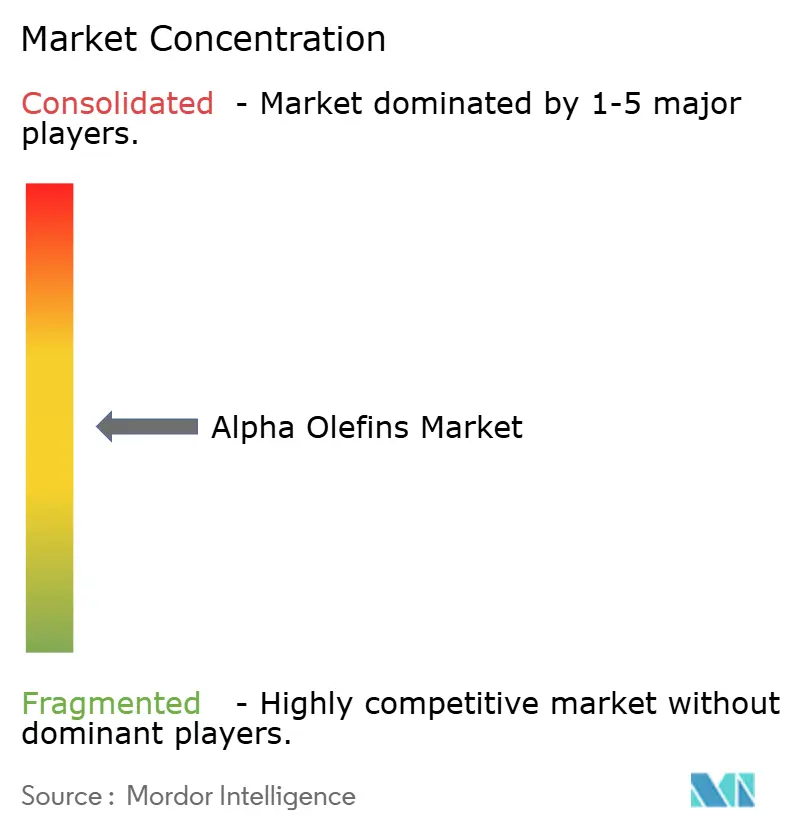

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alpha Olefins Market Analysis by Mordor Intelligence

The Alpha Olefins Market size is estimated at 7.32 Million tons in 2026, and is expected to reach 9.40 Million tons by 2031, at a CAGR of 5.13% during the forecast period (2026-2031). Capacity additions in Asia-Pacific and the Middle-East, shale-ethane cost advantages in North America, and soaring demand for comonomers in linear low-density polyethylene (LLDPE) films underpin this growth trajectory. Rising poly-alpha-olefin (PAO) lubricant adoption, particularly for electric-vehicle (EV) thermal-management fluids, further elevates volumetric prospects, while integrated producers leverage backward integration into ethylene to secure supply and margin resilience. Feedstock economics remain the pivotal competitive lever; United States ethane output climbed to 2.8 million barrels per day in 2024, delivering a structural cost edge over naphtha-fed crackers in Europe and Northeast Asia. Simultaneously, China’s state-backed Sinopec-Aramco Fujian complex and Saudi Arabia-controlled projects in Fujian and Yanbu are adding more than 3.6 million tons of ethylene capacity between 2024 and 2026, redrawing supply chains toward the East.

Key Report Takeaways

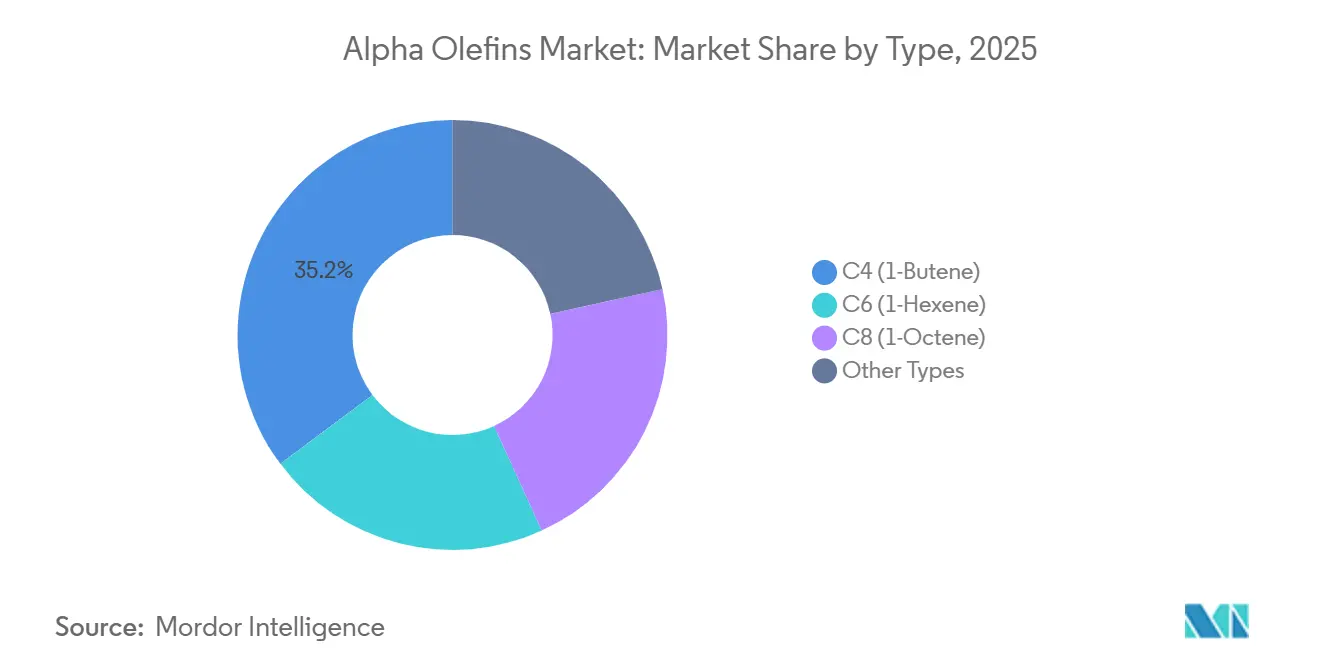

- By type, C4 (1-butene) held 35.23% of alpha olefins market share in 2025, whereas C6 (1-hexene) recorded the fastest 5.88% CAGR through 2031.

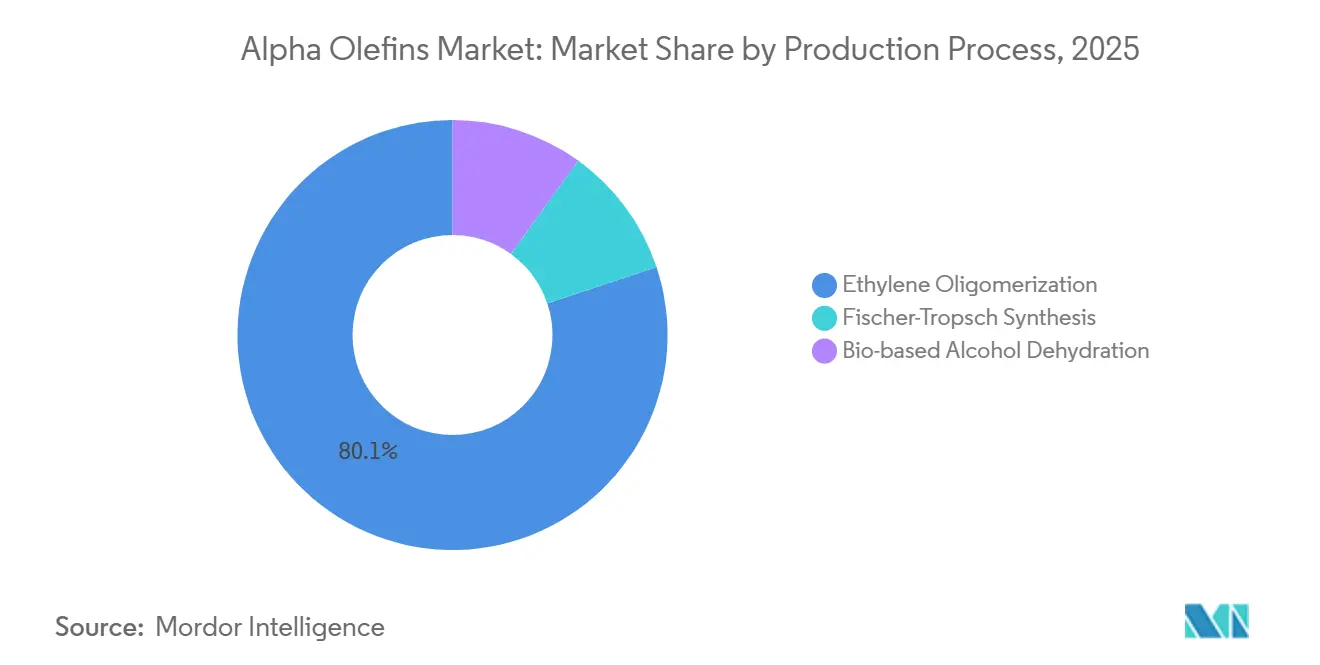

- By production process, ethylene oligomerization contributed 80.12% of 2025 output and is forecast to grow at a 5.67% CAGR through 2031.

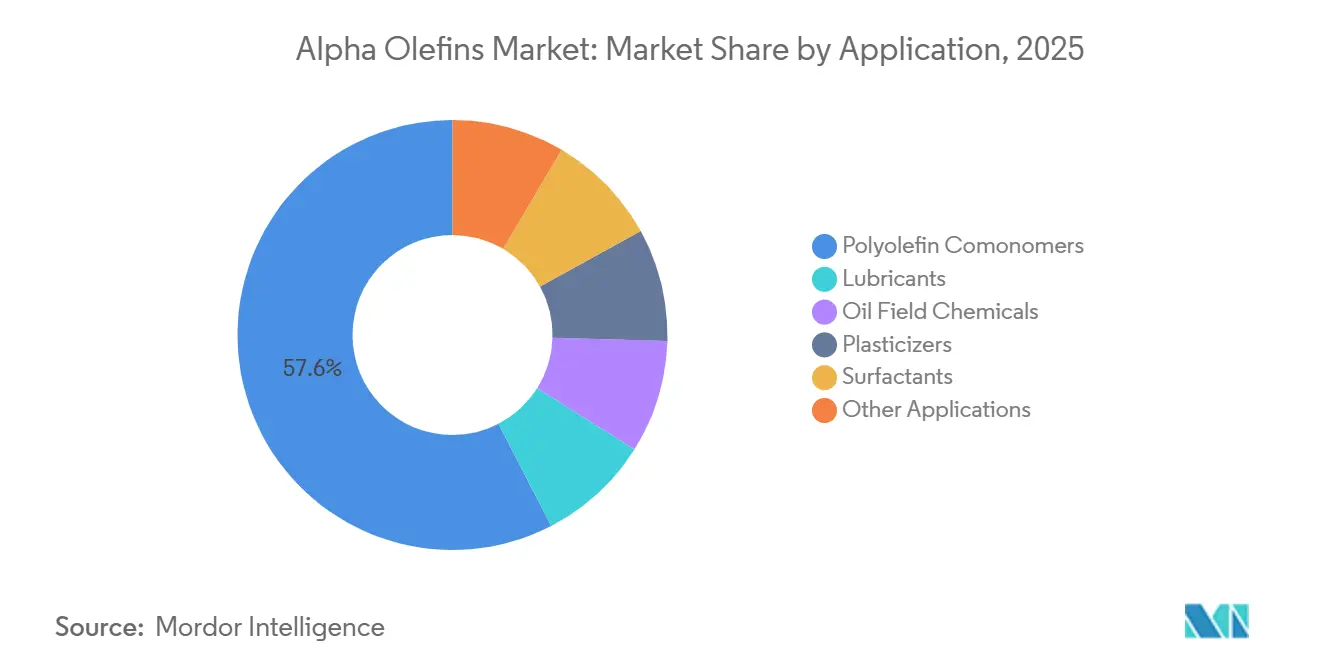

- By application, polyolefin comonomers commanded 57.58% of the alpha olefins market size in 2025 and will expand at a 6.26% CAGR to 2031.

- By end-use industry, packaging led with 36.45% volume share in 2025 and is advancing at a 6.15% CAGR to 2031.

- By geography, Asia-Pacific captured 40.45% of 2025 demand; the region is anticipated to post a 6.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alpha Olefins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Polyethylene Comonomer Demand | +2.1% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Growth in Synthetic Lubricants | +1.3% | North America, Europe, APAC automotive hubs | Medium term (2-4 years) |

| Shale-Ethane Cost Advantage in North America | +0.9% | North America, spillover to Latin America | Short term (≤ 2 years) |

| Capacity Additions in Emerging Economies | +1.5% | APAC core (China, India), Middle-East | Long term (≥ 4 years) |

| EV Thermal Management Fluid Requirements | +0.6% | Europe, North America, China EV clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Polyethylene Comonomer Demand

Metallocene LLDPE grades require tighter molecular-weight control, elevating consumption of high-purity 1-hexene and 1-octene comonomers. Chevron Phillips Chemical expanded its Cedar Bayou cracker to 1.5 million tons-per-year ethylene capacity and co-located alpha-olefin trains to monetize the ethylene-to-C6/C8 spread. Shell’s Monaca complex follows a similar integration model, ensuring captive comonomer supply for 1.6 million tons of polyethylene demand. E-commerce logistics accelerate stretch-film uptake, and brand owners prefer downgauged yet puncture-resistant films that only metallocene LLDPE can deliver. This downstream pull renders comonomer demand inelastic to modest price spikes. As new Asian LLDPE reactors switch from Ziegler-Natta to metallocene catalysts, alpha olefins market volumes receive a structural uplift.

Growth in Synthetic Lubricants

Poly-alpha-olefin base stocks achieve viscosity indices above 130 and pour points below -50 °C, enabling next-generation engine oils that satisfy API SP and ILSAC GF-6 specifications. Chevron Phillips Chemical broke ground in November 2025 on a PAO expansion in Beringen, Belgium, to service European automakers pursuing longer drain intervals and hybrid powertrains. EVs further amplify PAO demand, as direct battery-cell cooling requires fluids stable above 150 °C with high dielectric strength. Industrial gearboxes and compressors similarly upgrade to PAO to extend service life and reduce downtime. Economies of scale are narrowing the PAO-to-mineral-oil cost delta, hastening substitution in mid-tier lubricant formulations.

Shale-Ethane Cost Advantage in North America

United States ethane production reached 2.8 million barrels per day in 2024, while exports averaged 620,000 barrels per day during Q1 2024. Ethane pricing below USD 0.20 per gallon kept U.S. ethylene cash costs under USD 300 per ton, versus USD 600-700 per ton for naphtha crackers in Europe. Fourteen prospective Gulf Coast crackers totaling 9.19 million tons of ethylene will be co-located with alpha-olefin units, locking in feedstock and bolstering regional alpha olefins market competitiveness[1]American Chemistry Council, “U.S. Ethylene Investment Tracker,” americanchemistry.com . This edge squeezes naphtha-dependent producers in Northeast Asia and Europe, prompting portfolio restructuring and asset rationalization.

Capacity Additions in Emerging Economies

China’s Sinopec-Aramco Fujian complex started up in November 2024, integrating a USD 10 billion refinery and 1.5 million tons-per-year ethylene cracker that includes on-purpose alpha olefin capacity. SABIC approved a 1.8 million tons-per-year cracker in Fujian for 2026 completion, while Yasref’s 1.8 million tons-per-year project in Yanbu advances toward FID in 2026. India’s petrochemical demand grew 7% in fiscal 2024-2025, outstripping domestic LAO capacity and spurring imports[2]Petroleum Planning and Analysis Cell, “Petrochemical Demand Forecast,” ppac.gov.in . State-backed financing and feedstock security in these regions reinforce long-term alpha olefins market growth corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethylene Feedstock Price Volatility | -1.2% | Global, acute in naphtha-dependent regions (Europe, Northeast Asia) | Short term (≤ 2 years) |

| Non-Biodegradability of Polyethylene | -0.5% | Europe, North America (regulatory pressure zones) | Medium term (2-4 years) |

| Catalyst Deactivation in Bio-Based LAO Synthesis | -0.3% | Europe, North America (bio-based development hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ethylene Feedstock Price Volatility

Brent crude oscillated between USD 70 and USD 90 per barrel during 2024-2025, compressing naphtha cracker margins and disrupting oligomerization economics. Asian ethylene spot prices fluctuated USD 800-1,100 per ton, forcing comonomer suppliers to hedge through futures contracts that dilute profitability. European producers face an additional EUR 50-70 per ton carbon-cost headwind under the EU ETS. Consequently, standalone LAO units reliant on merchant ethylene are deferring capacity expansions, while integrated Gulf Coast complexes run at elevated rates.

Non-Biodegradability of Polyethylene

Alpha-olefin-rich LLDPE films are non-biodegradable, drawing scrutiny from the European Union’s Single-Use Plastics Directive and impending U.S. state bans on non-recyclable packaging. Regulatory headwinds threaten demand elasticity in mature markets. Producers are countering with chemical-recycling tie-ins and design-for-recyclability initiatives, yet legislative timelines tighten beyond 2028, capping upside for conventional resin volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: C6 (1-Hexene) Drives Performance Upgrading, C4 (1-Butene) Maintains Dominance

C4 (1-Butene) captured 35.23% of 2025 volume on cost advantage and legacy Ziegler-Natta LLDPE use. Conversely, C6 (1-Hexene) grew at a 5.88% CAGR, steering alpha olefins market size expansion toward higher-value streams. Dow’s AFFINITY plastomers leverage C8 (1-octene) for elastomeric films, commanding premiums of 15-20% over C4-based resins.

Metallocene catalysts require 1-hexene or 1-octene for narrow molecular-weight distributions, improving dart impact and stress-crack resistance. Higher carbon-number alpha olefins (C10-C20+) serve synthetic lubricants and plasticizer alcohols, sustaining margin diversity even as volume concentrates in C4-C8. Fischer-Tropsch-derived alpha olefins target multi-cut portfolios but remain below 10% of output due to capital intensity.

By Production Process: Oligomerization Dominates Owing to Catalyst Selectivity and Integration Economics

Ethylene oligomerization delivered 80.12% of 2025 production and is projected to expand at 5.67% CAGR, underpinned by catalyst selectivity surpassing 95% for 1-hexene. Chevron Phillips and INEOS capitalize on captive ethylene, achieving margin insulation against feedstock volatility. Fischer-Tropsch synthesis monetizes stranded gas in Qatar and coal in South Africa, yet remains subscale. Bio-alcohol dehydration pilot plants in Europe stay below 10,000 tons-per-year until catalyst lifetimes improve.

Integration economics favor oligomerization, as ethylene crackers can swing between LAO, polyethylene, and ethylene derivatives depending on spreads, preserving alpha olefins industry competitiveness across cycles.

By Application: Polyolefin Comonomers Anchor Demand

Polyolefin comonomers accounted for 57.58% of demand in 2025, rising at a 6.26% CAGR as flexible-packaging converters downgrade film thickness without compromising performance. Lubricants are benefiting from PAO’s high viscosity index and low-temperature fluidity. Oil-field chemicals, plasticizers, and surfactants collectively absorb the remaining share, capitalizing on alpha olefins’ hydrophobicity and chain-length flexibility.

Comonomer consumption closely tracks global polyethylene capacity, especially in Asia-Pacific and the Middle-East, anchoring long-term alpha olefins market growth. Lubricant and surfactant segments, while smaller, capture higher value per ton and diversify geographic exposure toward Europe and North America.

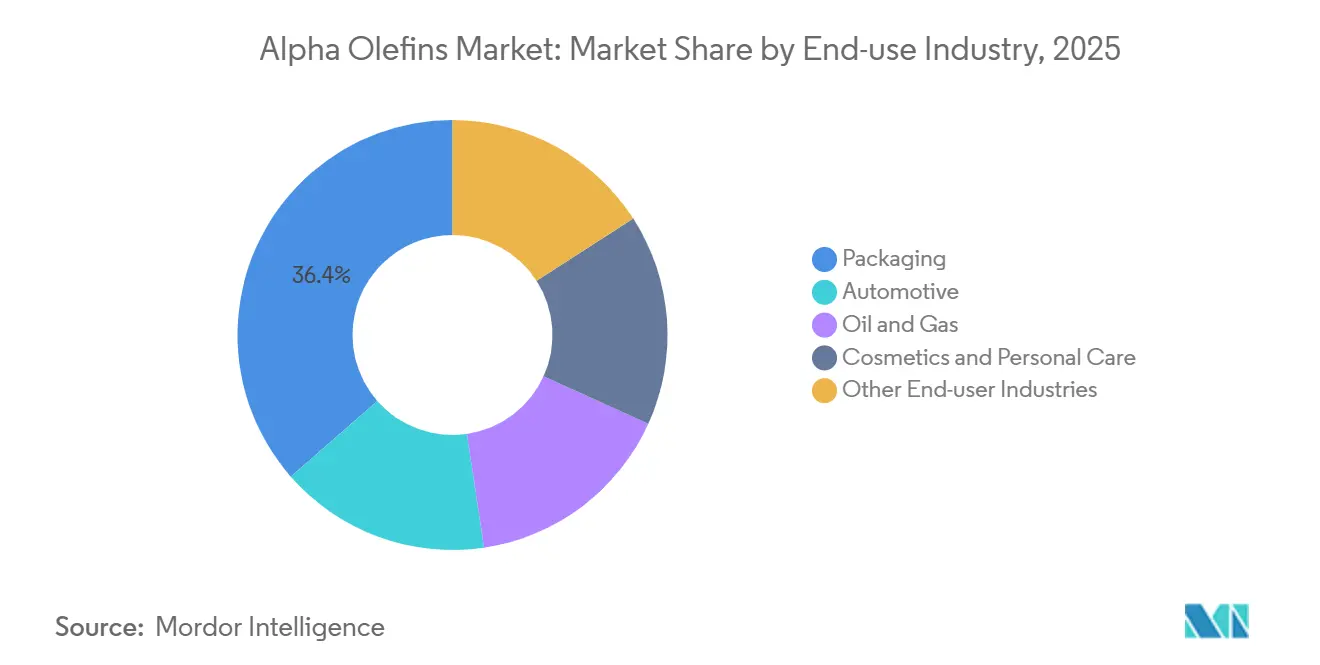

By End-use Industry: Packaging Innovation Drives Consumption

Packaging accounted for 36.45% of the projected 2025 volume and is expected to grow at a CAGR of 6.15% through 2031, driven by the increasing adoption of e-commerce platforms and the rising demand for convenience food products in the Asia-Pacific region. Automotive applications, including engine oils, EV thermal management fluids, and elastomeric interior films, are also experiencing significant growth due to advancements in vehicle technologies and the growing electric vehicle market.

The remaining demand is attributed to oil and gas drilling fluids, cosmetics, and construction materials, which provide niche but stable demand opportunities, supported by consistent industrial and consumer requirements.

Geography Analysis

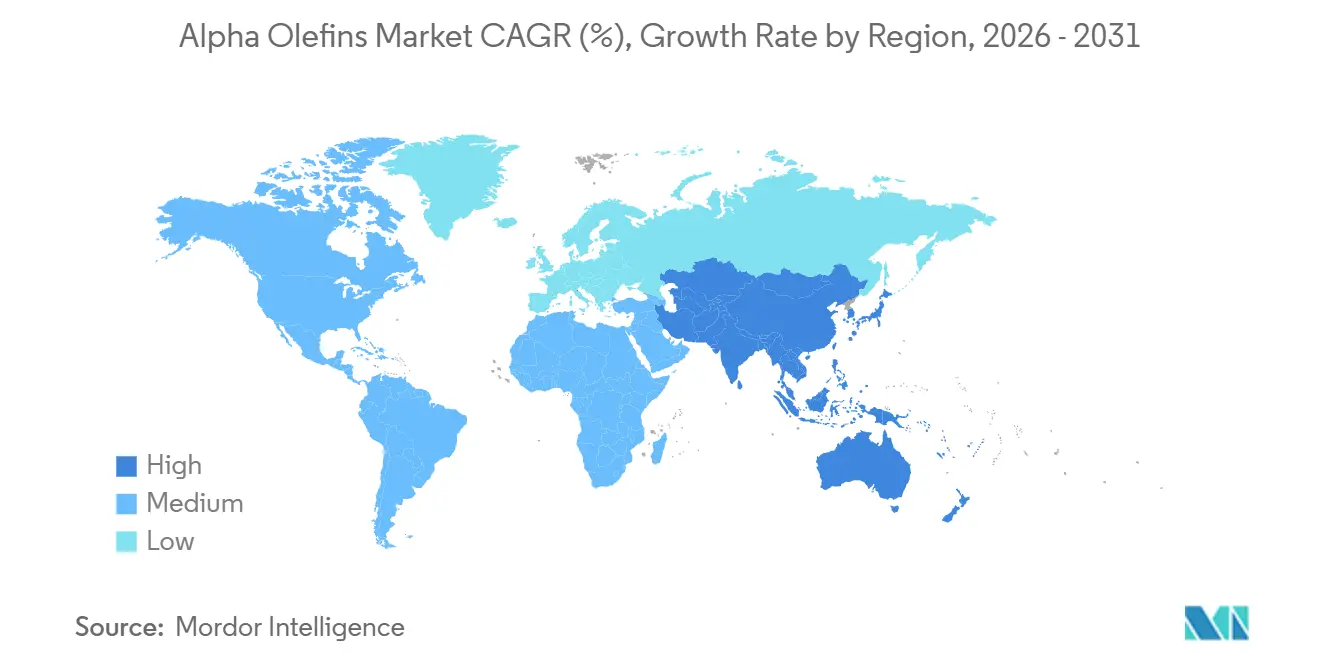

Asia-Pacific controlled 40.45% of 2025 demand and is set to grow at a 6.89% CAGR, driven by China’s USD 10 billion Sinopec-Aramco Fujian complex and India’s 7% annual petrochemical consumption uptick. With local alpha olefin capacity trailing demand, regional imports from the Middle-East remain robust, yet upcoming Chinese and Saudi capacities reposition supply chains eastward. Japan and South Korea import high-purity C6/C8 for specialty LLDPE, whereas ASEAN polyolefin demand expands above 6% annually, absorbing incremental alpha olefins market volumes.

North America leverages shale-ethane pricing, enabling ethylene cash costs nearly 50% lower than European naphtha equivalents. Fourteen Gulf Coast crackers totaling 9.19 million tons of ethylene will support co-located LAO units, reinforcing the region’s role as a net exporter. Canadian and Mexican deficits ensure cross-border flows, consolidating the continent’s feedstock advantage into downstream competitiveness.

Europe faces structural headwinds: high naphtha costs, EU ETS carbon pricing, and plant closures such as SABIC’s Geleen Olefins 3 and Teesside crackers removing 500,000 tons of ethylene capacity. The Middle-East, conversely, accelerates ethane-fed expansions like Yasref’s planned 1.8 million tons-per-year cracker, bridging Asian demand. South America remains anchored by Braskem in Brazil, but macroeconomic volatility and limited upstream investment restrain growth potential.

Competitive Landscape

The top five producers-Chevron Phillips Chemical, Shell, INEOS, SABIC, and Sasol-command an estimated 55-60% of global capacity, defining a moderately concentrated alpha olefins market. Backward integration into ethylene frames competitiveness; Chevron Phillips’ proprietary chromium catalyst system yields more than 95% 1-hexene selectivity, while INEOS operates oligomerization units in the U.S. and Europe with captive feedstock. Shell and Sasol exploit Fischer-Tropsch co-products for specialty PAO and surfactant feedstocks.

Strategic moves underscore divergence. Chevron Phillips initiated its Belgian PAO expansion to address EV thermal-management growth. SABIC shuttered high-cost European crackers, reallocating capital to Middle Eastern assets with ethane advantage. ExxonMobil patented a novel trimer catalyst achieving viscosity indices above 140, targeting premium engine-oil basestocks.

Emergent players include LG Chem and Mitsui Chemicals, partnering with Middle Eastern complexes for cost-competitive feedstock. Regulatory compliance-REACH registration and EU sustainability directives-creates entry barriers favoring incumbents with established testing portfolios. As Asian capacities ramp and European assets exit, competitive balance tilts toward feedstock-abundant geographies, sustaining a moderate concentration profile.

Alpha Olefins Industry Leaders

Chevron Phillips Chemical Company LLC

Shell plc

Exxon Mobil Corporation

INEOS

SABIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CNOOC & Shell Petrochemicals Company Limited finalized its investment decision to expand its petrochemical complex in Daya Bay, Huizhou, located in southern China. The expansion, which is expected to be completed by 2028, included downstream derivative units to produce chemicals, including linear alpha olefins.

- October 2024: The National Institute of Clean-and-Low-Carbon Energy (NICE), part of CHN Energy, in partnership with Eindhoven University of Technology and other institutions, made significant progress in catalytic technology. This advancement involved the use of a pure-phase χ-iron carbide catalyst to directly convert syngas into high-value chemicals, particularly linear alpha olefins.

Global Alpha Olefins Market Report Scope

Alpha olefins are a family of organic compounds, alkenes (also known as olefins), with a chemical formula CxH2x, distinguished by having a double bond at the primary or alpha (α) position. This location of a double bond enhances the reactivity of the compound and makes it useful for a number of applications.

The alpha olefins market is segmented by type, production process, application, end-use industry, and geography. By type, the market is segmented into C4 (1-Butene), C6 (1-Hexene), C8 (1-Octene), and other types. By production process, the market is segmented into ethylene oligomerization, Fischer-Tropsch synthesis, and bio-based alcohol dehydration. By application, the market is segmented into polyolefin comonomers, lubricants, oil field chemicals, plasticizers, surfactants, and other applications. By end-use industry, the market is segmented into packaging, automotive, oil and gas, cosmetics and personal care, and other end-user industries. The report also covers the market size and forecasts for alpha olefins in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| C4 (1-Butene) |

| C6 (1-Hexene) |

| C8 (1-Octene) |

| Other Types |

| Ethylene Oligomerization |

| Fischer-Tropsch Synthesis |

| Bio-based Alcohol Dehydration |

| Polyolefin Comonomers |

| Lubricants |

| Oil Field Chemicals |

| Plasticizers |

| Surfactants |

| Other Applications |

| Packaging |

| Automotive |

| Oil and Gas |

| Cosmetics and Personal Care |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | C4 (1-Butene) | |

| C6 (1-Hexene) | ||

| C8 (1-Octene) | ||

| Other Types | ||

| By Production Process | Ethylene Oligomerization | |

| Fischer-Tropsch Synthesis | ||

| Bio-based Alcohol Dehydration | ||

| By Application | Polyolefin Comonomers | |

| Lubricants | ||

| Oil Field Chemicals | ||

| Plasticizers | ||

| Surfactants | ||

| Other Applications | ||

| By End-use Industry | Packaging | |

| Automotive | ||

| Oil and Gas | ||

| Cosmetics and Personal Care | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the volume of the alpha olefins market?

The alpha olefins market size reached 7.32 million tons in 2026 and is forecast to reach 9.40 million tons by 2031.

How fast is global demand for alpha olefins expected to grow?

The market is forecast to expand at a 5.13% CAGR to 2031.

Which application segment drives most alpha olefins consumption?

Polyolefin comonomers account for 57.58% of 2025 demand and will grow at a 6.26% CAGR.

Why are poly-alpha-olefin lubricants gaining popularity?

PAO offers high viscosity indices and thermal stability above 150 °C, meeting stringent EV and hybrid engine requirements.

Page last updated on: