Alpha Emitters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 322.54 Million |

| Market Size (2031) | USD 698.98 Million |

| Growth Rate (2026 - 2031) | 16.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

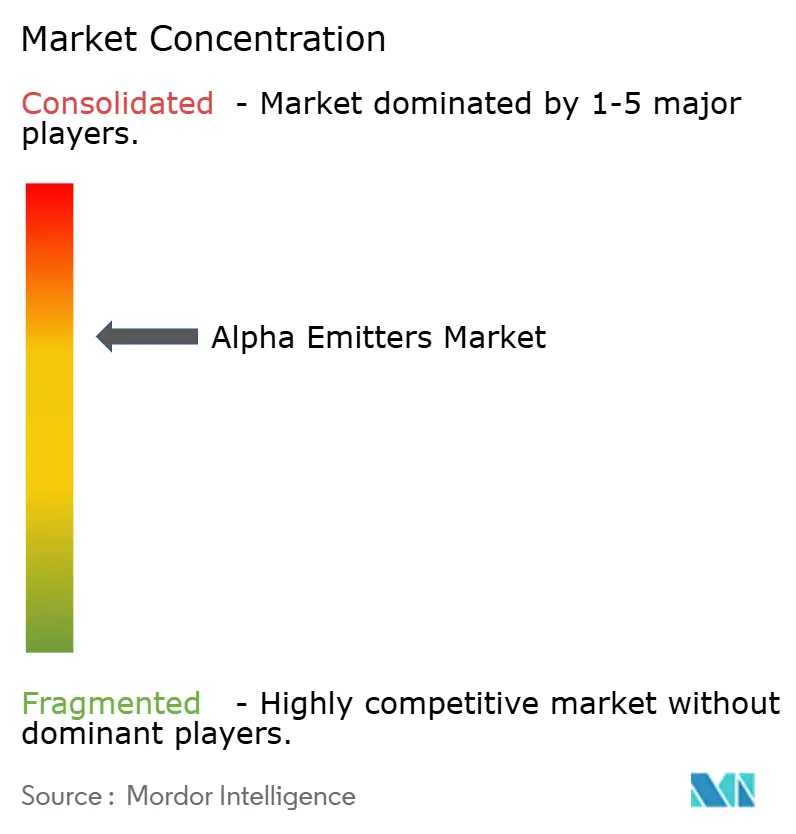

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alpha Emitters Market Analysis by Mordor Intelligence

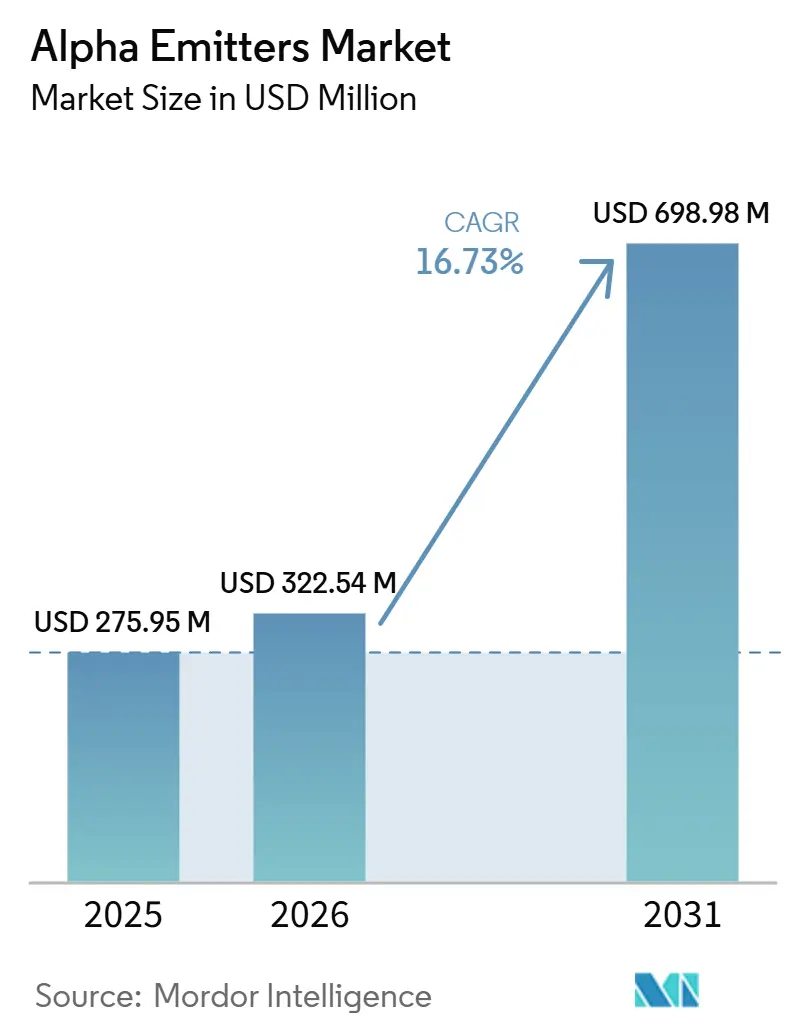

The Alpha Emitters Market size was valued at USD 275.95 million in 2025 and is estimated to grow from USD 322.54 million in 2026 to reach USD 698.98 million by 2031, at a CAGR of 16.73% during the forecast period (2026-2031).

The Alpha emitters market is being supported by oncology programs that use high-linear-energy-transfer agents against resistant micrometastases, including disease that persists after chemotherapy, androgen-pathway inhibitors, or beta-emitting radioligands. Radium-223 dichloride accounted for most commercial activity through 2025, although actinium-225 and lead-212 programs are moving through later-stage development, and Orano Med’s AlphaMedix received FDA Breakthrough Designation in 2024. Improved chelators and targeting-peptide conjugation are broadening treatment options and may support use earlier in care pathways. The Alpha emitters market also depends on isotope supply, which makes producer capacity and long-term supply contracts important to commercial access. Reimbursement remains uneven outside the United States and Germany, which may delay use even after regulatory approval.

Key Report Takeaways

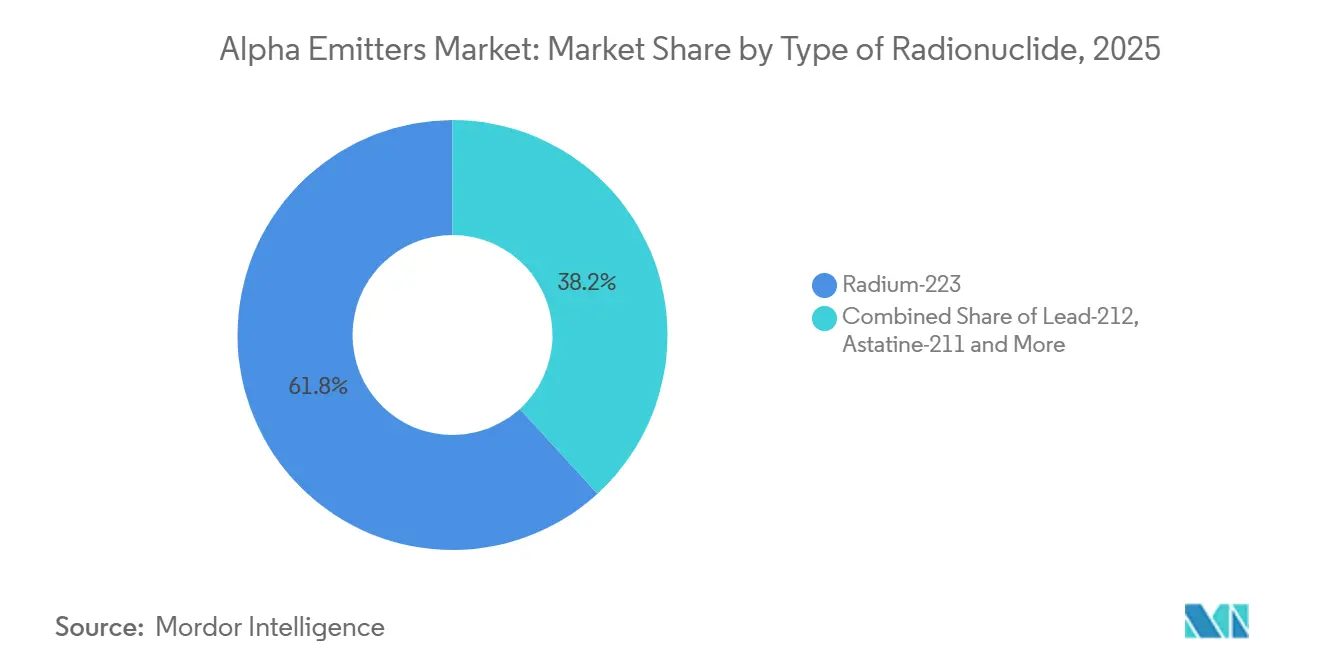

- By type of radionuclide, radium-223 held 61.77% of alpha emitters market share in 2025; lead-212 is expected to record the fastest CAGR at 29.57% through 2031.

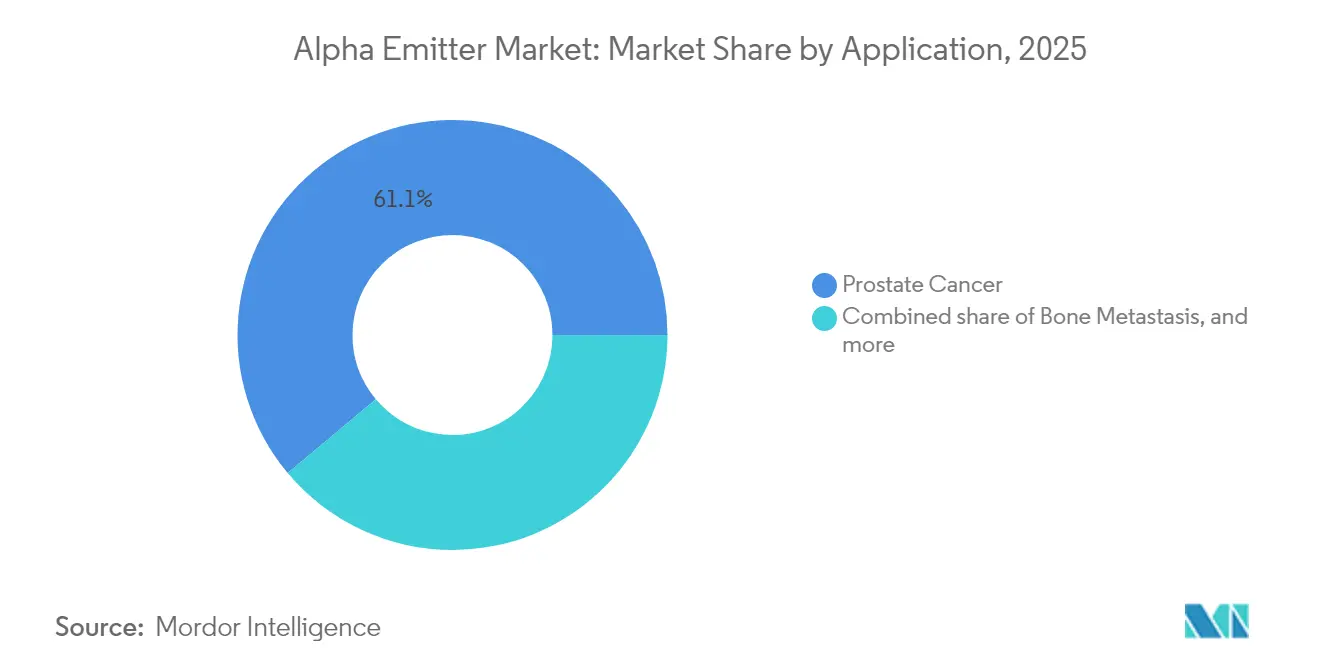

- By application, prostate cancer commanded 50.66% share of the alpha emitters market size in 2025, while endocrine tumors are projected to expand at 21.63% CAGR between 2026-2031.

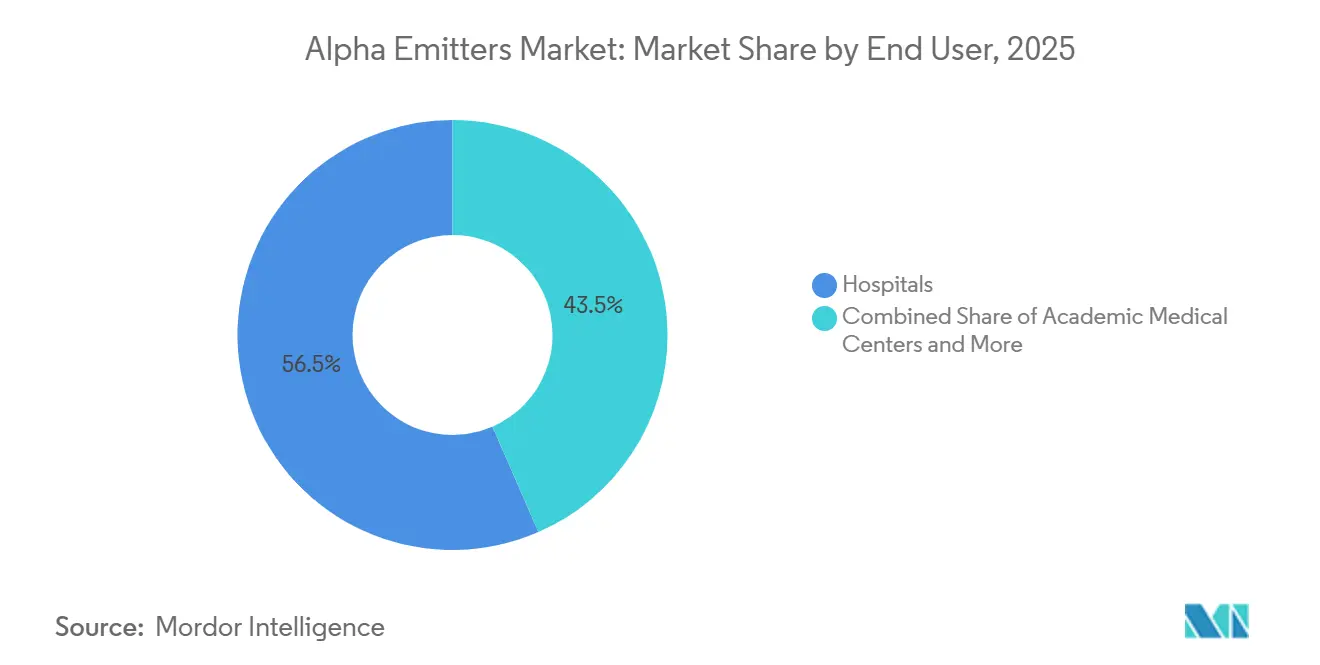

- By end user, hospitals accounted for 56.55% utilization of the alpha emitters market in 2025; academic medical centers are forecast to grow 16.92% annually to 2031.

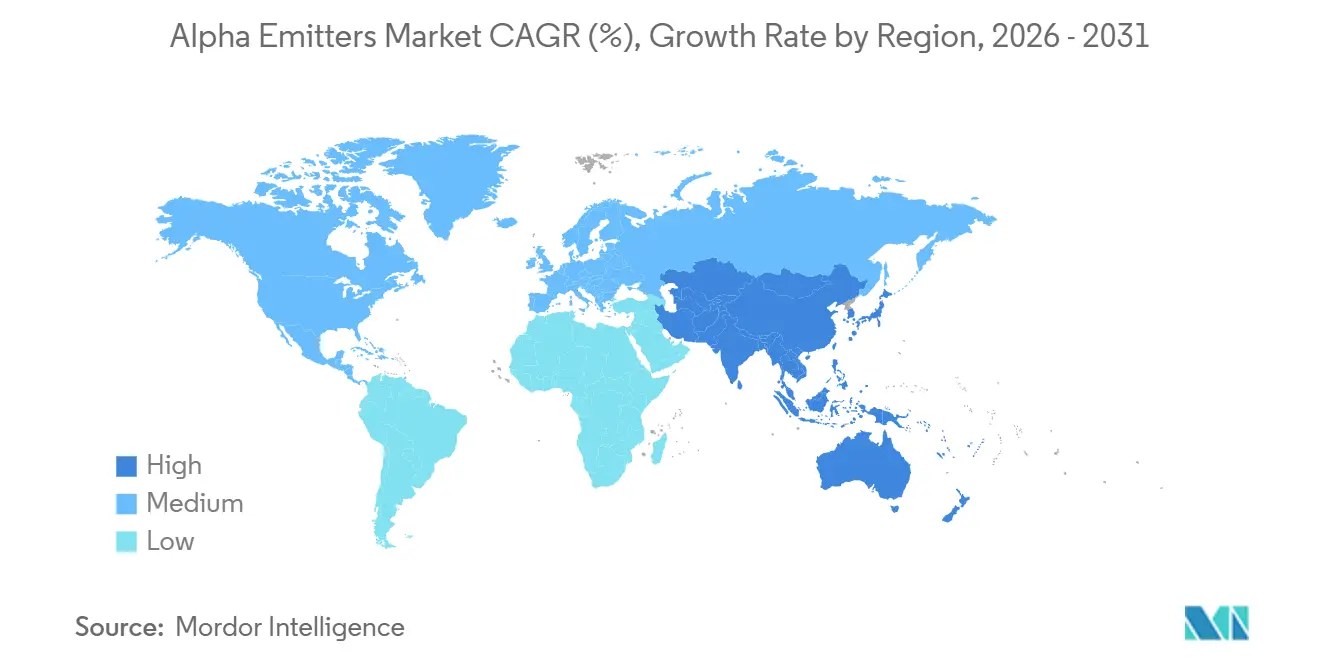

- By geography, North America led with 50.09% revenue share of the alpha emitters market in 2025, and Asia-Pacific is expected to have the highest CAGR of 18.17% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Alpha Emitters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Incidence Of Hard-To-Treat Solid Tumors | +3.5% | Global | Short term (≤ 2 years) |

| Superior Tumor-Killing Efficiency | +3.2% | Global | Medium term (2-4 years) |

| Strategic Pharmaceutical Investments | +3.8% | North America and Europe | Short term (≤ 2 years) |

| Expanding Isotope Production Infrastructure | +2.6% | North America and Europe | Medium term (2-4 years) |

| Evolving Regulatory And Reimbursement Frameworks | +1.3% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Shift Toward Radionuclide-Drug Conjugates | +1.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Incidence Of Hard-To-Treat Solid Tumors Driving Demand

The Alpha emitters market is linked to the growing need for treatment options in difficult-to-treat solid tumors, particularly where patients no longer respond adequately to earlier systemic therapy. The World Health Organization projected 35 million new cancer cases in 2050, compared with 20 million in 2022, which increases the potential pool of patients with refractory and metastatic disease that may require additional treatment options[1]World Health Organization, “Global Cancer Burden Growing, Amidst Mounting Need For Services,” World Health Organization, who.int. Bone-metastatic disease and resistant solid tumors are important because many patients have progressed after chemotherapy, androgen-pathway inhibitors, or other treatments that have already addressed the primary disease. Alpha radiation can produce double-strand DNA damage, which is relevant where tumors have adapted to repair damage from earlier treatment and have become less responsive to conventional approaches. Better first-line prostate cancer treatment can extend survival and leave more patients facing bone micrometastases later in care, which can broaden the clinical window for radium-223. Updated nuclear medicine protocols have encouraged consideration of radionuclide therapy earlier in metastatic castration-resistant prostate cancer management rather than only after every other systemic option has been exhausted.

Superior Tumor-Killing Efficiency Boosting Clinician Confidence

Alpha particles deposit 50 to 230 keV/µm of energy across a 40 to 90 µm path length and have a reported relative biological effectiveness of 3 to 7 compared with conventional radiation. This physical profile supports use in heterogeneous tumors because radiation is delivered over a limited range rather than across a wider area of surrounding tissue. The Alpha emitters market benefits when physicians can consider both controlled evidence and routine-practice experience, especially for agents that require specialized treatment planning. Final PEACE-3 results published in February 2026 showed that radium-223 plus enzalutamide reduced mortality risk by 24% versus enzalutamide alone in patients with metastatic castration-resistant prostate cancer and bone metastases. Median overall survival was 38.2 months with the combination and 32.6 months with enzalutamide alone, with a hazard ratio of 0.76 and p=0.0096, adding a defined clinical result to the treatment discussion. The short radiation path may limit dose to nearby healthy tissue, which can affect toxicity concerns, retreatment considerations, and physician confidence when weighing localized radiation options.

Strategic Pharmaceutical Investments Accelerating Development

Strategic acquisitions and supply agreements are changing how the Alpha emitters market is financed and developed because clinical assets alone do not ensure access to the required isotopes. AstraZeneca acquired Fusion Pharmaceuticals in a transaction valued at up to USD 2.4 billion, while Eli Lilly acquired Point Biopharma for USD 1.4 billion, and both transactions strengthened access to radiopharmaceutical assets. Bayer reported encouraging Phase I and II data in February 2026 for 225Ac-PSMA-Trillium, which combines a PSMA-targeting motif, albumin-binding domain, and Macropa chelator to support tumor retention. Large developers have sought multiyear isotope arrangements, treating allocation as a strategic requirement that must be secured alongside drug development instead of a routine procurement activity after clinical success. This approach combines pipeline ownership, supply security, and dedicated manufacturing arrangements, which can raise practical entry barriers for smaller developers without similar contracting capacity. The Alpha emitters market therefore favors companies that can coordinate drug development, isotope sourcing, specialized manufacturing, and the timing of late-stage clinical programs.

Expanding Isotope Production Infrastructure Improving Availability

New production investment is intended to address the actinium-225 shortage that has restricted trial activity and commercial planning, although new facilities still require time to enter qualified production. TerraPower Isotopes broke ground in May 2026 on a USD 450 million, 250,000-square-foot cGMP facility in Philadelphia that is designed to increase global actinium-225 capacity twentyfold and create 225 permanent positions[2]TerraPower Isotopes, “TerraPower Isotopes Breaks Ground On World’s Largest Actinium-225 Manufacturing Facility In Philadelphia,” TerraPower Isotopes, terrapower.com. Cardinal Health stated in April 2026 that it had quadrupled weekly actinium-225 output since routine production began in late 2024 and planned USD 150 million of investment over 3 years, with supply supporting more than 15 active clinical trials worldwide. ITM Radiopharma reported that its Actineer venture achieved a closed-loop radium-226 recycling process in 2025, which can improve precursor efficiency without requiring additional primary radium-226 sourcing. Orano Med completed a dry-in construction milestone for its lead-212 production facility in France during September 2025, with commercial startup planned for 2027 and a long-term capacity target to treat up to 25,000 patients annually. These projects can expand available supply and diversify isotope production pathways, but commercial-grade delivery will still depend on qualification, reliable operations, and logistics that match the short half-lives of the materials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Manufacturing Capacity | -1.2% | Global | Short term (≤ 2 years) |

| Specialized Infrastructure Requirements | -0.6% | All geographies excluding North America | Medium term (2-4 years) |

| Inconsistent Reimbursement Guidelines | -0.4% | Europe, Asia-Pacific, and Middle East and Africa | Long term (≥ 4 years) |

| Limited Long-Term Safety Data And Physician Familiarity | -0.3% | Asia-Pacific, South America, and Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Manufacturing Capacity Creating Supply Bottlenecks

The Alpha emitters market still faces a gap between isotope output and the requirements of expanding clinical programs, even though producers are investing in new capacity. Actinium-225 has a 9.9-day half-life, which leaves limited time for production, quality testing, shipping, and patient administration and makes each step operationally dependent on the last. A disruption at one qualified facility can therefore delay several studies and treatment schedules at the same time because there is limited opportunity to hold replacement inventory. The present supplier base for cGMP-grade actinium-225 remains narrow relative to the number of late-stage programs seeking supply, which creates concentration risk for developers and trial sites. Facility construction alone does not resolve the issue because radiopharmaceutical production requires validation and cGMP qualification before material can support commercial use at consistent quality. Supply pressure may therefore persist into 2027 even as newly announced capacity is built, particularly for programs that need dependable allocations rather than occasional production batches.

Specialized Infrastructure Requirements Driving Provider Costs

Treatment delivery requires shielded administration suites, trained nuclear medicine physicians, dosimetry capability, and approved radioactive waste disposal, creating an operational threshold that many community oncology centers do not currently meet. These centers would need substantial capital investment to establish the required facilities and staffing, which can keep qualified treatment networks concentrated in large hospitals and academic settings. The Alpha emitters market can therefore face access limits even when a product has regulatory approval and reimbursement because patients still require a nearby qualified administration site. Lead-212 has a 10.6-hour half-life, which further requires careful logistics, cold-chain management, and just-in-time coordination from production through patient dosing. Generator-produced isotopes can offer operational advantages because daughter-isotope generation can extend practical availability at the point of care and reduce dependence on direct shipment of the final isotope. Until provider networks expand, hospitals and academic centers will remain the main treatment settings in many countries, which can slow broader adoption outside established nuclear medicine systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type Of Radionuclide: Lead-212 Expands Development Beyond Radium-223

Radium-223 held 61.77% of the Alpha emitters market share in 2025 because it remained the only commercially approved alpha emitter and had an established clinical position. Its position reflects use in metastatic castration-resistant prostate cancer with symptomatic bone metastases, where hospitals already had relevant treatment procedures. PEACE-3 and post-market evidence have added clinical information that can support earlier placement in treatment pathways for appropriate patients. Actinium-225 has attracted substantial developmental investment, with several programs in later-stage evaluation and a growing group of cGMP supply agreements intended to support development. Bismuth-212, bismuth-213, and other radionuclides such as terbium-149 remain mainly in academic, preclinical, or early Phase I work, with short half-lives and distribution needs limiting their immediate commercial role.

Lead-212 is projected to record a 29.57% CAGR from 2026 to 2031, making it the fastest-growing radionuclide category in the Alpha emitters market. Its 10.6-hour half-life supports labeling and clinical delivery, while its decay sequence through bismuth-212 provides sequential alpha and beta emissions intended to concentrate dose at the tumor site. AlphaMedix received FDA Breakthrough Designation in 2024 for gastroenteropancreatic neuroendocrine tumors, and Orano Med expanded its collaboration with Roche in December 2025. Bicycle Therapeutics announced an end-to-end lead-212 supply chain in December 2025 for its BRC platform, which uses peptide-targeting agents for EphA2 and MT1-MMP. The growth of lead-212 increases the importance of thorium-228 generator networks, diversifies supply risk beyond cyclotron or reactor capacity, and could support wider distribution where direct actinium-225 supply is difficult.

By Application: Prostate Cancer Anchors Revenue While Endocrine Tumors Advance

Prostate Cancer accounted for 50.66% of the Alpha emitters market share in 2025, supported by radium-223 use in metastatic castration-resistant prostate cancer with symptomatic bone metastases. The Alpha emitters market size associated with this application also reflects a pipeline of PSMA-targeting actinium-225 conjugates that are progressing through later-stage evaluation. Bone Metastasis remains a major indication because radium-223 acts as a calcium mimic and localizes to bone, although its clinical use overlaps with prostate cancer treatment. Ovarian Cancer and Pancreatic Cancer remain earlier-stage applications for alpha therapy because both can involve radioresistant and disseminated disease. Their adoption during the forecast period depends on regulatory-grade Phase III evidence that can establish the treatment role and support regulatory decisions.

Endocrine Tumors is expected to grow at a 21.63% CAGR through 2031, the highest application growth rate in the Alpha emitters market. Phase Ib ACTION-1 data for 225Ac-DOTATATE in gastroenteropancreatic neuroendocrine tumors reported a confirmed objective response rate of 29.4% and no serious treatment-related adverse events. A 2025 systematic review and meta-analysis also assessed actinium-225 DOTATATE in advanced, metastatic, or inoperable neuroendocrine neoplasms. Patients receiving alpha therapy in this setting commonly have exhausted lutetium-177 peptide receptor radionuclide therapy, and wider use of lutetium-177 can enlarge the later group considered for alpha therapy. Other applications include hematological malignancies, solid tumors addressed through antibody radioconjugates, and emerging FAP-targeting programs that are still gaining early clinical attention.

By End User: Academic Medical Centers Build Treatment Capability

Hospitals accounted for 56.55% of the Alpha emitters market share in 2025 because they have radiation-handling infrastructure, licensed specialists, and compliance processes for radioactive drugs. Large tertiary hospitals and integrated cancer networks have supported much of the existing radium-223 treatment volume through established radiopharmacy departments and dosimetry teams. Their operational capacity allows them to administer short-lived isotopes more readily than smaller providers that do not have dedicated nuclear medicine facilities. Other end users include specialized radiopharmacy compounding centers and contract research organizations, which have a growing role in regional distribution of short-lived isotopes. Direct patient treatment nevertheless remains concentrated in credentialed clinical facilities because they meet the practical and regulatory requirements for administration.

Academic Medical Centers are projected to expand at a 16.92% CAGR through 2031 in the Alpha emitters industry. These institutions serve as trial sites for investigator-initiated and sponsor-led Phase I through Phase III studies, which gives clinical teams practical experience before wider use. The University of Pennsylvania is listed as a lead sponsor for the Phase I 211At-MABG study in advanced neuroendocrine cancers, with enrollment planned for August 2026 in collaboration with the National Cancer Institute. Trial activity helps radiation oncology, nuclear medicine, and medical physics teams develop operational expertise that can later move through affiliated hospital systems. Academic center growth therefore matters beyond current revenue because it can increase the qualified administration network that presently limits commercial access in many locations.

Geography Analysis

North America held 50.09% of the Alpha emitters market share in 2025, supported by the FDA-approved Xofigo platform, established nuclear medicine centers, and concentrated clinical trial activity. The United States benefits from regulatory pathways for radiopharmaceuticals with demonstrated clinical benefit, while Orano Med’s AlphaMedix received FDA Breakthrough Designation in 2024. Canada contributes to supply through its partnership in the Actineer venture. Mexico remains at an earlier stage because nuclear medicine infrastructure is more limited. The presence of actinium-225 producers in Michigan, Indiana, Philadelphia, and Wisconsin gives the region an important supply-chain advantage.

The United States is a major center for commercial isotope supply, with IONETIX, Cardinal Health, TerraPower Isotopes, and SHINE Technologies operating or developing production capacity. SHINE Technologies received a USD 263 million conditional commitment from the US Department of Energy in April 2026 for medical isotope manufacturing infrastructure. Europe held the second-largest geographic position, with Germany and France accounting for much of regional activity through nuclear medicine centers and radiopharmaceutical production. Eckert & Ziegler expanded its supply network through agreements with Actinium Pharmaceuticals, GlyTherix, and SK Biopharmaceuticals during 2024 and 2025. Orano Med is investing EUR 250 million (USD 284.3 million) in its ATEF facility, with EUR 22 million (USD 25 million) of French government support under France 2030, to develop industrial-scale lead-212 precursor production. Middle East and Africa and South America remain smaller contributors because treatment infrastructure and isotope import logistics are less developed.

Asia-Pacific is forecast to grow at an 18.17% CAGR through 2031, making it the fastest-growing regional part of the Alpha emitters market size. Japan has an established alpha therapy research base and accelerated review pathways for novel radiopharmaceuticals. The Alpha-T1 trial at Osaka University evaluated [211At]NaAt in radioiodine-refractory differentiated thyroid cancer and reported tolerability and preliminary efficacy in 11 patients. South Korea’s planned domestic actinium-225 production can shorten supply lines and reduce dose costs for developers. China’s Healthy China 2030 initiative includes support for advanced oncology modalities and targeted radionuclide therapy. Government-backed isotope localization efforts can reduce import dependence and encourage a domestic alpha therapy ecosystem within the forecast period.

Competitive Landscape

The Alpha emitters market has medium concentration because radium-223 dichloride generated most commercial revenue while a larger group of developers and producers remained in clinical or supply-stage activity. Leading participants are pursuing vertical integration across targeting vectors, isotope supply agreements, and manufacturing capacity in response to the limited availability of actinium-225 and lead-212. AstraZeneca’s acquisition of Fusion Pharmaceuticals and Eli Lilly’s acquisition of Point Biopharma reflect the strategic value attached to radiopharmaceutical pipelines. These transactions also show that isotope access and alpha-payload expertise are being evaluated alongside clinical-stage assets. Isotope producers have become strategic partners rather than routine input suppliers.

Bayer is developing next-generation alpha therapy while retaining its commercial radium-223 platform. Its February 2026 update on 225Ac-PSMA-Trillium showed continued work on a targeted radionuclide therapy that uses a PSMA-targeting motif, albumin-binding domain, and Macropa chelator. Orano Med advanced its lead-212 program and collaboration with Roche, reinforcing the role of lead-212 in future targeted treatment development. Cardinal Health expanded its actinium-225 production line during April 2026, supporting more than 15 active clinical trials globally. Long-term allocations can create switching costs and reward companies that establish supply relationships early.

The Alpha emitters market has open areas in combination treatments and smaller tumor targets. Radium-223 combinations with androgen receptor pathway inhibitors have documented mechanisms that may support further clinical study. Antibody radioconjugates are being considered for micrometastatic hematologic disease and peritoneal carcinomatosis, including Actinium Pharmaceuticals’ ATNM-400 program disclosed in its 2025 filing[3]Actinium Pharmaceuticals Inc., “Form 10-Q, Quarterly Report,” US Securities and Exchange Commission Filing, actiniumpharma.com. Generator-based lead-212 suppliers may have an advantage in regions where cyclotron infrastructure and centralized isotope logistics remain limited. Nusano’s accelerator-based multi-isotope model and the January 2026 NorthStar Medical Radioisotopes and Convergent Therapeutics partnership show how infrastructure partnerships are becoming part of competition. The competitive structure may become less concentrated as more late-stage programs secure supply and approach commercialization.

Alpha Emitters Industry Leaders

BWXT Medical Ltd.

Eckert & Ziegler

NorthStar Medical Radioisotopes LLC

State Atomic Energy Corporation (Rosatom)

TerraPower, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cardinal Health expanded Ac-225 production at its Center for Theranostics Advancement in Indianapolis, adding a high-capacity production line to its Drug Master File. The company has quadrupled weekly Ac-225 output since initiating routine production in late 2024 and plans a total USD 150 million investment over three years.

- February 2026: Niowave and Novartis signed a long-term global Ac-225 supply agreement providing Novartis with scalable isotope supply for its radioligand therapy portfolio. Niowave announced plans to begin construction of a new manufacturing facility in Lansing, Michigan, in early 2026 to support the expanded commitment.

Research Methodology Framework and Report Scope

Segmentation Overview

- By Type of Radionuclide

- Astatine-211

- Radium-223

- Actinium-225

- Lead-212

- Bismuth-212

- Other Radionuclides

- By Application

- Prostate Cancer

- Bone Metastasis

- Ovarian Cancer

- Pancreatic Cancer

- Endocrine Tumors

- Other Applications

- By End User

- Hospitals

- Academic Medical Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Key Questions Answered in the Report

What is the projected size of the alpha emitters market by 2031?

The Alpha emitters market is forecast to reach USD 698.98 million by 2031 from USD 322.54 million in 2026, at a 16.73% CAGR.

Which radionuclide leads current revenue?

Radium-223 led radionuclide revenue with a 61.77% share in 2025, supported by its commercial approval and established clinical use.

Which alpha-emitting radionuclide is growing fastest?

Lead-212 is projected to grow at a 29.57% CAGR through 2031, supported by development programs and thorium-228 generator supply models.

Which cancer application has the largest revenue position?

Prostate Cancer held 50.66% of 2025 revenue, while Endocrine Tumors is the fastest-growing application at a 21.63% CAGR through 2031.

Why is isotope supply important for alpha therapy development?

Actinium-225 has a 9.9-day half-life, so production, testing, shipment, and administration must occur within a narrow operating window.

Which region is expected to grow fastest through 2031?

Asia-Pacific is forecast to expand at an 18.17% CAGR through 2031, supported by regulatory modernization and growing isotope infrastructure.

Page last updated on: