Market Overview

| Study Period | 2019 - 2030 |

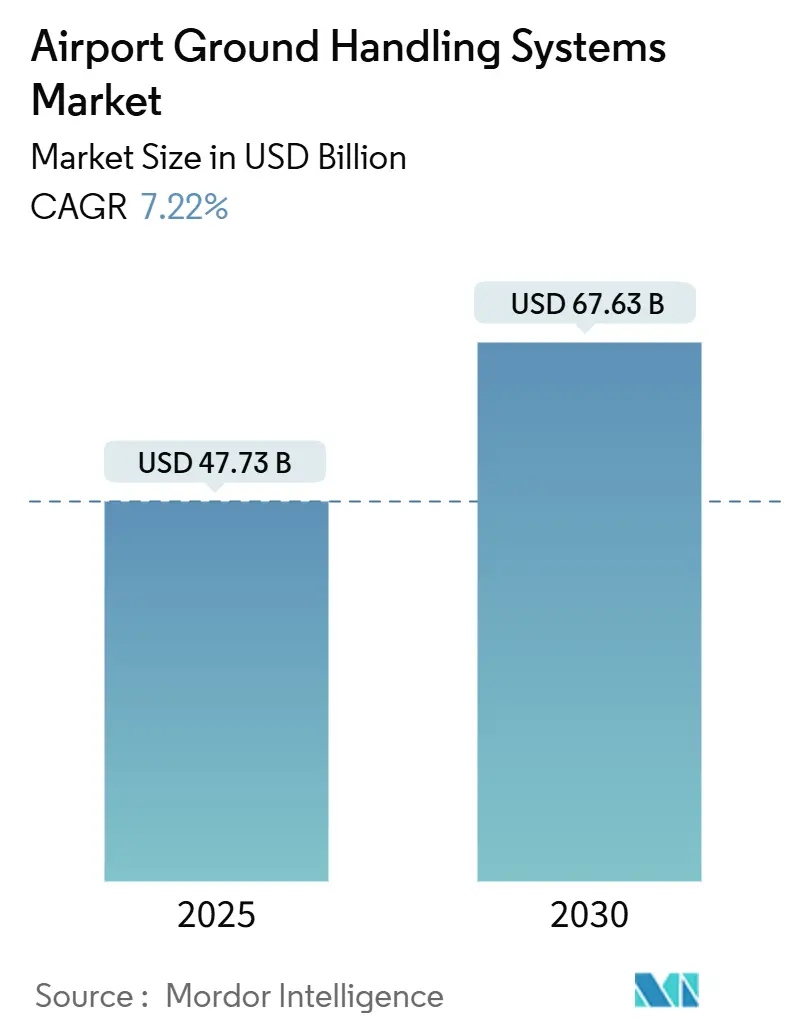

| Market Size (2025) | USD 47.73 Billion |

| Market Size (2030) | USD 67.63 Billion |

| Growth Rate (2025 - 2030) | 7.22% CAGR |

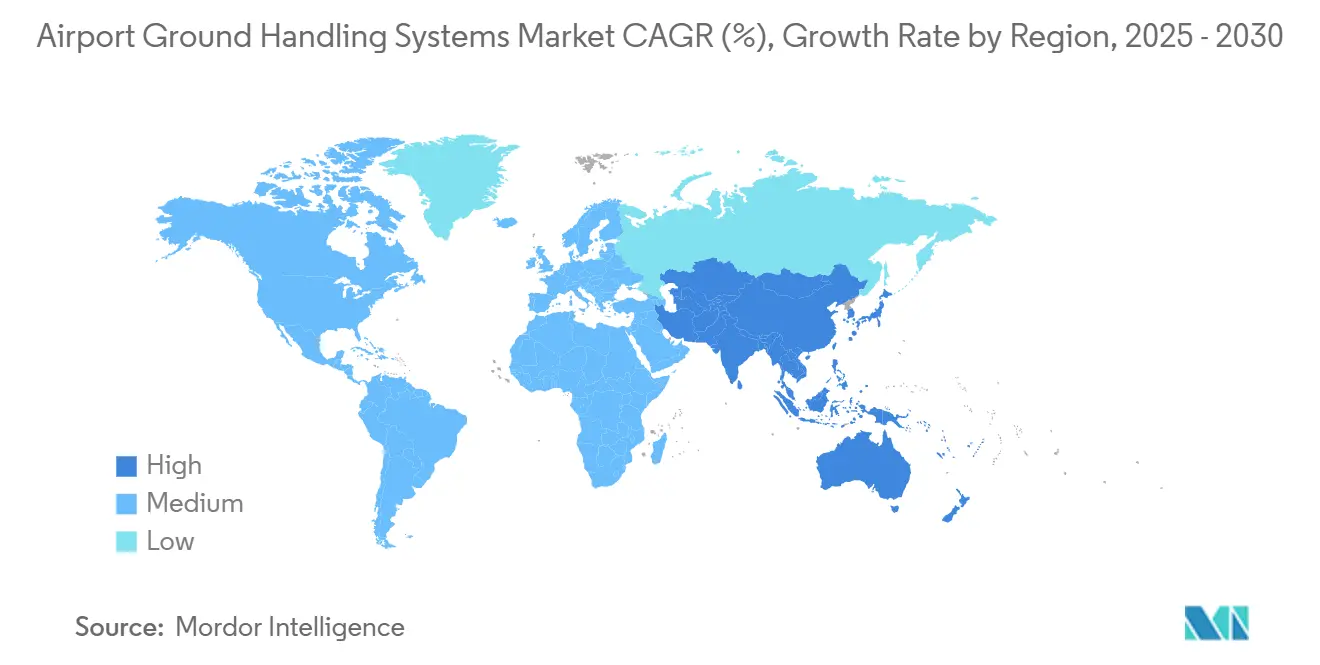

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Airport Ground Handling Systems Market Analysis by Mordor Intelligence

The airport ground handling systems market stood at USD 47.73 billion in 2025 and was forecast to reach USD 67.63 billion by 2030, advancing at a 7.22% CAGR. The expansion captured the aviation sector’s rapid push for greener ramp operations, the need to process rising passenger and cargo volumes at capacity-constrained hubs, and the widespread digitalization of asset management systems. Airlines up-gauged fleets to wide-bodies, driving replacement demand for powerful tractors and larger passenger bridges. At the same time, airport operators redirected capital budgets toward electrified fleets to meet tightening carbon targets and to lower fuel and maintenance expenses. Government incentives, led by the FAA’s PFAS-replacement grant program in the United States, accelerated the adoption of fluorine-free firefighting and de-icing assets. Competitive pressures intensified as manufacturers introduced autonomous baggage movers, real-time telematics, and 5G-enabled predictive maintenance suites that lifted equipment utilization rates while mitigating labor shortages.

Key Report Takeaways

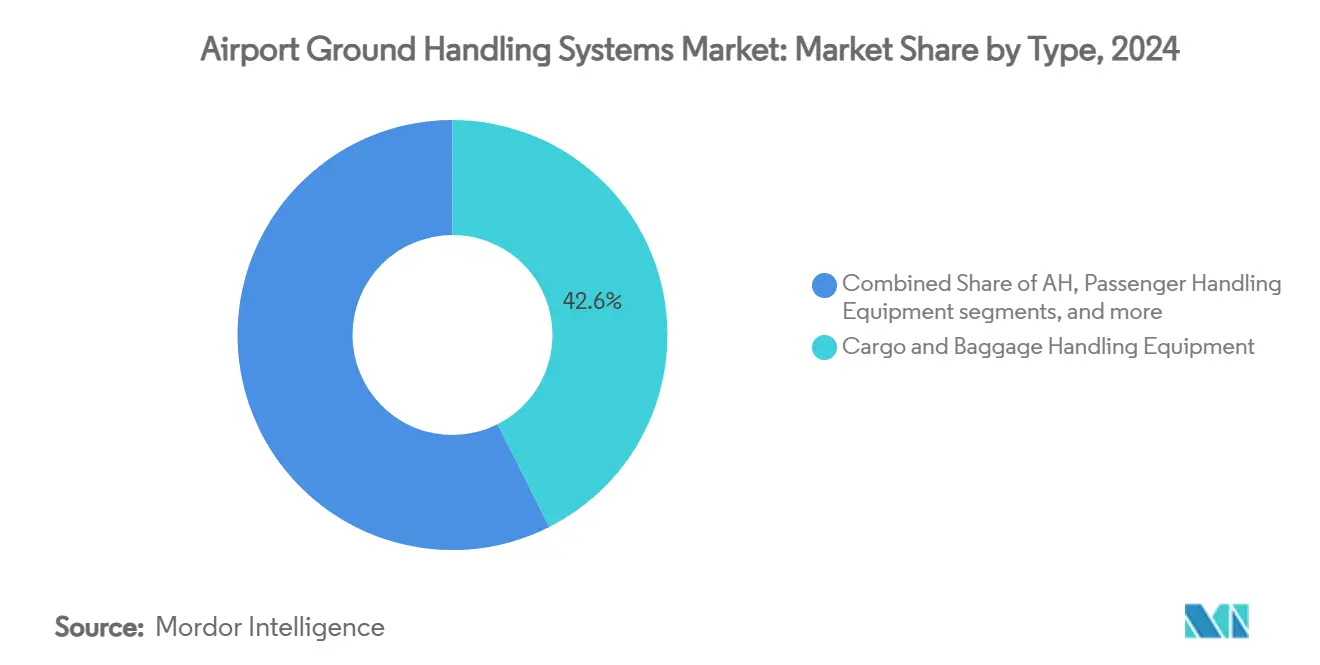

- By type, cargo and baggage handling equipment led with 42.56% of the airport ground handling systems market share in 2024; passenger handling equipment was projected to post the fastest 8.21% CAGR through 2030.

- By power source, non-electric units accounted for a 62.50% share of the airport ground handling systems market size in 2024, while electric alternatives were expected to expand at a 10.45% CAGR to 2030.

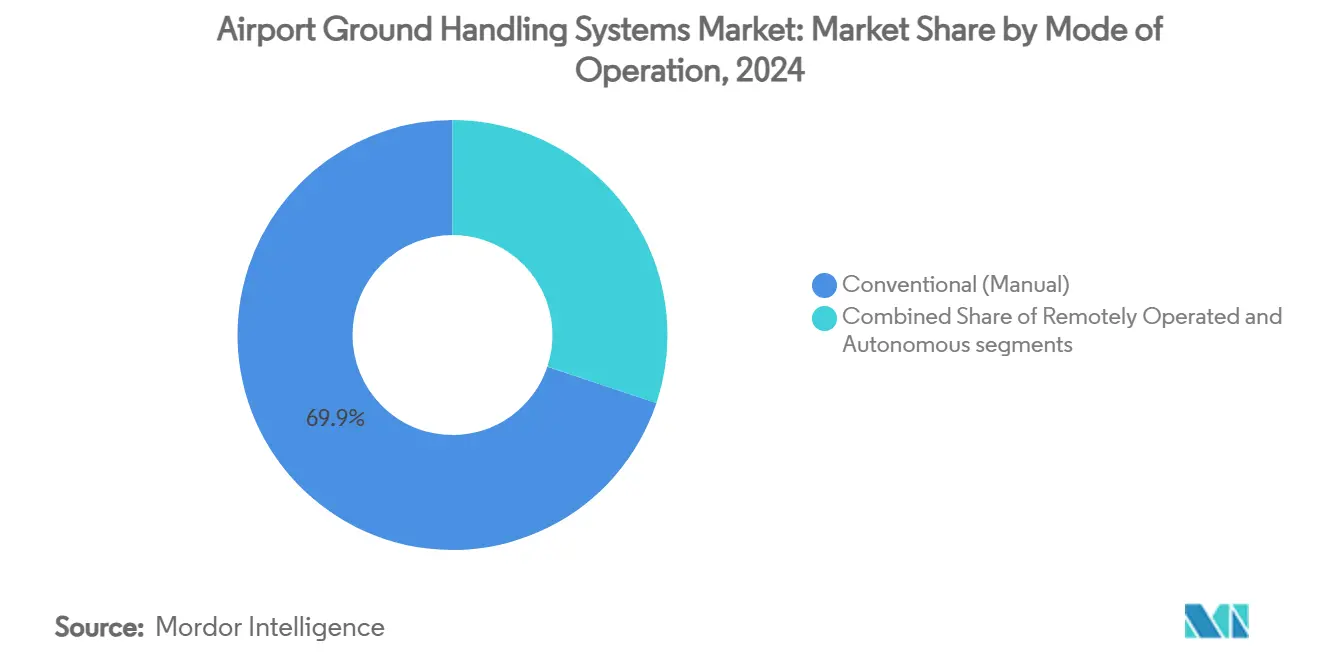

- By mode of operation, conventional-operated systems held 69.87% share of the airport ground handling systems market in 2024; autonomous systems recorded the highest 12.40% projected CAGR through 2030.

- By end user, commercial airports represented 78.85% of the airport ground handling systems market size in 2024, whereas military airports were projected to register a 9.78% CAGR between 2025 and 2030.

- By geography, Asia-Pacific dominated with 39.80% airport ground handling systems market share in 2024 and was expected to remain the fastest-growing region at an 8.45% CAGR.

Global Airport Ground Handling Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet up-gauging at slot-constrained hubs | +1.2% | North America and Europe; spill-over to APAC | Medium term (2-4 years) |

| Surge in green-airport capex programs | +1.8% | Global; early gains in Europe, North America | Long term (≥ 4 years) |

| Low-touch passenger processes (e.g. biometrics) | +0.9% | Global; concentrated at major international hubs | Short term (≤ 2 years) |

| 5G-enabled asset-tracking and predictive maintenance | +1.1% | APAC core; spill-over to North America and Europe | Medium term (2-4 years) |

| On-airport hydrogen infrastructure pilots | +0.7% | Europe and North America; selective APAC markets | Long term (≥ 4 years) |

| Expansion of "GSE-as-a-Service" leasing and pooling models | +1.3% | North America and Europe initially, expanding to APAC and emerging markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Fleet Up-Gauging at Slot-Constrained Hubs

Airlines turned to larger A350 and future B777X platforms to maximise revenue per scarce slot, forcing airports to procure higher-capacity loaders, powerful dual-mode pushback tractors, and taller passenger boarding bridges.[1]Source: Boeing, “Airport Compatibility for Wide-Body Aircraft,” boeing.com The heavier equipment shortened replacement cycles for legacy fleets that could not safely service widebodies. Operators at Heathrow, JFK, and Narita prioritised high-throughput stand equipment to keep turnaround times flat even as per-flight passenger counts rose. Leasing companies also entered the airport ground handling systems market to finance the premium assets, enabling smaller hubs to keep pace with airline fleet shifts.

Surge in Green-Airport Capex Programmes

Airports channelled record investments into electrified fleets after ESG-linked financing cut the cost of capital for low-carbon projects. Dnata’s USD 210 million commitment in May 2025 underscored how electrified tractors, loaders, and buses delivered 40-60% lower operating costs and immediate emissions cuts. European operators reacted quickly to the EU taxonomy rules by tying concession renewals to demonstrable CO₂ reductions. The wave of purchase orders lifted utilization at battery charging networks and sparked airport-wide load-management software deployments that aligned charging cycles with flight schedules.

Low-Touch Passenger Processes (Biometrics)

Biometric boarding and bag-drop systems compressed passenger dwell times and shifted peak baggage loads into tighter windows. Cincinnati/Northern Kentucky’s deployment of the Auto-DollyTug in 2024 revealed how AI-driven routing software matched each dollie’s dispatch to real-time passenger data, shrinking equipment idle time and cutting apron congestion. Airports that rolled out face-recognition gates saw a 25-35% drop in queue times, compelling handlers to speed up loading cycles with semi-autonomous conveyors and faster belt loaders.

5G-Enabled Asset-Tracking and Predictive Maintenance

Private 5G networks, such as the one Köln Bonn Airport installed in 2024, enabled millisecond-latency telemetry for thousands of ramp assets.[2]Source: NTT, “Köln Bonn Airport Private 5G Case Study,” services.global.ntt Maintenance teams shifted from reactive repairs to predictive scheduling, lifting electric fleet uptime by up to 25%. Deep battery analytics identified early-stage cell degradation, allowing packs to be swapped before winter peaks. The connectivity backbone also unlocked dynamic dispatching, routing the closest-available tractor to stands and cutting fuel burn on positioning runs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical airport capex linked to traffic volatility | -1.5% | Global; particularly leisure-dependent markets | Short term (≤ 2 years) |

| ROI uncertainty for fully-electric GSE in cold climates | -0.8% | Northern North America, Northern Europe, parts of Asia | Medium term (2-4 years) |

| Air-side labor union resistance to autonomy | -0.6% | North America and Europe; selective APAC | Medium term (2-4 years) |

| PFAS regulations impacting AFFF-based de-icers | -0.4% | Global; immediate impact in North America and EU | Short term (≤ 2 years) |

Source: Mordor Intelligence

Cyclical Airport Capex Linked to Traffic Volatility

Passenger dips triggered by macro shocks led many leisure-focused airports to defer equipment renewals in 2024, prioritising revenue-generating retail refurbishments over ramp assets. Rising interest rates further squeezed borrowing capacity, slowing award cycles for electrification tenders even as regulatory deadlines loomed. Small regional hubs with thinner cash reserves were the most exposed, prompting OEMs to offer pay-per-use and leasing models to sustain order pipelines.

ROI Uncertainty for Fully-Electric GSE in Cold Climates

Sub-zero operations cut battery efficiency by up to 40%, forcing airports in Canada, Scandinavia, and Northern Japan to install heated chargers and insulated garages that added 20-25% to lifetime costs. Several pilots reverted to hybrid tractors after persistent winter reliability gaps eroded service-level agreements. Manufacturers fast-tracked solid-state battery R&D, but the performance parity milestone was not expected before 2027, limiting electric penetration across roughly a quarter of global stations. [3]Source: ALVEST Group, “ESG Report 2023,” tld-group.com

Segment Analysis

By Type: Cargo Operations Drive Equipment Demand

Cargo and baggage handling assets commanded 42.56% of the airport ground handling systems market share in 2024 and remained vital as e-commerce volumes kept overnight express lanes full. The airport ground handling systems market size for cargo loaders and belt systems was projected to post steady revenue through 2030 as airlines converted holds for high-yield freight. SATS’ 2025 partnership with Guangtai illustrated how handlers co-developed fully automated cargo decks to tackle labour scarcity and next-day delivery commitments.

Passenger handling equipment, though smaller, recorded the strongest 8.21% CAGR as biometric gates and premium boarding bridges improved on-time performance metrics. Airports upgraded apron buses with low-floor electric units that cut boarding time and accommodated contactless payment. Aircraft handling equipment held a stable slice of the airport ground handling systems market as fleet up-gauging mandated higher-torque pushbacks and taller maintenance platforms. Ramp support gear, including hybrid de-icers compatible with fluorine-free foams, grew as regulatory deadlines approached, opening a niche for retrofit kits that extended legacy chassis life cycles.

Note: Segment shares of all individual segments available upon report purchase

By Power Source: Electric Transition Accelerates

Non-electric fleets still formed 62.50% of the airport ground handling systems market in 2024, yet the electric cohort notched a robust 10.45% CAGR. Light-duty baggage tractors were frequently the first to switch, supported by quick-swap battery cabinets that avoided peak-hour downtime. Finance providers structured green-linked revolving credit lines, such as Swissport’s 2024 facility, to lower barriers for bulk conversions.

Heavy-duty loaders and de-icers turned to hybrid drivetrains as interim solutions because charging speeds under cold ambient temperatures often failed to match peak turnaround windows. Hydrogen pilots under the Airbus GOLIAT project signalled an alternative for equipment that demanded high duty cycles and rapid refuelling; early demonstrations suggested the fuel could capture up to 20% share of this sub-segment by 2030.

By Mode of Operation: Automation Gains Momentum

Manual control systems retained 69.87% of the airport ground handling systems market share in 2024, but faced a rapid shift towards autonomy as labour shortages worsened and safety regulations tightened. Semi-autonomous tugs used geofenced pathways to shuttle bags, freeing staff to manage exceptions rather than routine hauls. FAA guidance issued in early 2025 set baseline standards for fail-safe logic and remote hand-off procedures, giving operators clarity on certification pathways.

Labour unions raised concerns over displacement, echoing port-sector disputes reported by CNBC, yet negotiated upskilling clauses that created new remote-operator and data-analyst roles. The controlled airport perimeter, compared with open-access container terminals, eased implementation barriers and allowed stepwise deployments that layered autonomy atop existing fleets.

By End User: Military Modernization Drives Faster Growth

Commercial hubs drove 78.85% of the airport ground handling systems market size in 2024, buoyed by competitive concession regimes that rewarded quick turnarounds and low emissions. Brands such as ALVEST leveraged ESG-centric procurement criteria to secure framework agreements with Europe’s top five hubs.

Although smaller, military airfields grew at a faster 9.78% CAGR as defence ministries migrated to next-generation transport aircraft like the KC-46 that required larger loaders and advanced refuellers. The USD 10.8 million US Air Force order in January 2025 illustrated sustained federal capital flows, enabling OEMs to develop ruggedised autonomous solutions that later cascaded into civilian variants.

Geography Analysis

Asia-Pacific captured 39.80% of the market in 2024, with an 8.45% CAGR. Aggressive infrastructure programs in China, India, and Indonesia filled backlogs for new loaders, passenger stairs, and GPU units. Flagship airports such as Beijing Daxing introduced full-suite asset-tracking, allowing domestic manufacturers to field-test autonomous vehicles at scale before exporting to Africa.

North America ranked second as the FAA’s USD 2 million PFAS grants and state-level zero-emission mandates spurred bulk replacement orders for firefighting vehicles and e-GPU carts. Mature hub operators used predictive maintenance tools to squeeze extra cycles from ageing fleets while waiting for hydrogen pilots to prove cost parity in sub-zero operations.

Europe pioneered decarbonization metrics that tied bond coupons to CO₂ per-turnaround thresholds, nudging airports toward fleet electrification ahead of 2030 climate benchmarks. Royal Schiphol Group ring-fenced EUR 6 billion (USD 7.03 billion) for low-emission infrastructure, with a sizable allocation to apron equipment electrification.

The Middle East funnelled oil revenue diversification funds into mega-hub expansions at Riyadh and Doha, specifying premium boarding bridges, high-capacity cargo loaders, and autonomous dolly systems. Africa’s smaller but fast-growing aviation sector leapfrogged directly to electric tractors at green-field airports financed by multilateral climate funds, bypassing diesel infrastructure entirely to lock in lower lifetime emissions.

Competitive Landscape

The airport ground handling systems market displayed moderate fragmentation in 2025. ALVEST pushed electric models to 50% of its 2023 shipments and targeted the full phase-out of combustion engines by 2025. Textron leveraged a USD 3.3 billion Q1 2025 backlog to invest in autonomous drive modules and data platforms adaptable across its ground-handling brands.

Private-equity-backed roll-ups reshaped the mid-tier. CVC DIF’s 2024 acquisition of CTC Airport Equipment and SPS International created a full-line vendor to supply turnkey fleets to Chinese and Middle-Eastern green-field airports. Niche specialists carved out space in cold-climate electrification and hydrogen refuelling skids where incumbents were slower to respond.

Digital integrators partnered with OEMs to embed sensor suites and subscription telematics. Predictive-maintenance algorithms became a differentiator in multiyear service contracts, shifting revenue models from one-off sales to performance-based uptime guarantees. Suppliers able to quantify CO₂ savings and deliver platform-agnostic autonomy gained procurement preference under airports’ ESG scoring rubrics.

Airport Ground Handling Systems Industry Leaders

-

Tug Technologies Corporation (Textron Inc.)

-

Air T Inc.

-

Oshkosh AeroTech (Oshkosh Corporation)

-

Dabico Airport Solutions

-

Alvest Group Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Dnata committed USD 210 million to electrify its global fleet and lower ramp emissions.

- March 2025: SATS partnered with Guangtai to co-develop automated cargo handling solutions for Asian hubs.

Global Airport Ground Handling Systems Market Report Scope

Aircraft ground handling systems include equipment used to offer services to an aircraft while on the ground and parked at a terminal gate.

The market is segmented by type, power source, and geography. Based on type, the market is segmented into aircraft handling, passenger handling, and cargo and baggage handling. Based on power sources, the market is divided into non-electric and electric. The market does not include military cargo and baggage handling equipment. The report covers the market sizes and forecasts for the airport ground and cargo handling services market in major countries across different regions. For each segment, the market sizes and forecasts are provided in terms of value (USD).

| By Type | Aircraft Handling Equipment | |||

| Passenger Handling Equipment | ||||

| Cargo and Baggage Handling Equipment | ||||

| Ramp and Support Equipment | ||||

| By Power Source | Non-electric | |||

| Electric | ||||

| Hybrid | ||||

| By Mode of Operation | Conventional (Manual) | |||

| Remotely Operated | ||||

| Autonomous | ||||

| By End User | Commercial Airports | |||

| Military Airports | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | United Kingdom | |||

| Germany | ||||

| France | ||||

| Italy | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

By Type

| Aircraft Handling Equipment |

| Passenger Handling Equipment |

| Cargo and Baggage Handling Equipment |

| Ramp and Support Equipment |

By Power Source

| Non-electric |

| Electric |

| Hybrid |

By Mode of Operation

| Conventional (Manual) |

| Remotely Operated |

| Autonomous |

By End User

| Commercial Airports |

| Military Airports |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the airport ground handling systems market in 2025?

The market is valued USD 47.73 billion in 2025 and is projected to climb to USD 67.63 billion by 2030 at a 7.22% CAGR.

Which equipment segment generates the most revenue?

Cargo and baggage handling equipment held 42.56% of the airport ground handling systems market share in 2024, the highest among all segments.

What region grows the fastest through 2030?

Asia-Pacific is expected to post the strongest 8.45% CAGR, supported by new airport construction and fleet modernisation across China, India and Southeast Asia.

How quickly are electric ground support vehicles being adopted?

Electric ground support equipment is forecasted to register a 10.45% CAGR, outpacing the overall market as airports pursue decarbonisation and lower operating costs.

Why are autonomous systems gaining traction?

Labour shortages and the precision timing required by biometric passenger flows are propelling autonomous equipment, which is projected to grow at a 12.40% CAGR through 2030.

What challenges limit full electrification in cold climates?

Battery efficiency drops of up to 40% in sub-zero conditions increase total cost of ownership, delaying ROI and slowing adoption at northern airports until next-generation batteries arrive.