Air Crane Helicopter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

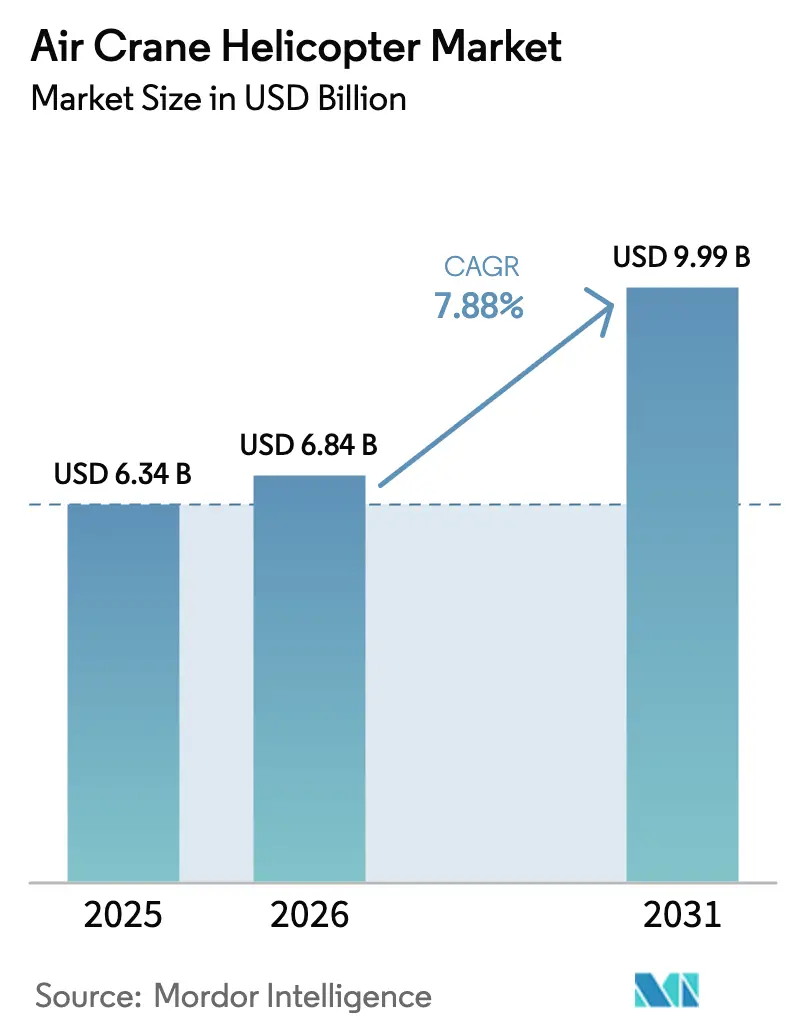

| Market Size (2026) | USD 6.84 Billion |

| Market Size (2031) | USD 9.99 Billion |

| Growth Rate (2026 - 2031) | 7.88% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Crane Helicopter Market Analysis by Mordor Intelligence

Air crane helicopter market size in 2026 is estimated at USD 6.84 billion, growing from 2025 value of USD 6.34 billion with 2031 projections showing USD 9.99 billion, growing at 7.88% CAGR over 2026-2031. Rising heavy-lift requirements across wildfire suppression, offshore wind installation, remote infrastructure replacement, and military recapitalization place the air crane helicopter market at the center of global logistics strategies. Civil agencies and defense ministries increasingly view these aircraft as the only practical option for moving multi-ton payloads into austere or environmentally sensitive sites. This shift has accelerated new-build demand and long-term leasing activity. Consolidation among operators continues, with integrated service providers capturing share by coupling lift capacity, specialized crews, and fleetwide maintenance programs. At the same time, engineering advances in hybrid-electric powertrains and survivability upgrades expand the mission envelope, reinforcing confidence in fleet renewal cycles. Heightened urgency around climate-driven disasters, sustained energy transition spending, and cross-border defense cooperation ensure a resilient growth trajectory for the air crane helicopter market through 2030.

Key Report Takeaways

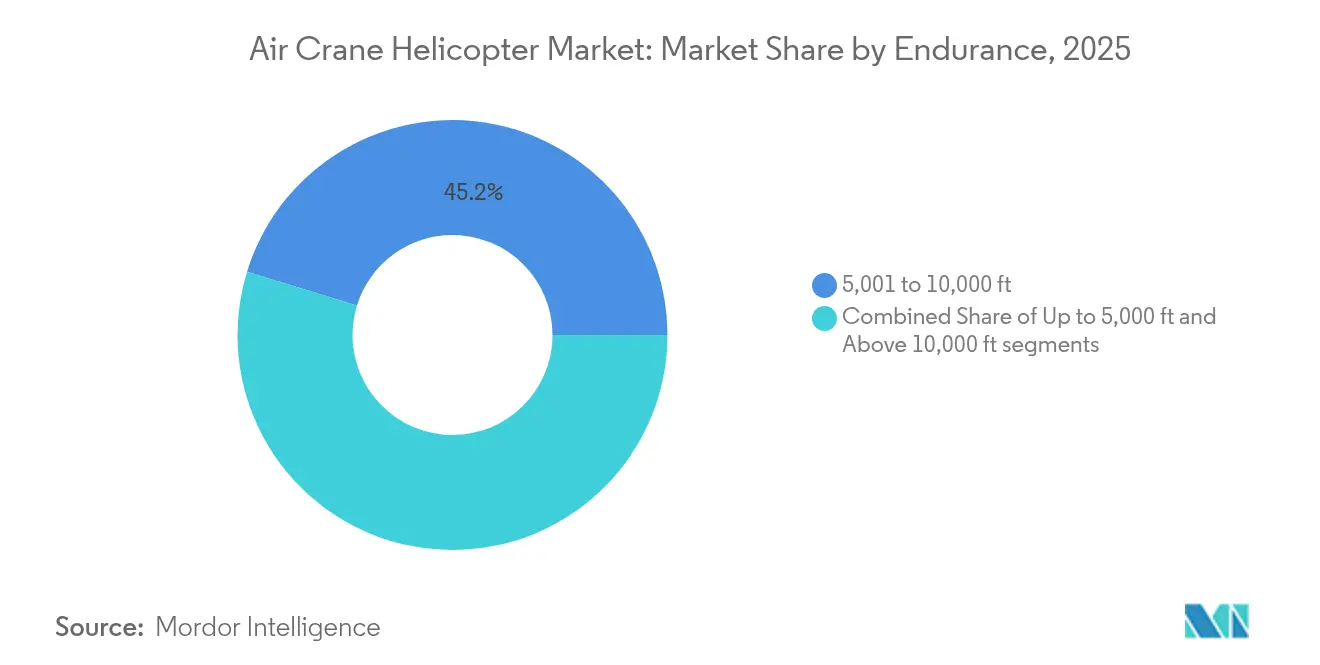

- By endurance, the 5,001-10,000 ft band held 45.24% of the air crane helicopter market share in 2025, while the above-10,000 ft band is projected to grow at a 9.18% CAGR through 2031.

- By load capacity, aircraft in the 3,001-6,000 lb bracket captured 39.35% of the air crane helicopter market size in 2025; the 12,001-15,000 lb bracket is advancing at a 9.78% CAGR between 2026-2031.

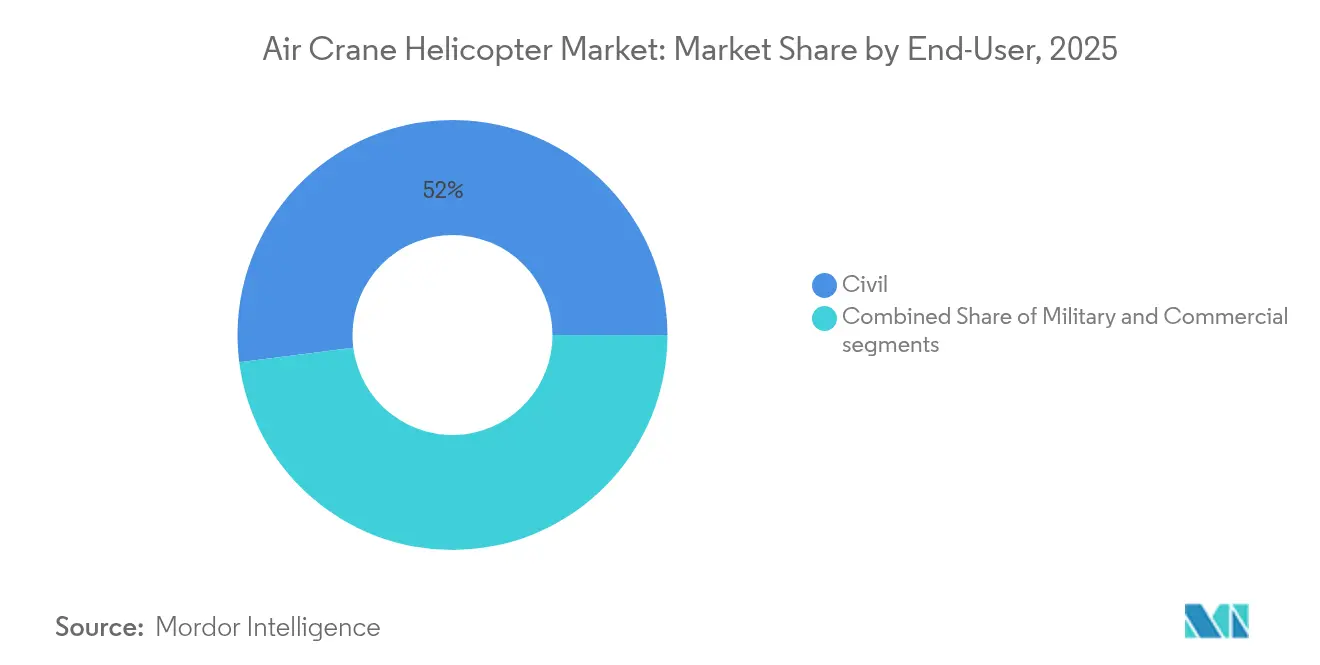

- By end-user, civil government operations commanded 52.02% of the air crane helicopter market share in 2025, whereas commercial operators are expanding at an 8.05% CAGR to 2031.

- By application, heavy construction and infrastructure activities accounted for 48.41% of the air crane helicopter market size in 2025; fire-fighting is rising fastest at a 9.35% CAGR through 2031.

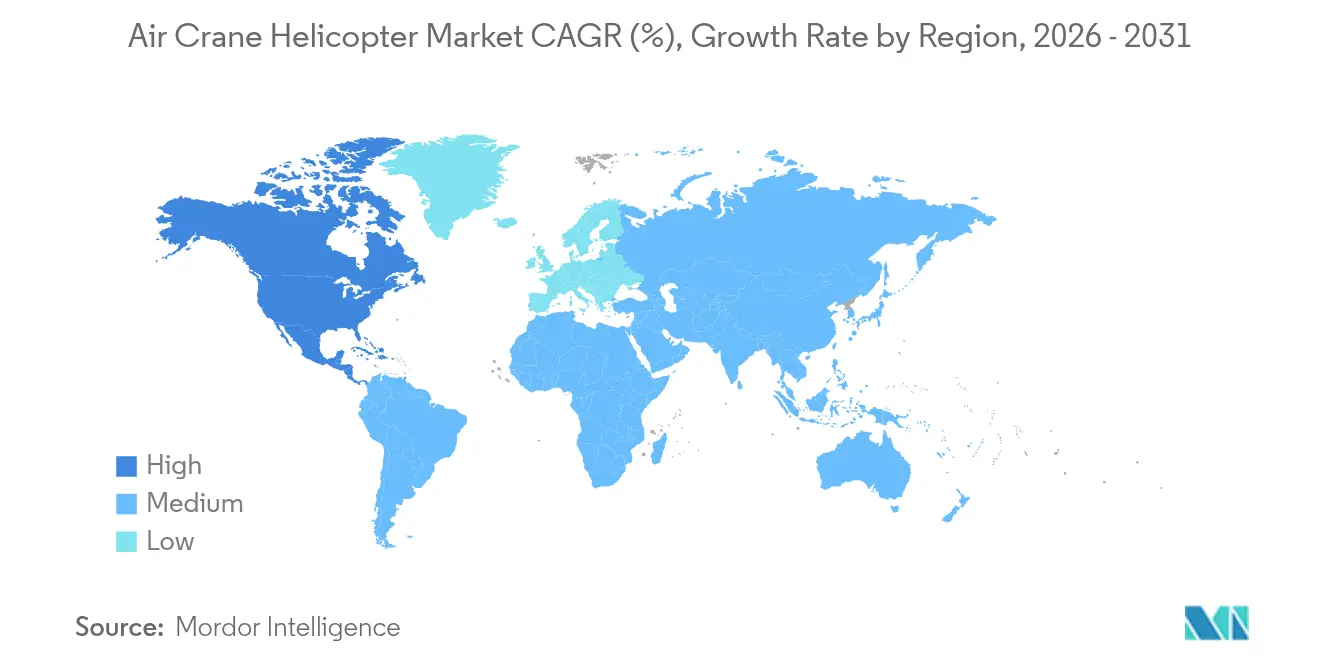

- Geographically, Asia-Pacific led with 43.12% of the air crane helicopter market share in 2025; North America posts the quickest regional CAGR of 7.32% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Air Crane Helicopter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy-lift demand from offshore wind turbine installation | +1.2% | North Sea, S. East Coast, East Asia | Medium term (2-4 years) |

| Emergency wildfire suppression contracts expanding in Western US and Australia | +0.9% | Western US, Australia, Mediterranean Europe | Short term (≤ 2 years) |

| Aging infrastructure replacement projects in remote areas (e.g., power-line towers) | +0.8% | North America, Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| Military rotorcraft fleet recapitalization programs (CH-53K, CH-47F Block II) | +1.1% | US, India, European NATO allies | Medium term (2-4 years) |

| Exploration of hybrid-electric propulsion conversions for S-64/CH-54 platforms | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Remote modular energy and mining projects (Arctic micro-grids, desert solar farms) needing heavy-lift assembly | +0.6% | Asia-Pacific, Middle East, Africa, Arctic | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heavy-lift Demand from Offshore Wind Turbine Installation

Offshore wind developers are moving turbines farther from shore and lifting nacelle weights past 120 tonnes, spurring specialized flight operations, reinforcing the air crane helicopter market. HTM Helicopters’ recent order for additional H145s dedicated to German and French wind farms took its fleet to eight aircraft, signaling a consistent fleet expansion by European service providers.[1]Airbus, “HTM Helicopters Orders Additional H145s for Offshore Wind,” airbus.com In North America, HeliService USA safely moved more than 2,500 technicians to Atlantic wind-farm sites between mid-2023 and early 2025, showcasing a cost-effective alternative to slow crew-transfer vessels. Medium-lift models in the 3,001-6,000 lb segment increasingly dominate crew change and light cargo missions because they balance payload with two-engine reliability in salt-spray environments. As turbine hub heights and rotor diameters grow, demand also spreads into heavier classes for pre-assembly lifts, widening revenue streams for the air crane helicopter market. Stakeholders expect sustained contract backlogs through at least 2029 as UK, Germany, Japan, and South Korean regulators approve new leases and tax incentives.

Emergency Wildfire Suppression Contracts Expanding

Climate-driven fire seasons extend beyond traditional summer windows, pushing civil agencies to fund multi-year helicopter availability programs. During Australia's season, Coulson Aviation closed a USD 400 million, 10-year contract with New South Wales Rural Fire Service to deploy CH-47 Chinooks and Type 1 tankers.[2]Coulson Aviation, “Coulson Aviation Awarded 10-Year NSW RFS Contract,” coulsonaviation.com The Forest Service's rule to overhaul aerial suppression procurement in the United States could triple annual flight hours for large helicopters by 2027. Greece followed with an order for eight H215s outfitted for night water drops exceeding 4,000 liters. Platform preferences skew toward aircraft able to ferry 10-12 crew, sling 10,000+ lb external loads, and integrate IR-stabilized mapping systems for nocturnal ops. Such capabilities allow quick redeployment across continents, sustaining utilization rates while deepening strategic relevance for the air crane helicopter market.

Aging Infrastructure Replacement Projects in Remote Areas

Electric-utility upgrades, mountain hydro renovations, and remote bridge rebuilds have converged to create a steady pipeline of multi-ton lifts. The Yoakum-Defrenn Heliport taxiway rehabilitation, valued between USD 25-100 million by the US Army Corps of Engineers, typifies projects that would otherwise need weeks of road closures. Power-line contractors leverage 6,001-12,000 lb helicopters to string new conductors across canyons, citing up to 40% savings against ground-based crane barges when terrain or environmental rules restrict land access. Renewable developers are applying the same model to solar farms on desert escarpments, where lifting prefabricated inverter stations by air prevents soil disturbance and shortens commissioning schedules. As governments earmark trillions for resilience and clean-energy infrastructure through 2030, the cumulative lift-hour demand reinforces high asset-utilization forecasts for the air crane helicopter market.

Military Rotorcraft Fleet Recapitalization Programs

Armed forces are fielding next-generation heavy-lifters with greater power margins, digital survivability suites, and wider mission sets. Boeing booked contracts topping USD 375 million for CH-47F Block II deliveries during 2024-2025 and another USD 240 million in 2025 for five MH-47Gs destined for Special Operations Aviation Command.[3]Boeing, “US Army Awards CH-47F Block II Contract,” boeing.com India’s landmark USD 7.36 billion order for 156 Prachand light combat helicopters gives Hindustan Aeronautics a production bridge until 2032 while satisfying high-altitude lift requirements above 5,000 m. International programs around the CH-53K, UH-60M, and CH-47 Block II keep assembly lines busy in the United States, Germany, and Japan, with unit prices amplified by comprehensive support packages. The cumulative procurement pipeline secures predictable deliveries throughout the decade, embedding a structural demand layer that buffers the air crane helicopter market from cyclical civil downturns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile aviation turbine fuel (ATF) prices squeezing operator margins | -1.4% | Global | Short term (≤ 2 years) |

| Shortage of certified Type I heavy-lift pilots and maintenance engineers | -0.8% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Scarcity of legacy spare-part inventories for retired airframes | -0.6% | Global, concentrated in CH-54 and early S-64 operators | Long term (≥ 4 years) |

| Stringent noise and emissions regulations limiting urban/EU heavy-lift flight permits | -0.5% | Europe, North American cities, developed Asia-Pacific urban corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Aviation Turbine Fuel Prices Squeezing Operator Margins

Jet-fuel costs represent almost one-third of direct operating expenses for Type I helicopter operators. The International Air Transport Association projected an average USD 2.7095 per gallon price for 2024 amid Middle-East supply risk, trimming margins for even the most efficient fleets.[4] IATA, “Jet Fuel Price Monitor,” iata.org Heavy-lift missions burn more than 500 gallons per hour when hovering with sling loads, magnifying price swings. Smaller charter firms lacking hedging tools confront cash-flow stress that limits fleet modernization, nudging them toward mergers or asset sales. Larger carriers invest in engine digital-twin monitoring, flight-profile optimization, and sustainable aviation fuel blends; however, SAF availability lingers below 1% of global supply, constraining immediate relief. Persistent volatility is therefore expected to temper rate increases and slow near-term capacity additions across the air crane helicopter market.

Shortage of Certified Type I Heavy-lift Pilots and Maintenance Engineers

Eighty percent of companies surveyed in Rotor Pro’s 2024 salary report cited pilot deficits, even with heavy-lift captains earning USD 110,000–200,000 annually. Regional airlines drawing rotorcraft talent into fixed-wing cockpits exacerbate attrition, and certification for external-load operations requires two to three years of supervised flying. Maintenance engineers certified on S-64s or CH-54s head toward retirement fast, while supply-chain bottlenecks limit retraining throughput. Vertical Aviation International formed a Workforce Development Working Group, but course approvals stretch into 2027, anchoring the staffing shortage through the medium term. Resulting downtime during peak fire and construction seasons can sideline 5-8% of global heavy-lift capacity, dampening growth potential for the air crane helicopter market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Endurance: High-Altitude Operations Drive Premium Demand

Endurance segmentation mirrors mission altitude more than flight duration. Aircraft certified for 5,001-10,000 ft operations commanded 45.24% of the air crane helicopter market share in 2025, anchored by mountainous power-line projects from the Rockies to the Himalayas. Operators cite these platforms’ ability to hover with payloads in thin air without sacrificing cycle economies. The air crane helicopter market size tied to this band will exceed USD 4.49 billion by 2031. Above-10,000 ft aircraft, historically niche, now expand at 9.18% CAGR as border patrols in Tibet, Andean renewable builds, and Alpine turbine swaps require even more power margin. Manufacturers respond with uprated engines, FADEC-driven torque control, and lighter composite blades that deliver 15-20% better lift-to-weight ratios. Conversely, the under-5,000 ft bracket maintains relevance for offshore wind shuttles and coastal SAR missions where density altitude is less punishing.

Mission specialists in the higher bands also invest heavily in avionics to handle variable wind shear and GNSS-degraded canyons. Enhanced‐vision systems, LPV approaches, and all-weather radars now appear as baseline configurations on new CH-47F Block II deliveries. Altitude-optimized rotorcraft enjoy premium hourly rates, offsetting ownership costs even when utilization trails utility helicopters. This economics reinforces R&D into propulsion de-rate management and de-icing automation, themes likely to dominate OEM roadmaps through 2032. The dynamic maintains a multi-tier aircraft ecosystem inside the broader air crane helicopter market, with platform choice increasingly guided by elevation-specific payload efficiency.

By Load Capacity: Heavy-Lift Segment Accelerates with Infrastructure Demand

Platforms in the 3,001 to 6,000 lbs class formed the core of day-to-day lifting, accounting for 39.35% of the air crane helicopter market size in 2025. Nevertheless, infrastructure megaprojects and expeditionary military logistics are tilting growth toward the 12,001 to 15,000 lbs category, forecasted at 9.78% CAGR through 2031. The CH-53K King Stallion’s 36,000 lbs external-lift demonstration for the US Marine Corps set a new benchmark, raising customer expectations for single-sortie capability. Utility markets still favor mid-capacity K-Max, AW189, and S-92 variants for conductor pulls, cellular-tower placement, and offshore wind nacelle access where deck clearances are limited.

Unit economics influence procurement decisions. High-capacity helicopters cost up to three times more per flight hour but can halve total lift cycles on a bridge-girder project, compressing schedule risk penalties. As insurance underwriters reward fewer ground resets and lower worksite congestion, project bid models tilt toward the upper capacity brackets. Meanwhile, OEMs innovate quick-attach modular rigs, letting 6,001 to 12,000 lbs aircraft undertake precision lifts one day and personnel shuttles the next, sustaining year-round use rates. These developments reinforce layered demand and diversify revenue in the air crane helicopter market.

By End-user: Commercial Sector Emerges as Growth Leader

Civil or government agencies such as forestry departments and emergency management offices retained 52.02% of the air crane helicopter market share in 2025, underpinned by multi-year wildfire and disaster relief budgets. Yet the commercial segment, spanning construction, mining, and energy, now posts an 8.05% CAGR through 2031, outpacing public buyers. The shift reflects public–private partnerships that outsource lift operations to specialized contractors seeking longer-term service leases instead of capital purchases. Helicopter Express’ acquisition of Erickson’s air-crane fleet exemplifies consolidation aimed at aggregating utilization across fire, wind, and infrastructure domains.

Military end-users continue to place pivotal volume orders but exhibit longer procurement cycles tied to budget appropriations. The US Army’s MH-47G Block II contract for five aircraft worth USD 240 million underscores selective modernization for special operations units. Commercial operators, by contrast, hedge cyclicality by negotiating power-by-the-hour packages with OEMs like Leonardo, ensuring predictable costs as flight hours swing with commodity prices. This service-centric purchasing behavior feeds a parallel growth track inside the air crane helicopter market, emphasizing uptime guarantees over outright fleet expansion.

By Application: Firefighting Surges with Climate Pressures

Heavy construction and infrastructure remained the largest application, contributing 48.41% of the air crane helicopter market size in 2025. Firefighting represents the fastest-growing use case at a 9.35% CAGR amid lengthening burn seasons from California to Greece. Governments channel dedicated climate-adaptation funds into rotorcraft acquisition, such as Greece’s EUR 800 million (USD 937.7 million) purchase of eight H215s for aerial suppression missions. Technical innovations like FAA-certified retractable tanks for CH-47s double sortie volumes and cut turnaround times, boosting water-delivery productivity.

Oil-and-gas support hours decline gradually as offshore wind ascends; however, helicopter providers often redeploy the same crews and airframes, smoothing fleet utilization. Timber-harvest activity faces stricter environmental rules, yet precision logging in protected zones still requires helicopters to mitigate ground disturbance. Diversification across emergency, industrial, and environmental portfolios thus creates a balanced demand mix, stabilizing growth in the broader air crane helicopter market.

Geography Analysis

Asia-Pacific dominated the air crane helicopter market with 43.12% share in 2025, propelled by Indian and Chinese procurement drives plus remote infrastructure projects across Indonesia, the Philippines, and Australia. India’s record USD 7.36 billion Prachand order aims for more than 65% localized content, bolstering indigenous supply chains and long-term maintenance ecosystems. Japan’s acquisition of 17 CH-47 Block II Chinooks and the Philippines’ plan to operate 47 S-70i Black Hawks illustrate sustained defense outlays across the region. Parallel civil demand stems from Australian wildfire campaigns and Indonesian hydro dam construction, creating year-round lift requirements that feed the regional air crane helicopter market.

North America remains the fastest-expanding region, tracking a 7.32% CAGR for 2026-2031. The US Infrastructure Investment and Jobs Act accelerates bridge and grid rebuilds, while Western wildfire budgets break spending records yearly. Bell Textron’s USD 632 million Fort Worth facility, scheduled to open in 2028 to assemble V-280 components, underscores the industrial confidence surrounding heavy-lift rotorcraft. Canada’s Griffon Limited Life Extension project keeps medium-lift fleets viable through the mid-2030s, ensuring cross-border MRO demand and technician training pipelines. These factors support the continent's dynamic and resilient air crane helicopter market.

Europe posts steady gains anchored by NATO capability targets and offshore wind expansion across the North Sea and Baltic. Greece’s EU-backed H215 firefighting contract highlights coordinated regional funding to address climate threats. The UK’s CH-47ER procurement guarantees Royal Air Force heavy-lift readiness beyond 2040, while Leonardo’s EUR 20.9 billion (USD 24.5 billion) order haul in 2024 demonstrates competitive momentum for European OEMs. Simultaneously, operators like HTM grow turbine-maintenance fleets, reinforcing pan-European network effects that amplify the air crane helicopter market’s value proposition.

Competitive Landscape

Market structure leans toward moderate concentration, with a handful of OEMs and vertically integrated operators supplying most global lift hours. Helicopter Express’ April 2025 purchase of Erickson’s S-64 Skycrane fleet fundamentally rebalanced commercial capacity, creating a trans-regional giant able to bid simultaneously on US fire contracts and Asian infrastructure lifts. The move mirrors a broader pattern where scale enables investment in advanced training, parts pooling, and fleet digitalization, differentiating leaders within the air crane helicopter market.

OEM strategies target lifecycle revenue over unit sales. Bristow Group’s power-by-the-hour deals with Leonardo for AW139 and AW189 fleets exemplify contracts that guarantee spare parts, simulators, and predictive analytics in exchange for multi-year flight-hour commitments. Boeing, Sikorsky, and GE Aerospace concurrently advance hybrid-electric demonstrators, betting that emission caps and fuel-cost volatility will accelerate adoption of turbine-battery architectures. These R&D races influence future platform competitiveness, especially for civil operators sensitive to ESG reporting.

Regional specialists defend niche domains through tailored capabilities. Arctic operators emphasize airframe winterization and satellite connectivity, while Middle-Eastern contractors market high-temperature derate kits. Such specialization sustains diversity, yet cross-border mergers may rise as pilot shortages and capital-intensive fleet refresh cycles pressure sub-scale firms. Technology investment, service bundling, and geographic breadth underpin competitive positioning in the air crane helicopter market.

Air Crane Helicopter Industry Leaders

Erickson Incorporated

Airbus Helicopters

Kaman Corporation

Bell Textron Inc.

Lockheed Martin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Leonardo and Weststar Aviation Services launched a USD 3.5 billion fleet-expansion program in Malaysia covering 28 helicopters.

- April 2025: Greece ordered eight Airbus H215s for forest-fire combat under EU-funded procurement.

- April 2025: Boeing delivered the fourth CH-47F Block II Chinook to the US Army, advancing fleet modernization.

- April 2024: Helicopter Express completed acquisition of Erickson’s operating division and S-64 Skycrane fleet, reshaping commercial heavy-lift supply.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the air-crane helicopter market as all newly built rotorcraft engineered or structurally modified at the factory to sling external loads above 3,000 lb for construction, emergency response, energy, and government heavy-lift missions. According to Mordor Intelligence, life-extended legacy fleets, aftermarket kits, tilt-rotors, eVTOLs, and unmanned cargo drones remain outside this scope.

Scope exclusion: fixed-wing tankers and other non-rotary aerial lifters are not covered.

Segmentation Overview

- By Endurance

- Up to 5,000 ft

- 5,001 to 10,000 ft

- Above 10,000 ft

- By Load Capacity

- Up to 3,000 lbs

- 3,001 to 6,000 lbs

- 6,001 to 12,000 lbs

- 12,001 to 15,000 lbs

- By End-user

- Civil (Forestry, Disaster Management)

- Commercial (Construction, Logging, Utility)

- Military

- By Application

- Firefighting

- Timber Harvest and Logging

- Heavy Construction and Infrastructure

- Oil and Gas/Offshore Wind Lifting

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with OEM engineers, aerial-construction operators across North America, Europe, and Asia-Pacific, and procurement leads in fire services. These discussions clarified payload breakpoints, utilization hours, ASP movements, and retirement intent, filling gaps left by public data.

Desk Research

We screen authoritative open sources such as FAA and EASA rotorcraft registries, national wildfire statistics, U.S. Census construction spending, UN Comtrade turbine-engine imports, and OECD defense-budget tables to size regional demand pools.

Those benchmarks are enriched with company 10-Ks, contract award notices, aerospace trade press, and paid feeds from D&B Hoovers and Dow Jones Factiva that flag deliveries, backlogs, and price shifts. The sources listed are illustrative; many additional publications inform the workbook.

Market-Sizing & Forecasting

A top-down rebuild converts heavy-lift flight hours, construction outlays, wildfire acreage, offshore wind installations, and defense modernization budgets into potential demand, which is then priced with primary-validated average sales prices. Selective bottom-up checks, OEM delivery roll-ups, and sampled lease rates fine-tune totals. A multivariate regression with ARIMA error correction projects each driver, while scenario analysis captures commodity-price swings. Gaps in delivery disclosure are bridged with rolling three-year utilization factors agreed upon with operators.

Data Validation & Update Cycle

Outputs face three-layer analyst review; outlier thresholds trigger immediate source rechecks, and values are benchmarked against independent safety-registry fleet counts. Reports refresh each year, with interim updates after material events such as program delays or major wildfire seasons.

Why Mordor's Air Crane Helicopter Market Baseline Commands Reliability

Published figures often diverge because providers choose alternative payload cut-offs, fold in retrofit revenues, or apply uniform ASP growth curves; our disciplined scope and annual refresh cadence minimize such drift.

Differences fade once scopes, drivers, and refresh schedules are normalized, leaving Mordor's mid-range estimate as the most balanced and transparently traceable baseline for strategic planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.34 B (2025) | Mordor Intelligence | |

| USD 6.62 B (2025) | Global Consultancy A | Bundles light utility lifts and assumes constant ASP escalation |

| USD 5.30 B (2024) | Industry Consultancy B | Omits government firefighting procurements and freezes defense outlook |

| USD 5.55 B (2023) | Research Firm C | Relies solely on OEM deliveries, excludes aftermarket conversions |

Differences fade once scopes, drivers, and refresh schedules are normalized, leaving Mordor's mid-range estimate as the most balanced and transparently traceable baseline for strategic planning.

Key Questions Answered in the Report

What is the current value of the air crane helicopter market?

The air crane helicopter market size is USD 6.84 billion in 2026, climbing to USD 9.99 billion by 2031 at an 7.88% CAGR.

Which region leads the air crane helicopter market?

Asia-Pacific holds the largest regional share at 43.12% in 2025, driven by massive defense procurement and remote-area infrastructure projects.

What segment is growing fastest in load capacity?

Helicopters rated between 12,001 to 15,000 lbs are forecasted to expand at a 9.78% CAGR thanks to infrastructure megaprojects and military logistics needs.

Why are wildfire suppression contracts important to market growth?

Extended fire seasons have prompted multi-year, high-value contracts such as Coulson Aviation’s USD 400 million deal with New South Wales, boosting fleet utilization and new acquisitions.

How is technology shaping future competition?

Hybrid-electric propulsion demonstrations by Sikorsky and GE Aerospace indicate a shift toward lower-emission, fuel-efficient platforms that could reduce operating costs and regulatory exposure.

What challenges threaten near-term expansion?

Volatile jet-fuel prices and acute shortages of certified heavy-lift pilots and engineers can squeeze margins and delay service availability despite strong underlying demand.

Page last updated on: