Airborne ISR Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

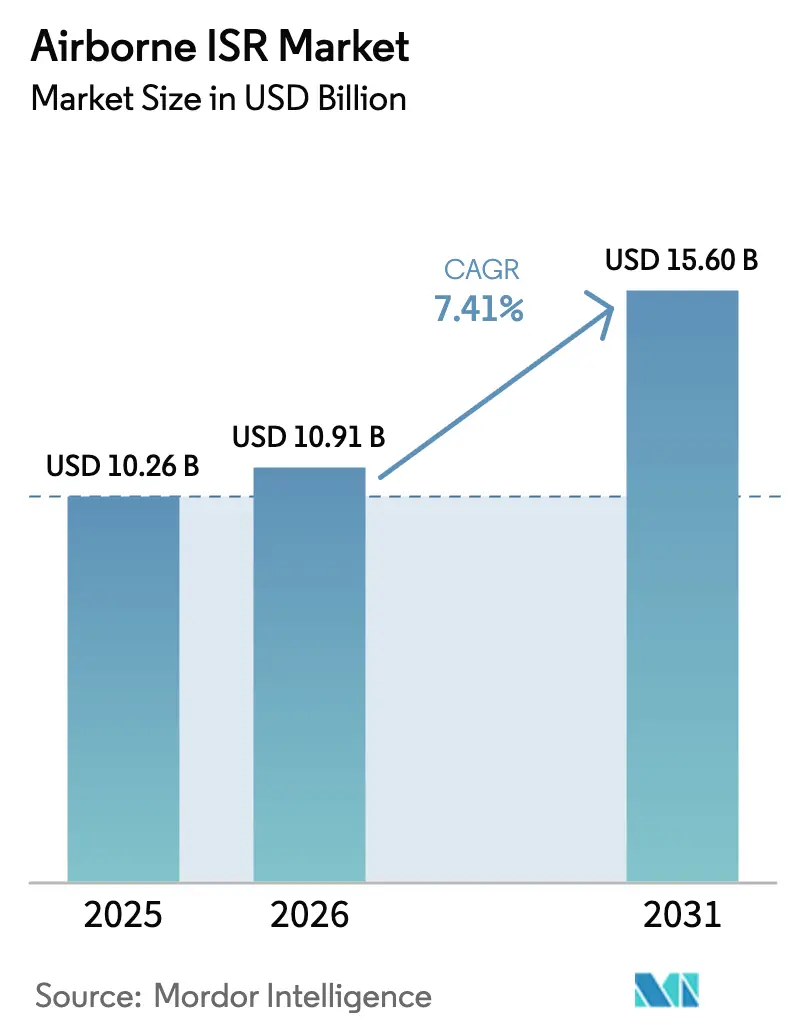

| Market Size (2026) | USD 10.91 Billion |

| Market Size (2031) | USD 15.60 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airborne ISR Market Analysis by Mordor Intelligence

The airborne ISR market size is expected to grow from USD 10.26 billion in 2025 to USD 10.91 billion in 2026 and is forecasted to reach USD 15.60 billion by 2031 at a 7.41% CAGR over 2026-2031. Rising geopolitical flashpoints, the US Department of Defense's (DoD's) Replicator push for 1,000 attritable drones, and mandatory adoption of open-architecture standards such as SOSA and CMOSS are reshaping platform procurement, shortening upgrade cycles, and unlocking multi-supplier competition.[1]Source: Colin Demarest, “DoD Announces Replicator Initiative,” defense.gov Simultaneously, AI-enabled processing, exploitation, and dissemination now deliver actionable intelligence in under five minutes, opening recurring software revenue pools that supplement sensor and airframe sales. Affordable uncrewed aircraft priced under USD 5 million create fresh addressable demand across homeland security, disaster response, and commercial verticals without cannibalizing large manned fleets. However, sensor-grade semiconductor shortages, spectrum congestion, and new zero-trust cybersecurity mandates elevate cost and schedule risk for prime contractors. At the same time, smaller integrators exploit commercial-off-the-shelf (COTS) payloads to bypass export bottlenecks and undercut incumbents.

Key Report Takeaways

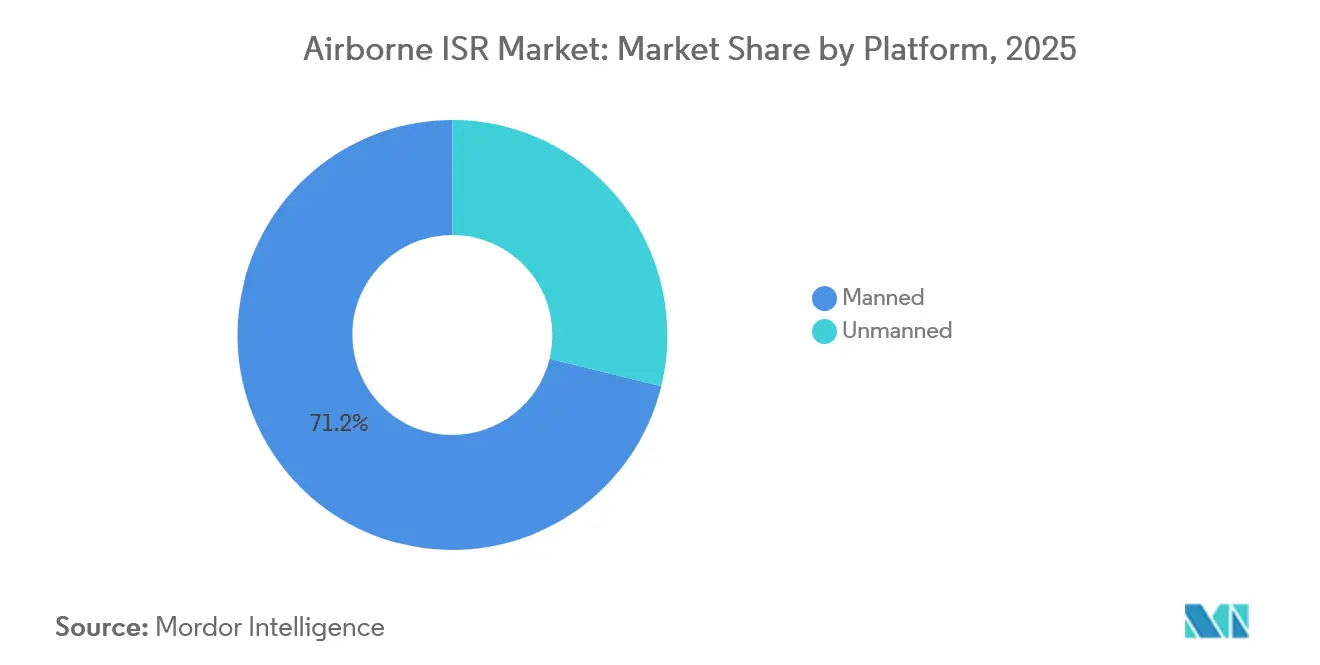

- By platform type, manned aircraft led the airborne ISR market, accounting for 71.17% of the market share in 2025; unmanned systems are projected to advance at a 10.45% CAGR through 2031.

- By application, warfare missions accounted for 41.80% of revenue in 2025 and are projected to grow at a 7.75% CAGR through 2031.

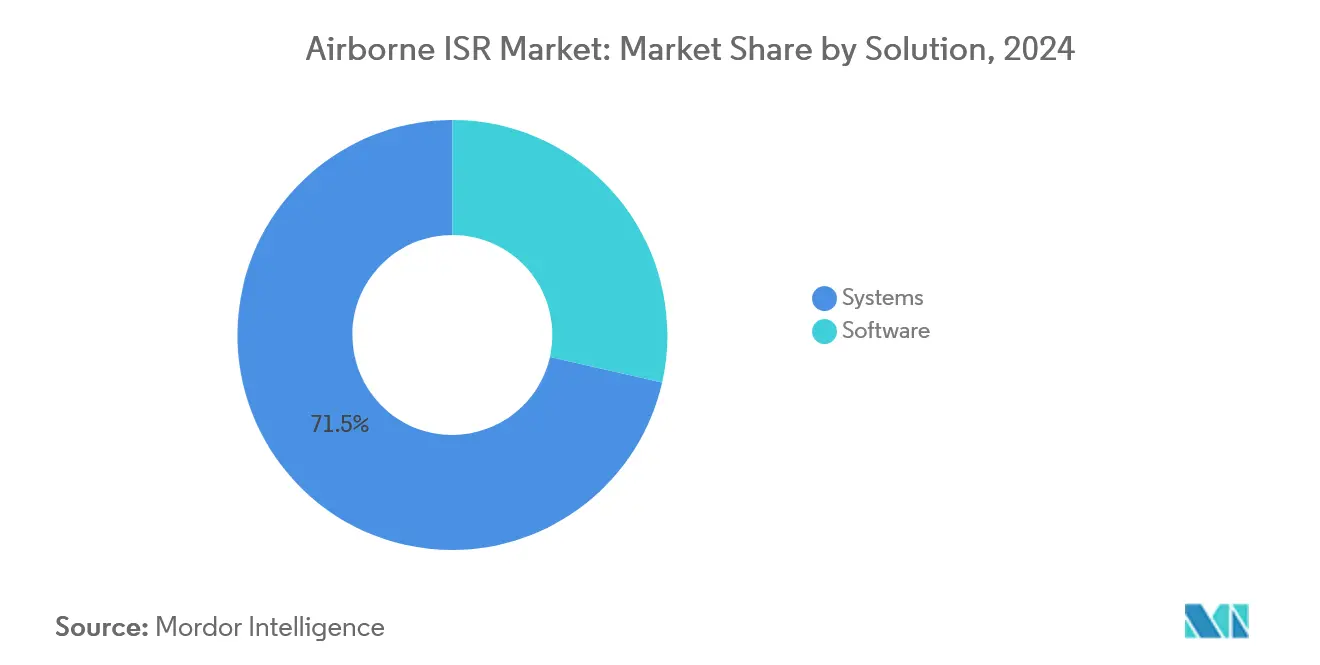

- By solution, hardware-centric systems commanded 71.45% of the airborne ISR market size in 2025, while software is forecast to expand at an 8.50% CAGR between 2026 and 2031.

- By end user, defense organizations accounted for 66.28% of the 2025 revenue and are expected to rise at a 7.64% CAGR through 2031.

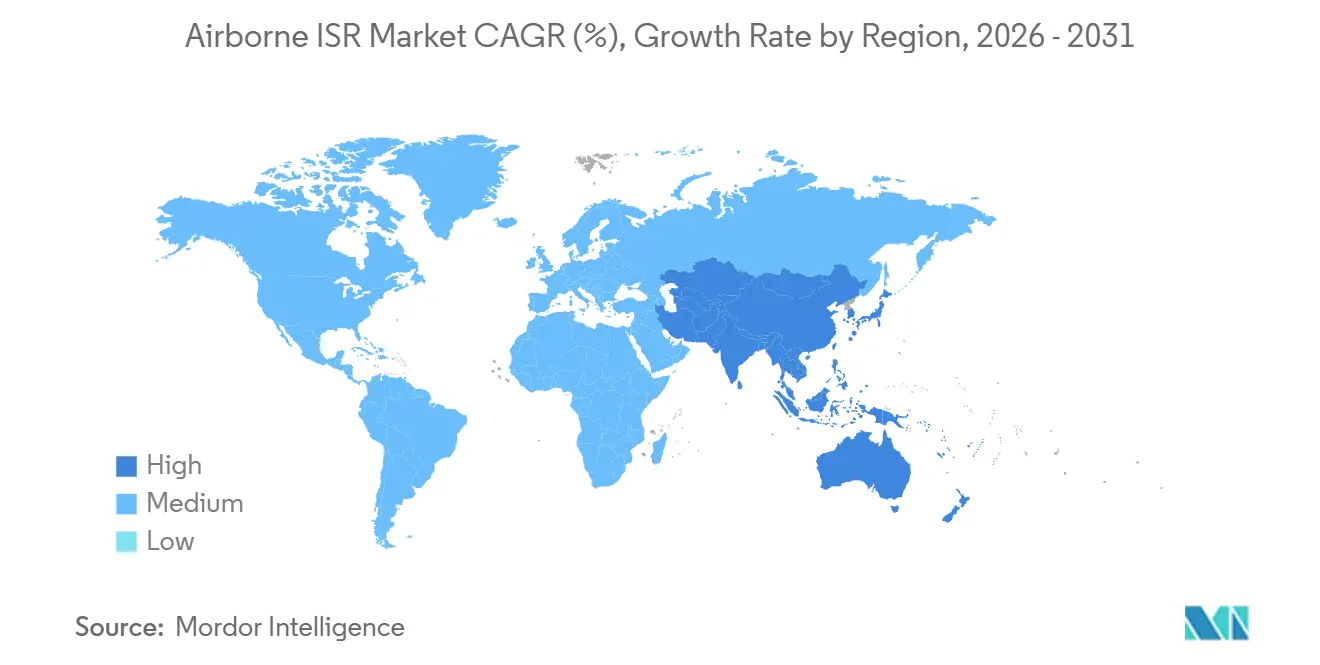

- By geography, North America held a 34.20% share in 2025, whereas the Asia-Pacific is projected to have the fastest CAGR of 7.87% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Airborne ISR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating shift to multi-INT sensor fusion on open-architecture pods | +1.2% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| AI-enabled PED reducing tip-to-product cycle below 5 minutes | +1.5% | North America, Europe, advanced Asia-Pacific markets | Short term (≤ 2 years) |

| DoD Replicator program spurring demand for attritable ISR drones | +1.0% | North America with spill-over to allied nations | Short term (≤ 2 years) |

| Geopolitical flash-points fueling 8-year ISR recapitalization boom | +1.8% | Indo-Pacific, Middle East, Eastern Europe | Long term (≥ 4 years) |

| Commercial-satellite data licensing lowering entry barriers for SMEs | +0.7% | Global, especially North America and Europe | Medium term (2-4 years) |

| Defense-cloud zero-trust mandates driving airborne edge-compute retrofits | +0.9% | North America, Europe, advanced Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift to Multi-INT Sensor Fusion on Open-Architecture Pods

Open-architecture pods that blend EO/IR, SAR, SIGINT, and ELINT streams on a single pylon are displacing monolithic mission systems. L3Harris’s SOSA-certified AgilePod, a 450-pound unit that has now exceeded 10,000 flight hours on F-16 and MQ-9 platforms, enables operators to swap sensor loads in under four hours, eliminating weeks-long depot cycles.[2]Source: L3Harris, “AgilePod Achieves 10,000 Flight Hours,” l3harris.com The US Air Force’s Open Mission Systems mandate requires all new airborne ISR market entrants to comply by fiscal 2027, nudging export buyers to follow suit. Smaller nations thus field multi-INT capability without procuring purpose-built SIGINT aircraft, broadening the airborne ISR market’s customer base. Modular pods also drive after-sales revenue, as each new sensor cartridge ships with its own software license.

AI-Enabled PED Reducing Tip-to-Product Cycle Below Five Minutes

Machine-learning models now auto-cue targets, classify vehicles, and prioritize frames, collapsing the PED chain from hours to minutes. Project Maven processes full-motion video at 30 frames per second and flags anomalies with 92% accuracy, enabling strike cells to act before adversaries relocate. Northrop Grumman’s AI-PED suite trimmed analyst workload by 60% during 2025 Indo-Pacific drills on the RQ-4 Global Hawk, raising mission tempo without additional personnel. These gains justify premium software subscriptions, reinforce platform relevance against space-based substitutes, and underpin a 1.5 percentage-point CAGR uplift across the airborne ISR market.

DoD Replicator Program Spurring Demand for Attritable ISR Drones

The Pentagon’s Replicator initiative aims to develop 1,000 attritable autonomous systems by August 2025, with approximately 40% of these systems carrying ISR payloads. Unit acquisition costs of USD 2-5 million democratize persistent surveillance for second-tier militaries and homeland security agencies. General Atomics has already delivered 120 MQ-9B SkyGuardian aircraft under the program, each equipped with expendable sensor pods that detach before the airframe is lost, reinforcing a “mass over exquisite” procurement mindset. This paradigm adds 1.0% CAGR headroom to the airborne ISR market as buyers supplement high-value manned fleets with disposable drones.

Geopolitical Flash-Points Fueling an Eight-Year ISR Recapitalization Boom

Escalating tensions in the South China Sea, Ukraine, and the Middle East are catalyzing an eight-year cycle of fleet replacement. The US Navy plans to grow the P-8A Poseidon inventory from 128 aircraft in 2024 to 156 by 2030, while India and Japan collectively earmarked over USD 5.6 billion for P-8I and E-2D purchases in 2024-2025.[3]Source: Naval News, “P-8A Poseidon ASW Upgrades,” navalnews.com These programs stabilize order books for primes and lift the airborne ISR market trajectory by 1.8 percentage points through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RF spectrum congestion and ITAR constraints delaying export clearances | -0.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Sensor-grade semiconductor shortages lengthening lead-times more than 24 months | -1.2% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| High-altitude balloons and LEO satellites emerging as lower-cost substitutes | -0.6% | Global, early adoption in Asia-Pacific and commercial sectors | Long term (≥ 4 years) |

| Cyber-hardening mandates adding 12-15% to sustainment budgets | -0.9% | North America, Europe, advanced Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

RF Spectrum Congestion and ITAR Constraints Delaying Export Clearances

The FCC’s 2024 C-band auction carved 100 MHz from DoD allocations, forcing ISR datalinks to hop frequencies or accept degraded throughput. Concurrently, ITAR classifies advanced EO/IR sensors and AI-PED software as defense articles, stretching export reviews to as long as 24 months for otherwise close allies. L3Harris disclosed that such delays postponed USD 180 million in international ISR contracts during 2024, driving it to develop downgraded export variants. The result is a 0.8 percentage-point drag on the medium-term growth of the airborne ISR market.

Sensor-Grade Semiconductor Shortages Lengthening Lead-Times Beyond 24 Months

Limited GaN foundry capacity and export controls on lithography tools are extending lead times for AESA radar amplifiers and InGaAs focal plane arrays by more than 2 years. Raytheon cited these shortages as the reason for missing delivery schedules for 40 AN/APG-82 radars in Q3 2024, which, in turn, led to delays in the delivery of ISR pods. New CHIPS-Act-funded fabs will not reach volume until 2027, leaving integrators to ration sensor allocations or accept capability trade-offs, such as Northrop Grumman’s decision to qualify a commercial detector with 10% lower sensitivity for the RQ-4 turret. This shortage subtracts 1.2 percentage points from forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Manned Dominance, Unmanned Acceleration

Manned aircraft maintained 71.17% of airborne ISR revenue in 2025, demonstrating that traditional crewed fleets continue to dominate budgets even as new technologies emerge. The cornerstone platforms are the P-8A Poseidon maritime patrol aircraft and the E-7 Wedgetail airborne early warning jet, both of which have confirmed procurement lines extending into the 2030s. Each airframe carries payloads exceeding 20,000 pounds and can remain on station for well above ten hours, enabling comprehensive anti-submarine sweeps and real-time analysis by onboard mission crews. Because both designs share commercial B737 structures, international operators benefit from global parts inventories and established maintenance networks, locking in multi-year logistics contracts that deliver predictable annual profit streams.

Unmanned systems are projected to post a robust 10.45% CAGR through 2031, gradually reducing the proportional dominance of crewed platforms while pushing total units delivered to new highs. The MQ-9B SkyGuardian exemplifies this trend; priced at roughly one-quarter of a P-8A, it offers 30-hour endurance, satellite-tolerant datalinks, and plug-and-play multi-INT pods compatible with the Replicator initiative’s requirement for rapid, low-cost mass production. Parallel Collaborative Combat Aircraft prototypes will act as autonomous wingmen, funneling sensor data directly into the Joint All-Domain Command and Control network to bypass contested air defenses.

By Application: Warfare Missions Sustain Leadership

Warfare missions remained the economic backbone of airborne ISR in 2025, bringing in 41.80% of total revenue and charting a forward 7.75% CAGR through 2031. Within this domain, P-8A patrols across the Indo-Pacific routinely drop about 400 sonobuoys per sortie, while Northrop Grumman’s ALQ-257 pod determines hostile-emitter coordinates in two seconds. High-tempo, sensor-intensive sorties guarantee a steady refresh cycle for radars, processors, and edge-compute hardware. Although traditional overland and maritime surveillance remains the second-largest application, civil uses such as wildfire mapping and search-and-rescue are currently the fastest-growing niches as governments dedicate climate-resilience funding to persistent aerial sensing operations.

The warfare slice is reinforcing its primacy, even amid proliferating low-Earth-orbit (LEO) constellations that challenge traditional surveillance roles. In contrast, applications dominated by routine border observation or economic-zone patrols are growing more slowly, reflecting budget competition from orbital sensors and shifting procurement priorities inside many defense ministries. The divergence highlights a strategic spending pattern: stakeholders allocate premium budgets to mission sets that directly support strike effectiveness, submarine deterrence, and electromagnetic maneuver warfare, while delegating broad-area awareness to less expensive space-based or commercial data services for routine security requirements.

By Solution: Hardware Heavy, Software Surging

Hardware sales continue to anchor airborne ISR economics, with integrated systems, including airframes, sensors, datalinks, and ground stations, accounting for 71.45% of the 2025 turnover. The segment’s resilience stems from the high entry costs of active electronically scanned array (AESA) radars, high-definition electro-optical turrets, and long-endurance airframes, which require multi-year budgeting and extensive industrial infrastructure. Raytheon and similar vendors lock in predictable upgrade revenue by releasing incremental improvements in range, resolution, and electronic-protection features that trigger follow-on procurement. Governments favor contracting structures that pair initial acquisition with performance-based logistics, thereby extending hardware cash flows over a decade or more. Consequently, the capital-intensive nature of ISR platforms shields the systems sub-market from spending shocks or austerity cycles during down-cycle budget negotiations.

Software is accelerating fastest, registering an 8.50% CAGR that outpaces every hardware category. Palantir’s USD 480 million Maven Smart System award illustrates the trajectory, enabling automated target recognition, natural-language query of sensor databases, and continuous algorithm updates delivered through secure cloud repositories. Subscription licensing converts historically cyclical modernization budgets into annual operating expenditures, a structural shift welcomed by treasury departments seeking smoother cash profiles. Complementing new code, Lockheed Martin’s edge-compute kits for legacy U-2 aircraft perform real-time video analytics on board, lowering satellite bandwidth costs while implementing mandatory zero-trust cybersecurity.

By End User: Defense Core, Homeland Security Rising

Defense ministries remained the dominant customer block, securing 66.28% of airborne ISR turnover in 2025 and earmarking growth to 2031 despite fiscal pressure. The US DoD alone budgeted USD 12.3 billion for airborne sensing, covering additional P-8A tails, RQ-4 sustainment, and early development of the Collaborative Combat Aircraft. NATO members collectively lifted ISR appropriations by 18%, with newer eastern allies emphasizing unmanned systems to monitor contested borders where Russian activity is persistent. Strategic planners value airborne platforms because they knit together the kill chain when space assets are jammed or destroyed, and because manned crews can adapt tactics in dynamic engagements, reinforcing defense’s central spending priority for the next budget planning cycle worldwide.

Homeland security and civil agencies, though smaller, now account for 22% of sector revenue and are climbing steadily. US Customs and Border Protection is expanding its MQ-9 fleet to 18 airframes, and the Coast Guard signed a USD 280 million deal for SeaGuardian drones equipped with maritime-search radars tailored to intercept illegal fishing and drug trafficking. State emergency departments are also procuring twin-turboprop ISR aircraft equipped with infrared line-scan sensors, which deliver real-time wildfire perimeter maps, enabling faster evacuation orders and more efficient resource allocation. These application cases demonstrate how governments outside the defense sphere are adopting military-grade situational awareness tools to protect populations, infrastructure, and economic resources under tightening disaster-response timelines worldwide.

Geography Analysis

North America contributed 34.20% of the 2025 airborne ISR revenue, primarily driven by the United States, which plans to operate 156 P-8A Poseidons by 2030 and has awarded USD 1.5 billion for the development of the Collaborative Combat Aircraft. Canada added 16 Poseidons to replace its CP-140 Aurora patrol planes, while Mexico converted additional King Air 350ERs into ISR (Intelligence, Surveillance, and Reconnaissance) roles to support counternarcotics patrols along the shared border. The regional focus remains on anti-submarine surveillance across the Arctic and Pacific gateways, as well as constant monitoring of drug-trafficking corridors. Extensive industrial bases in Washington, California, and Quebec supply avionics, mission software, and depot maintenance, ensuring that North America retains technological leadership and large sustainment budgets throughout the forecast period.

In Europe, the United Kingdom is phasing in E-7 Wedgetail aircraft to replace aging E-3D Sentry platforms, while Germany has ordered five P-8A Poseidons to retire its veteran P-3C Orion fleet. France is advancing the tri-national Future Combat Air System, integrating stealth fighters with loyal-wingman drones that will share sensor data across secure clouds. Poland, Romania, and the Baltic states continue procuring MQ-9B SkyGuardian systems to monitor Russian troop concentrations, demonstrating alignment between eastern and western members on airborne threat detection. This mix of high-end manned assets and adaptable drones consolidates Europe’s medium-term growth trajectory for ISR modernization.

Asia-Pacific posts the highest CAGR of 7.87%, reflecting mounting maritime disputes and rapid force modernization. India’s USD 3.5 billion order for six additional P-8I aircraft will enlarge its fleet to 18 for Indian Ocean patrols. At the same time, Japan has allocated USD 2.1 billion to field E-2D Hawkeye and RQ-4 Global Hawk platforms that shadow Chinese carrier strike groups. Australia is introducing MQ-4C Triton drones to ensure persistent coverage of northern sea lanes, and South Korea is procuring high-altitude unmanned systems to monitor missile sites. Nascent operators, such as those in the Philippines, are exploring medium-altitude UAVs for exclusive economic zone surveillance, driving regional market growth.

Regulatory Landscape

Airborne ISR procurement and deployment is being shaped by tighter security-of-supply and export-control frameworks, alongside maturing unmanned-airworthiness rules. In the United States, the FAR Council prohibition on contractors using federal funds for FASC-prohibited unmanned aircraft systems (effective December 2025) is pushing program offices and primes to re-qualify compliant air vehicles, datalinks, and subcomponents, with direct implications for ISR UAV sourcing and sustainment.

In Europe, implementation of the certified UAS continuing-airworthiness framework advanced with Commission Delegated Regulation (EU) 2024/1107 (Annex II, Part-CAO.UAS enforcement starting February 2026) and Implementing Regulation (EU) 2024/1109 (applying from May 2025), adding compliance overhead for certified unmanned ISR fleets and their maintenance organizations. Export controls remain a parallel constraint and enabler: the Council of the European Union adopted the updated Common Military List in February 2026, while the US BIS issued an interim final rule in January 2026 easing export controls for certain civil UAV categories to partner nations. This effectively bifurcates pathways for civil versus defense-configured ISR platforms and payloads.

Value Chain Analysis

The airborne ISR value chain covers missionized airframes (manned and unmanned), sensors and payloads (EO/IR, AESA radar, SIGINT/ELINT), onboard and edge compute, datalinks and SATCOM, ground stations, and software for processing, exploitation, and dissemination (PED). Prime contractors such as Boeing, Northrop Grumman, and Lockheed Martin typically orchestrate platform integration and certification. Specialized subcontractors supply radars, turrets, EW/ESM subsystems, embedded computing, and cybersecurity hardening. Open-architecture initiatives, including the FACE Consortium and US DoD open mission systems approaches cited in the report context, increase software portability and enable multi-supplier upgrades, widening the role of software vendors and subsystem integrators across retrofit and new-build programs.

Upstream bottlenecks remain tied to defense electronics, where GaN and sensor-grade components can extend lead times beyond 24 months, cascading into pod and platform delivery schedules. Downstream, service-led models and mission operations require additional infrastructure and workforce readiness. The US Army HADES push (intent to procure up to 11 Bombardier Global 6500-based ISR jets announced in January 2026, plus a July 2026 decision to relocate the 116th Military Intelligence Brigade to Texas to support HADES starting in FY2027) illustrates how business-jet ISR adds hangar, depot, and operational-support nodes alongside traditional defense aviation sustainment.

Competitive Landscape

The airborne ISR market is semi-consolidated, characterized by a few players each developing platforms and subsystems for various armed forces. Key players in the market include Airbus SE, Northrop Grumman Corporation, Leidos Holdings, Inc., Leonardo S.p.A., and Thales Group. Vertical integration grants these companies leverage across airframes, sensors, mission software, and lifecycle support, allowing them to offer turnkey packages that lock in customers for decades. Northrop Grumman’s AI-powered PED suite, which has been demonstrated to cut analyst workload by 60%, provides an added differentiator. Meanwhile, Boeing’s global B737 support network underwrites competitive operating costs for the P-8A. Together, their scale, political influence, and access to classified programs keep procurement pipelines robust despite tightening defense budgets in many allied markets.

Disruptive challengers, including General Atomics, AEVEX Aerospace, and Metrea, target price-sensitive or schedule-driven buyers by adapting commercial airframes and leveraging COTS sensors. General Atomics combines low acquisition cost with partnerships that stream commercial satellite imagery into the MQ-9 mission system, removing the need for government-owned ground infrastructure. AEVEX delivers modified King Air 350 platforms within 18 months, satisfying USSOCOM requirements that legacy primes could not meet on time, and Metrea offers fractional-ownership ISR flight hours to customers wishing to avoid capital purchases. Collectively, these firms expand market access, promote pay-by-the-hour contracting models, and encourage incumbents to adopt open-architecture payloads, rapid software updates, and diversified semiconductor supply chains for enhanced delivery and resilience.

Recent strategic actions underscore competitive dynamics. In January 2025, Lockheed Martin installed a 40-pound edge-compute module on the U-2, enabling airborne AI inference and zero-trust cybersecurity compliance without reducing mission endurance. Boeing renegotiated its P-8A sustainment agreement in late 2024, raising contract value to fund encrypted datalink upgrades and mandatory CMMC audits. Northrop Grumman mitigated chip shortages by qualifying commercial InGaAs detectors for the RQ-4’s EO/IR turret, accepting a minor sensitivity penalty to maintain delivery schedules. These moves reveal how primes invest in software, cybersecurity, and supply-chain flexibility to protect backlog, comply with new regulations, and preserve performance credibility amid component scarcity during an increasingly constrained global market.

Airborne ISR Industry Leaders

Northrop Grumman Corporation

Airbus SE

Leonardo S.p.A.

Leidos Holdings, Inc.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A white-space is forming around faster-to-field deep-sensing aircraft and their supporting mission systems, especially when programs replace legacy turboprop ISR fleets with higher-altitude, higher-speed business-jet platforms. The US Army HADES and broader Multi-Domain Sensing System (MDSS) family provide a demand signal: the first fully developed HADES prototype aircraft based on a modified Bombardier Global 6500 is scheduled for delivery in fiscal year 2026, and technical requirements call for operations between 41,000 and 51,000 feet with a minimum 14,000-pound payload and 12 hours unrefueled endurance. This creates near-term openings for radar/EO-IR payload integrators, airborne edge-compute suppliers, and datalink providers that can meet size, weight, and power constraints while supporting standoff collection and rapid dissemination.

Interoperability and real-time sensor-to-shooter data flows are also expanding the addressable upgrade market across existing fleets. The US Army reported an end-to-end data flow going live after the August 2024 JITC re-certification of an improved Interoperability Data Message component under the TROJAN program, which indicates continued investment in making airborne ISR outputs usable across joint networks. Sustainment and spiral modernization remain another monetization path: Raytheon’s $512.2 million US Army award in December 2025 to support aerial ISR through 2036 points to multi-year demand for sensor development and maintenance, favoring suppliers that combine hardware refresh, software updates, and cybersecurity compliance under long-duration support structures.

Recent Industry Developments

- July 2026: Denmark, Finland, Germany, and Norway signed a letter of intent under NATO to procure up to five Northrop Grumman MQ-4C Triton uncrewed ISR aircraft. The procurement increases HALE uncrewed surveillance capacity among European allies and reinforces interoperability-driven demand for long-endurance ISR platforms and associated ground and data-processing ecosystems.

- February 2025: Airbus signed a study contract with the French DGA to define Frances future maritime patrol aircraft, based on an A321 MPA concept intended to replace Atlantique 2 aircraft in the 2030-2040 timeframe. The study supports a new fixed-wing MPA/ISR pipeline and indicates continued interest in using commercial-derivative airframes for ISR roles with mission-system integration opportunities.

- December 2024: The US Navy awarded Northrop Grumman a $3.5 billion contract to develop the E-130J, the successor to the E-6B Mercury for airborne command and control. The program underpins demand for resilient airborne mission systems and communications payloads, adjacent to ISR architectures that require secure connectivity and rapid dissemination across contested environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the airborne ISR market is the revenue generated from airborne platforms and onboard mission systems that collect, process, and share intelligence, surveillance, and reconnaissance data for defense, security, and selected civil missions.

Scope exclusions: We exclude purely space-based ISR assets and ground-only ISR networks unless they are sold as part of an airborne ISR solution.

Segmentation Overview

- By Platform Type

- Manned

- Unmanned

- By Application

- Overland/Maritime Survelliance

- Border Patrol

- ISTAR Operations

- Exclusive Economic Zone (EEZ)

- Warfare Mission

- Anti-Submarine Warfare (ASW) and Anti-Surface Warfare (ASuW)

- Air to Ground Support (AGS)

- Electronic Warfare

- Critical Infrastructure Monitoring

- Environmental Monitoring

- Pollution Monitoring

- Disaster Relief

- Search and Rescue (SAR)

- Maritime SAR

- Land SAR

- Overland/Maritime Survelliance

- By Solution

- Systems

- Software

- By End User

- Defense

- Homeland Security

- Commercial and Civil

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Israel

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with mapping what typically gets budgeted and procured under airborne ISR, then aligning those categories with measurable demand signals. We relied on public defense budget documents, procurement releases, and fleet modernization notes to understand what is being funded and when upgrades tend to occur.

To keep assumptions consistent, we used public and official sources such as defense ministry publications, US DoD budget justification books, NATO and allied capability roadmaps, aviation regulators and registries for aircraft counts, and trade and customs statistics where available for major platform and sensor categories. We also reviewed company annual reports, investor presentations, press releases, and reputable defense press for program timing and delivery milestones, then cross-checked select figures using paid subscriptions for company financials, contract tracking, and patent databases to confirm technology direction and pricing ranges. These sources are illustrative only, and many other public references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews focused on confirming what portion of platform spend is attributed to ISR missionization, and how upgrade cycles shift spending between new procurement and retrofit. We spoke with stakeholders across operators, integrators, and subsystem specialists, and we used regional coverage to confirm differences in mission mix, delivery schedules, and sustainment intensity.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 49% |

| Mid tier: 49% | Functional/Unit leaders: 36% | EMEA: 33% |

| Smaller Players: 15% | Managers: 52% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where defense and security spend, fleet and sortie intensity, and mission system upgrade cycles were used to reconstruct the addressable airborne ISR demand pool by region. Once that anchor was set, we corroborated totals with selective bottom-up checks, such as sample program roll-ups, platform deliveries and retrofit counts, and typical mission-system ASP bands multiplied by expected volumes.

Key inputs that shaped the model included manned versus unmanned fleet additions, sensor mix shifts (EO/IR, radar, SIGINT), retrofit share versus new-build missionization, sustainment and training intensity tied to operational tempo, and delivery timing of major programs. Where direct volume visibility was limited, gaps were handled through proxy indicators such as aircraft inventory trends, procurement lot sizes, and recurring upgrade intervals that were validated through expert feedback.

Forecasting used scenario analysis supported by trend-based smoothing, since budgets, procurement timing, and delivery slippages can move year-to-year results in a lumpy way. Assumptions for inflation, FX conversion, and average selling price progression were reviewed with interviewees to keep the forecast realistic under base, conservative, and accelerated modernization cases.

Data Validation & Update Cycle

Outputs were checked against independent signals, including defense budget movement, known contract awards, fleet growth, and stated delivery schedules, before the numbers were finalized. When an outlier appeared, we re-tested the drivers, then ran a second-pass review to remove any double counting between platform, payload, and services.

The report is refreshed annually, and interim updates are triggered when material events occur, including major procurement shifts, large contract wins, or meaningful currency moves. Before delivery, we do a final review pass so the model reflects the latest public data and the newest feedback received during follow-ups.

Mordor Intelligence's Airborne Isr Market Sizing Compared With Other Published Estimates

Published airborne ISR market values can look far apart because the market boundary is not always treated the same way, and because timing choices can change the number even when demand is similar. Differences often come from what gets counted as mission systems versus platform value, and whether services and software are included as recurring revenue.

In a refresh-led build, the spread is usually driven by when exchange rates are applied, how ASPs are stepped up for newer sensor payloads, and whether delayed deliveries are shifted between years. By rechecking contract timing and keeping FX conversion consistent to the stated year, the estimate stays current in fast-moving procurement cycles, which is a practical choice used in the model by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.91 B (2026) | |

| Global Consultancy A | USD 10.65 B (2026) | Uses a different base year and tends to smooth pricing and mix changes across the forecast window, which can mute ASP step-ups tied to newer payload configurations. |

| Regional Consultancy B | USD 7.16 B (2024) | Reported year is earlier and the scope is typically tighter around core systems, with less consistent treatment of software, upgrades, and support, and FX timing may reflect the base-year average rather than updated conversion. |

Overall, the table shows that part of the gap is simply year alignment, and the rest comes from scope and pricing logic. When procurement timing, upgrade cadence, and consistent currency conversion are applied step-by-step, the resulting market size is easier to trace back to observable fleet, program, and budget signals.

Key Questions Answered in the Report

What is the current airborne ISR market size and growth outlook?

The airborne ISR market size is USD 10.91 billion in 2026 and is projected to reach USD 15.60 billion by 2031, reflecting a 7.41% CAGR.

Which platform category leads spending in airborne ISR?

Manned aircraft hold 71.17% revenue share, led by P-8A Poseidon and E-7 Wedgetail fleets.

Which region will grow fastest in airborne ISR through 2031?

Asia-Pacific is forecasted to post the quickest 7.87% CAGR, propelled by Indian, Japanese, and Australian procurements.

How are AI-enabled PED tools changing ISR operations?

AI models now compress processing cycles below five minutes and cut analyst workload by 60%, unlocking recurring software revenue.

What impact do semiconductor shortages have on airborne ISR deliveries?

GaN and InGaAs component shortages extend radar and sensor lead-times past 24 months, delaying platform hand-offs and trimming forecast CAGR by 1.2 points.

Page last updated on: