Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 20.04 Billion |

| Market Size (2031) | USD 29.05 Billion |

| Growth Rate (2026 - 2031) | 7.71% CAGR |

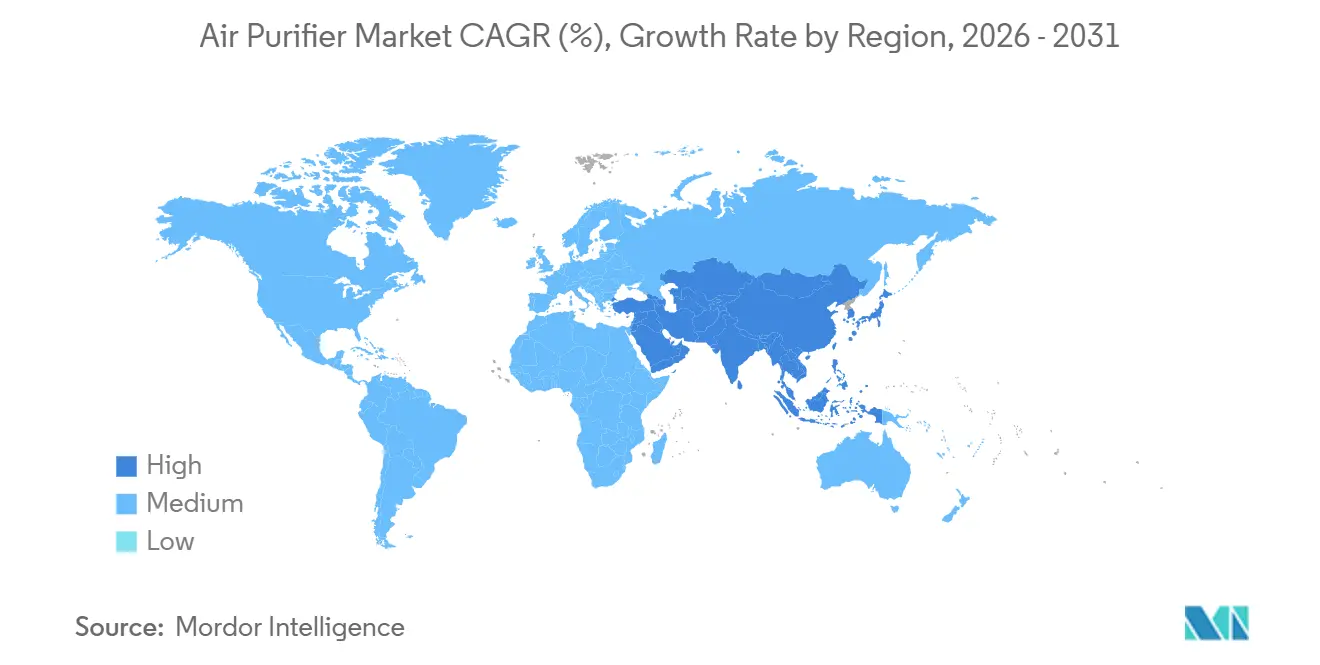

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

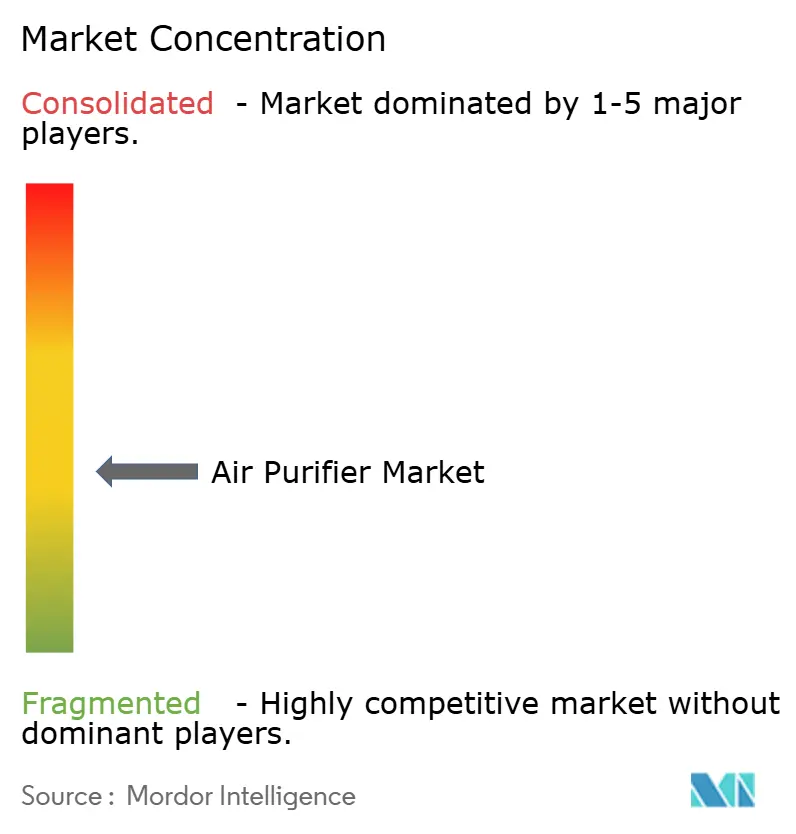

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Purifier Market Analysis by Mordor Intelligence

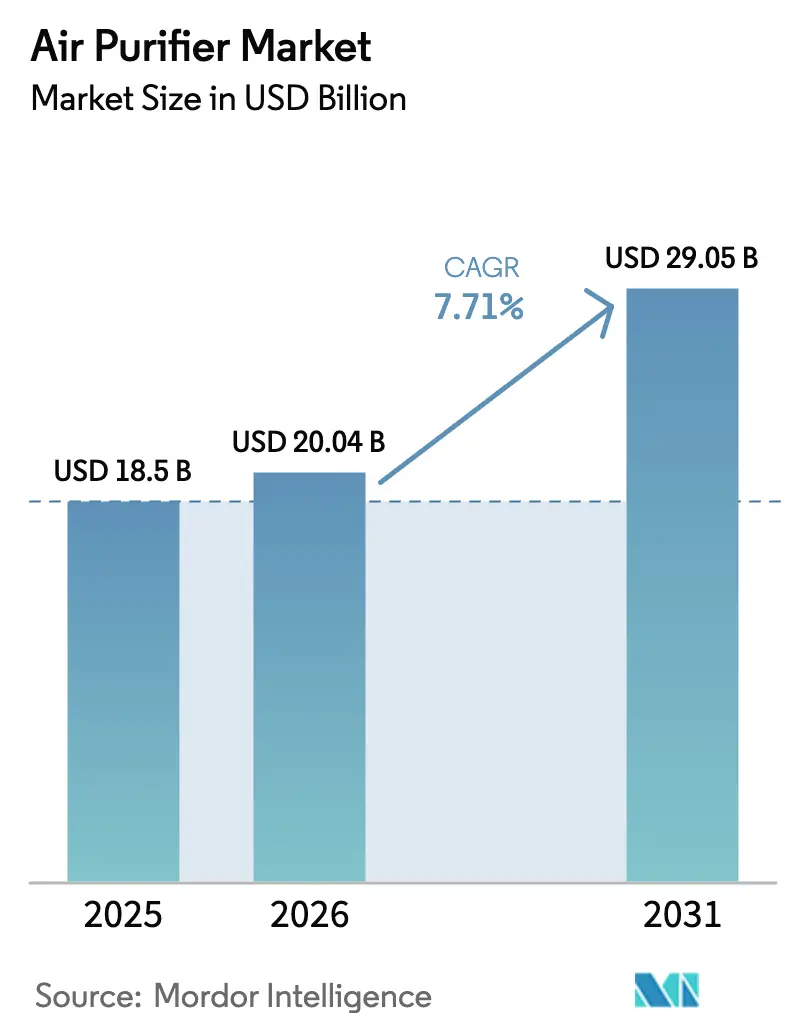

The Air Purifier Market is expected to grow from USD 18.5 billion in 2025 to USD 20.04 billion in 2026 and is forecasted to reach USD 29.05 billion by 2031 at 7.71% CAGR over 2026-2031.

This expansion reflects a structural shift from pandemic-era panic buying toward policy-driven indoor-air-quality mandates that are embedding purification into commercial real-estate retrofits, semiconductor cleanrooms, and connected-home ecosystems. LEED v4.1 requirements for MERV 13 or higher filtration, along with real-time PM2.5 monitoring, are accelerating upgrades in North America. At the same time, the CHIPS and Science Act is channeling USD 52.7 billion into U.S. fab construction, each facility demanding ISO Class 4-6 environments supported by HEPA and ULPA systems.[1]National Institute of Standards and Technology, “CHIPS Act Funding Overview,” nist.gov Asia-Pacific continues to anchor demand as chronic urban pollution, national clean-air programs, and electronics manufacturing hubs sustain high household and institutional adoption, while smart-home connectivity and ESG reporting requirements create premium niches in Europe and the Gulf.

Key Report Takeaways

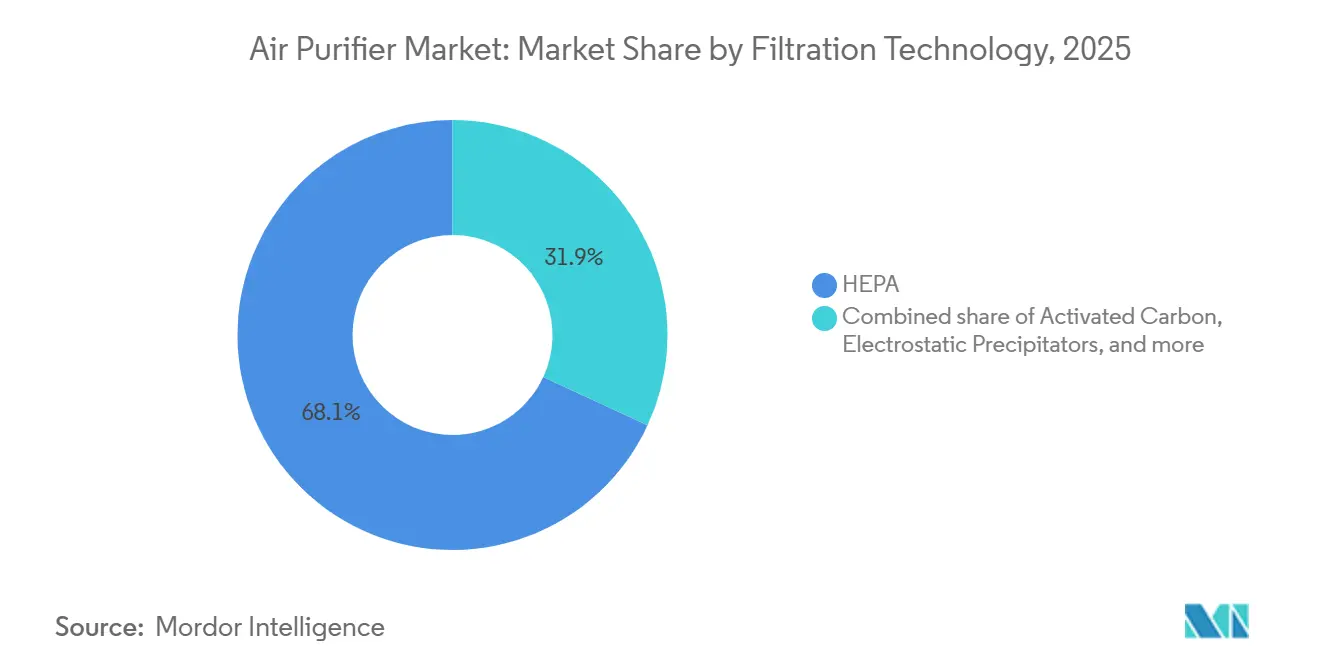

- By filtration technology, HEPA systems led with 68.1% of air purifier market share in 2025; hybrid multi-stage units are forecast to expand at a 9.3% CAGR through 2031.

- By type, stand-alone portable units captured 79.5% of the air purifier market in 2025, whereas in-duct central HVAC solutions are growing at an 8.8% CAGR to 2031.

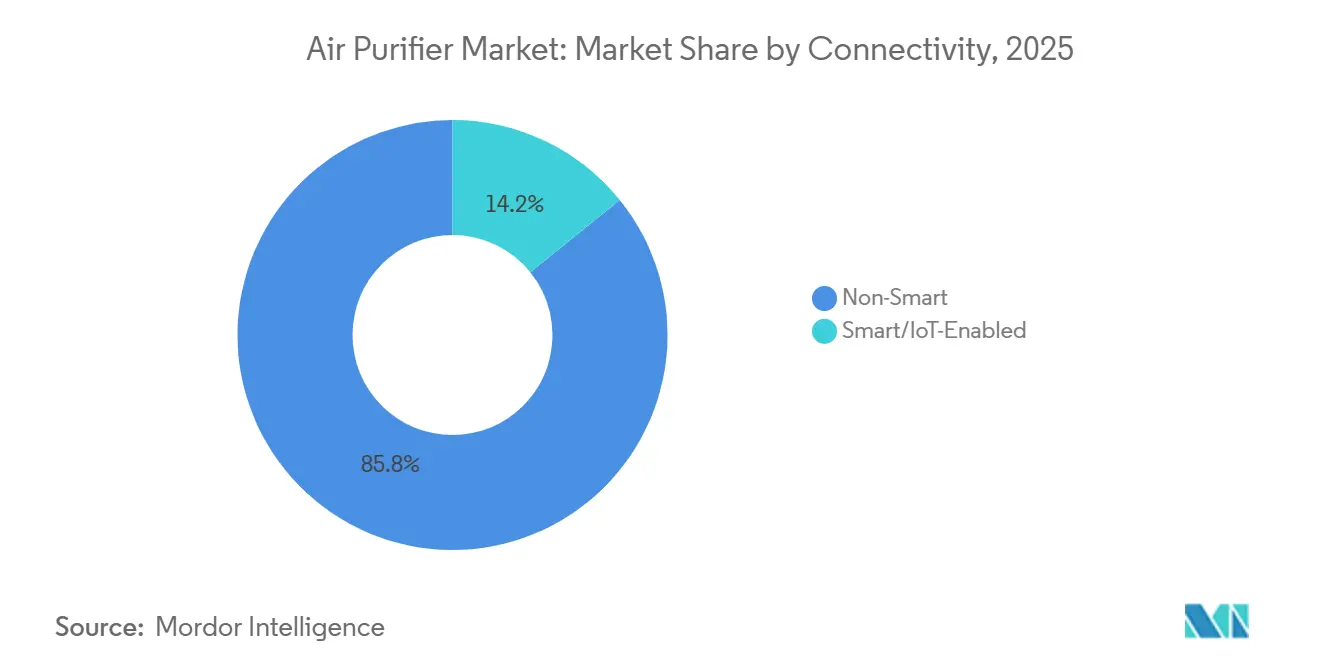

- By connectivity, non-smart analog models dominated with 85.8% volume share in 2025, while IoT-enabled purifiers are rising at an 11.2% CAGR.

- By end user, residential buyers accounted for 61.7% of the air purifier market size in 2025; commercial deployments are advancing at a 9.7% CAGR on ESG and healthy-building mandates.

- By geography, Asia-Pacific held 42.9% revenue share of the air purifier market in 2025, and is also the fastest regulatory-driven growth at 8.5% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Air Purifier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID Health-Centric Device Adoption in East Asian Metros | +1.2% | China, Japan, South Korea, Taiwan | Medium term (2-4 years) |

| Stricter PM2.5 Commercial Real-Estate Standards in North America (LEED v4.1) | +1.5% | United States, Canada | Long term (≥ 4 years) |

| Semiconductor Clean-room Capacity Build-out in the US & South Korea | +0.9% | United States, South Korea, Taiwan | Long term (≥ 4 years) |

| Smart-Home Integration Pull for Connected Purifiers in EU & US | +1.3% | European Union, United States | Medium term (2-4 years) |

| ESG-Driven Hospitality Upgrades across GCC Countries | +0.7% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Indian NCAP Subsidies for HEPA Purifiers in Public Schools | +0.4% | India (102 non-attainment cities) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Health-Centric Device Adoption in East Asian Metros

Persistent PM2.5 readings above national targets in Beijing, Seoul, and Tokyo have normalized year-round purifier ownership, extending the air purifier market beyond the pandemic spike. China’s Ministry of Ecology and Environment confirmed that 38 of 168 monitored cities missed PM2.5 goals in 2024.[2]Ministry of Ecology and Environment, “China Air Quality Report 2024,” mee.gov.cn Japan’s health ministry updated indoor-air guidelines in 2024 to recommend HEPA filtration in childcare and eldercare facilities, institutionalizing a replacement cycle.[3]Ministry of Health, Labour and Welfare, “Indoor Air Quality Guidelines 2024,” mhlw.go.jp Semiconductor engineers in South Korea, exposed to ultra-clean fabs, increasingly mirror workplace standards at home, creating a premium residential cohort. Xiaomi’s RMB 2.5 billion smart-appliance factory opened in Wuhan in 2025, adding 7 million units of annual capacity that can flex between domestic and export orders. This combination of regulatory push and consumer pull solidifies a stable East-Asian demand base.

Stricter PM2.5 Commercial Real-Estate Standards in North America (LEED v4.1)

LEED v4.1’s Indoor Environmental Quality credit mandates MERV 13 or higher filtration and continuous PM2.5 monitoring, compelling U.S. and Canadian building owners to retrofit or specify advanced purification from the design stage. Compliance budgets ranging from USD 50,000 to USD 150,000 for a 100,000-square-foot office are increasingly justified as tenants demand healthy-building certification for talent attraction and ESG reporting. ASHRAE 62.1-2022 further tightens outdoor-air ventilation rates, encouraging hybrid solutions that pair in-duct HEPA modules with portable units in meeting spaces. The Canada Green Building Council noted that 68% of new commercial projects sought LEED certification in 2025, signaling mainstream adoption. These standards are likely to cascade into Europe as revisions to the Energy Performance of Buildings Directive embed indoor-air metrics by 2027.

Semiconductor Cleanroom Capacity Build-out in the US & South Korea

The CHIPS and Science Act directs USD 52.7 billion toward domestic semiconductor manufacturing, with Intel, TSMC, and Samsung allocating more than USD 200 billion to fab construction through 2030. Every ISO Class 4-6 cleanroom cycles air 300-400 times per hour, translating into thousands of HEPA or ULPA modules per site. South Korea mirrors this intensity as SK Hynix and Samsung expand fabs that will add 1.5 million m² of cleanroom space by 2028, each square meter requiring 15-20 HEPA filter modules. Daikin’s USD 163 million R&D lab announced in 2025 targets these industrial niches with next-generation filtration platforms. The technology spillover influences home-purchase decisions among engineers who internalize cleanroom standards, fueling premium residential sales.

Smart-Home Integration Pull for Connected Purifiers in EU & US

Matter protocol adoption by Apple, Google, Samsung, and Amazon is dissolving brand silos and making smart purifiers a seamless node in the connected-home stack. Voice-assistant triggers, real-time dashboards, and predictive filter alerts command a USD 100-USD 200 premium over analog units but resonate with digitally native households. Dyson’s Big+Quiet couples PM2.5 and VOC sensors with automatic speed modulation, achieving up to 30% energy savings compared with fixed-speed models. The European Union’s energy-labeling regulation now requires air cleaners to disclose energy use per cubic meter, further incentivizing sensor-driven optimization. Utility rebates of USD 50-USD 100 for ENERGY STAR-certified smart purifiers in California and New York accelerate payback periods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ozone-Emission Restrictions on Ionizers in California & Japan | -0.8% | California, Japan, South Korea | Short term (≤ 2 years) |

| High Filter Replacement Cost Sensitivity in ASEAN Mass Market | -1.1% | Indonesia, Philippines, Vietnam, Thailand | Medium term (2-4 years) |

| Consumer Skepticism on CADR Claims - Lack of Unified Test Protocol | -0.6% | Global, with acute impact in North America & EU | Medium term (2-4 years) |

| HVAC In-duct Filtration Diluting Stand-alone Unit Demand in Large Offices | -0.5% | North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ozone-Emission Restrictions on Ionizers in California & Japan

California’s Air Resources Board capped ozone output from indoor cleaners at 0.050 ppm in 2024, effectively sidelining ionizer-centric designs.[4]California Air Resources Board, “Indoor Air Cleaner Regulation,” arb.ca.gov Japan’s health ministry imposed parallel labeling rules in 2025 that limit ionizer sales in childcare facilities. Brands dependent on ionization, including Sharp and Panasonic, face USD 15-USD 25 per-unit redesign costs to meet thresholds, crimping margins in entry segments. The rule change funnels demand toward HEPA-pure or hybrid devices, benefiting competitors without ion emitters.

High Filter Replacement Cost Sensitivity in ASEAN Mass Market

HEPA and carbon filters are often priced at 40%-60% of the original unit cost in ASEAN, making ownership expensive relative to per-capita income. With local filter manufacturing still nascent, import duties add up to 30% to landed costs in Vietnam and Thailand. Xiaomi’s washable pre-filters extend service intervals but reduce CADR 15%-20%, reinforcing consumer skepticism over performance claims. Until regional supply chains mature or subscription models proliferate, mass-market penetration remains constrained.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filtration Technology: Hybrid Systems Gain as Contaminant Diversity Widens

HEPA media captured 68.1% of the air purifier market share in 2025, favored for its 99.97% efficiency at 0.3 µm and endorsements from the U.S. EPA and WHO. Hybrid configurations that pair HEPA with activated carbon, UV-C, or photocatalytic oxidation are slated for a 9.3% CAGR because households and businesses now target VOCs, pathogens, and odors in a single chassis. Daikin’s Streamer plasma module showed 99.9% SARS-CoV-2 inactivation in 2024 lab tests. Panasonic’s nanoe X hydroxyl-radical generator is popular in Japan’s eldercare market, where pathogen control ranks with particulate capture. Ionic precipitators retreat to niche industrial uses as ozone-cap rules in California and Japan tighten. Lack of harmonized efficacy standards for hybrid units, however, tempers adoption in risk-averse hospitals and pharmaceutical plants.

Hybrid systems also dovetail with smart-sensor arrays that trigger stage-specific filtration to curb energy draw and extend filter life. LG’s Clean Booster vortex airflow increases CADR 47% over conventional centrifugal fans, enabling similar room coverage with smaller form factors. UV-C and photocatalytic modules remain premium add-ons costing USD 80-USD 120 per unit, limiting penetration below the USD 500 price tier. Prospective regulation around UV-C exposure could further shape the competitive field, but no global consensus exists yet.

By Type: In-Duct Systems Capitalize on Whole-Building IAQ Mandates

Stand-alone devices accounted for 79.5% of the air purifier market volume in 2025 as renters and homeowners favored plug-and-play solutions priced between USD 150 and USD 800. Nevertheless, in-duct installations are scaling at an 8.8% CAGR through 2031, especially within commercial campuses that prefer centralized maintenance. A single in-duct HEPA retrofit costing USD 20,000-USD 40,000 can meet LEED air-change requirements for a 50,000-square-foot office, whereas equivalent coverage with portables would need 50 units and recurring labor for filter swaps. Samsung’s 2025 acquisition of FläktGroup extends its HVAC reach into purification modules that target hospitals and airports. Data-center operators adopt in-duct systems to keep airborne particulates below 10 µg/m³, protecting high-density servers from overheating or shorts. Portable units remain dominant in hospitality and multifamily housing, where room-specific control and aesthetics outweigh operational consolidations.

Regional HVAC penetration shapes these trends: North America and Europe, with about 85% central-HVAC adoption in commercial buildings, naturally migrate to in-duct solutions. By contrast, Asia-Pacific’s heterogeneous building stock sustains portable demand, although new Grade-A offices in Beijing, Seoul, and Singapore are increasingly designed with built-in filtration plenum space. Suppliers that can package both portable and in-duct offerings stand to address the full project life cycle, from break-fix replacements to green-field architectural specs.

By Connectivity: IoT Purifiers Command Premium but Face Interoperability Hurdles

Smart models represented only 14.2% of shipments in 2025 but are on an 11.2% CAGR trajectory as they integrate into broader home-automation platforms. Real-time particulate dashboards, filter-life analytics, and voice-assistant triggers justify a USD 100-USD 200 uplift, with early adopters concentrated in North America and Western Europe. Xiaomi’s Mi Air Purifier 4 Pro, priced at RMB 1,499, secured 18% of China’s smart segment by bundling Wi-Fi and Matter compatibility without premium price drift. The European energy label now requires disclosure of kWh per cubic meter, pushing manufacturers to embed occupancy and pollutant sensors that modulate fan speed, cutting electricity use by up to 30%.

Interoperability, however, remains a pinch point. A 2025 Consumer Technology Association study showed 38% of owners reported set-up or stability issues, dampening repeat intent. Analog devices persist in ASEAN and Latin America, where smartphone penetration lags, and consumers prioritize upfront cost over feature depth. The air purifier market will likely bifurcate: premium brands extend IoT ecosystems, while budget players refine cost-efficient analog units.

By End User: Commercial Segments Outpace Residential on ESG and Regulatory Tailwinds

Residential buyers held 61.7% of the air purifier market size in 2025, yet commercial demand across hospitality, healthcare, education, and corporate offices is rising at a 9.7% CAGR. Marriott aims to retrofit 80% of its Middle-East properties by 2027 to meet LEED and Dubai tourism requirements. U.S. hospitals follow CDC guidance mandating 12 air changes per hour in isolation rooms, driving HEPA upgrades. Indian public schools tap NCAP subsidies, though filter-replacement funding gaps threaten long-term efficacy. Industrial niches, semiconductor fabs, food-processing plants, and data centers offer smaller volumes but high average selling prices owing to mission-critical uptime. Daikin’s new R&D center will develop purifier-HVAC bundles tailored for AI data centers, where particulate contamination can cause costly downtime.

Seasonal volatility affects residential sales during wildfire seasons in California and Australia and during severe pollution episodes in Delhi and Beijing. Conversely, commercial contracts are longer term, often three- to five-year service agreements that bundle consumables and remote monitoring, smoothing revenue streams for vendors.

Geography Analysis

Asia-Pacific generated 42.9% of 2025 revenue for the air purifier market and will climb at an 8.5% CAGR through 2031 on sustained urban PM2.5 levels, aggressive semiconductor investments, and government clean-air programs. China’s environment ministry reported 38 non-attainment cities in 2024, underpinning stable household demand. Xiaomi’s Wuhan factory adds 7 million units of annual output, reinforcing local cost advantages. Japan’s updated childcare IAQ guidelines promote HEPA installations, creating steady replacement cycles.

North America, though smaller in unit volume, exhibits the fastest policy-driven acceleration as LEED v4.1, ASHRAE 62.1, and CHIPS Act funds converge. Semiconductor fabs under construction across Arizona, Texas, and Ohio mandate HEPA/ULPA infrastructure, pulling through significant B2B orders. Canada’s 68% LEED adoption rate for new builds underscores continental alignment with IAQ standards.

Europe’s forthcoming Energy Performance of Buildings Directive revision will formalize indoor-air metrics by 2027, driving uptake in Germany, France, and the Nordics. The Middle East leverages hospitality retrofits under Saudi and Emirati climate pledges, producing double-digit growth, albeit from a small base. South America trails as economic volatility and limited regulatory frameworks hamper widespread adoption, although pollution in São Paulo and Buenos Aires nudges incremental residential sales.

Competitive Landscape

The top five vendors, Daikin, Sharp, Dyson, Philips, and LG, control roughly 35%-40% of global shipments, placing the air purifier market in a moderately fragmented state. Technology differentiation and cost leadership form dual competitive axes. Incumbents bank on proprietary modules (Sharp’s Plasmacluster ionizer, Panasonic’s nanoe X, and Daikin’s Streamer plasma) to justify price premiums, while challengers like Xiaomi deploy vertically integrated factories to offer IoT-equipped units at 40%-50% lower prices.

Samsung’s EUR 1.5 billion purchase of FläktGroup in 2025 marks a pivot toward integrated HVAC-purification platforms aimed at hospitals, airports, and corporate campuses. Daikin’s USD 163 million R&D laboratory will focus on data-center and cleanroom applications, eyeing high-margin industrial niches. Smaller disruptors such as Airdog and Medify Air introduce washable filters and subscription consumables, courting cost-sensitive ASEAN consumers.

Innovation intensity is evident: Dyson filed 127 purification patents in 2024-2025 covering formaldehyde sensing and catalytic destruction. LG’s vortex airflow increased CADR 47%, highlighting aerodynamic advances. Regulatory pressure around ozone emissions forces ionizer-heavy portfolios to redesign, temporarily advantaging HEPA-focused rivals. Lack of unified CADR protocols remains a strategic risk, opening the door for standards-compliant brands to differentiate through certified performance data.

Air Purifier Industry Leaders

Daikin Industries Ltd

Dyson Ltd

Sharp Corporation

Koninklijke Philips N.V.

LG Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Adsorbi secured EUR 1 million to advance bio-based filter materials that lower end-of-life waste.

- January 2025: Levoit unveiled a pet-specific purifier at CES 2025 featuring motion sensing and targeted odor capture.

- September 2024: Wind Point Partners completed its purchase of Clean Solutions Group, signaling private-equity consolidation momentum.

- April 2024: Daikin invested in Breakthrough Energy Ventures to speed up direct-air-capture and carbon-capture filtration know-how.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global air purifier market as revenue generated from the sale of new, electrically powered devices that actively remove particulate matter, gases, and microbiological contaminants from indoor air through mechanical, electrostatic, or photochemical means. Coverage spans portable and in-duct systems used across residential, commercial, and light-industrial premises, and values are captured at final invoiced price to the first end-user.

Scope exclusions include automotive cabin purifiers, HVAC filter-only replacements sold without a powered fan module, and purely passive ion-emitting gadgets, which are outside our market boundary.

Segmentation Overview

- By Filtration Technology

- HEPA

- Activated Carbon

- Ionic/Electrostatic Precipitators

- UV-Cand Photocatalytic Oxidation

- Hybrid and Multi-stage Systems

- By Type

- Stand-alone/Portable

- In-duct/Central HVAC

- By Connectivity

- Non-Smart (Manual/Analog)

- Smart/IoT-Enabled (App and Voice Controlled)

- By End User

- Residential

- Commercial (Hospitality and Leisure, Healthcare Facilities and Clinics, Educational Institutions and Corporate Offices and Retail)

- Industrial (Manufacturing and Warehousing, Food and Beverage Processing, Pharmaceuticals and Clean-rooms and Data Centers and Server Rooms)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- Nordic Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with distributors, facility-management contractors, pulmonologists, and component suppliers in Asia-Pacific, North America, Europe, and the Gulf helped validate end-use mix, penetration ceilings, and filter-replacement cadence. Follow-up surveys with smart-home integrators clarified the take-up rate of IoT-enabled models before these insights fed our model.

Desk Research

Mordor analysts first mapped the universe of installed stock, shipments, and pricing by reviewing publicly available Tier-1 sources such as the World Health Organization ambient-air database, the United States EPA Indoor Air Quality program dashboards, UN Comtrade customs codes for HS 842139, and regional trade association bulletins from APAC and Europe. Company 10-Ks, investor decks, and product catalogs supplied average selling prices and wattage classes, which were then corroborated with import duty filings. Paid knowledge hubs including D&B Hoovers for company financial splits and Questel for patent momentum added early signals on emerging filtration media.

Additional triangulation drew on peer-reviewed journals tracking CADR effectiveness and building-code revisions (for example, ASHRAE 241), giving us load factors and replacement cycles. The sources cited above are illustrative; many other public datasets and industry briefings informed smaller calibration steps.

Market-Sizing & Forecasting

A top-down reconstruction began with annual production plus net import volumes, converted to retail revenue through blended ASPs; results were then cross-checked against a sampled bottom-up roll-up of fifteen brand portfolios to adjust for channel mark-ups. Key variables like urban PM2.5 exceedance hours, HEPA media cost trends, household disposable income bands, green-building floor-space additions, and IoT sensor attach rates drive our scenario inputs. A multivariate regression with lagged pollution indicators underpins the base outlook, while ARIMA smoothing captures short-run shocks such as wildfire events. Gaps in bottom-up coverage, especially in fragmented emerging markets, were bridged by applying verified penetration ratios obtained from primary calls.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer analyst cross-checks, and senior sign-off. Reports refresh each year, with interim tweaks when material events, such as regulatory shifts or large recalls, trigger a re-contact of key informants. Clients therefore receive the latest vetted view every time they download.

Why Mordor's Air Purifier Baseline Commands Reliability

Published estimates seldom align because firms differ in geographic reach, inclusion of aftermarket filter revenue, currency translation points, and refresh cadence.

Key gap drivers include whether industrial clean-room units are pooled with consumer models, how aggressively smart-service subscriptions are annualized, and if ASPs are held constant or inflation-indexed. Mordor's base case reports full device plus first-year filter value, applies real-time FX, and is updated annually, which together tighten variance margins.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.5 B (2025) | Mordor Intelligence | |

| USD 18.1 B (2025) | Global Consultancy A | Excludes filter-replacement and IoT-service revenue streams |

| USD 16.9 B (2024) | Trade Journal B | Omits Latin America & MEA and relies on constant-currency 2022 ASPs |

Values sourced from each publisher's public synopsis; names withheld for neutrality.

In sum, minor numerical spreads stem less from "right or wrong" counting and more from scope discipline. By combining transparent boundaries, recurring field calls, and variable-level modeling, Mordor Intelligence delivers a balanced baseline decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

How large will the global air purifier market be by 2031?

It is forecast to reach USD 29.05 billion by 2031, advancing at a 7.71% CAGR from 2026 to 2031.

Which filtration technology leads current sales?

HEPA media leads with 68.1% of 2025 revenue, thanks to 99.97% particle capture efficiency.

Why are in-duct systems growing faster than portable units?

Commercial buildings opt for centralized HEPA retrofits to meet LEED v4.1 and ASHRAE 62.1 standards, delivering whole-building compliance with lower lifecycle cost.

Which region holds the largest revenue share?

Asia-Pacific commanded 42.9% of 2025 turnover on the back of chronic PM2.5 pollution and robust electronics manufacturing.

What regulatory trend most influences North American demand?

LEED v4.1’s requirement for MERV 13 or higher filtration and real-time PM2.5 monitoring is driving widespread retrofits in offices and public buildings.

Page last updated on: