Air Insulated Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 93.96 Billion |

| Market Size (2031) | USD 121.58 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Insulated Switchgear Market Analysis by Mordor Intelligence

Air Insulated Switchgear market size in 2026 is estimated at USD 93.96 billion, growing from 2025 value of USD 89.24 billion with 2031 projections showing USD 121.58 billion, growing at 5.29% CAGR over 2026-2031.

Momentum stems from renewable integration mandates, national grid‐resilience programs, rising data-center load, and the phased restriction of SF₆-based equipment in Europe and North America. Utilities are shifting substation investment toward medium-voltage AIS because its upfront cost is lower than comparable GIS at voltage classes ≤38 kV. Supply-chain bottlenecks have lengthened typical delivery cycles beyond 90 weeks, prompting higher inventory buffers and dual-sourcing. The market also benefits from steady modernization of post-war transmission assets in the United States and Europe and electrification pushes in manufacturing hubs across Asia-Pacific and the Middle East.

Key Report Takeaways

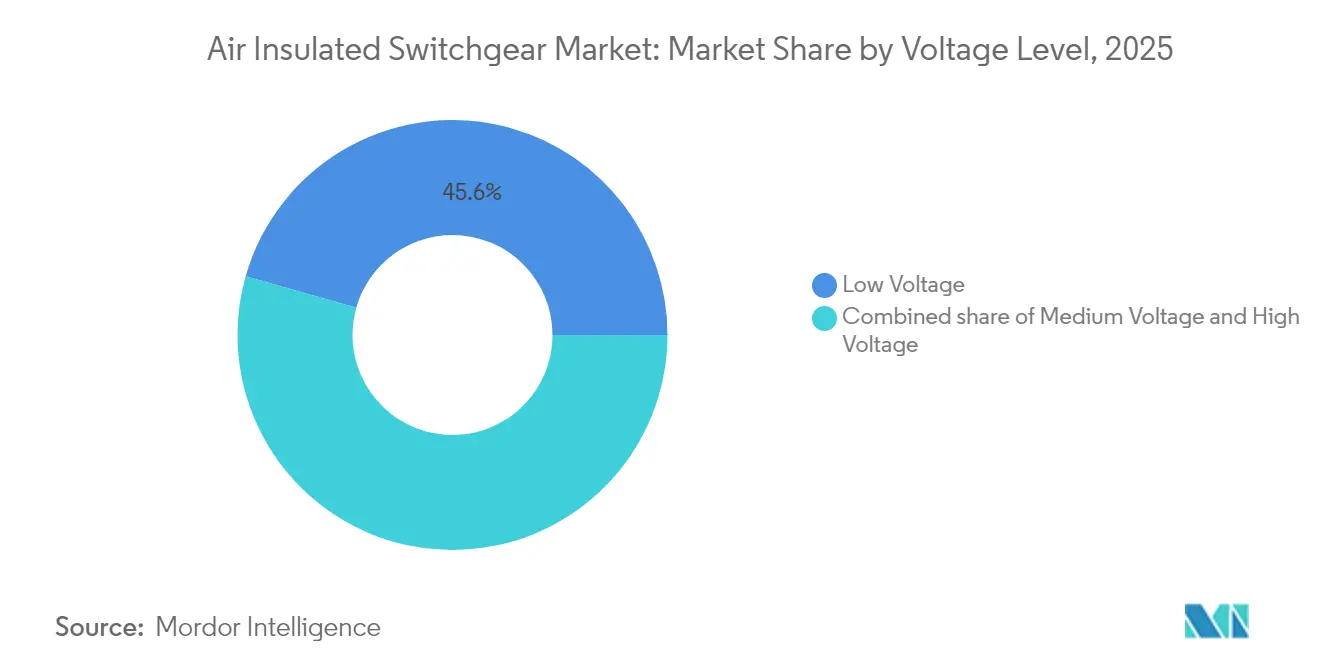

- By voltage classification, the Low-Voltage segment (Up to 1 kV) accounted for 45.60% of the air-insulated switchgear market share in 2025; the Medium-Voltage segment is projected to expand at a 6.05% CAGR to 2031.

- By end user, power utilities controlled a 57.50% share of the air-insulated switchgear market in 2025, whereas the industrial segment is advancing at the fastest 7.78% CAGR through 2031.

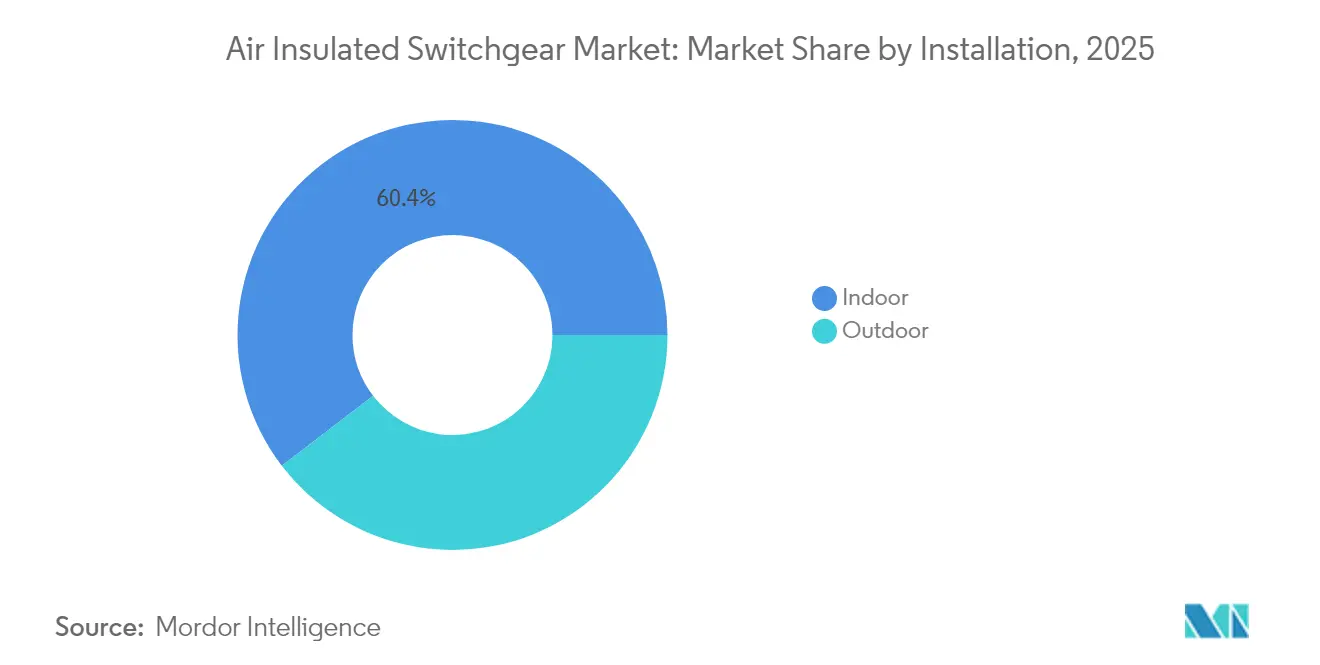

- By installation, indoor products held a 60.40% share of the air-insulated switchgear market size in 2025, yet outdoor units are moving ahead at a 6.74% CAGR to 2031.

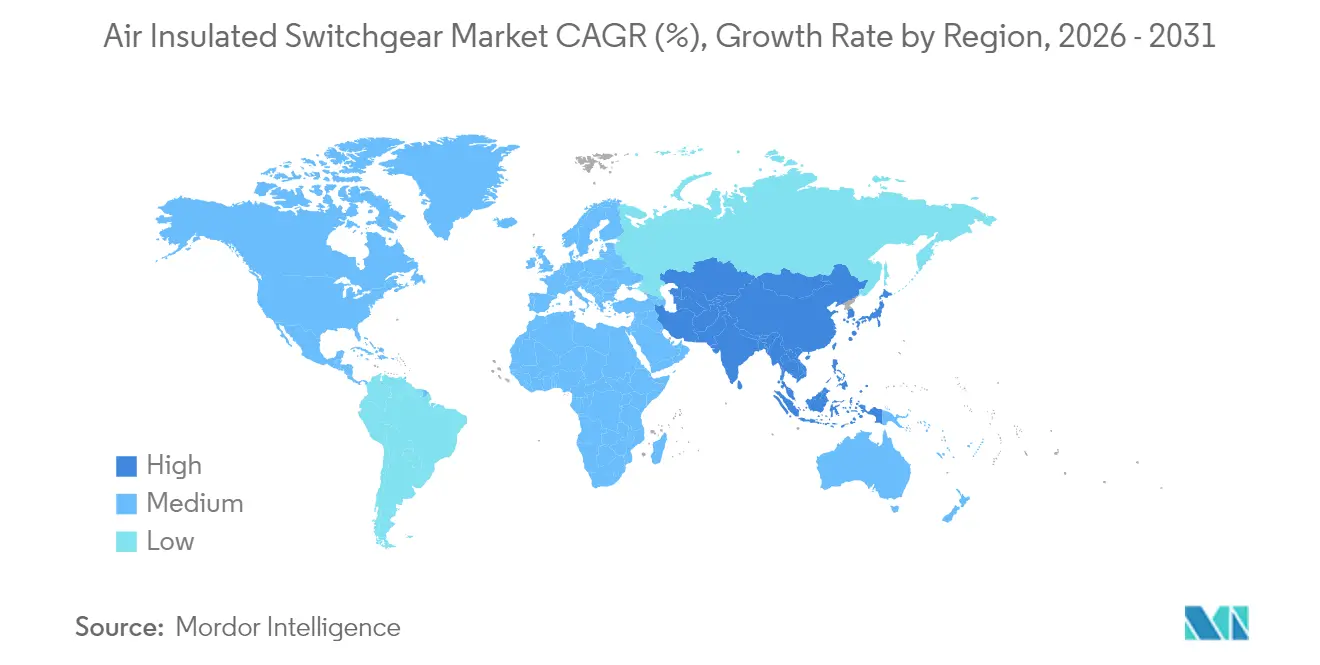

- By geography, Asia-Pacific led with 45.70% revenue share of the air-insulated switchgear market in 2025; the region is poised to grow at a 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Air Insulated Switchgear Market*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy build-out needs new AIS substations | +1.2% | Global, concentrated in APAC and North America | Medium term (2-4 years) |

| Replacement of ageing T&D infrastructure | +0.9% | North America & EU; spill-over to developed APAC | Long term (≥ 4 years) |

| Rapid urbanisation & electrification in emerging economies | +0.8% | APAC core; spill-over to MEA and South America | Long term (≥ 4 years) |

| AIS cost advantage over GIS at ≤38 kV | +0.6% | Global, strongest in price-sensitive markets | Short term (≤ 2 years) |

| Data-center boom driving campus MV-AIS demand | +0.5% | North America & EU; emerging presence in APAC | Medium term (2-4 years) |

| Microgrid uptake needing modular indoor AIS | +0.3% | Global, early adoption in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy Build-Out Needs New AIS Substations

Grid operators expanding wind and solar capacity deploy AIS collector substations to manage bidirectional power flow and voltage variability. The U.S. National Transmission Planning Study projects a need to double transmission transfer capability by mid-century, suggesting large volumes of new medium-voltage bays that favor AIS for cost and modularity.[1]U.S. Department of Energy, “Grid Resilience Grants,” energy.gov Saudi Arabia plans USD 126 billion for transmission upgrades, where the bulk of medium-voltage renewable interties adopt AIS to manage cost envelopes. Manufacturers are enhancing protection algorithms to stabilize networks with high intermittent feed-in, further strengthening AIS value propositions. Land availability in onshore renewables corridors eases footprint concerns, allowing utilities to prioritize total ownership cost. As clean-energy auctions tighten commissioning timelines, faster AIS manufacturing cycles give project developers a scheduling hedge.

Replacement of Ageing T&D Infrastructure

Over half of North American substation assets date to the 1960s–1980s build-out. Entergy Texas alone earmarked USD 335 million for distribution and substation upgrades in 2025. European utilities show parallel urgency; National Grid’s Wimbledon rebuild underscores the scale of legacy replacement[2]Institution of Civil Engineers, “National Grid Wimbledon Upgrade,” ice.org.uk. Condition-monitoring retrofits drive predictive maintenance, letting asset managers phase out obsolete gear with minimal service loss. AIS vendors are capitalizing by bundling digital sensors and arc-flash containment as standard features. The replacement wave spreads investment over a 10-year horizon, delivering consistent demand for the air-insulated switchgear market even in mature economies.

Rapid Urbanisation & Electrification in Emerging Economies

Asia-Pacific adds more than 15 million urban residents yearly, pushing distribution feeders deeper into peri-urban zones. India’s Saubhagya initiative connected 28 million households since 2017, expanding medium-voltage AIS roll-out across rural districts.[3]Hitachi Energy, “Saubhagya Electrification Support,” hitachienergy.com China’s state utilities press ahead with smart-grid pilots, integrating distributed generation, elevating demand for digitally enabled AIS cubicles. As manufacturing migrates to Southeast Asia, industrial parks specify campus sub-stations that favor modular AIS for quick expansion. Governments increasingly require climate-resilient infrastructure, prompting higher ingress-protection ratings on outdoor AIS panels suited for extreme heat and dust.

AIS Cost Advantage Over GIS at ≤38 kV

Capital bids indicate GIS can carry a 10-40% premium over comparable AIS at medium-voltage ratings, widening in markets with foreign-currency pressure on imported gas-insulated kits.[4]Beta Engineering, “Cost Comparison of AIS Versus GIS,” betaengineering.com AIS further avoids specialized gas handling and the compliance burden tied to SF₆ audits, cutting life-cycle cost. Although land-constrained urban projects often tilt toward compact GIS, most renewable, industrial, and utility expansions still occur where land cost is moderate, preserving the air-insulated switchgear market’s price edge. Emerging SF₆-free GIS narrows the gulf but remains in early scale-up, keeping AIS in a favorable position during the forecast period.

Restraints Impact Analysis of Air Insulated Switchgear Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban-space constraints favour compact GIS | -0.7% | Dense urban nodes in APAC and EU | Short term (≤ 2 years) |

| Shift to SF₆-free GIS / solid-insulated alternatives | -0.5% | EU and North America lead; global diffusion | Medium term (2-4 years) |

| Commodity-supply shocks stretch AIS lead times | -0.4% | Global; copper-intensive products most exposed | Short term (≤ 2 years) |

| Rising digital-safety codes push arc-resistant switchgear | -0.3% | North America and EU; developed APAC gaining | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urban-Space Constraints Favour Compact GIS

High land prices in megacities such as Jakarta and Mumbai compel utilities to move primary substations underground. An AIP study shows underground GIS stations use 60–75% less surface area than air-insulated yards.[5]AIP Conference Proceedings, “Underground GIS Substation Design,” aip.scitation.org Municipal authorities often waive permit fees for compact footprints, offsetting GIS hardware premiums. European urban planners push similar policies to preserve streetscapes, nudging transmission owners toward indoor GIS even at traditional AIS voltage levels. Distribution companies also deploy compact ring-main units in mixed-use buildings, limiting the addressable share for outdoor AIS within dense cores.

Shift to SF₆-Free GIS / Solid-Insulated Alternatives

The EU regulation 2024/573 bans new fluorinated-gas switchgear in most medium-voltage classes beginning in 2026, accelerating supplier roadmaps for clean-air or solid-insulated solutions. Hitachi Energy and Siemens Energy have launched SF₆-free 170 kV and 145 kV lines, signaling a structural pivot that may siphon demand from higher-voltage AIS. North American utilities are voluntarily piloting similar equipment to meet corporate net-zero goals. Although AIS technology carries no SF₆, competitive pressure rises as buyers weigh environmental footprints alongside cost. Vendors must therefore differentiate with integrated monitoring and arc-resistant enclosures to maintain relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Air Insulated Switchgear Market Segment Analysis

By Voltage Level:

Medium Voltage Drives InnovationThe Low-Voltage segment held 45.60% of the air-insulated switchgear market 2025, primarily serving residential and light-commercial circuits. Medium-Voltage demand is projected to advance at a 6.05% CAGR, anchored in renewable collector stations, data-center campuses, and process-industry electrification. High-Voltage units occupy a smaller yet stable niche that benefits from grid rebuilds and emerging HVDC back-to-back stations.

Growth reflects divergent application profiles. Low-Voltage boards rely on mass-produced designs where price and footprint dictate selection. Medium-Voltage buyers increasingly specify digital current transformers and IEC 61850 gateway modules that enable predictive analytics. As a result, the air-insulated switchgear market size for medium-voltage applications is forecast to contribute USD 12.35 billion incremental value by 2031. High-Voltage projects, though fewer, demand engineered-to-order panels that integrate phase-shifting transformers and complex protection logic. Suppliers leverage these projects to showcase advanced arc-resistant metal-clad designs and to test SF₆-free interrupters.

By End-User:

Industrial Segment AcceleratesPower utilities owned 57.50% of the worldwide air-insulated switchgear market share in 2025, owing to their stewardship of national grids. Industrial facilities, especially semiconductor, automotive, and food-processing plants, will grow at 7.78% CAGR through 2031. Commercial complexes adopt AIS for building electrification and EV-charging halls, but their expansion pace is moderate relative to industrial builds.

Manufacturing electrification raises fault-current ratings and mandates sectionalized feeders, pushing factory owners toward medium-voltage AIS with digital relays. Schneider Electric’s USD 700 million U.S. expansion dedicates an entire line to such solutions. Utility buying cycles remain linked to regulatory rate approvals, yet grid-hardening investments stabilize baseline volume. Over time, diversified demand reduces reliance on state-funded projects and spreads the air-insulated switchgear industry’s revenue base.

By Installation:

Outdoor Applications Gain MomentumIndoor switchgear installations retained a 60.40% share of the global air-insulated switchgear market in 2025 because controlled environments extend equipment life and simplify maintenance. Outdoor units will outpace at a 6.74% CAGR as renewable farms and remote substations expand. The installation of split mirrors in climate resilience planning, with utilities retrofitting enclosures to withstand flooding and temperature swings.

Regulatory updates, including the 2023 National Electrical Code requirement for visible arc-flash labeling above 1,000 A, influence enclosure designs. Outdoor AIS now ships with reinforced arc-chimneys and stainless hardware to handle corrosive atmospheres. Indoor panels are integrating IoT-ready sensors for continuous thermal tracking. The air-insulated switchgear market size for outdoor applications is projected to reach USD 51.58 billion by 2031 as public-private utilities extend feeders into solar clusters and rural electrification corridors.

Geography Analysis

APAC, EMEA and North America Air Insulated Switchgear Market

Asia-Pacific dominated the air-insulated switchgear market with a 45.70% revenue share in 2025, powered by China’s state-led grid upgrades and India’s ongoing village electrification. Chinese utilities continue to pilot 35 kV digital AIS bays that dovetail with rooftop solar aggregation, while India ramps up procurement under its Revamped Distribution Sector Scheme. Japan, South Korea, and Australia add a steady backlog through data-center and offshore wind expansions. Southeast Asia contributes rising volume as industrial estates proliferate across Vietnam, Thailand, and Indonesia.The Middle East and Africa region is one of the fastest-growing, underpinned by Saudi Arabia’s USD 126 billion transmission blueprint and the UAE’s renewable portfolio targets. GCC utilities favor AIS for medium-voltage collector nodes because desert siting mitigates land-use pressure. African electrification projects, notably in Kenya and Egypt, depend on concessional financing that aligns with AIS’s lower capex relative to GIS. Local fabrication partnerships emerge as governments push content requirements, broadening supply footprints for international vendors.North America and Europe display mature yet opportunity-rich profiles. Despite rate shocks, the U.S. government’s USD 2.2 billion grid-resilience grants maintain public utility spending. Canadian provinces pursue the life extension of hydro-linked substations, blending refurbishment and selective replacement. Europe’s SF₆ phase-out has a dual effect: high-voltage buyers pivot toward clean-air GIS, while low- and medium-voltage owners revisit AIS for cost-effective compliance. Domestic manufacturing expansions from GE Vernova and Hitachi Energy illustrate reshoring policy traction and offer lead-time relief for regional buyers.

Mordor Intelligence provides coverage of the air insulated switchgear market across other key regional markets, including Middle East and Africa, North America, South America, and Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The air-insulated switchgear market features moderate concentration. ABB, Siemens, Schneider Electric, Hitachi Energy, and GE Vernova combined held a major revenue share in 2024. Each player invests heavily in SF₆-free interrupters and digital twins, with cumulative announced capex exceeding USD 2 billion through 2027. Product roadmaps converge on IEC 61850 native designs and cloud-hosted asset-health dashboards that provide subscription revenue.

Strategically, incumbents expand localized manufacturing. Schneider’s El Paso plant will double North American AIS output by 2026, while Hitachi Energy upgrades its Pennsylvania base to scale EconiQ SF₆-free breakers. GE Vernova allocates USD 600 million for U.S. switchgear and transformer capacity, aligning with Buy-America preferences. Simultaneously, Chinese and Korean suppliers grow exports by leveraging lower cost structures, challenging Latin America and Africa's price points.

Partnerships and selective acquisitions accelerate technology breadth. ABB’s purchase of Siemens Gamesa’s power-electronics arm expanded its renewable-integration portfolio by 40 GW of installed base.[6]ABB, “Acquisition of Gamesa Electric Power Electronics,” abb.com TE Connectivity added Harger’s grounding expertise, improving system-level resilience for utility clients. Service is a crucial differentiator; vendors embed multiyear condition-monitoring contracts that guarantee uptime and help lock future hardware replacements.

Air Insulated Switchgear Industry Leaders

ABB Ltd

Siemens AG

Schneider Electric SE

Mitsubishi Electric Corp

Eaton Corp plc

- *Disclaimer: Major Players sorted in no particular order

Air Insulated Switchgear Market Companies Covered in this Report

- ABB Ltd

- Siemens AG

- Schneider Electric SE

- Eaton Corp plc

- Mitsubishi Electric Corp

- General Electric (Vernova)

- Hitachi Energy Ltd

- Larsen & Toubro Ltd

- Alfanar Group

- Tavrida Electric

- Wenzhou Unisun Electric

- Elatec Power Distribution

- Fuji Electric Co Ltd

- Chint Group

- Lucy Electric

- Ormazabal

- S&C Electric Co

- Powell Industries

- Rockwill Electric

- C&S Electric

Recent Industry Developments in Air Insulated Switchgear Market

- April 2025: Hitachi Energy committed over USD 70 million to a new Pennsylvania facility focused on EconiQ SF₆-free high-voltage switchgear.

- March 2025: Hitachi Energy set aside another USD 250 million to expand transformer-component output worldwide to meet AI-driven electricity demand.

- January 2025: EMCOR Group agreed to acquire Miller Electric Company for USD 865 million to deepen data-center electrical capabilities.

- January 2025: GE Vernova announced plans to spend nearly USD 600 million on U.S. manufacturing sites, scaling domestic switchgear output.

Global Air Insulated Switchgear Market Report Scope

The air insulated switchgear market report includes:

Segmentation Overview

| Low Voltage (Up to 1 kV) |

| Medium Voltage (1 to 38 kV) |

| High Voltage (Above 38 kV) |

| Power Utilities (T&D) |

| Industrial |

| Commercial |

| Residential |

| Indoor |

| Outdoor |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Voltage Level | Low Voltage (Up to 1 kV) | |

| Medium Voltage (1 to 38 kV) | ||

| High Voltage (Above 38 kV) | ||

| By End-User | Power Utilities (T&D) | |

| Industrial | ||

| Commercial | ||

| Residential | ||

| By Installation | Indoor | |

| Outdoor | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the air insulated switchgear market?

The market is valued at USD 93.96 billion in 2026 and is projected to reach USD 121.58 billion by 2031.

Which region leads the air insulated switchgear market?

Asia-Pacific accounts for 45.70% of global revenue, driven by ongoing grid upgrades in China and India.

Why is medium-voltage AIS gaining traction?

Industrial automation, renewable-energy collector stations, and data-center campuses prefer medium-voltage AIS for its modularity, digital readiness, and lower life-cycle cost versus GIS.

How will SF₆ regulations affect AIS demand?

European and North American bans on fluorinated gases boost interest in AIS as a compliant alternative at voltage classes where GIS traditionally dominates.

What are typical lead times for AIS equipment in 2025?

Supply-chain disruptions have extended delivery cycles to more than 90 weeks, leading utilities to maintain higher inventory buffers.

Which companies are investing in domestic AIS production?

GE Vernova, Hitachi Energy, Schneider Electric, and Mitsubishi Electric all announced new U.S. facilities or expansions slated for completion by 2027.

Page last updated on: