Air-based C4ISR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

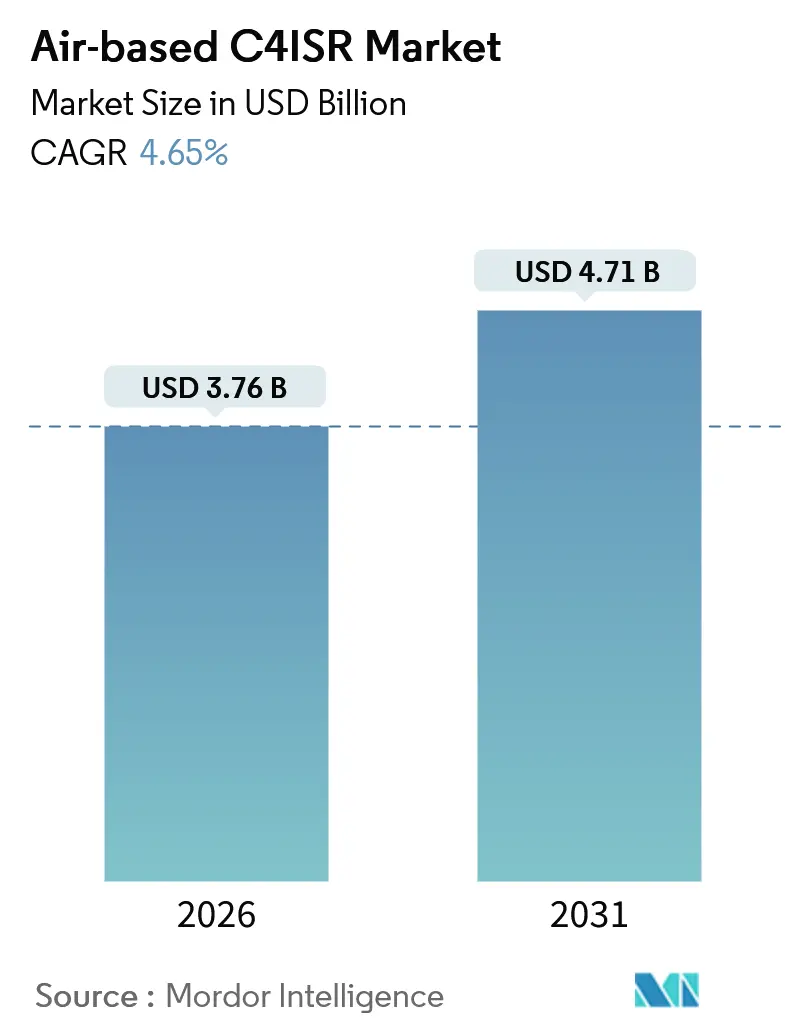

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 4.71 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

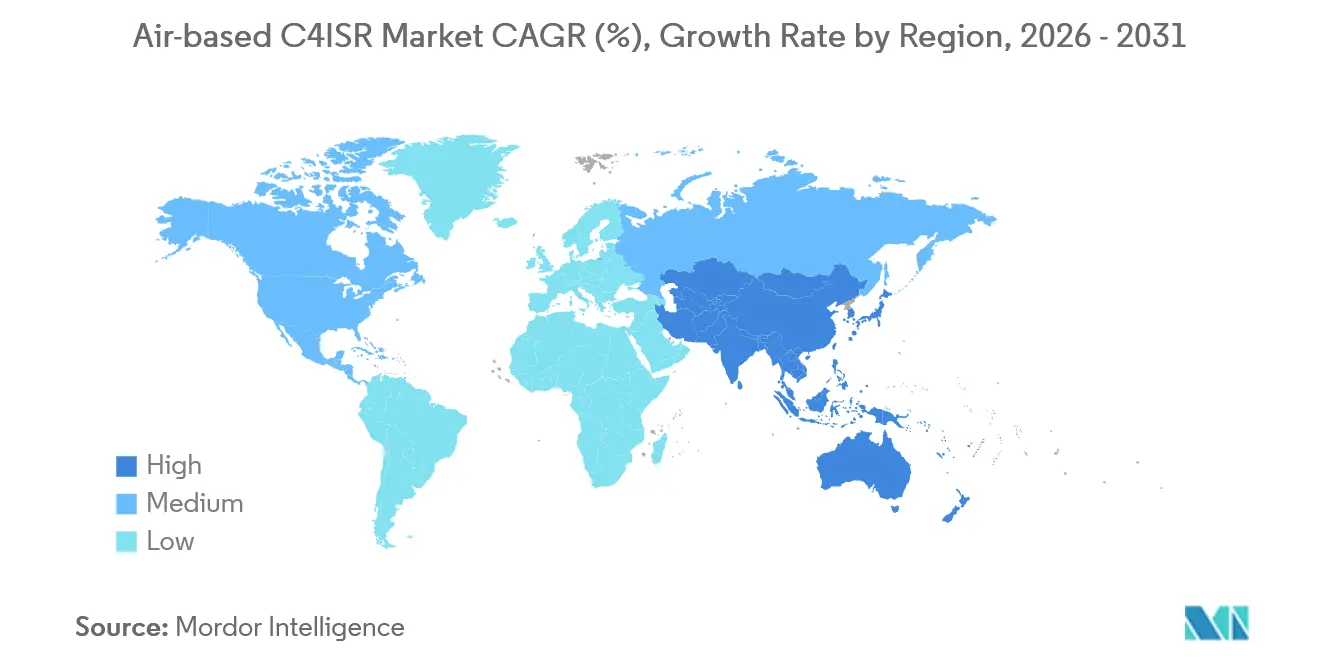

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air-based C4ISR Market Analysis by Mordor Intelligence

The air-based C4ISR market is expected to grow from USD 3.76 billion in 2026 to USD 4.71 billion by 2031, registering a CAGR of 4.65%. The adoption of network-centric doctrines, such as the US Department of Defense’s USD 13.8 billion allocation for the Joint All-Domain Command and Control initiative, is driving investments in software-defined sensors capable of real-time intelligence sharing across platforms. Sovereign data-residency regulations in regions like Europe and Asia-Pacific are encouraging prime contractors to integrate edge processing capabilities into airframes, while open-architecture requirements, such as the Modular Open Systems Approach (MOSA), are reducing the dominance of proprietary integration systems. Additionally, unmanned High-Altitude Long-Endurance (HALE) and Medium-Altitude Long-Endurance (MALE) fleets are increasingly taking on roles traditionally performed by crewed aircraft. Low-Earth-orbit satellite operators are addressing coverage gaps that previously hindered consistent airborne connectivity. However, challenges such as reliance on Chinese gallium and rare-earth processing, along with spectrum congestion in peer-adversary anti-access zones, continue to constrain near-term market growth.

Key Report Takeaways

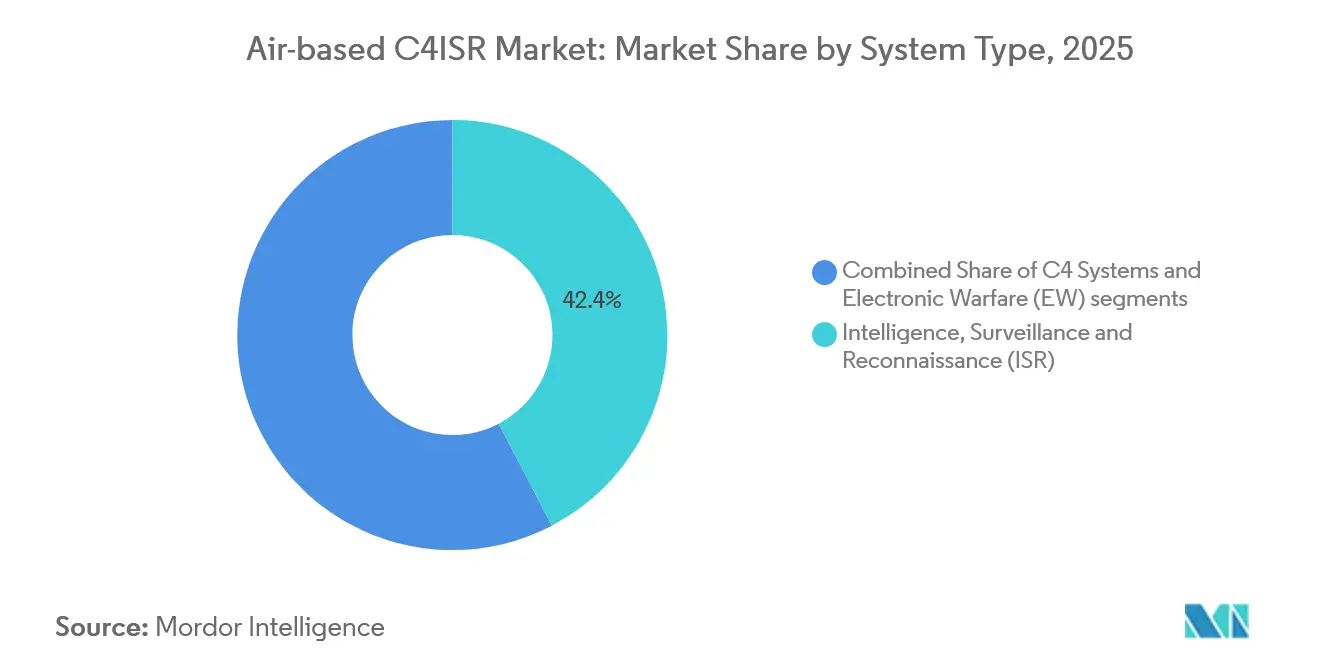

- By system type, intelligence, surveillance, and reconnaissance held 42.35% Air-based C4ISR market share in 2025, while also recording the fastest 6.47% CAGR through 2031.

- By platform, manned aircraft accounted for 36.41% of the Air-based C4ISR market size in 2025, whereas unmanned systems are advancing at a 5.98% CAGR to 2031.

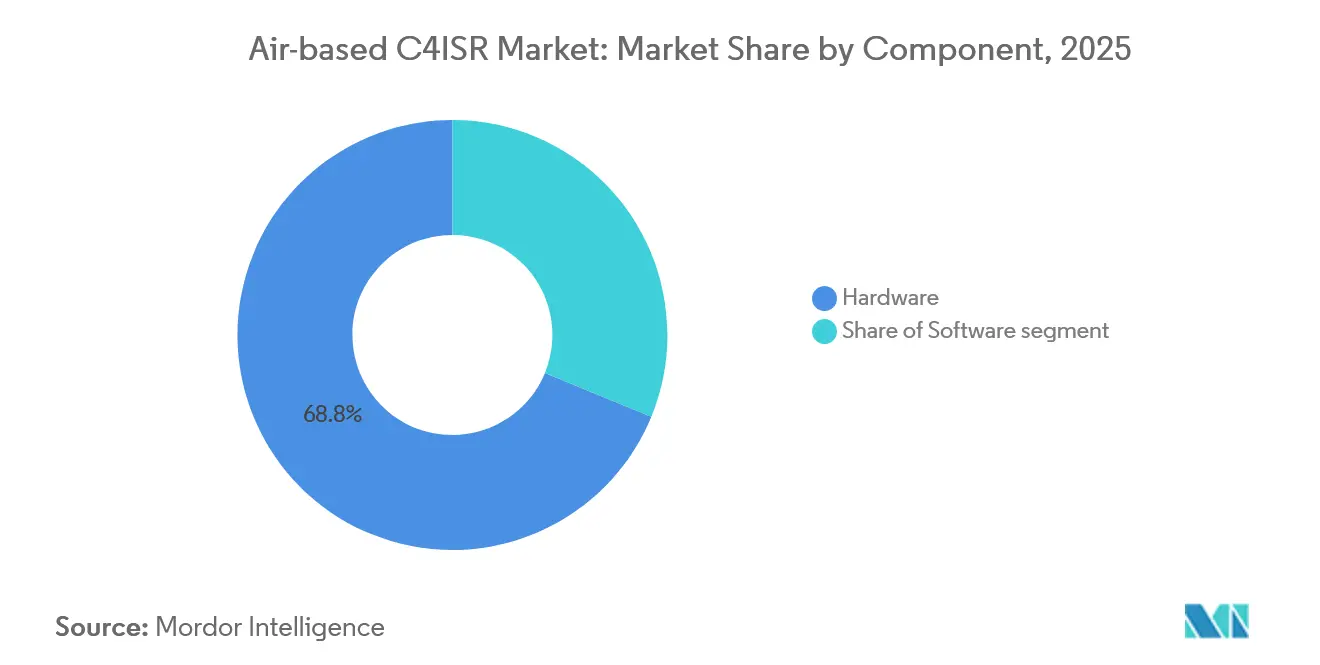

- By component, hardware captured a 68.79% share in 2025; software is set to post a 5.15% CAGR as open standards accelerate refresh cycles.

- By end-user, defense forces commanded 86.59% revenue share in 2025, but civil and government agencies are expanding at a 5.04% CAGR through 2031.

- By geography, North America led with a 36.82% Air-based C4ISR market share in 2025, while the Asia-Pacific region is forecast to grow the quickest at a 5.08% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Air-based C4ISR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid multi-domain operations doctrine | +1.20% | North America, NATO Europe, Australia | Medium term (2-4 years) |

| AI-enabled sensor-to-shooter data fusion | +0.90% | United States, Israel, South Korea | Long term (≥ 4 years) |

| Proliferation of HALE / MALE UAV fleets | +0.80% | Asia-Pacific, Middle East, North America | Short term (≤ 2 years) |

| Modular Open Systems Architecture mandates | +0.70% | North America, Europe | Medium term (2-4 years) |

| Low-Earth-orbit sat-com constellations | +0.50% | Indo-Pacific, Arctic, remote theaters | Long term (≥ 4 years) |

| Silicon-photonics RF front-ends | +0.40% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Multi-Domain Operations Doctrine Reshaping Procurement Priorities

Joint all-domain frameworks demonstrated during Exercise Northern Edge 2025 enabled an F-35 to share target coordinates with an Army missile battery, completing engagement in under 90 seconds.[1]U.S. Air Force Public Affairs, “Northern Edge 25 Demonstrates Cross-Domain Kill Chain,” af.mil Canada allocated USD 1.5 billion to integrate CP-140 Aurora aircraft into the same network in 2025, while Australia’s Project AIR 7000 mandated open mission systems for P-8A Poseidon upgrades. These initiatives are redirecting spending toward middleware capable of transmitting high-resolution sensor data beyond the capacity of legacy Link 16 systems. As a result, integrators that can rapidly certify new waveforms are securing contracts, while primes resisting the Modular Open Systems Approach (MOSA) standards risk disqualification from future competitions.

AI-Driven Sensor Fusion Accelerating Decision Cycles

Northrop Grumman’s AI planning suite on the RQ-4 Global Hawk achieved 92% target-identification accuracy and reduced analyst workload by 60% in 2025.[2]Northrop Grumman Corporation, “Annual Report 2025,” northropgrumman.com Israel’s Air Force deployed an autonomous mission manager on Hermes 900 UAVs, enabling aircraft rerouting without human intervention. Additionally, the US Joint Artificial Intelligence Center standardized 12 petabytes of imagery for algorithm training. However, certification remains a challenge, as FAA and EASA regulations for AI-powered flight-critical software are still in draft form, delaying civil adoption despite military demand for greater autonomy. The advancements in AI-driven sensor fusion are expected to significantly enhance operational efficiency and decision-making capabilities in complex scenarios.

Proliferation of HALE / MALE UAV Fleets Requiring Plug-and-Play C4ISR

India finalized a 31-unit MQ-9B SkyGuardian order in 2025, including indigenous radar pods that can be swapped in under four hours. The UAE’s Wing Loong II fleet adopted NATO-standard datalinks in 2024, highlighting the demand for open interfaces even on Chinese platforms. South Korea’s KUS-FS drone demonstrated hot-swap payload capabilities within 90 minutes, reducing turnaround times and cutting lifecycle costs by 30%. This adaptability positions unmanned systems to take on missions where crewed aircraft are unsuitable due to threat environments or endurance requirements. The increasing reliance on HALE and MALE UAV fleets underscores the importance of plug-and-play C4ISR systems in modern military operations.

MOSA Mandates Fragmenting Traditional Integration Models

The US Department of Defense’s clause 252.227-7019 requires new C4ISR contracts to adopt open standards, allowing third-party software updates without OEM involvement. In 2025, L3Harris secured a USD 496 million contract to retrofit P-8A Poseidons with MOSA-compliant systems. NATO’s parallel initiative mandates the retirement of non-compliant aircraft by 2028, encouraging smaller vendors to enter the air-based C4ISR market, which has been previously dominated by proprietary incumbents. The shift toward MOSA standards is expected to drive innovation and competition, reshaping traditional integration models across the defense industry.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dense spectrum congestion over A2AD bubbles | -0.60% | Taiwan Strait, South China Sea, Eastern Europe | Short term (≤ 2 years) |

| Sovereign data-localization laws | -0.40% | Europe, India, China, Middle East | Medium term (2-4 years) |

| Gallium and rare-earth supply risk | -0.50% | Global, heavy impact on US and European manufacturers | Long term (≥ 4 years) |

| Certification delays for AI software on legacy airframes | -0.30% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion in Anti-Access Environments Degrading Link Reliability

China’s coordinated jamming during the 2025 exercises reduced Global Hawk datalink availability to below 70% for extended periods. Similarly, Russia’s Krasukha-4 system caused comparable disruptions in the Baltic region, prompting NATO members to adopt frequency-hopping radios, which add USD 4 million per aircraft. DARPA’s Spectrum Collaboration Challenge awarded USD 3.5 million to autonomous algorithms capable of identifying open frequencies. However, FAA approval for integration into manned aircraft remains pending. As a result, Air-based C4ISR market participants must develop multi-band solutions capable of operating in high-noise environments until regulatory frameworks are finalized. The increasing spectrum congestion highlights the need for robust and adaptive communication technologies to maintain operational effectiveness in contested environments.

Gallium and Rare-Earth Supply Concentration Threatening T/R Module Production

China’s control of 70% of global gallium processing led to a 60% price increase following 2023 export restrictions, extending radar lead times from 18 to 32 weeks by 2025.[3]Demetri Sevastopulo, “PLA Ramps Up Electronic Warfare,” ft.com The US Department of Defense awarded MP Materials USD 35 million to expand domestic separation capacity, though significant output is not expected until 2027. In 2025, Germany secured a 24-month gallium inventory to protect Hensoldt programs from supply volatility. Until supply chains diversify, growth in the Air-based C4ISR market will remain constrained by semiconductor availability. The concentration of gallium and rare-earth processing underscores the critical need for supply chain diversification to ensure the stability of T/R module production and broader market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: ISR Systems Sustain Lead on Multi-Sensor Fusion

Intelligence, surveillance, and reconnaissance (ISR) solutions accounted for 42.35% of the Air-based C4ISR market share in 2025, growing at a 6.47% CAGR due to the demand for persistent wide-area coverage. Armed forces are replacing single-purpose platforms with drones and pods that integrate synthetic-aperture radar, electro-optical, and SIGINT sensors. This transition reduces per-hour operating costs while improving detection probabilities. In 2024, BAE Systems delivered a laser-guided rocket equipped with ISR sensors, demonstrating how expendable ordnance now serves dual purposes as both a weapon and a data collector.

Conversely, command-and-control networks are growing at a slower pace due to the maturity of Link 16 infrastructure and episodic demand for electronic warfare (EW), which spikes after incidents such as Russia’s jamming activities in Ukraine. However, ISR and EW are increasingly converging. For example, Elbit’s SPECTRO XR pod combines passive collection with active jamming, reducing drag by 18% compared to separate passive and active jamming pods. This integration is expected to sustain dynamism in the Air-based C4ISR market throughout the forecast period.

By Platform: Unmanned Assets Accelerate Growth in Contested Airspace

Manned aircraft retained 36.41% of revenue in 2025, supported by platforms like the P-8A Poseidon, which provides maritime reach that most drones cannot achieve. Rotary-wing variants remain essential for anti-submarine warfare, as dipping sonar technology has not yet been miniaturized for unmanned helicopters.

Unmanned systems, however, are growing at a 5.98% CAGR as operators shift risk to machines and leverage endurance profiles of up to 48 hours, exemplified by Turkey’s Bayraktar Akinci demonstrations. Countries such as India, the United Kingdom, and South Korea are prioritizing UAVs over new manned fleets, signaling a long-term shift toward platform autonomy in the Air-based C4ISR market.

By Component: Software Captures Incremental Value Under Open Standards

Hardware accounted for 68.79% of revenue in 2025; however, software is growing at a 5.15% CAGR due to the adoption of the Modular Open Systems Approach (MOSA) and the Future Airborne Capability Environment (FACE) standards, which separate applications from physical avionics. Collins Aerospace’s FACE-compliant software for Future Vertical Lift enables annual threat library updates without requiring re-certification, resulting in a 35% reduction in lifecycle costs.

While hardware growth is tied to 25-year platform replacement cycles, software can be deployed more frequently. For instance, Thales provides over-the-air updates for French Rafale fighters, and Leonardo’s software-defined radio replaces four separate units, highlighting how software increasingly defines capability. This shift underscores a long-term transformation in the Air-based C4ISR market economics.

By End-User: Civil Agencies Broaden Scope Beyond Traditional Defense

Defense ministries generated 86.59% of demand in 2025; however, civil and government agencies are growing at a 5.04% CAGR, as border security and disaster relief operations require real-time situational awareness. Organizations such as Japan’s Coast Guard and the European Maritime Safety Agency are adopting service-leasing models to avoid significant capital expenditures.

Civil operators prefer commercial-off-the-shelf solutions, prompting manufacturers to develop commercial variants of military pods. Regulatory frameworks, such as GDPR, necessitate onboard data processing to minimize cross-border data transfers, influencing procurement decisions and driving regional variations in the Air-based C4ISR market.

Geography Analysis

North America accounted for 36.82% of the revenue in 2025, supported by Pentagon funding for Joint All-Domain Command and Control (JADC2) and FAA waivers that facilitated unmanned operations beyond the visual line of sight. Canada is integrating CP-140 Aurora aircraft into combined networks, while Mexico’s King Air 260 ISR fleet addresses counter-narcotics missions. Although ITAR export controls limit external sales, domestic demand ensures a stable trajectory for the regional Air-based C4ISR market.

The Asia-Pacific region is growing at a 5.08% CAGR, driven by India’s USD 3.5 billion MQ-9B acquisition, Japan’s ISR enhancements following North Korean missile activity, and South Korea’s indigenous drone programs. China’s GJ-11 stealth UAVs are prompting neighboring countries to accelerate upgrades, while Taiwan’s additional E-2D Advanced Hawkeye orders highlight continued reliance on crewed early-warning aircraft.

Europe and the Middle East exhibit similar growth trends, with NATO standardization and GCC joint procurement initiatives helping to reduce unit costs. Germany’s Airbus A321MPA acquisition reflects Europe’s preference for native sensors, while Saudi Arabia’s Vision 2030 localization strategy is fostering joint ventures that redirect a portion of the global Air-based C4ISR market into Gulf supply chains.

Regulatory Landscape

Air-based C4ISR procurements are increasingly shaped by open-architecture and interoperability requirements that affect eligibility for new awards. In the United States, DoD policy rooted in 10 U.S.C. 4401-4403 has formalized the Modular Open Systems Approach (MOSA) as a default for defense acquisition programs, reinforced by a Tri-Service alignment memo signed on Dec 17, 2024, and complementary guidance such as the Defense Logistics Agency Digital Standards Strategy (Jan 8, 2026), which emphasizes digital standards adoption across defense programs.

Standardization is also tightening through multinational frameworks that influence platform integration and cross-border teaming. In NATO, the enhanced Air Command and Control (eAirC2) Complex Armament Programme (CAP) is being used to integrate multi-domain air operations and surveillance, while NATO modular Ground-Based Air Defense (GBAD) activities highlight interoperability and data sharing, including a June 2026 consortium milestone led by Lockheed Martin UK (with Leonardo, MBDA, and Indra) advancing architecture work. In Europe, the European Defence Fund (EDF) 2026 Work Programme adopted on Dec 17, 2025 (EUR 1.01 billion) channels collaborative R&D into information superiority and multi-domain themes, shaping compliant technology roadmaps and consortium formation for C4ISR-related avionics, mission systems, and secure communications.

Value Chain Analysis

The air-based C4ISR value chain starts with mission-system requirements and architecture definition (defense ministries and airworthiness or qualification authorities), then moves to prime integration on manned and unmanned airframes. It continues through subsystem supply (radars, EO/IR, SIGINT/EW, communications, encryption, processors), software and middleware (open-architecture applications, data fusion, mission management), and then test, certification, fielding, and long-tail sustainment such as depot maintenance, upgrades, spares, and training. Open standards such as MOSA and FACE shift more value toward portable software, middleware, and rapid payload swaps, while export controls and national industrial participation rules influence where integration and maintenance are performed.

Partnerships and cross-tier teaming are central to delivering end-to-end airborne capability, especially for business-jet special mission aircraft and unmanned payload integration. Saab and General Atomics Aeronautical Systems (June 2025) cooperated on an unmanned airborne early warning concept integrating Saab sensors on MQ-9B, and Frequentis C4i supplied multi-domain communications to Lockheed Martin Australia for AIR6500 (March 2025). Sub-tier constraints have become a gating factor for program schedules, with 2025-2026 bottlenecks highlighted around optical terminals, encryption devices, specialized electronics (including gallium nitride substrates and radiation-tolerant components), and machining capacity, which amplifies lead-time risk for primes and MRO providers supporting upgrades across mixed fleets.

Competitive Landscape

The Air-based C4ISR market is moderately concentrated, with the top five companies accounting for 55% of revenue. However, open-architecture standards are reducing traditional barriers. Lockheed Martin and Northrop Grumman maintain strong integration capabilities, while Kratos Defense has secured UAV pod contracts by offering MOSA-compliant payloads at 40% lower costs. Major players are increasingly acquiring software firms to enhance their digital capabilities, as demonstrated by Northrop Grumman’s 2024 acquisition of a radar analytics company.

Disruptors from the commercial space sector are also entering the market. For example, Starlink terminals have been approved for military aircraft retrofits, providing enhanced bandwidth with minimal capital expenditure. Consortia like Team Reaper combine complementary expertise to secure billion-dollar modernization contracts, distributing risks among its members. Compliance with standards such as DO-178C and MOSA is becoming a critical requirement; proposals lacking these certifications often fail technical evaluations despite competitive pricing.

Looking ahead, companies that integrate proprietary security systems with open APIs are likely to maintain their market share, while those that fail to adapt risk being commoditized. The Air-based C4ISR market is expected to strike a balance between economies of scale and the need for agility, paving the way for selective consolidation focused on AI software and miniature sensor technologies.

Air-based C4ISR Industry Leaders

Lockheed Martin Corporation

BAE Systems plc

L3Harris Technologies, Inc.

Northrop Grumman Corporation

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Modernization programs that prioritize data-layer interoperability and faster sensor-to-shooter integration are creating demand for modular airborne mission systems, middleware, and resilient communications spanning air, ground, and space. In the United States, the Army has publicized progress in establishing an NGC2 common data layer baseline (June 2026) and scheduled a division-scale validation event at the National Training Center (Project Convergence-Capstone 6, July 2026), which supports demand for airborne nodes that can publish, subscribe, and translate data across heterogeneous tactical networks. In parallel, the DoD FY2026 request for USD 23.2 billion across procurement and RDT&E for C4I systems reinforces the scale of budgetary commitment to digital command-and-control upgrades that involve airborne platforms, gateways, and mission applications.

Opportunities also extend to the air-space interface, where proliferated space sensing and missile tracking architectures raise the need for airborne relay, cueing, and fusion capabilities in contested environments. The Space Development Agency awarding about USD 1.75 billion for 36 Accelerated Missile Defense Tranche 3 space vehicles (July 2026) and the Space Systems Command prototype solicitation for Ground Based Radar Digitization (June 2026) both reflect active investment in digitized sensor networks and integrated fire-control quality data paths. For air-based C4ISR suppliers, this points to near-term demand for interoperable gateways, multi-band SATCOM integration, edge processing aligned with sovereign data constraints, and certification-ready software packages that can be updated frequently under open-architecture constraints rather than tied to long hardware refresh cycles.

Recent Industry Developments

- July 2026: L3Harris received a follow-on contract worth up to USD 499.6 million to support the Missile Defense Agency Flight Test Airborne Sensors program, with ordering extending through September 2036. The award supports airborne instrumentation and sensing used to evaluate missile defense performance, reinforcing demand for high-end missionized aircraft integration and long-term sustainment capacity.

- April 2026: L3Harris secured a second international customer for its Global 6500-based Aeris X airborne early warning and control platform. The additional customer expands the business-jet special mission aircraft pipeline and strengthens an ecosystem of mission-system suppliers focused on modular sensors, communications, and open-architecture integration.

- February 2026: Lockheed Martin was awarded a USD 328.5 million Foreign Military Sales contract for production of IRST21 Legion-ES sensor systems for Taiwan. The deal expands installed base for podded passive sensing and data sharing across fighter fleets, supporting allied interoperability and accelerating demand for integration of high-bandwidth onboard processing and secure datalinks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the air-based C4ISR market covers the value of airborne command, control, communications, computers, intelligence, surveillance, and reconnaissance capabilities used to sense, communicate, process, and support decisions during missions across air platforms.

Scope exclusions: The sizing excludes space-only C4ISR programs and purely ground or naval C4ISR systems that are not installed on an air platform.

Segmentation Overview

- By System Type

- C4 Systems

- Intelligence, Surveillance and Reconnaissance (ISR)

- Electronic Warfare (EW)

- By Platform

- Manned

- Fixed Wing

- Rotary Wing

- Unmanned

- Manned

- By Component

- Hardware

- Software

- By End-user

- Defense Forces

- Civil and Government Agencies

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest OF Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping what gets counted as air based C4ISR and what does not, then building a set of demand signals that can be checked year after year. We leaned on public defense budget documents, procurement and contract award notices, and official program releases to understand spending direction and timing.

For data points, we referred to sources such as defense ministry publications, parliamentary or congressional budget records, aviation and defense regulators, trade and customs statistics for relevant electronics categories, and patent databases for sensing and communications technologies. We also reviewed company filings, investor presentations, press releases, and reputable defense press to cross-check platform plans, upgrade cycles, and integration themes. In a few places, paid subscriptions for company financials, news and financials, defense contracts and tenders, and aircraft and engine level databases were used to speed up verification of public signals. The above list is not exhaustive, and many other public sources were reviewed for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually being procured and installed, how upgrade timing changes during conflicts, and how hardware versus software value splits tend to move on different platforms. We spoke with a mix of system integrators, subsystem suppliers, defense users, and civil or government agencies across the main operating regions so assumptions on adoption, refresh cycles, and pricing could be tightened.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 49% |

| Mid tier: 55% | Functional/Unit leaders: 32% | EMEA: 33% |

| Smaller Players: 14% | Managers: 56% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic together, but anchored on a top-down view that reconstructs the demand pool from defense and agency spending patterns tied to airborne mission needs. In practice, we started from platform activity and modernization priorities, and then translated that into likely C4ISR content by system type and component.

A few key inputs were tracked because they move the market in predictable ways, including fleet mix across manned fixed wing, manned rotary wing, and unmanned platforms, upgrade and mid-life retrofit cycles, procurement timing for ISR and electronic warfare suites, and the shift toward open-architecture integration that changes software content over time. Contracting tempo, electronics lead times, and mission intensity were also used as practical checks on whether year-to-year changes looked reasonable.

Forecasts were produced using scenario analysis supported by trend smoothing on the main drivers, and then refined using expert views on expected budget direction and platform deployment. To corroborate totals, selective bottom-up approximations were done using a sampled set of program values, typical content per platform, and price progression for major subsystems, and then gaps were handled by applying conservative adoption ranges where interview inputs were mixed.

Data Validation & Update Cycle

Outputs were checked against independent signals like defense budget moves, contract award patterns, and known platform upgrade milestones, and then any outliers were reviewed before sign-off. When a region or system type showed a step change that did not align with these signals, respondents were re-contacted to confirm whether it was a real shift or an assumption issue.

Each report is refreshed annually, and interim updates are made when material events happen, such as major procurement announcements, conflict-driven deployment changes, or new program starts. Before delivery, a final pass is completed so the model reflects the latest publicly available updates and the most recent validation notes from primary discussions.

Mordor Intelligence's Air Based C4isr Market Sizing Compared With Other Published Estimates

Published market sizes for air-based C4ISR can vary, even when the topic label looks similar at first glance. Differences usually come from what is counted as airborne scope, how platforms and components are grouped, and how quickly assumptions are refreshed when budgets and programs shift.

The key gaps normally sit in scope and timing choices, such as whether services are included along with hardware and software, whether civil use cases are counted broadly, and whether the estimate is anchored to a single base year versus a longer historical reconstruction. Currency conversion timing and the treatment of multi-year defense programs can also push values apart, especially when contract awards do not translate into deliveries in the same year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.76 B (2026) | |

| Industry Publisher A | USD 1.20 B (2024) | Uses an earlier base year and appears to treat the demand pool as narrower, which can happen when only select military programs or a limited set of airborne subsystems are counted, and then growth is applied forward from that smaller start point. |

| Industry Publisher B | USD 3.50 B (2025) | Includes services and a broader end-use lens in its stated scope, which can raise the value in the start year, and it also uses a longer horizon where slower price progression assumptions can compress near-term growth. |

The table shows a wide spread mainly because the year picked for the starting point and what gets included in scope are not aligned across publications. In Mordor Intelligence's model, the total is built for 2026 with only hardware and software across airborne C4 systems, ISR, and electronic warfare on manned fixed wing, manned rotary wing, and unmanned platforms. When a similar market is instead anchored to an earlier year or expanded to add services and broader use cases, the reported value shifts even if the underlying mission need is similar. By keeping the sizing steps tied to clear platform and procurement signals, the final figure stays traceable and can be repeated when assumptions are updated.

Key Questions Answered in the Report

What is the current value of the Air-based C4ISR market?

The Air-based C4ISR market size stands at USD 3.76 billion in 2026.

How fast is the market expected to grow through 2031?

The market is forecast to expand at a 4.65% CAGR, reaching USD 4.71 billion by 2031.

Which system type leads in revenue and growth?

Intelligence, surveillance and reconnaissance systems held 42.35% share in 2025 and are projected to post the fastest 6.47% CAGR to 2031.

Which region is expanding the quickest?

Asia-Pacific shows the highest growth, advancing at a 5.08% CAGR on the back of large UAV procurements and rising threat perceptions.

What role do open-architecture mandates play?

MOSA and similar standards allow third-party software integration, shifting value toward modular payloads and shortening upgrade cycles.

Who are the key market players?

Lockheed Martin, Northrop Grumman, RTX, L3Harris, and BAE Systems collectively capture about 55% of global revenue.

Page last updated on: