Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 127.75 Billion |

| Market Size (2031) | USD 152.47 Billion |

| Growth Rate (2026 - 2031) | 3.61% CAGR |

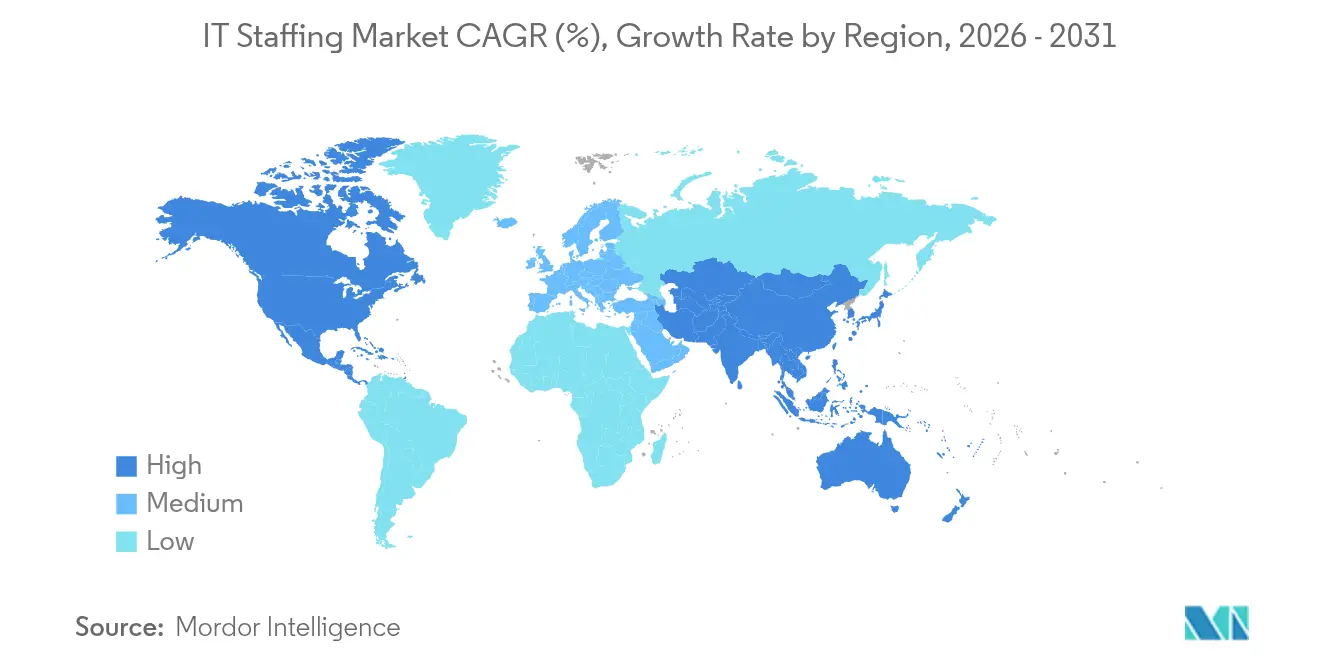

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

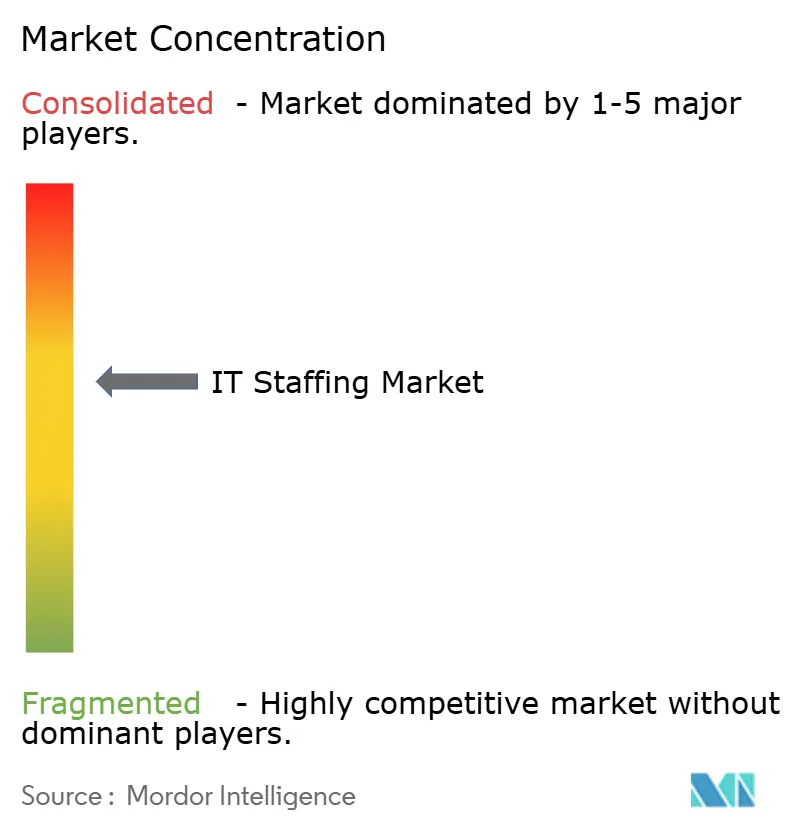

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IT Staffing Market Analysis by Mordor Intelligence

The IT staffing market size is expected to grow from USD 123.30 billion in 2025 to USD 127.75 billion in 2026 and is forecast to reach USD 152.47 billion by 2031 at 3.61% CAGR over 2026-2031. This steady expansion reflects enterprises realigning talent strategies toward specialized skill acquisition rather than volume hiring, a change reinforced by cloud, artificial intelligence, and cybersecurity spending priorities. Temporary and contract engagements remain the dominant hiring mechanism, yet growth is gravitating toward Statement-of-Work models that shift delivery risk to providers. Generative-AI engineering, edge computing, and cyber-resilience needs are reshaping job requisitions, while persistent global skill shortages sustain upward wage pressure. At the same time, vendor consolidation across Global-2000 clients compresses margins for managed service providers but also deepens their wallet share with retained customers.

Key Report Takeaways

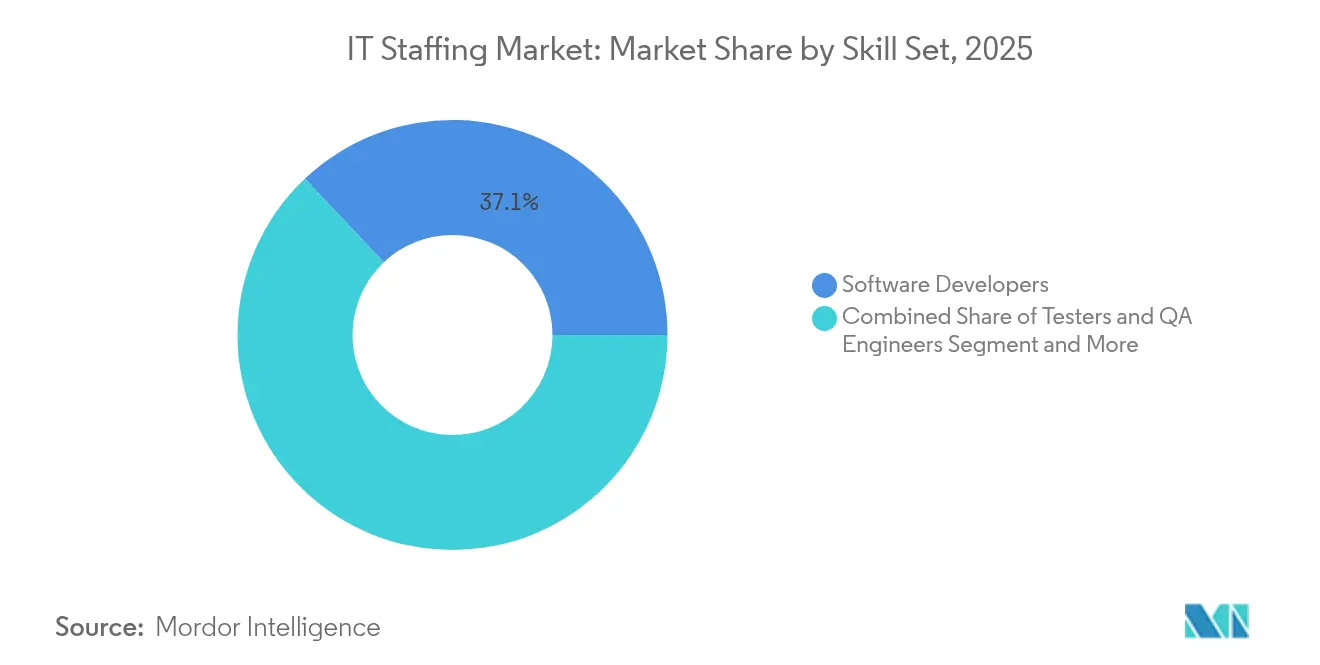

- By skill set, software developers led with 37.05% of IT staffing market share in 2025, while generative-AI roles are forecast to post a 11.75% CAGR through 2031.

- By end-user industry, BFSI held 24.15% of demand in 2025; healthcare IT staffing is projected to expand at a 10.25% CAGR to 2031, the fastest among all verticals.

- By staffing service type, temporary and contract engagements accounted for 63.15% of the IT staffing market size in 2025, yet Statement-of-Work deals are advancing at an 11.10% CAGR.

- By enterprise size, large enterprises controlled 70.80% share of the IT staffing market size in 2025, whereas the SME segment is growing at 8.85% CAGR on the back of cloud-first adoption.

- By geography, North America commanded 44.05% revenue in 2025; Asia-Pacific is scaling at an 8.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IT Staffing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption of AI-, cloud- and IoT-centric projects | +1.2% | Global, North America and Asia-Pacific | Medium term (2-4 years) |

| Remote and hybrid work models | +0.8% | Global, North America and Europe | Short term (≤ 2 years) |

| Cyber-resilience staffing under insurance mandates | +0.9% | Global, North America and EU | Medium term (2-4 years) |

| Post-pandemic digital-budget rebound | +0.6% | Global | Short term (≤ 2 years) |

| Generative-AI supervision roles | +0.7% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Vendor consolidation among Global-2000 clients | +0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of AI-, Cloud- and IoT-Centric Digital-Transformation Projects

Fourteen percent of global tech job postings now demand AI or machine-learning skills, up from 9% a year earlier [1]DHI Group, “As AI Transforms Tech Hiring,” dhigroupinc.com . Cloud migrations call for specialized DevOps engineers and security architects, while edge-computing investments that are projected to reach USD 139.58 billion by 2030 require blended infrastructure-plus-IoT talent. NTT DATA’s program to train 200,000 employees in generative AI further underscores the scale of reskilling underway [2]NTT DATA, “Generative AI Talent Development Framework,” nttdata.com . Interdisciplinary project teams that connect AI algorithms, cloud resources, and device networks are therefore driving sustained expansion in the IT staffing market.

Expansion of Remote and Hybrid Work Models Requiring Distributed Talent

Sixty-five percent of Dell Technologies personnel use formal flexibility arrangements, signaling lasting normalization of location-agnostic hiring. Employers gain access to broader talent pools, yet must navigate cross-border compliance and rising pay parity expectations. ManpowerGroup’s 2025 outlook shows 41% of firms plan to add headcount, with technology roles topping demand charts. Competitive bidding now spans continents, increasing compensation levels and compelling agencies to enhance retention packages that extend beyond salary.

Surging Demand for Cyber-Resilience Staff Driven by Cyber-Insurance Mandates

Eighty-nine percent of organizations anticipate expanding security teams to meet NIS 2 Directive obligations. Insurance carriers require demonstrable controls, lifting needs for security architects, cloud-config auditors, and continuous-monitoring analysts. Data sovereignty laws that localize citizen information add further complexity and spur recruitment of legal-plus-technical hybrid professionals. Given the acute talent shortfall, many firms pursue staff-augmentation contracts to secure expertise without permanent hiring overheads.

Digital-Transformation Budget Rebound Post-Pandemic Fuels Staff-Augmentation Demand

Deferred projects from 2020-2023 are now back on executive roadmaps, placing near-term strain on internal hiring pipelines. ASGN forecasts 20% revenue growth in 2025 by pairing consulting acquisitions with flexible delivery models that promise faster ramp-up. Organizations increasingly sign outcome-based SOW agreements that share delivery risk with providers, reshaping the IT staffing market from pure labor sourcing to value-based capability provision.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global skill shortages in niche technologies | -0.7% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Wage inflation compressing MSP margins | -0.5% | North America and Europe | Medium term (2-4 years) |

| AI-based self-service hiring platforms | -0.4% | Global, early adoption in North America | Long term (≥ 4 years) |

| Tightening data-sovereignty laws | -0.3% | Europe, expanding into Asia-Pacific and the Americas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Global Skill Shortages in Niche Technologies

It is estimates that unresolved digital-skills gaps could cost the global economy by 2034, underscoring structural supply constraints for quantum, advanced AI, and zero-trust security expertise. Universities have not kept curriculum pace, creating multiyear lags before new graduates enter these specializations. The scarcity elevates compensation packages and lengthens project timelines, compelling enterprises to bankroll intensive reskilling initiatives that erode near-term ROI.

Wage Inflation Compressing MSP Bill-Rate Margins

Specialist salaries are rising faster than providers can renegotiate multiyear contracts, particularly in government and highly regulated industries where rate caps are common. Insight Global notes that bill-rate growth trails wage inflation by several points, squeezing gross margins for mid-tier providers [3]Insight Global, “IT Wage Correction 2024,” insightglobal.com . Smaller firms lacking scale are becoming acquisition targets, accelerating consolidation but also reducing competitive pricing pressure in the IT staffing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Skill Set: Generative-AI Roles Reshape Traditional Development Hierarchies

Software developers accounted for 37.05% of IT staffing market share in 2025, reflecting entrenched application modernization projects. Generative-AI engineers are projected to register a 11.75% CAGR through 2031, underscoring growing demand for prompt design, model auditing, and LLM fine-tuning. The IT staffing market size for data and AI engineering is projected to escalate sharply as edge-cloud pipelines scale. Salary corridors signal premium pricing that providers can command when supplying hybrid AI-development expertise.

Traditional testers and QA roles face automation headwinds, pushing many professionals toward AI-enabled verification tools. Systems analysts are pivoting to integration architecture, and network specialists are upskilling in AI-driven threat monitoring. Emerging skills—quantum development, blockchain architecture, and IoT device security—collectively remain a small but rapidly expanding slice of the IT staffing market.

By End-User Industry: Healthcare Digital Mandates Accelerate IT Adoption

BFSI remained the largest adopter with 24.15% share in 2025, driven by open-banking compliance and fintech platform upgrades. Healthcare emerges as the fastest-growing vertical at 10.25% CAGR, propelled by electronic-health-record modernization and AI-assisted diagnostics. The IT staffing market size for healthcare projects is expected to widen as telemedicine and patient-data interoperability standards take hold.

Manufacturing prioritizes smart-factory deployments requiring IoT and predictive-maintenance talent. Retail and e-commerce continue omnichannel build-outs, while public sector agencies earmark cybersecurity and citizen-service digitization budgets. Energy, automotive, and smart-city programs fill the “Other Industries” category, each demanding bespoke skill combinations and feeding diverse pipelines for the IT staffing market.

By Staffing Service Type: Project-Based Models Gain Strategic Prominence

Temporary and contract staffing dominated with 63.15% contribution in 2025, demonstrating enterprise preference for cost-containment flexibility. Statement-of-Work engagements, however, are recording an 11.10% CAGR as clients shift toward outcome accountability. Providers that master project governance and risk management capture premium pricing and greater stickiness in the IT staffing market.

Permanent placement shows muted expansion because rapid technology cycles deter long-term headcount commitments. Managed Service Provider and outsourced models benefit from vendor consolidation, as conglomerates seek fewer, broader suppliers capable of global compliance assurance and performance analytics.

By Enterprise Size: SME Cloud Adoption Drives Specialized Demand

Large enterprises claimed 70.80% of IT staffing market share in 2025, leveraging preferred-supplier frameworks to secure scarce talent. Nonetheless, SMEs are projected to advance at a 8.85% CAGR thanks to turnkey cloud platforms that require implementation support. The IT staffing market size for SMEs is enlarging as these firms invest in cybersecurity hardening and e-commerce integrations.

SME engagements generally favor short, milestone-driven contracts, enabling providers to rotate teams across multiple customers. Large-scale clients continue multi-year transformation initiatives but pressure suppliers on rate optimization, reinforcing the importance of delivery productivity and automation.

Geography Analysis

North America retained 44.05% share in 2025, supported by deep tech ecosystems, large digital budgets, and rigorous security mandates. Continuous visa policy shifts and wage escalation challenge talent availability, prompting more near-shoring to Canada and Latin America. The United States leads demand due to Silicon Valley software projects and Wall Street cloud overhauls, while Canada provides cost-advantaged hubs in Toronto and Montréal.

Asia-Pacific is the fastest-growing region at an 8.15% CAGR, buoyed by India’s IT services scale-up, Japanese reskilling initiatives, and Singapore’s regional headquarters attraction. Managed-services annual contract value in the region rose 32% in 2024 as multinationals diversified sourcing. China’s platform rebound and Korea’s semiconductor R&D add further pull on specialist headcount.

Europe posts stable demand in Germany and the United Kingdom, even as Eastern European destinations evolve from pure cost-arbitrage to niche specialist centers. GDPR compliance maintains high cybersecurity uptake. Middle East and Africa trail but register steady growth; Saudi Arabia’s smart-city projects and South Africa’s English-language service hubs are notable demand pockets. Currency-adjusted wage differentials across these markets shape provider margin strategies within the global IT staffing market.

Regulatory Landscape

Cross-border deployment of IT talent is increasingly shaped by EU-wide labor-mobility and digital compliance initiatives that affect how staffing firms source, screen, and place candidates. In April 2026, the EU adopted Regulation (EU) 2026/1047 establishing the EU Talent Pool, a Union-level platform to match registered third-country jobseekers with vacancies. This adds a formal channel for international recruiting and associated compliance workflows.

Governance around the use of AI in recruiting and workforce management is also tightening. In July 2026, the European Commission published guidelines on transparency obligations under Article 50 of the EU AI Act, with transparency requirements applying from 2 August 2026. That shift increases the need for documented disclosures and controls when staffing providers and clients use AI-enabled tools for candidate interaction, screening, and evaluation. Separately, the EU continued work in 2026 on simplifying implementation through an AI omnibus proposal discussed at the Council level, reinforcing the value of monitorable, auditable hiring and compliance processes for global staffing operations serving European clients.

Value Chain Analysis

The IT staffing value chain begins with talent supply creation and aggregation (universities, reskilling programs, independent professionals, and offshore delivery centers), then moves to sourcing and screening (staffing agencies, digital marketplaces, and AI-enabled matching tools). Compliance and onboarding follow, including background checks, right-to-work validation, payroll and tax, and data-handling controls, before delivery through temporary or contract staffing, MSP programs, and SOW or project-based engagements. Demand is shaped by enterprise IT roadmaps in cloud, AI, and cybersecurity, with large enterprises using preferred-supplier lists and MSPs to rationalize vendor count, while SMEs tend to rely on short, milestone-driven engagements aligned to cloud-first adoption.

Bottlenecks tend to cluster around niche skill availability and time-to-fill, which is driving higher investment in candidate pipelines, nearshore and offshore delivery, and automation in screening and documentation. The market context also reflects a shift from volume staffing to outcome-based models, with temporary and contract engagements at a 63.15% share in 2025 while SOW engagements advance faster. That reinforces the role of project governance, risk ownership, and quality assurance in provider operations. As vendor consolidation among Global-2000 clients progresses, providers that combine compliant global delivery with specialized practices (data and AI engineering, cybersecurity, and cloud) can capture more program share and integrate more deeply into client procurement and workforce planning.

Competitive Landscape

The IT staffing industry shows moderate fragmentation with rising consolidation. TEKsystems generated USD 5.8 billion revenue in 2024, while ASGN, Randstad, and Cognizant’s staffing arms deepen consulting overlaps. Providers differentiate through AI-driven candidate matching, workforce-planning analytics, and automated compliance tools that reduce time-to-fill cycles.

Large MSPs dominate Fortune 500 accounts, yet specialized boutiques carve niches in quantum computing, industrial IoT, and sector-specific AI. Technology-enabled marketplaces threaten to disintermediate traditional agencies by directly connecting employers with vetted freelancers.

Margin compression from wage inflation triggers MandA activity: HeadFirst-Impellam’s merger created an EUR 8 billion spend platform, while System One, GEE Group, and Kelly Services executed smaller capability acquisitions in 2025. Scale economies are now essential for maintaining profitability and investing in proprietary sourcing technology.

IT Staffing Industry Leaders

TEKsystems Inc. (Allegis Group Holdings Inc.)

ASGN Incorporated

Insight Global LLC

Randstad NV

Kforce Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large-scale data center and AI infrastructure buildouts are creating multi-year demand for specialized IT and digital engineering talent across design, cloud platform implementation, cybersecurity, and operational automation. Staffing providers are positioned to supply both build-phase and run-phase roles. In February 2026, Amazon announced a USD 12 billion investment in northwest Louisiana for new data center campuses. In July 2026, Meta expanded its Richland Parish, Louisiana data center investment to USD 50 billion, targeting 5 GW of compute capacity and associated construction and operational hiring. These announcements support ongoing demand for cloud, data, and security skill sets that are typically fulfilled through contract and project-based models.

Regulatory and programmatic changes also create whitespace in compliant, cross-border hiring and governed AI-enabled recruitment. The EU Talent Pool created under Regulation (EU) 2026/1047 in April 2026 provides a formal platform for third-country job matching, which can increase the need for staffing intermediaries to handle immigration-adjacent coordination, credential verification, and localized onboarding. At the same time, EU AI Act transparency obligations applying from 2 August 2026 increase scrutiny of AI used in screening and candidate communications, creating a services opportunity for providers that can embed auditability, human oversight, and documentation into recruiting workflows and MSP or SOW delivery programs.

Recent Industry Developments

- July 2026: Insight Global opened a new 49,000-square-foot Seattle hub at 2323 Elliott to expand its presence in the Pacific Northwest. The facility supports scaling delivery teams and client coverage in a major technology market, aligning with demand for specialized AI, cloud, and enterprise transformation talent.

- June 2026: Insight Global launched IG Labs, a dedicated AI services and products practice focused on operationalizing AI for enterprise clients. This move shifts the company further toward higher-value, project-led delivery models that blend staffing with solution execution capabilities.

- March 2026: ASGN Incorporated closed its acquisition of Quinnox Inc. for USD 290 million, adding digital engineering capabilities and strengthening offshore delivery capacity. The deal supports broader SOW and transformation engagements by combining specialist skills with scalable global delivery.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the IT staffing market is defined as the revenue earned by staffing and recruitment providers from placing IT talent for client projects and roles, including contract, contract-to-hire, and permanent placements, measured in current USD.

Scope exclusions: Outsourced managed services delivery where the provider owns the end-to-end IT outcome (rather than supplying personnel) is excluded.

Segmentation Overview

- By Skill Set

- Software Developers

- Testers and QA Engineers

- Systems Analysts / Business Analysts

- Technical Support Professionals

- Networking and Security Experts

- Data and AI Engineers

- Other Skill Sets

- By End-User Industry

- Telecom

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Manufacturing

- Retail and e-Commerce

- Government and Public Sector

- Other Industries

- By Staffing Service Type

- Temporary / Contract Staffing

- Permanent Placement

- Statement-of-Work (SOW) / Project-based

- Managed Service Provider (MSP) / Outsourced Staffing

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the hiring demand environment and the supply side of staffing services. We reviewed public labor market and macro signals such as the US Bureau of Labor Statistics, Eurostat labor and wage series, and ILOSTAT indicators to understand employment levels, openings, and wage inflation that influence bill rates.

To keep assumptions anchored, we also referenced sources such as OECD digital economy statistics, World Bank macro datasets, and publicly available releases from industry bodies like staffing associations. These inputs were supplemented with company filings, investor presentations, reputable press coverage, and paid subscriptions for company financials and news screening for company-specific trends in IT hiring demand. We also used a patent database to track hiring-related automation themes that could shift recruiter workflows over time. The sources listed here are illustrative only, and many other public and paid references were used for cross-checks and clarification.

Primary Interviews and Surveys

Primary work was used to test what desk signals cannot fully answer, especially billing rate movement, utilization patterns, and the mix shift between contract and permanent placements. We spoke with staffing leaders, delivery managers, and large buyers of IT talent across APAC, EMEA, and the Americas so assumptions could be adjusted for regional hiring cycles and project pipelines.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 20% | APAC: 48% |

| Mid tier: 53% | Functional/Unit leaders: 33% | EMEA: 33% |

| Smaller Players: 20% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

The model begins with a top-down demand pool build that ties IT staffing revenue to the addressable IT labor demand, and then applies staffing penetration and bill-rate logic by region. As the totals are formed, they are checked with selective bottom-up approximations such as sampled bill rate times deployed headcount, supplier revenue roll-ups for key geographies, and channel checks with buyers to confirm what portion is actually fulfilled via staffing firms.

Key inputs that drive the math include IT job openings and placements momentum, average bill-rate and pay-rate spreads, recruiter throughput and time-to-fill trends, utilization rates of contractors, and the mix between contract staffing and permanent placement fees. When detailed splits are missing for smaller countries, reasonable proxies are used based on nearby markets with similar wage levels and hiring patterns, and then validated through interviews.

For forecasting, scenario analysis is used because client IT budgets and project starts can move quickly with macro conditions. Growth paths are set by regional IT spending outlook, wage inflation, and hiring plans shared by buyers, and then reconciled back to historical staffing cycles so the curve stays realistic.

Data Validation & Update Cycle

Outputs are tested using multiple checks so the totals do not rely on a single assumption. We compare implied revenue per deployed worker, regional growth rates, and bill-rate progression against independent labor indicators and against what interviewees report as normal ranges.

If any country or segment shows an unusual jump, the drivers are re-reviewed, and follow-up calls are triggered to confirm whether the shift is real or model-led. Reviews are completed in steps before sign-off so calculation errors and scope misreads are caught early. Reports are refreshed annually, with interim updates when major events occur, and a final pre-delivery pass is done to ensure the newest public data is reflected.

Mordor Intelligence's IT Staffing Market Size Compared With Other Published Estimates

Different published numbers for IT staffing are common because the service line can be interpreted in more than one way. Some estimates blend pure staffing with adjacent outsourced delivery or broader HR services, and others use different currency timing and base years, which changes the converted value.

The biggest gaps usually come from what is counted as staffing revenue, how bill rates are progressed year to year, and whether utilization is treated as stable or cyclical during hiring slowdowns. When contract staffing is sized using labor openings alone, or when permanent placement fees are assumed at a flat share across regions, the final totals tend to drift away from what buyers and suppliers report in practice, which is why managed services delivery is kept outside staffing and revalidation calls are done before finalizing the 2025 value, a discipline followed by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 123.30 B (2025) | |

| Trade Publisher A | USD 69.20 B (2025) | Appears to scope closer to temporary and contract staffing only, and can understate revenue by excluding permanent placement fees and higher-rate specialized roles in cybersecurity and cloud. |

| Global Research Portal B | USD 80.34 B (2024) | Uses a different base year and may blend mixed staffing definitions across regions, with less visibility on bill-rate inflation assumptions and how utilization is normalized after demand dips. |

The spread across sources mostly reflects scope choices and the rate and utilization assumptions that sit under the math. By keeping the unit economics checks visible and tying growth to observable hiring and wage signals, the resulting market size stays traceable to repeatable steps instead of one-time expert judgment.

Key Questions Answered in the Report

What is the projected value of the global IT staffing market by 2031?

The market is forecast to reach USD 152.47 billion by 2031, reflecting a 3.61% CAGR.

Which skill segment is growing fastest in IT staffing?

Generative-AI engineering roles are expanding at a 11.75% CAGR through 2031.

Why are Statement-of-Work engagements gaining traction?

Clients favor outcome accountability and risk sharing, pushing SOW deals to an 11.10% CAGR.

Which region is recording the highest growth in technical staffing demand?

Asia-Pacific leads with an 8.15% CAGR driven by India, Japan, and Southeast Asia.

How are skill shortages affecting provider margins?

Scarcity inflates wages faster than bill-rate adjustments, compressing MSP margins and spurring consolidation.

Page last updated on: