AI In Cold Chain Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

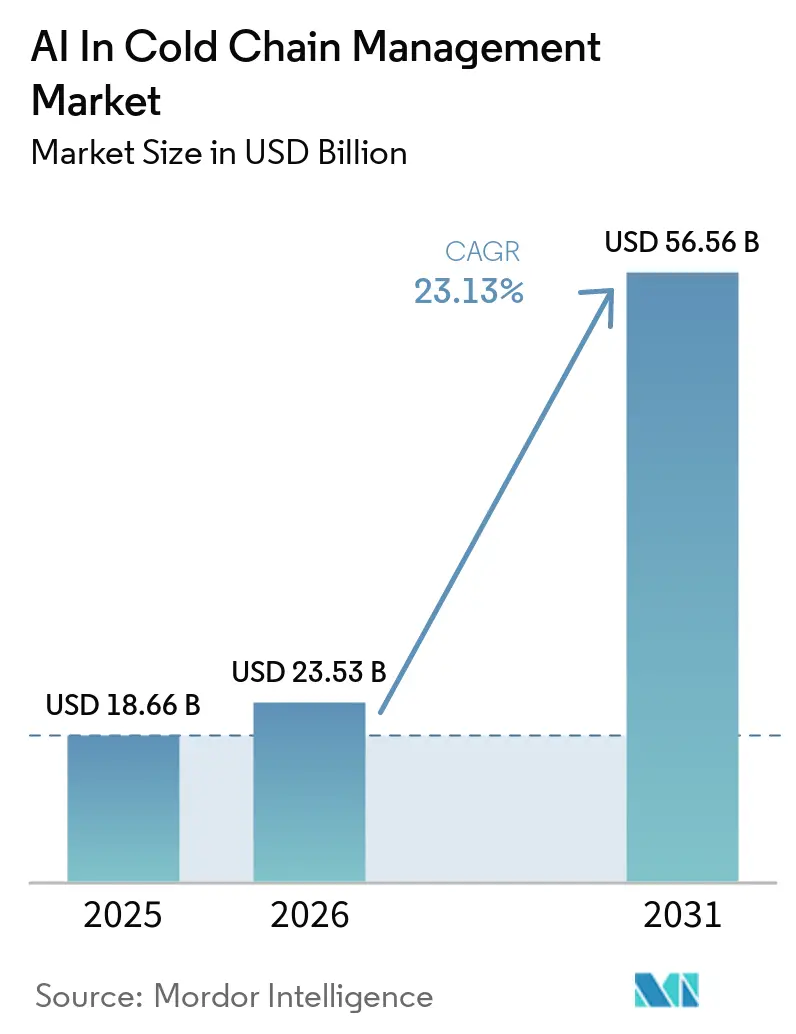

| Market Size (2026) | USD 23.53 Billion |

| Market Size (2031) | USD 56.56 Billion |

| Growth Rate (2026 - 2031) | 23.13% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

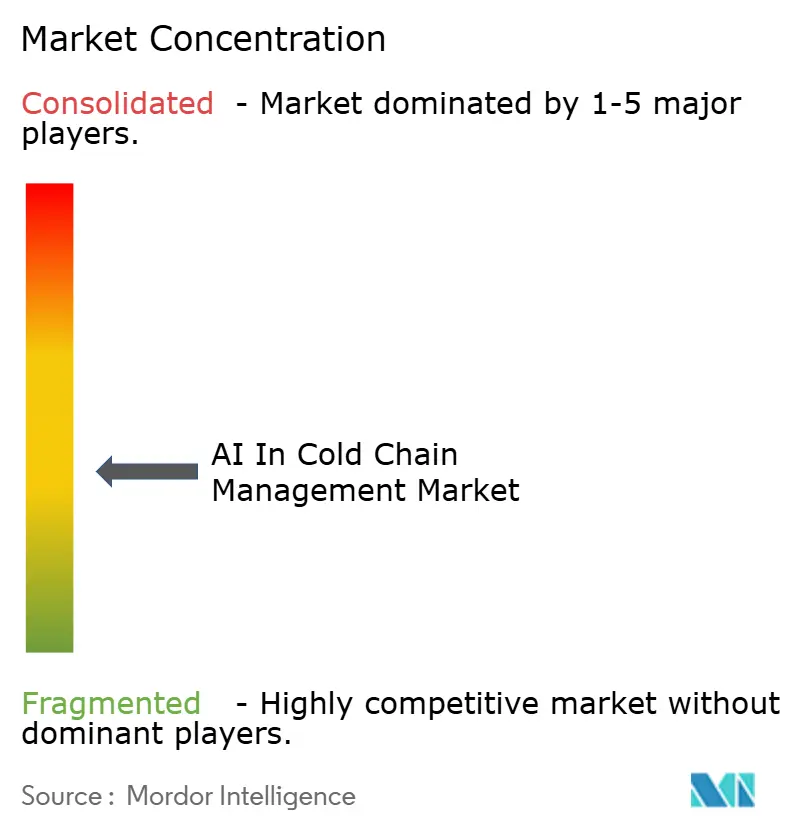

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Cold Chain Management Market Analysis by Mordor Intelligence

The AI In Cold Chain Management Market size is expected to increase from USD 18.66 billion in 2025 to USD 23.53 billion in 2026 and reach USD 56.56 billion by 2031, growing at a CAGR of 23.13% over 2026-2031.

The market is shifting from basic compliance logging to advanced systems that enable early risk detection, failure prediction, and faster actions across storage and transport networks. This transition has accelerated due to regulatory requirements mandating cleaner and more connected data flows during handoffs. Improved compliance infrastructure enhances historical data quality, making AI in cold chain management more effective for predictive modeling and automated exception handling. With increasing costs associated with temperature-sensitive biologics, GLP-1 therapies, and direct-to-patient delivery models, AI is now viewed as a critical tool for protecting margins and ensuring service quality. The pharmaceutical sector faces significant losses annually due to temperature excursions, further emphasizing the importance of AI in loss prevention and operational efficiency.

Key Report Takeaways

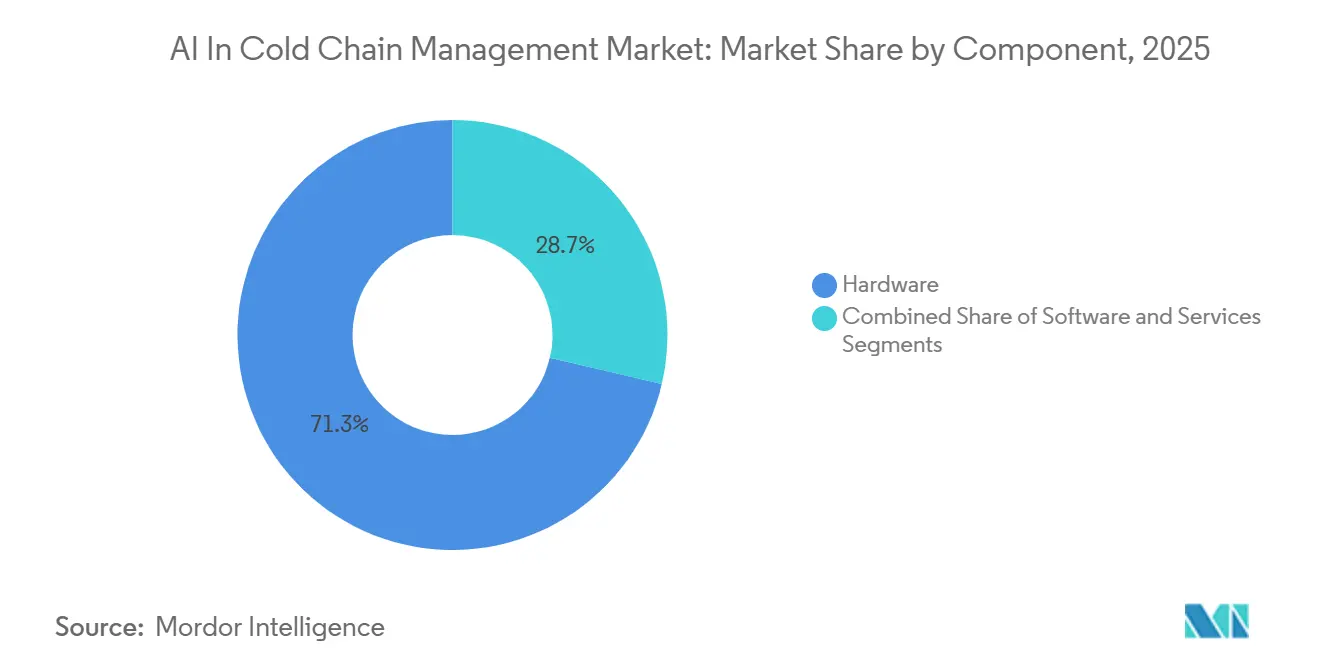

- By component, hardware held 71.34% revenue share in 2025, while software is projected to expand at a 28.55% CAGR through 2031.

- By temperature range, chilled accounted for 61.45% share in 2025, while frozen is forecasted to grow at a 27.79% CAGR during 2026-2031.

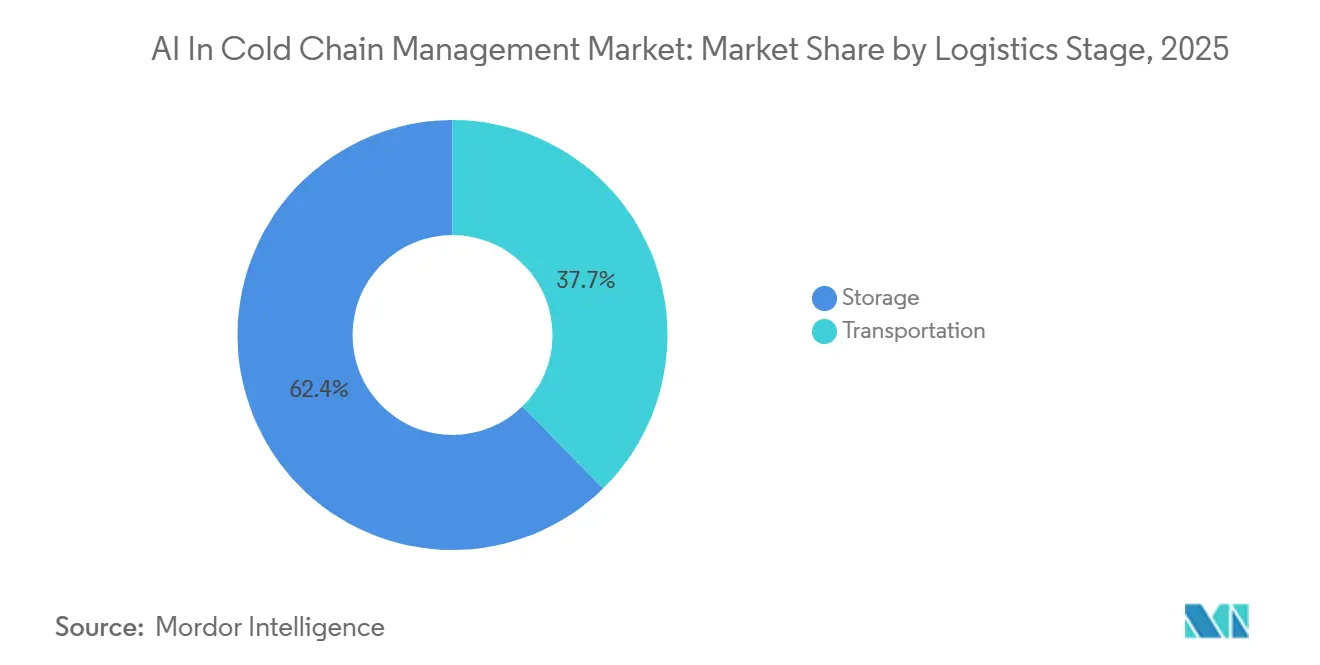

- By the logistics stage, storage captured 62.35% share in 2025, while transportation is expected to advance at a 27.98% CAGR through 2031.

- By end-use industry, food and beverages led with 41.55% share in 2025, while pharmaceuticals and healthcare are projected to grow at a 29.15% CAGR through 2031.

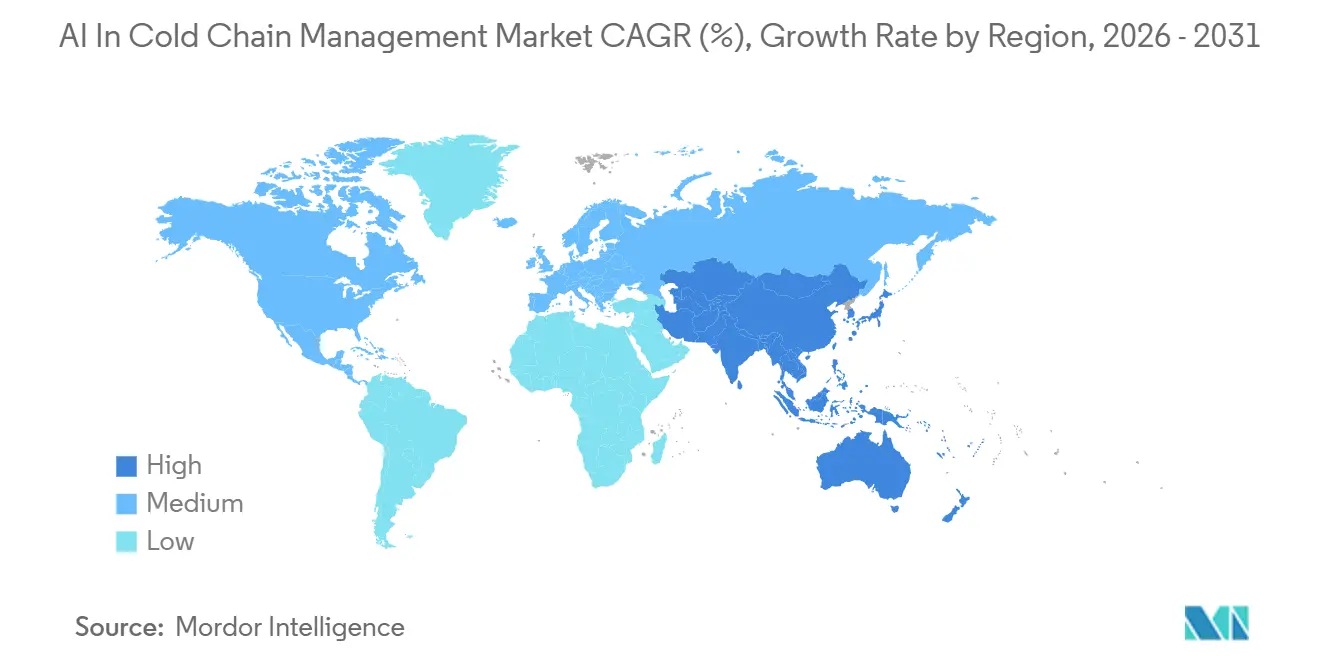

- By geography, North America led with 42.45% share in 2025, while Asia-Pacific is projected to grow at a 29.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Cold Chain Management Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Compliance-led digital traceability adoption | +5.2% | Global, with highest intensity in North America and Europe | Short term (≤ 2 years) |

| Biologics and specialty pharma cold-chain expansion | +5.8% | Global, with early gains in North America, Western Europe, and Japan | Medium term (2-4 years) |

| Food-waste reduction and perishable e-grocery growth | +4.1% | Asia-Pacific core, with spillover to Middle East and Africa and South America | Medium term (2-4 years) |

| Shift from passive logging to real-time predictive monitoring | +4.3% | Global | Short term (≤ 2 years) |

| GLP-1 direct-to-patient cold-chain complexity | +3.7% | North America, Western Europe, South Korea, and Australia | Medium term (2-4 years) |

| Automated product-release decisioning in pharma | +3.0% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compliance-Led Digital Traceability Is Rewriting Cold-Chain IT Architecture

Traceability has evolved from a back-office function to a critical part of daily operations in regulated supply chains. In the AI-driven cold chain management market, serialized identifiers and event records must transition seamlessly across handoffs while ensuring interoperability and accuracy. The FDA's package-level electronic tracing requirements under DSCSA have driven stakeholders toward EPCIS-aligned data exchanges, increasing the demand for systems capable of real-time data processing.[1]U.S. Food and Drug Administration, “Federal Register, Volume 90 Issue 83,” Federal Register, govinfo.gov These event streams, initially compliance-focused, now serve as inputs for predictive models assessing risks across specific routes and facilities, particularly in pharmaceuticals and other cold-chain operations.

Biologics and Specialty Pharma Cold-Chain Expansion Demands Narrow-Range Precision

The growth of biologics, mRNA platforms, and advanced therapies has tightened acceptable temperature ranges, driving the need for continuous intelligence in cold chains. This has increased demand for advanced sensors and software that monitor and interpret conditions to prevent temperature excursions. Enhanced monitoring systems have demonstrated significant operational benefits, such as reducing temperature excursions and improving audit efficiency. With substantial financial losses linked to temperature excursions, precise oversight and timely interventions are critical, aligning AI deployment with the expansion of specialty pharmaceuticals.

Food-Waste Reduction and Perishable E-Grocery Growth Create Parallel AI Demand Curve

Food cold chains face challenges where timing, route quality, and temperature stability directly impact perishability economics. AI and IoT optimizations have shown potential in reducing energy use, transport time, and emissions, improving operational efficiency. These advancements are particularly relevant for e-grocery and short-cycle delivery models, where delays or temperature variations can immediately affect waste, customer satisfaction, and margins. As food operators seek to optimize vehicles, cold storage, and labor, AI adoption is expanding from pilot projects to integrated workflows.

Shift from Passive Logging to Real-Time Predictive Monitoring Restructures Operating Models

The AI in cold chain management market is transitioning from passive data logging to predictive monitoring, enabling proactive interventions. This shift enhances operational stability by addressing issues before they occur, offering a stronger value proposition. Predictive platforms now combine real-time monitoring with modeling to estimate risks across global routes, reducing temperature excursions and unplanned equipment downtime. These advancements not only prevent spoilage and interruptions but also optimize labor and maintenance planning, increasing customer retention through integrated predictive workflows.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High implementation cost and unclear ROI realization | -2.8% | Global, most acute in South America, Middle East and Africa, and Southeast Asia | Short term (≤ 2 years) |

| ERP-WMS-TMS-IoT interoperability gaps | -2.1% | Global, with acute severity in Europe due to legacy ERP exposure | Medium term (2-4 years) |

| Tariff-driven inflation in sensing and edge hardware | -1.6% | North America and South America | Short term (≤ 2 years) |

| Refrigeration and reefer technician shortages | -1.4% | North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation Cost and Unclear ROI Realization Slow Enterprise Adoption

Adopting AI in cold chain management presents significant investment challenges, as enterprises require enterprise-grade hardware, validated software, and integration support. Deploying IoT for a fleet of 1,000 vehicles incurs high costs, making full-scale implementation unaffordable for smaller operators. These smaller companies, which dominate cold-chain operations, often lack the financial capacity to manage extended payback periods. The issue is more pronounced in regulated environments, where compliance with validation, documentation, and audit standards further increases costs. As a result, adoption is often delayed until compliance demands, product risks, or customer requirements make the returns more evident.

ERP-WMS-TMS-IoT Interoperability Gaps Create Systemic Data Blind Spots

System fragmentation significantly impacts the AI in cold chain management market, as data quality, continuity, and standardization are critical for model performance. Many firms cite data privacy and competitive risks as barriers to inter-system data sharing, while mismatched interfaces between platforms drive up integration costs. These gaps create blind spots between warehouse systems, transport networks, and sensor arrays, delaying alerts or providing insufficient context for decision-making. Incomplete event histories reduce forecasting accuracy and complicate exception management. Enterprises operating across multiple regions and legacy systems face additional challenges, slowing integration and limiting AI adoption to specific nodes rather than full network deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominates, Software Compounds Value on Installed Infrastructure

Hardware held 71.34% of AI in the cold chain management market share in 2025, which shows that physical sensing and connectivity remain the first investment layer in most deployments. The hardware base includes temperature sensors, gateways, edge processors, and connectivity modules that make condition data available at shipment, pallet, vehicle, and facility levels. This pattern is consistent with how the AI in the cold chain management market has developed, because no analytics stack can scale if reliable field data is weak or intermittent.

The revenue weight of hardware does not reduce the importance of software, because the fastest compounding value often appears after the sensor estate is already in place. Software is projected to record a 28.55% CAGR during 2026-2031, reflecting rising demand for analytics, automated compliance reporting, route risk scoring, and digital twin tools that extract more value from installed infrastructure.

By Temperature Range: Chilled Segment Anchors Revenue While Frozen Reflects New Therapy Demands

Chilled accounted for 61.45% of AI in cold chain management market size in 2025, making it the largest temperature segment by a clear margin. This range covers a broad mix of products, including insulin, GLP-1 injectables, dairy, fresh produce, and many standard vaccines, so shipment volumes are naturally deeper than they are in more specialized ranges. Frozen is projected to grow at a 27.79% CAGR through 2031, which reflects the stronger need for precise control as advanced pharmaceutical products move through colder environments.

By Logistics Stage: Storage Dominates, Transportation Attracts Disruptive AI Deployment

Storage represented 62.35% of AI in cold chain management market size in 2025, reflecting the concentration of monitoring devices and the longer dwell times seen inside temperature-controlled warehouses. That operating context makes continuous sensing easier to justify because assets remain in a stable environment where alerts, trend analysis, and intervention routines can be tied directly to facility teams. Transportation is forecast to expand at a 27.98% CAGR through 2031, which makes it the faster-moving logistics stage despite storage’s larger current base. The reason is straightforward, because in-transit conditions create more variability from route disruption, last-mile delays, handling quality, reefer performance, and multimodal exposure.

By End-use Industry: Food and Beverages Leads by Volume, Pharma Leads by Value Intensity

Food and beverages held 41.55% of AI in cold chain management market size in 2025, which reflects the sheer scale and frequency of refrigerated movement across produce, dairy, prepared foods, and frozen categories. Pharmaceuticals and healthcare is projected to grow at a 29.15% CAGR through 2031, which makes it the fastest-growing end-use segment in the AI in cold chain management market. This reflects the growing share of biologics, specialty injectables, advanced therapies, and direct-to-patient distribution models that raise the cost of handling failure.

Geography Analysis

In 2025, North America accounted for 42.45% of the AI-driven cold chain management market share, securing its position as the leading revenue contributor. This dominance is driven by the region's advanced pharmaceutical distribution systems, strong cold logistics infrastructure, and early regulatory initiatives that have expedited advancements in digital traceability and monitoring. The implementation of DSCSA has played a pivotal role in this market by prioritizing data interoperability and package-level traceability in daily operations. Phased compliance deadlines for DSCSA, extending through November 2026 for smaller dispensers, continue to drive procurement activities and system upgrades across pharmaceutical distribution networks. Additionally, North America's significant volume of temperature-sensitive pharmaceutical flows has facilitated the early adoption of predictive monitoring, validated data capture, and enhanced service standards in last-mile delivery operations.

Asia-Pacific is projected to achieve the highest growth rate in the AI-driven cold chain management market, with a CAGR of 29.67% through 2031. China leads in scale, while India represents a key growth opportunity, as both markets combine substantial perishable flows with significant potential for digital transformation. The region's growth is supported by increasing food distribution demands, the expansion of refrigerated logistics networks, and the need to reduce losses in temperature-sensitive supply chains. Asia-Pacific also presents a substantial opportunity for vendors offering low-integration solutions, as many operators are transitioning from basic visibility to proactive prediction and intervention. This creates a dual growth scenario, with immediate demand for hardware and long-term potential for software enhancements, particularly in areas where cold-chain modernization efforts are already underway.

Competitive Landscape

The AI in cold chain management market remains moderately fragmented, with no single player dominating the global landscape across hardware, software, and managed services. Competition is divided between niche cold-chain monitoring firms and expansive IoT platform providers. As a result, vendors often differentiate themselves through compliance strength, sensing quality, depth of analytics, and integration capabilities. Companies like Controlant, Sensitech, Tive, Roambee, and SpotSee are prominent in specialized monitoring. In contrast, broader platforms such as Samsara and Wiliot leverage stronger ecosystem narratives and data scale. This competitive landscape in the AI in cold chain management market underscores that customers prioritize not just device accuracy, but also the actionable insights derived from data, reporting, and workflow decisions. Consequently, attributes like technical breadth, ease of deployment, and audit readiness hold equal weight to raw monitoring performance.

Recent strategic developments in the AI in cold chain management market highlight a trend where vendors are bridging the gap between sensing and operational decision-making. For instance, ELPRO’s introduction of elproPREDICT in September 2024 marked a shift from traditional historical monitoring to probability-based prediction across various lanes. Similarly, Wiliot’s launch of its Gen3 IoT Pixel in January 2026 reflects this trend, as its battery-free sensing technology reduces deployment challenges while enhancing the economic feasibility of item-level visibility at scale. Adding to the competitive dynamics, Copeland introduced its GO Real-Time GL and GL XL cargo trackers in April 2026. These trackers, featuring global 4G LTE connectivity, provide monitoring across temperature, humidity, movement, and security, signaling Copeland's strategic focus on comprehensive cold chain solutions.

AI In Cold Chain Management Industry Leaders

ELPRO-BUCHS AG

Zebra Technologies

Emerson

Veeva Systems

testo se & co. kgaa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Copeland has introduced its GO Real-Time GL and GL XL cargo trackers, featuring global 4G LTE connectivity. These devices enable comprehensive monitoring of temperature, humidity, movement, and security, and are integrated with the Oversight360 AI analytics cloud for enhanced operational insights.

- April 2026: Wiliot and Velociti have formed a strategic partnership to scale the implementation of Physical AI across numerous U.S. distribution centers. Leveraging completed deployments at 500 locations, including grocery, logistics, and postal environments, the collaboration aims to enhance ambient IoT cold-chain monitoring capabilities.

- March 2026: The EMA has approved an update to Wegovy's label, allowing controlled-temperature delivery at up to 30°C for 48 hours. This makes Wegovy the first GLP-1 weight-loss therapy in Europe to provide last-mile temperature flexibility.

Global AI In Cold Chain Management Market Report Scope

As per the scope of the report, AI in cold chain management is the use of machine learning algorithms and predictive analytics to monitor, optimize, and secure temperature-sensitive supply chains. It shifts logistics from a reactive process to a proactive one by predicting failures, automating environmental controls, and preventing product spoilage.

The AI in cold chain management market is segmented by component, temperature range, logistics stage, end-use industry, and geography. By component, the market includes hardware, software, and services. By temperature range, the market is segmented into chilled, frozen, and deep-frozen & cryogenic. By logistics stage, the market is categorized into storage and transportation. By end-use industry, the market is segmented into food and beverages, pharmaceuticals and healthcare, chemicals, agriculture and horticulture, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Hardware |

| Software |

| Services |

| Chilled |

| Frozen |

| Deep-frozen and cryogenic |

| Storage |

| Transportation |

| Food and Beverages |

| Pharmaceuticals and Healthcare |

| Chemicals |

| Agriculture and Horticulture |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Temperature Range | Chilled | |

| Frozen | ||

| Deep-frozen and cryogenic | ||

| By Logistics Stage | Storage | |

| Transportation | ||

| By End-use Industry | Food and Beverages | |

| Pharmaceuticals and Healthcare | ||

| Chemicals | ||

| Agriculture and Horticulture | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the AI in cold chain management space?

The AI in cold chain management market size stands at USD 23.53 billion in 2026 and is forecast to reach USD 59.56 billion by 2031 at a 26.13% CAGR.

Which component generates the most revenue today?

Hardware leads the revenue mix, with a 71.34% share in 2025, because sensor networks, gateways, and edge devices remain the starting point for most deployments.

Which part of the value chain is growing fastest?

Transportation is the fastest-growing logistics stage, projected to expand at a 27.98% CAGR through 2031, driven by in-transit tracking, route optimization, and direct-to-patient delivery complexity.

Why is pharma becoming such a strong demand driver?

Pharmaceuticals and healthcare is projected to grow at a 29.15% CAGR through 2031, supported by biologics, specialty therapies, and the high cost of temperature excursions.

Which region leads adoption, and which region is growing fastest?

North America led with 42.45% share in 2025, while Asia-Pacific is expected to grow fastest at a 29.67% CAGR through 2031.

What is the main barrier to wider adoption?

The biggest barriers are high implementation cost and system interoperability gaps, especially when companies must connect ERP, WMS, TMS, and IoT data into one reliable operating flow.

Page last updated on: