Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

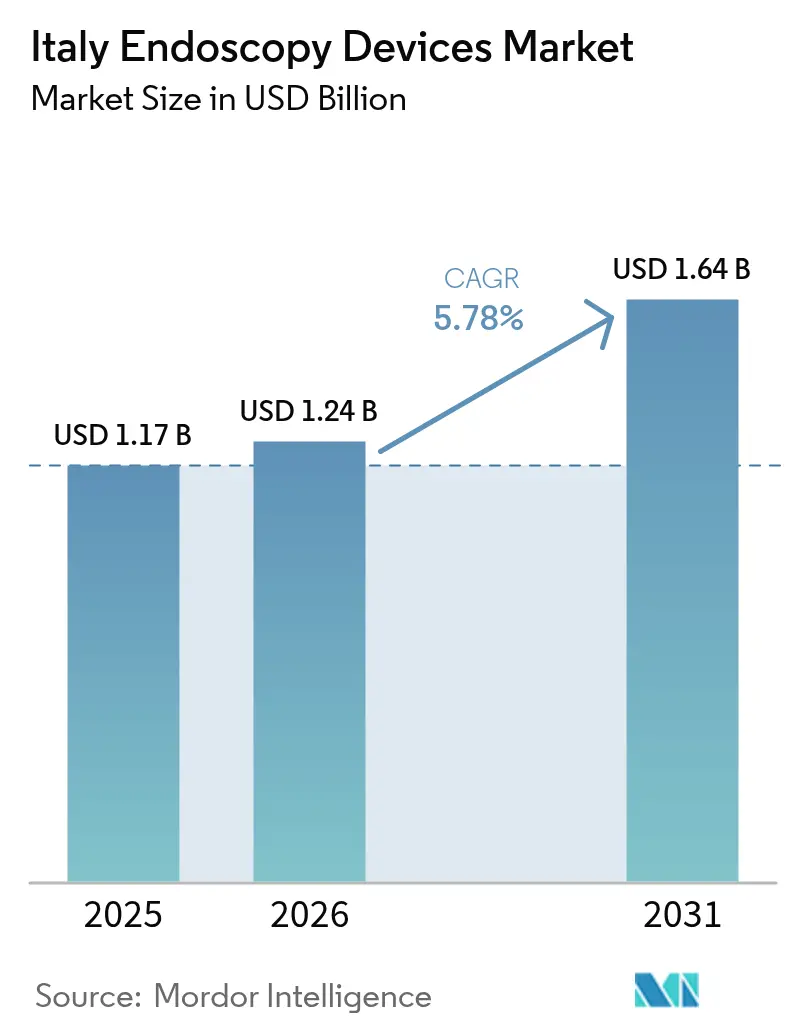

| Base Year Market Size (2025) | USD 1.17 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.64 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Endoscopy Devices Market Analysis by Mordor Intelligence

The Italy endoscopy devices market size is expected to grow from USD 1.17 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 1.64 billion by 2031 at 5.78% CAGR over 2026-2031. Momentum stems from a confluence of rising gastrointestinal disease incidence, wider clinical acceptance of artificial-intelligence-enabled imaging, and policy support that rewards minimally invasive approaches. Demand accelerates further as day-surgery centers multiply, giving providers cost-effective settings for routine diagnostic and therapeutic endoscopy. Meanwhile, single-use accessories gain traction in response to stringent reprocessing rules under the European Medical Device Regulation (MDR) and heightened patient safety expectations. Economic pressures and uneven staffing conditions in smaller or southern hospitals temper growth but have not derailed the broader upward trajectory.

Key Report Takeaways

- By product type, Endoscopes led with 37.40% of Italy Endoscopy Devices market share in 2025, while Accessories & Consumables are projected to expand at a 13% CAGR through 2031.

- By application, Gastroenterology accounted for 55.30% share of the Italy Endoscopy Devices market size in 2025; Bariatric & Metabolic Surgery is advancing at a 11.7% CAGR to 2031.

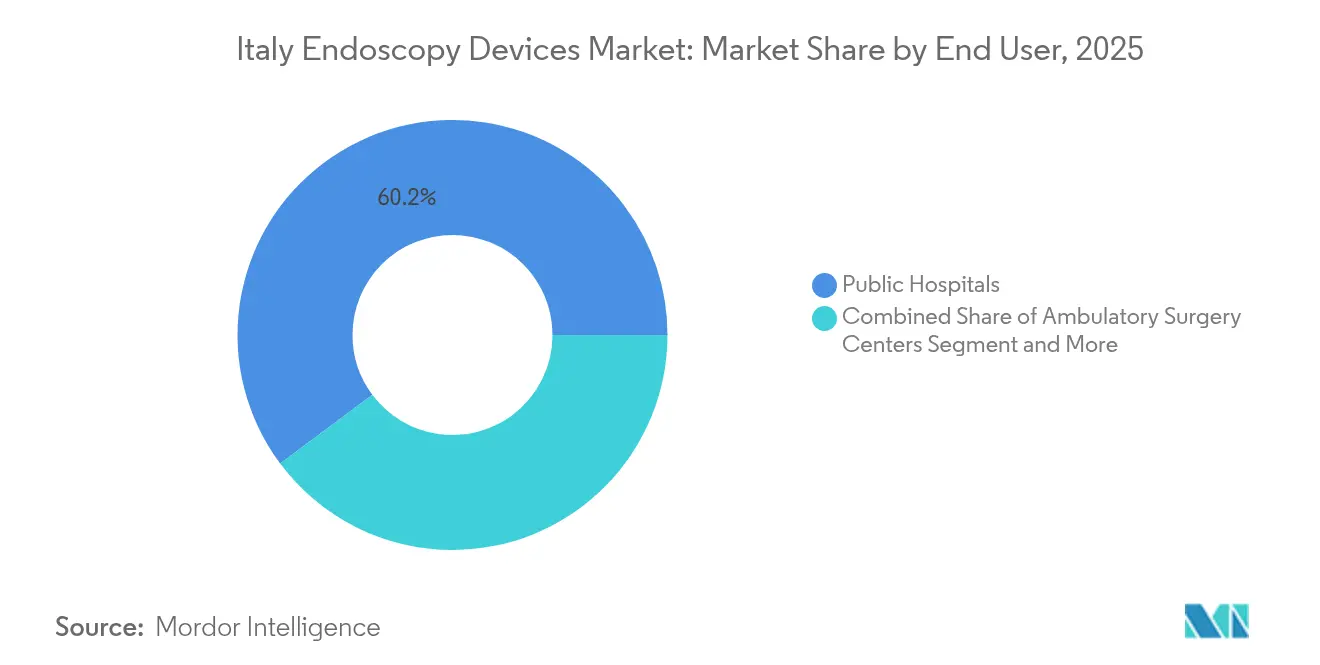

- By end user, Public Hospitals held 60.20% of the Italy Endoscopy Devices market in 2025; Ambulatory Surgery Centers record the highest projected CAGR at 9.3% through 2031.

- By hygiene, Reusable Endoscopes remained dominant with 81.10% share in 2025, but Single-Use Endoscopes are progressing at a 12.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Gastrointestinal Diseases Coupled with Growing Aging Population | +1.8% | National, with higher prevalence in Northern Italy | Long term (≥ 4 years) |

| Advancements in Endoscopic Technologies | +1.5% | National, with early adoption in major urban centers (Milan, Rome, Turin) | Medium term (2-4 years) |

| Expansion of Day-Surgery Centers Accelerates Flexible Endoscope Adoption | +0.9% | National, with concentration in Northern and Central Italy | Medium term (2-4 years) |

| Growing Awareness and Patient Preference for Minimally Invasive Procedures | +0.7% | National | Short term (≤ 2 years) |

| Improved SSN Reimbursement for Advanced Therapeutic Endoscopy | +0.6% | National, with regional variations based on healthcare budget allocation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Gastrointestinal Diseases Coupled with Growing Aging Population

Italy’s inflammatory bowel disease prevalence reached 218.3 cases per 100,000 residents in 2025, raising therapeutic endoscopy demand. Hospitalization persists at 16.5% for IBD patients, and cumulative six-year surgery risk remains high at 36% for Crohn’s disease and 20% for ulcerative colitis. Northern regions, with more specialty centers, therefore buy advanced imaging towers and high-definition flexible scopes to improve early detection and reduce surgical conversions. An older demographic intensifies procedure volumes for colorectal cancer screening, upper GI bleeding management, and chronic pancreatitis assessment, supporting multi-year equipment replacement budgets.

Advancements in Endoscopic Technologies

Cloud-based artificial intelligence now augments routine colonoscopy, Barrett’s Esophagus surveillance, and ulcerative colitis scoring. Olympus secured CE approval for CADDIE, CADU, and SMARTIBD in 2024, with Italian pilot deployments preceding the 2025 commercial rollout[1]Olympus Europa SE & Co. KG, “Olympus Announces CE Approval for Three Cloud-based AI Medical Devices,” olympus-europa.com. AI engines raise adenoma detection rates and standardize quality across hospitals with uneven specialist density. Integrated cloud analytics also streamline workflow documentation, easing MDR compliance and accelerating purchasing decisions for next-generation video processors.

Expansion of Day-Surgery Centers Accelerates Flexible Endoscope Adoption

Procedural migration from inpatient to ambulatory settings continues as day-surgery centers report fewer unplanned hospital returns—10.6 per 1,000 screening colonoscopies—than hospital outpatient departments. Northern and central provinces lead in opening such facilities, prompting demand for portable endoscopy towers, battery-powered insufflators, and slim flexible scopes compatible with lean reprocessing rooms. Device makers respond with compact carts and all-in-one visualization units that cut setup time and improve room turnover.

Growing Awareness and Patient Preference for Minimally Invasive Procedures

Public campaigns highlight faster recovery and lower complication profiles of endoscopic solutions. Interest peaks around bariatric alternatives: Italian data show 90% of Endoscopic Sleeve Gastroplasty recipients achieve ≥10% total body-weight loss within six months while also improving liver histology[2]Springer, “Economic Impact of RefluxStop in Italy,” link.springer.com. Similar sentiments push adoption of endoscopic anti-reflux options and third-space endoscopic myotomies, supporting sales of therapeutic accessories such as suturing systems, hemostatic powders, and bipolar energy probes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced equipment | -0.8% | Small hospitals, especially South | Medium term (2-4 years) |

| Shortage of trained endoscopy support staff | -0.6% | National, acute in South | Long term (≥ 4 years) |

| Economic and budget constraints | -0.5% | Varies by regional health fund | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Endoscopy Equipment

Price tags for AI-ready 4K towers often exceed EUR 200,000 (USD 226,597). Smaller clinics defer upgrades, extending depreciation cycles past manufacturer recommendations. MDR compliance adds certification expenses that funnel into end-user list prices. Vendors increasingly pitch leasing or pay-per-procedure plans to accelerate refresh decisions among cost-constrained buyers.

Shortage of Trained Endoscopy Support Staff in Hospitals

A national survey found a median six nurses per unit and revealed that 19% of centers disinfect rather than sterilize reusable scopes, while 23% cannot trace reprocessing records. Staffing shortages curb procedure slots and raise contamination risk, prompting hospitals to trial single-use duodenoscopes to minimize reprocessing burden. Southern regions face the steepest recruitment gaps, reinforcing geographic imbalances in service capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Outpace Core Equipment

The Accessories & Consumables category will climb at a 13% CAGR through 2031, outstripping capital equipment as infection-control mandates spur adoption of disposable biopsy forceps, snares, and valves. Single-use injectors and retrieval nets lower cross-contamination risk and expedite turnaround in facilities with limited washer-disinfector capacity. Endoscopes maintained 37.40% Italy Endoscopy Devices market share during 2025, anchored by high-definition flexible colonoscopes and gastroscopes from Olympus and Fujifilm. Video systems increasingly embed AI to flag lesions in real time, enhancing first-pass diagnostic accuracy.

Operative devices also witness innovations, notably bipolar energy platforms and controlled CO₂ insufflation pumps that facilitate advanced resections. The accessories boom moderates initial capital outlays; providers prioritize high-throughput consumables that boost revenue per procedure while avoiding large-ticket purchases. Bioplastic-based handles in single-use scopes illustrate how vendors couple infection control with sustainability concerns.

By Application: Bariatric Procedures Drive Specialized Innovation

Gastroenterology remained the backbone with 55.30% share of Italy Endoscopy Devices market size in 2025, underpinned by colorectal cancer screening and ulcerative colitis monitoring. AI-assisted polyp detection improves adenoma recognition, which in turn reinforces demand for large-channel colonoscopes compatible with therapeutic accessories. Bariatric & Metabolic Surgery is pacing the field at a 11.7% CAGR as ESG gains payer backing and patient acceptance. The Italy Endoscopy Devices market benefits from specialized suturing devices and intragastric balloon systems aimed at weight management.

Pulmonology gains ground thanks to flexible transbronchial needle biopsies that sample peripheral lung lesions, aided by articulating sheaths and electromagnetic navigation. Urology and gynecology segments adopt narrow-band imaging cystoscopes and hysteroscopes that enhance pathology detection. Orthopedic and ENT specialties experiment with micro-endoscopes for outpatient arthroscopy and laryngoscopy, broadening the Italy endoscopy devices market user base. Neurology remains nascent but attracts investments in 3D visualization platforms for minimally invasive spine procedures.

By End User: Ambulatory Centers Reshape Procedure Economics

Public Hospitals leveraged their SSN mandate to collect 60.20% Italy Endoscopy Devices market share in 2025, relying on volume contracts and teaching missions to justify procurement of integrated suites that blend endoscopic ultrasound with fluoroscopy. Ambulatory Surgery Centers expand at 9.3% CAGR as evidence shows only 10.6 unplanned visits per 1,000 screening colonoscopies compared with higher rates in hospital departments. Compact towers, integrated cooling, and simplified cabling appeal to ASC administrators mindful of room constraints.

Private Hospitals and specialty clinics pursue premium offerings, such as AI-enhanced Barrett’s Esophagus surveillance, to differentiate and capture privately insured patients. Office-based physician practices grow slowly but represent a beachhead for ultra-portable systems that connect to tablets. This diffusion of sites underpins consistent growth in the Italy endoscopy devices market by broadening access and accelerating repeat procedure cycles.

By Hygiene: Single-Use Revolution Transforms Infection Control

Reusable scopes still command 81.10% share, yet single-use devices accelerate at a 12.1% CAGR as providers grapple with MDR-driven traceability audits and workforce shortages. A Delphi consensus led by Italian experts recommended single-use bronchoscopy for immunocompromised patients and high-risk duodenoscopy. Early adopters cite reduced turnaround time and elimination of biofilm-associated outbreaks. Ambu reported 13.8% growth in its Endoscopy Solutions unit for 2023/24 on surging single-use scope demand.

Environmental concerns prompt suppliers to introduce sugarcane-derived bioplastics and recyclable packaging. Some hospitals run hybrid fleets, reserving disposable scopes for emergency after-hours or bronchoscopy in intensive care units while maintaining reusable fleets for routine GI work. The Italy Endoscopy Devices industry is thus witnessing parallel procurement streams that balance infection risk, cost, and sustainability objectives.

Geography Analysis

Northern Italy accounts for the lion’s share of procedural volume and routinely installs the newest AI-enabled systems. A nationwide audit showed 15% of southern centers lacked recovery rooms and 45% lacked segregated clean-dirty reprocessing areas, compared with far lower non-compliance rates in the North. Consequently, the Italy endoscopy devices market in Lombardy and Emilia-Romagna skews toward premium 4K visualization platforms, whereas Campania and Calabria emphasize cost-effective refurbishment and single-use options.

Urban hubs such as Milan, Rome, and Turin act as test beds for Olympus’ Intelligent Endoscopy Ecosystem, given their concentration of tertiary hospitals and research partnerships. Lombardy’s Pancreas Unit Network set unified diagnostic pathways for pancreatic tumors, triggering orders for echoendoscopes and fine-needle biopsy kits. Standardized metrics encourage peer benchmarking, spurring continuous equipment upgrades across the regional network.

Day-surgery centers proliferate more rapidly in northern and central provinces, tilting demand toward portable towers. Regional budget disparities remain, but some southern regions adopt leasing models or EU-funded modernization funds to bridge the gap. Vendors now craft tiered portfolios, positioning AI-ready processors for affluent northern buyers and robust HD systems for cost-sensitive southern hospitals, thereby sustaining nationwide expansion of the Italy endoscopy devices market.

Competitive Landscape

The sector shows moderate concentration. Fujifilm reinforced its local presence by establishing FUJIFILM Healthcare Italia S.p.A. in 2024 to capture a larger hospital installed base[3]Fujifilm, “Fujifilm Healthcare Italia S.p.A. Announcement,” fujifilm.com. Boston Scientific expands therapeutic accessory breadth with single-use duodenoscopes and biopsy tools and reported endoscopy segment growth in its 2024 report.

Strategic alliances multiply: Medtronic’s 2025 distribution deal with Dragonfly Endoscopy augments its pancreaticobiliary offering. Cosmo Pharmaceuticals collaborates on AI algorithms that overlay real-time detection on Medtronic scopes, illustrating cross-company synergies. Local start-up Endostart raised EUR 8.2 million to commercialize completion-assist devices that reduce incomplete colonoscopies, carving a niche beside dominant multinationals.

European MDR enforcement raises barriers; companies able to certify swiftly gain time-to-market advantages. Contract manufacturers such as Phoenix, newly acquired by Arterex in January 2025, expand domestic supply capacity for specialized molded components. Collectively these moves intensify competition on innovation rather than price, sustaining premium ASPs across the Italy endoscopy devices market.

Italy Endoscopy Devices Industry Leaders

Boston Scientific Corporation

Medtronic PLC

Olympus Corporation

Karl Storz SE & Co. KG

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Arterex acquired the Italian CDMO Phoenix, expanding its capabilities in specialized medical device components relevant to the endoscopy sector.

- October 2024: Olympus received CE approval for three cloud-based AI medical devices—CADDIE, CADU, and SMARTIBD—with launch slated for 2025.

Italy Endoscopy Devices Market Report Scope

As per the scope of the report, endoscope devices are minimally invasive and can be inserted into natural openings of the body, in order to observe an internal organ or a tissue in detail. Endoscopic surgeries are performed for imaging procedures and minor surgeries.

The Italy endoscopy devices market is segmented by type of device (endoscopy device (rigid endoscope, flexible endoscopes, capsule endoscope, robot assisted endoscope), endoscopic operative device, and visualization equipment) and application (gastroenterology, pulmonology, orthopedic surgery, cardiology, ENT surgery, neurology, and other applications). The report offers the value (in USD million) for the above segments.

By Product Type

| Endoscopes | Flexible Endoscopes |

| Rigid Endoscopes | |

| Capsule Endoscopes | |

| Robot-Assisted Endoscopes | |

| Disposable (Single-Use) Endoscopes | |

| Visualization Systems | Camera Heads |

| Light Sources | |

| Video Processors | |

| Monitors & Displays | |

| Data Recorders & Storage | |

| Endoscopy Operative Devices | Energy Systems |

| Insufflators & Suction Pumps | |

| Endoscopic Staplers & Suturing Devices | |

| Retrieval Devices | |

| Fluid Management Systems | |

| Accessories & Consumables |

By Application

| Gastroenterology |

| Pulmonology |

| Urology |

| Gynecology |

| Orthopedic Surgery (Arthroscopy) |

| Cardiology |

| ENT Surgery |

| Neurology |

| Bariatric & Metabolic Surgery |

| Other Applications |

By End User

| Public Hospitals |

| Private Hospitals & Specialty Clinics |

| Ambulatory Surgery Centers |

| Office-Based Physician Settings |

By Hygiene

| Reusable Endoscopes |

| Single-Use Endoscopes |

| By Product Type | Endoscopes | Flexible Endoscopes |

| Rigid Endoscopes | ||

| Capsule Endoscopes | ||

| Robot-Assisted Endoscopes | ||

| Disposable (Single-Use) Endoscopes | ||

| Visualization Systems | Camera Heads | |

| Light Sources | ||

| Video Processors | ||

| Monitors & Displays | ||

| Data Recorders & Storage | ||

| Endoscopy Operative Devices | Energy Systems | |

| Insufflators & Suction Pumps | ||

| Endoscopic Staplers & Suturing Devices | ||

| Retrieval Devices | ||

| Fluid Management Systems | ||

| Accessories & Consumables | ||

| By Application | Gastroenterology | |

| Pulmonology | ||

| Urology | ||

| Gynecology | ||

| Orthopedic Surgery (Arthroscopy) | ||

| Cardiology | ||

| ENT Surgery | ||

| Neurology | ||

| Bariatric & Metabolic Surgery | ||

| Other Applications | ||

| By End User | Public Hospitals | |

| Private Hospitals & Specialty Clinics | ||

| Ambulatory Surgery Centers | ||

| Office-Based Physician Settings | ||

| By Hygiene | Reusable Endoscopes | |

| Single-Use Endoscopes | ||

Key Questions Answered in the Report

What is the current size of the Italy endoscopy devices market?

The Italy Endoscopy Devices market size stands at USD 1.24 billion in 2026.

How fast is the market expected to grow?

It is projected to advance at a 5.78% CAGR, reaching USD 1.64 billion by 2031.

Which product segment is growing the fastest?

Accessories & Consumables are expanding at a 13% CAGR due to heightened infection-control requirements.

Why are Ambulatory Surgery Centers important for future growth?

ASCs deliver lower unplanned hospital visit rates, driving a 9.3% CAGR in endoscopy device demand for these settings.

How significant is single-use endoscopy adoption in Italy?

Single-Use Endoscopes presently grow at a 12.1% CAGR as hospitals address reprocessing challenges and MDR compliance.

Page last updated on: