Market Overview

| Study Period | 2021 - 2031 |

|---|---|

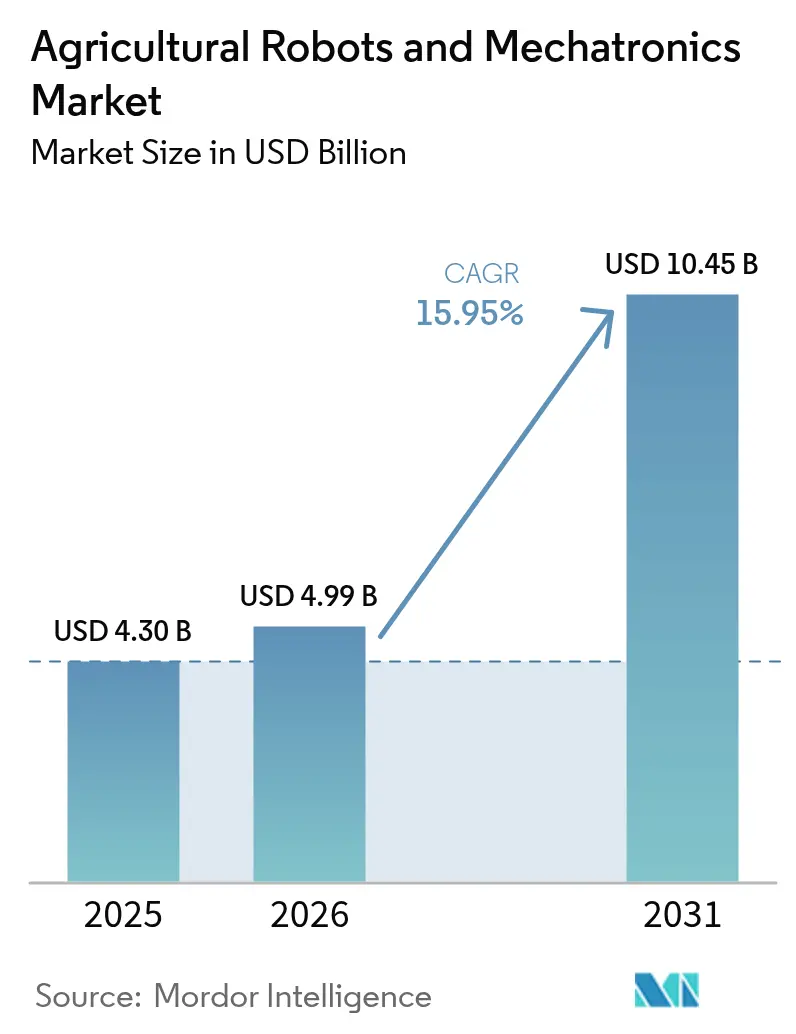

| Market Size (2026) | USD 4.99 Billion |

| Market Size (2031) | USD 10.45 Billion |

| Growth Rate (2026 - 2031) | 15.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Robots And Mechatronics Market Analysis by Mordor Intelligence

The agricultural robots and mechatronics market size was valued at USD 4.30 billion in 2025 and estimated to grow from USD 4.99 billion in 2026 to reach USD 10.45 billion by 2031, at a CAGR of 15.95% during the forecast period (2026-2031). Persistent labor shortages, tightening environmental rules, and falling sensor prices are converting autonomy from an option to a necessity. Precision crop-level interventions that cut chemical inputs by up to 40% are becoming the new standard, while bundled software and data services are strengthening recurring-revenue streams. Regional specialists that focus on weed-laser, drone spraying, and livestock robots are exploiting white spaces that large original equipment manufacturers leave open. Intensifying competition is anticipated to accelerate technology cost declines below 15% per year, raising adoption among mid-size farms that historically lacked capital access.

Key Report Takeaways

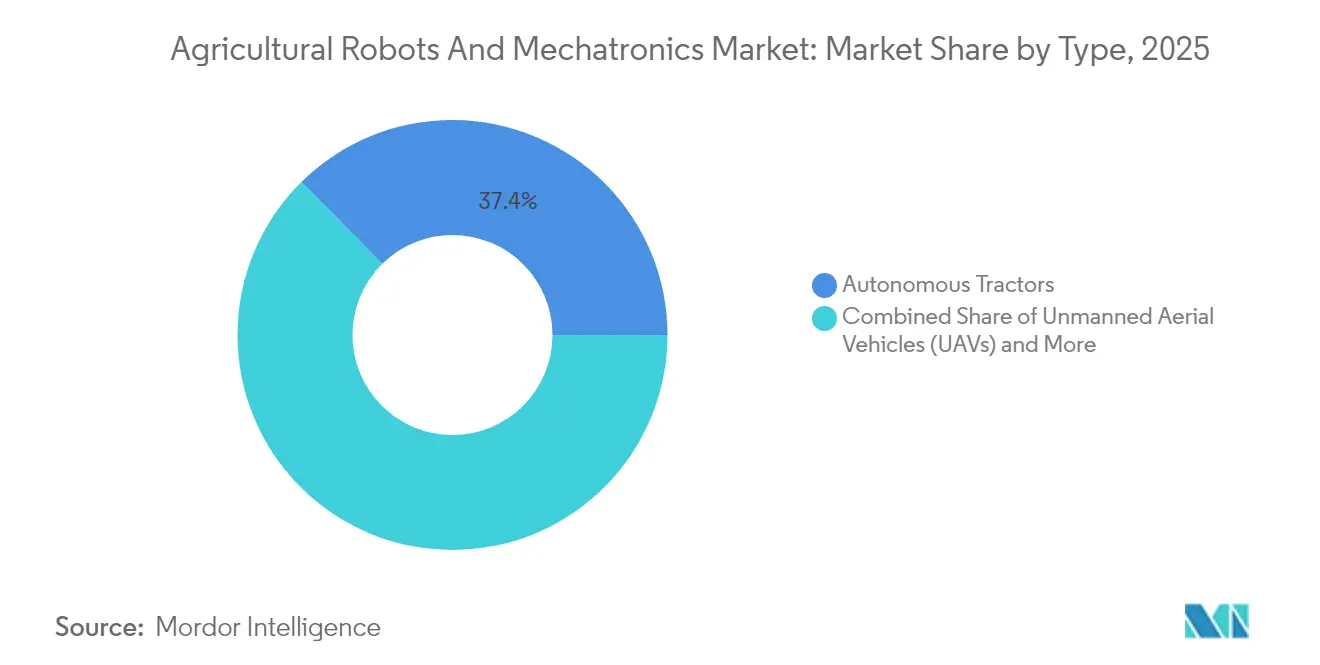

- By type, autonomous tractors led with 37.40% of the market share of the agricultural robots and mechatronics market in 2025, and unmanned aerial vehicles are forecast to expand at a 21.90% CAGR through 2031.

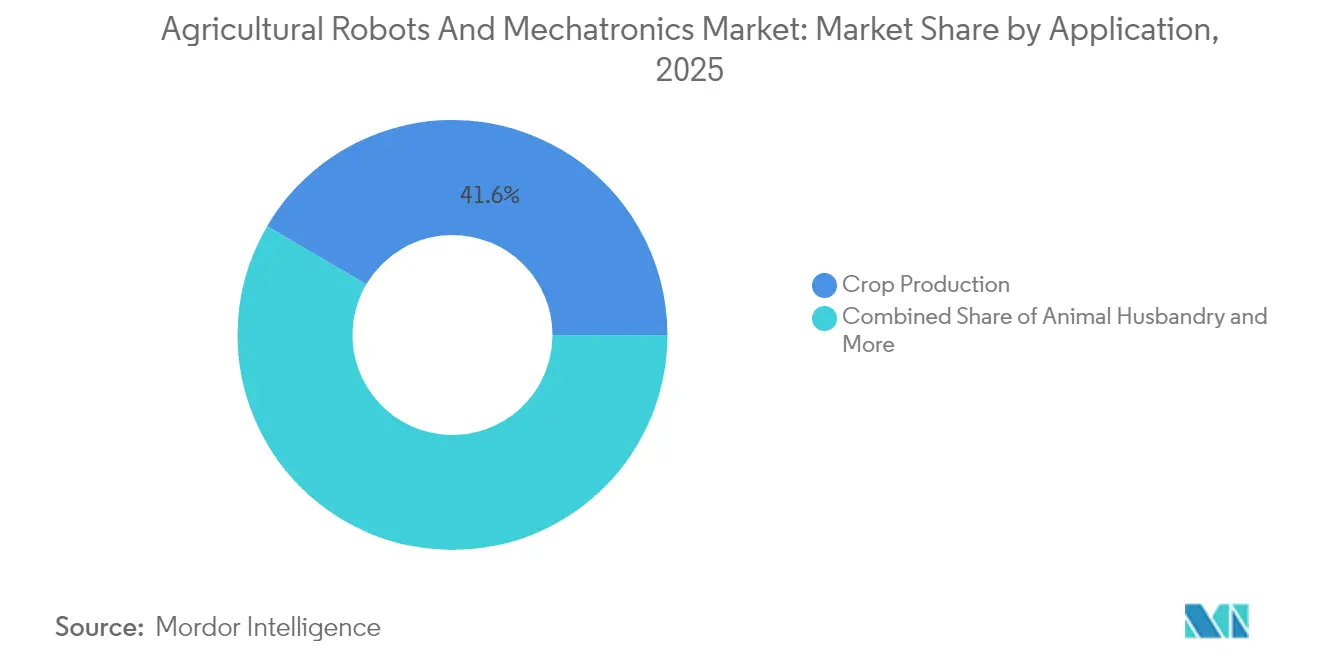

- By application, crop production accounted for 41.55% of the market share of the agricultural robots and mechatronics market in 2025, and is projected to expand at an 17.90% CAGR through 2031.

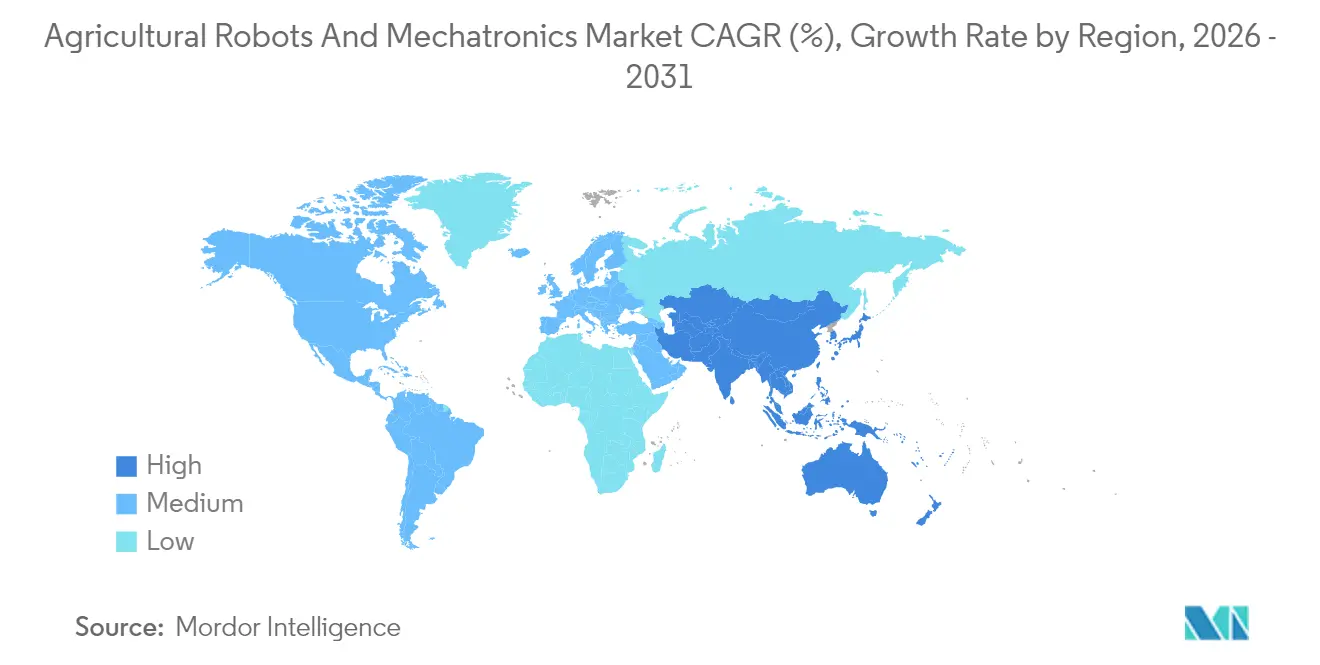

- By geography, North America held 39.30% market share of the agricultural robots and mechatronics market in 2025, and Asia-Pacific is set to grow at a 19.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Robots And Mechatronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Vision-Artificial intelligence (AI) Enables Sub-Centimeter Weeding Accuracy | +2.8% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Declining Light Detection and Ranging (LIDAR) and Multispectral Sensor Costs Cut Robot Prices | +2.5% | Global, benefiting Asia-Pacific and South America | Short term (≤ 2 years) |

| Shortage and Cost of Labor | +2.1% | North America, Western Europe, and Australia | Long term (≥ 4 years) |

| Robot-as-a-Service Financing Unlocks Small and Medium Farm Adoption | +1.9% | Asia-Pacific, South America, and Africa | Medium term (2-4 years) |

| Government Smart-Farming Incentives and Carbon-Credit Schemes | +1.6% | Europe, North America, and China | Medium term (2-4 years) |

| Agricultural Original Equipment Manufacturers (OEMs) Autonomy Roadmaps | +1.4% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Vision-Artificial intelligence (AI) Enables Sub-Centimeter Weeding Accuracy

Machine vision now distinguishes weeds from crops with 98% accuracy in 50 milliseconds, allowing laser or micro-spray systems to target individual plants while traveling 8 kilometers per hour. Carbon Robotics deployed over 100 LaserWeeder units in 2024, cutting herbicide use by 80% and labor costs by USD 200 per acre. Deere & Company’s See and Spray Ultimate pairs 36 cameras with Nvidia Orin processors, creating real-time weed maps to guide sub-centimeter spraying. EcoRobotix’s sun-powered Aerial Robot Arms (ARA) robot extends operating hours by eliminating diesel refueling. Peer-reviewed work in the Journal of Field Robotics confirms that hyperspectral imaging detects pre-emergent weeds seven days before they become visible, hinting at prophylactic weeding routines by 2027.

Declining Light Detection and Ranging (LIDAR) and Multispectral Sensor Costs Cut Robot Prices

Solid-state Light Detection and Ranging (LIDAR) modules that retailed at USD 8,000 in 2020 now cost under USD 1,200, while multispectral cameras fell from USD 15,000 to USD 3,500, lowering robot bills of material by roughly 30%. Trimble’s low-cost Global Navigation Satellite System-Real-Time Kinematic (GNSS-RTK) receivers reduce positioning error to under 2 centimeters without expensive base stations. Cost compression lets mid-tier vendors such as AGCO Corporation and Kubota Corporation sell autonomy packages to 500-acre growers rather than only 5,000-acre operations. Yamaha Motor’s Maximum Relaxation (RMAX) unmanned helicopter undercuts premium drones by 40% in rice farms. Studies in MDPI Sensors show low-cost cameras now achieve 92% of research-grade performance for normalized difference vegetation index mapping.

Shortage and Cost of Labor

Farm labor availability in the United States fell 11% between 2020 and 2024, lifting average hourly wages from USD 14.62 to USD 18.20. Germany and Spain recorded similar deficits, forcing early harvests that compromise quality. DeLaval and GEA robots now milk 35% of Dutch herds, emphasizing that livestock producers face the same labor squeeze. Naïo Technologies’ Oz weeder displaces three workers per hectare, reaching a payback in under two years. Agricultural Systems research links a 10% wage jump to a 6% rise in robotic uptake.

Robot-as-a-Service Financing Unlocks Small and Medium Farm Adoption

Farmers can now lease autonomous sprayers and weeders for USD 20–50 per hectare, replacing USD 150,000 capital purchases with operating expenses. Monarch Tractor’s three-year lease includes software, telematics, and maintenance, lowering total ownership cost by 40%. The European Union-funded ROBS4CROPS pilot raised Spanish and Greek adoption by 67% once payments aligned with harvest cash flow. Mitsubishi HC Capital reports that 54% of Japanese rice farmers would switch to robots under subscription terms. XAG bundles drone service with crop insurance and advisory, making recurring revenue bigger than hardware margin.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Outlay | -1.8% | Global, most acute in South America, Africa, and South Asia | Short term (≤ 2 years) |

| Connectivity Gaps in Rural Areas | -1.5% | North America, Sub-Saharan Africa, and rural India | Medium term (2-4 years) |

| Complexity of Multi-Vendor System Integration | -1.2% | Global, especially mixed-fleet operations | Medium term (2-4 years) |

| Evolving Liability and Safety Regulations for Field Autonomy | -0.9% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Outlay

Fully autonomous tractors sell for USD 350,000–450,000, three to four times a conventional model and above annual revenue for many 500-acre farms in Brazil and India. Retrofit kits that cost USD 150,000 still consume 40% of a medium farm’s equipment budget. The Federal Reserve found that 38% of autonomous-equipment loan applications were rejected in 2024 due to high debt-to-asset ratios [1]Source: Federal Reserve, “Agricultural Credit Survey 2024,” federalreserve.gov. DeLaval milking robots priced at EUR 180,000 (USD 195,000) per unit push a 100-cow dairy’s upgrade cost near USD 400,000. Agricultural Finance Review shows payback stretches to 12 years for farms under 1,000 acres, compared with four years for operations above 3,000 acres.

Connectivity Gaps in Rural Areas

Nineteen percent of rural Americans lack 25 Mbps broadband, and 4G Long Term Evolution coverage dips below 80% in many Midwest counties [2]Source: Federal Communications Commission, “Broadband Deployment Report,” fcc.gov. The United States Department of Agriculture (USDA) ReConnect program is investing USD 1.7 billion, but many projects will not finish until 2027. Only 28% of rural Sub-Saharan Africa has 3G coverage, and satellite links cost USD 80–120 per device monthly. Deere’s Gen2 autonomy kit runs all vision processing on edge modules, so the tractor works even without cellular backhaul. In India, expanding 4G to 68% of rural areas enabled Garuda Aerospace to spray 2.3 million acres in 2024.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Autonomous Tractors Lead and Unmanned Aerial Vehicles (UAVs) Surge

Autonomous tractors generated 37.40% of 2025 revenue, anchoring the agricultural robots and mechatronics market. Unmanned aerial vehicles are set to grow at a 21.90% CAGR, the fastest of any equipment class. Deere shipped 1,200 retrofit 8R tractors in 2024 and expects to double that in 2025 as component costs shrink. DJI’s Agras T50 drone sprays 40 acres per hour and already owns 35% of China’s drone-sprayer segment.

Ground and aerial platforms increasingly work together. Swarm approaches such as AGCO’s Xaver have shown a 60% soil-compaction reduction. Kubota's Agri Robo MR1000A rice transplanter, which achieved 15% penetration in Japan's Niigata Prefecture, is being adapted for wheat seeding in Australia, illustrating how task-specific designs can cross geographies. Yamaha Motor’s task-specific RMAX helicopter proves that specialized designs can undercut general-purpose drones by 40%. Precision Agriculture research confirms hybrid fleets lift net margins 22% over single-platform strategies. These developments reinforce sustained demand across the agricultural robots and mechatronics market.

By Application: Crop Production Leads Growth Momentum

Crop production applications represented 41.55% of 2025 revenue and now anchor the agricultural robots and mechatronics market size outlook, as the segment is forecast to advance at an 17.90% CAGR between 2026 and 2031. Herbicide-saving robots such as Carbon Robotics’ LaserWeeder and variable-rate sprayers like Deere & Company’s See and Spray Ultimate are cutting chemical costs by USD 40 to USD 60 per acre, reinforcing market attractiveness. Animal husbandry maintains steady expansion driven by DeLaval and GEA milking robots, while forest-control drones from DroneSeed illustrate early diversification into reforestation. Controlled-environment farms also adopt greenhouse robots at a double-digit pace, though their share remains modest relative to open-field crops.

Precision interventions continue to shift crop growers from blanket treatments toward plant-level care, with laser or micro-spray weeders reducing input use by up to 40% and unlocking carbon-credit revenue. Deployment momentum is strongest in high-value vegetables and row-crop monocultures, where labor pressure and eco-scheme incentives converge. Academic findings in Agricultural Systems show nitrogen runoff falling 32% on farms that adopt autonomous sprayers, highlighting compliance savings alongside yield protection. Startups focusing on orchards, berries, and specialty crops are enlarging the addressable base, and Robot-as-a-Service financing lowers entry barriers for mid-size producers. As hardware prices decline, crop production remains the clearest path to scale for vendors seeking recurring data and software fees across the agricultural robots and mechatronics market share landscape.

Geography Analysis

North America generated 39.30% of the 2025 revenue share in the agricultural robots and mechatronics market. Wide farm sizes, 92% fourth-generation Long Term Evolution coverage, and the United States Department of Agriculture (USDA) subsidies speed adoption. Autonomous tractors cluster in Iowa, Illinois, and Nebraska, where average holdings exceed 1,200 acres. Canada’s Prairie farms use autonomous grain carts to offset labor gaps, and federal AgriInnovate grants funded 30% of equipment bills for 420 operations in 2024. Mexico’s greenhouse sector is turning to robotic harvesters as labor deficits surpass 22%.

Asia-Pacific is the fastest mover, projected at 19.60% CAGR. China subsidizes up to 40% of drone and tractor costs, pushing mechanization toward a 70% target by 2025 . India’s new beyond-visual-line-of-sight rules let Garuda Aerospace deploy 1,800 spraying drones across 2.3 million acres. Japan’s Kubota Agri Robo transplanter controls 15% of the planted rice area in Niigata Prefecture, while Australia’s SwarmFarm Robotics grain carts combat a 19% labor shortage.

Europe accounted for a significant share of the projected 2024 revenue and is projected to grow at a notable rate. The Common Agricultural Policy allocates a portion of direct payments to eco-schemes, encouraging Spanish strawberry growers to adopt Naïo weeders, which offer a two-year payback period. In Germany, a substantial percentage of dairy herds are now equipped with milking robots, reducing labor requirements by one-third. French vineyards are increasingly utilizing autonomous tractors from Monarch Tractor and Fendt to comply with pesticide-reduction targets. South America, the Middle East, and Africa collectively contribute to the market value and are projected to grow at strong rates, driven by Brazil’s sugarcane farms and South African vineyards.

Regulatory Landscape

Safety, validation, and machinery-compliance requirements are tightening around autonomous agricultural equipment, pushing vendors toward standardized verification and clearly defined operating zones. ISO published ISO 18497-3:2024 (autonomous operating zones) and ISO 18497-4:2024 (verification and validation for autonomous agricultural machinery) in July 2024, providing a formal safety and test framework that OEMs, integrators, and farm operators can reference when deploying field autonomy.

In the European Union, Machinery Regulation (EU) 2023/1230 replaces the Machinery Directive 2006/42/EC and becomes mandatory on 20 January 2027, introducing updated health and safety requirements that explicitly cover autonomous mobile machinery and AI-enabled systems placed on the EU market. In the United States, April 2026 saw USDA announce the National Proving Grounds Network for AgTech (NPG-Ag) to evaluate agricultural technologies under real-world conditions. Proposed 2026 legislation, including the FARM AI Act (S. 4627) and the Advancing Automation Research and Development in Agriculture Act, also signaled increased federal focus on agricultural AI standards development (with NIST collaboration) and dedicated automation and mechanization R&D programs.

Competitive Landscape

The market exhibits moderate concentration, with key players accounting for a significant share of the projected 2024 revenue. Deere & Company is enhancing vertical integration by combining hardware, autonomy kits, and its cloud platform, which now generates a notable portion of its precision-segment revenue through subscriptions. DJI holds a substantial share of the global drone spraying market but faces competition from bundled service offerings in the Asia-Pacific region. AGCO Corporation and CNH Industrial N.V. are focusing on open APIs to reduce integration challenges for mixed fleets.

Specialty-crop automation is attracting startups. Companies are deploying vision-based pickers that achieve high efficiency at reduced costs. Monarch Tractor’s electric MK-V, offered through a Robot-as-a-Service model, reduces ownership costs and appeals to organic producers seeking zero-emission certifications. Solar-powered weeders are extending operational shifts without requiring diesel, making them suitable for operations located far from supply depots.

Patent filings highlight strategic priorities within the market. Recent patents have focused on autonomy and implement interoperability. Compliance with ISO standards is increasingly influencing procurement decisions at large cooperatives. A key emerging area of competition is data monetization. Platforms that dominate agronomic intelligence, such as yield prediction, carbon documentation, and input optimization, are positioned to capture significant ecosystem value.

Agricultural Robots And Mechatronics Industry Leaders

Deere & Company

DJI

AGCO Corporation

CNH Industrial N.V.

Kubota Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Retrofit autonomy and plant-level precision application point to a near-term whitespace, since they modernize existing mixed-brand fleets without requiring full replacement cycles. Active integration efforts reinforce this, including the June 2026 technical integration announced between Sabanto (autonomous tractor operation) and Verdant Robotics (SharpShooter plant-level precision application), which links operator-free driving to targeted input delivery for high-value cropping systems where labor intensity and chemical optimization are key purchase drivers.

Drone spraying and service-led deployment models are also broadening the addressable base by reducing per-acre adoption friction and shortening time to operational value. DJI's July 2026 global launch of the Agras T55 and T100 dual-battery spraying system highlights continued product cadence in UAV application equipment. In parallel, government programs are shaping commercialization pathways, including South Korea's Ministry of Agriculture, Food and Rural Affairs (MAFRA) unveiling a Next-Generation Agriculture and Bio R&D Strategic Roadmap in March 2026 that includes multiple Robotics-as-a-Service commercialization models and an explicit push for higher automation across major farming tasks. For vendors, participation in proving-ground style evaluation (for example, USDAs NPG-Ag) and alignment with emerging AI and safety standards (the ISO 18497 series and EU Machinery Regulation (EU) 2023/1230 readiness) are increasingly tied to go-to-market performance across compliance-grade validation, data interoperability, and measurable field outcomes.

Recent Industry Developments

- February 2026: Deere & Company announced the five companies selected for its 2026 Startup Collaborator Program, including participants focused on robotics and drone imagery (such as Aerobotics and TorqueAGI). The program expands Deere's pipeline for AI-enabled autonomy capabilities and indicates continued emphasis on integrating third-party innovation into its precision and autonomy stack.

- November 2025: CNH Industrial's New Holland debuted its R4 cabless autonomous robot concept for vineyard and orchard work. The unveiling highlighted a shift toward specialized robots for high-value specialty crops, where repeatable tasks and labor scarcity support faster operational payback.

- April 2024: AGCO and Trimble closed their joint venture to form PTx Trimble, combining mixed-fleet precision agriculture capabilities with a platform approach to autonomy-enabling technologies. The structure strengthens interoperability for farms running multiple equipment brands and helps reduce multi-vendor integration friction that can slow automation adoption.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market includes revenue generated from agricultural robots and mechatronics systems used to automate or assist farm operations, mainly across crop production and animal husbandry. It covers the associated hardware and integrated control elements sold into farms.

Scope exclusions: It does not include general farm inputs or conventional machinery that lacks an autonomous or robotic mechatronics function.

Segmentation Overview

- By Type

- Autonomous Tractors

- Unmanned Aerial Vehicles (UAVs)

- Milking Robots

- Other Types

- By Application

- Crop Production

- Animal Husbandry

- Forest Control

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Spain

- United Kingdom

- France

- Germany

- Russia

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the first version of the model and set realistic bounds for adoption and pricing across farm tasks. We mainly relied on public sources such as USDA and NASS releases, FAO production and crop area databases, Eurostat farm structure statistics, and customs and trade statistics from sources such as UN Comtrade. To keep definitions consistent, we also reviewed robotics and agriculture standards notes and safety guidance from sources such as ISO and government workplace safety bodies, where relevant.

On the company side, annual reports, investor presentations, product catalogs, and press releases were used to map product categories and likely price bands. We then sanity-checked directionally the split between robot types and use cases based on those disclosures. In a few places, paid subscriptions for company financials and news were used to confirm timelines like product launches and acquisitions, and a patent database was used to track where R and D intensity was rising. These desk sources are illustrative only, and other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were run to turn the desk assumptions into workable inputs, especially where public data is thin on unit shipments and farm level usage. We spoke with a mix of equipment makers, component suppliers, farm operators, and channel partners across the main consuming regions, and we used their feedback to validate adoption pacing, typical use intensity, and the price difference between entry systems and higher automation setups.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 18% | APAC: 49% |

| Mid tier: 53% | Functional/Unit leaders: 35% | EMEA: 33% |

| Smaller Players: 18% | Managers: 47% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool reconstruction, where cropped area and livestock herd sizes are connected to the workable tasks that can be automated, then scaled using penetration rates that reflect farm economics and labor availability. The model is cross-checked with selective bottom-up approximations, such as sampled average selling price ranges for key robot types multiplied by implied unit volumes discussed in interviews, followed by adjustments where the two views do not align.

A few market-specific inputs that matter in this space include farm labor cost pressure, planted area by major crops, dairy herd and milking parlor counts, average farm size and mechanization levels, and the expected pace of sensor and actuator cost decline that affects system pricing. Forecasts use scenario analysis, where adoption curves are stress-tested under faster and slower payback conditions, and the final view is selected based on what most experts considered feasible by region. When bottom-up signals are incomplete, such as when unit disclosures are missing, we used ranges and coverage ratios from channel feedback, then reconciled them back to the demand pool totals so the end number stays explainable.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, such as whether implied unit volumes make sense against cropped acreage, livestock intensity, and known seasonality in buying cycles. Large variances were flagged, reviewed by another analyst, and then rechecked by going back to selected respondents when assumptions moved materially.

The report is refreshed annually, and interim updates are made when major events occur, such as policy changes, major product releases, or sharp shifts in farm income drivers. Before publication, we run a fresh data pass to ensure the market size and near-term assumptions reflect the latest publicly available information.

Mordor Intelligence's Agricultural Robots and Mechatronics Market Sizing Compared With Other Published Estimates

Published market sizes for agricultural robots and mechatronics can appear far apart because boundaries are not always drawn the same way. Adoption assumptions also differ across regions and farm types. Variance can also come from how pricing is treated, particularly when some sources blend hardware with broader digital farm services.

The benchmark table shows a tighter 2026 to 2031 build than some longer-horizon figures. In Mordor Intelligence's model, totals are tied to defined robot and mechatronics categories mapped to farm operations, instead of extending scope into wider precision agriculture software revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.99 B (2026) | |

| Trade Publisher A | USD 5.47 B (2025) | Uses a different base year and appears to include a broader bucket of mechatronics and related services, which can lift the starting value even before adoption is modeled. |

| Industry Research Desk B | USD 4.30 B (2024) | Builds from an earlier base year with a narrower installed base assumption and a different set of application inclusions, which can suppress the starting point versus a later-year demand pool. |

Reading the three numbers together, most of the spread can be explained by scope boundaries, base year timing, and how adoption and pricing are progressed over time. By keeping the market definition linked to clear farm tasks and checking totals against practical adoption signals, the estimate stays traceable and repeatable for planning decisions.

Key Questions Answered in the Report

What is the 2026 value of the agricultural robots and mechatronics market?

The agricultural robots and mechatronics market size is valued at USD 4.99 billion in 2026.

Which equipment segment is growing the fastest through 2031?

Unmanned aerial vehicles are forecast to post a 21.90% CAGR, the quickest among all equipment types.

How large is North America's share of total demand?

North America accounted for 39.30% of 2025 revenue, the largest regional share.

What business model helps small farms afford robotics?

Robot-as-a-Service leasing lets growers pay USD 20-50 per hectare, avoiding large capital outlays.

Page last updated on: