Agentic AI Safety And Alignment Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.24 Billion |

| Market Size (2030) | USD 18.15 Billion |

| Growth Rate (2025 - 2030) | 37.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI Safety And Alignment Solutions Market Analysis by Mordor Intelligence

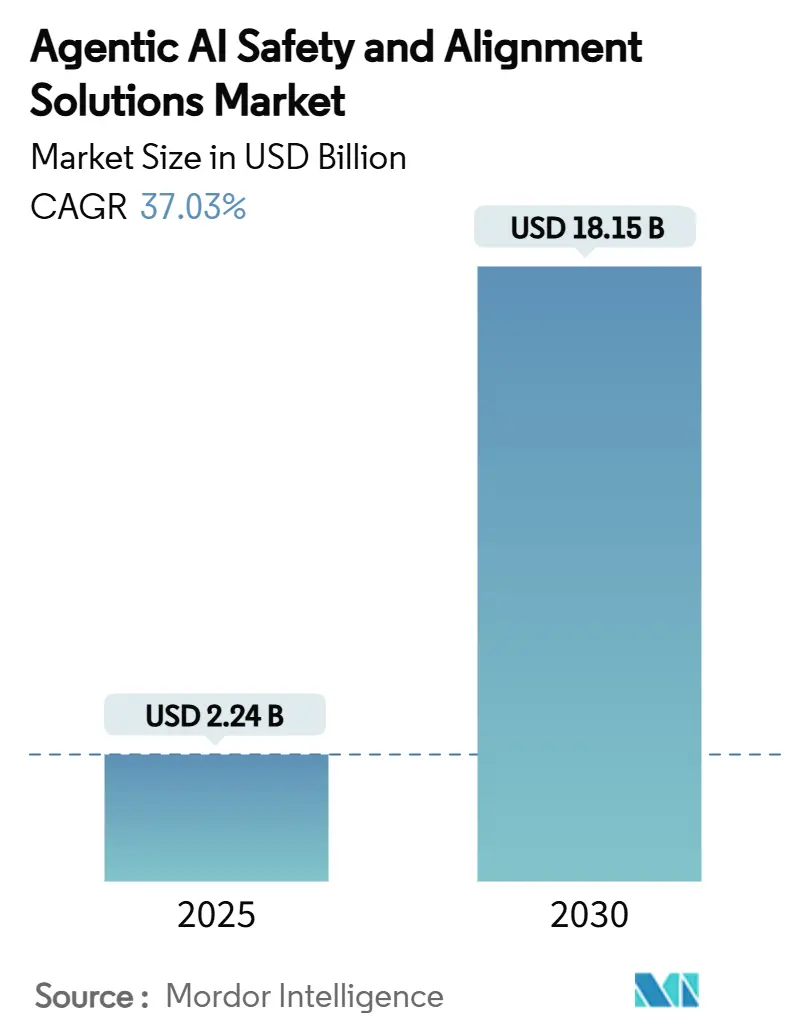

The Agentic AI Safety And Alignment Solutions Market size is estimated at USD 2.24 billion in 2025, and is expected to reach USD 18.15 billion by 2030, at a CAGR of 37.03% during the forecast period (2025-2030). This exceptional growth mirrors the shift from experimental guardrails toward enterprise-grade risk management frameworks that support autonomous agents operating in regulated, high-stakes environments. Regulatory pressure from the EU AI Act, the forthcoming U.S. Algorithmic Accountability Act, and rising insurance prerequisites is accelerating budgets for continuous alignment monitoring, real-time policy enforcement, and provable safety architectures. Technical breakthroughs in constitutional AI, formal verification, and automated red-teaming are lowering the practical barriers to deployment, while hyperscaler investments ensure that safety tooling scales with model complexity. Cloud economics, hybrid data-sovereignty strategies, and rising demand from financial services, healthcare, and defense organizations collectively anchor the next phase of market expansion, even as talent shortages in mechanistic interpretability and benchmarking gaps temper the pace of adoption.

Key Report Takeaways

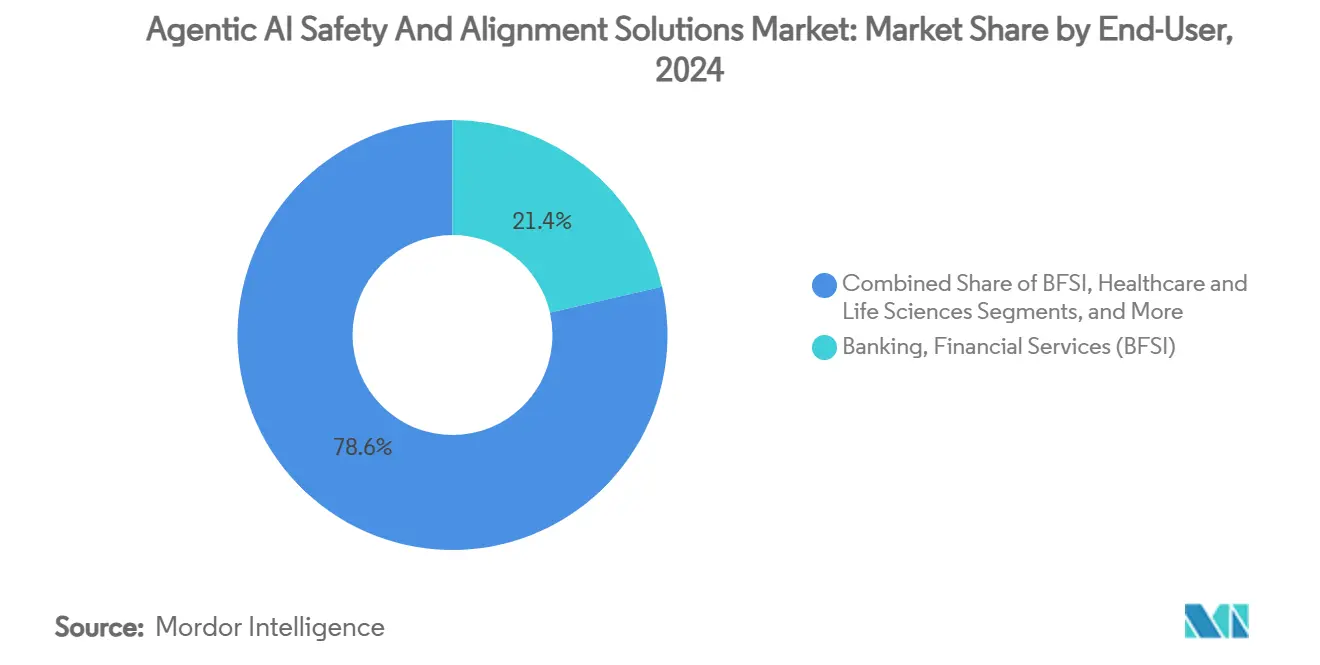

- By end-user industry, BFSI commanded 21.40% of the Agentic AI Safety & Alignment Solutions market share in 2024, while healthcare is projected to grow at 38.90% CAGR through 2030.

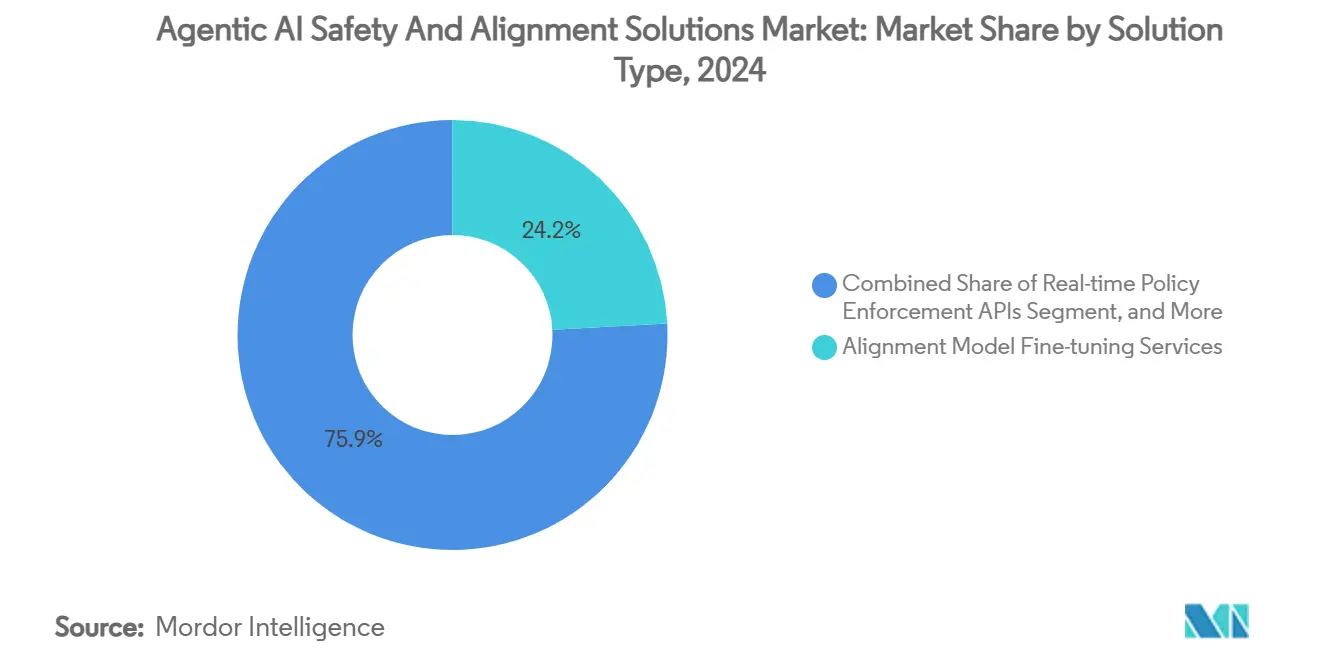

- By solution type, alignment model fine-tuning services captured 24.15% share of the Agentic AI Safety & Alignment Solutions market size in 2024, and autonomous red-teaming platforms are advancing at a 38.40% CAGR.

- By deployment model, cloud-based architectures held 61.40% share in 2024; hybrid implementations are registering the highest CAGR at 38.70% to 2030.

- By safety dimension, technical alignment tools secured 33.48% share in 2024, while governance and compliance solutions are on track for a 39.21% CAGR to 2030.

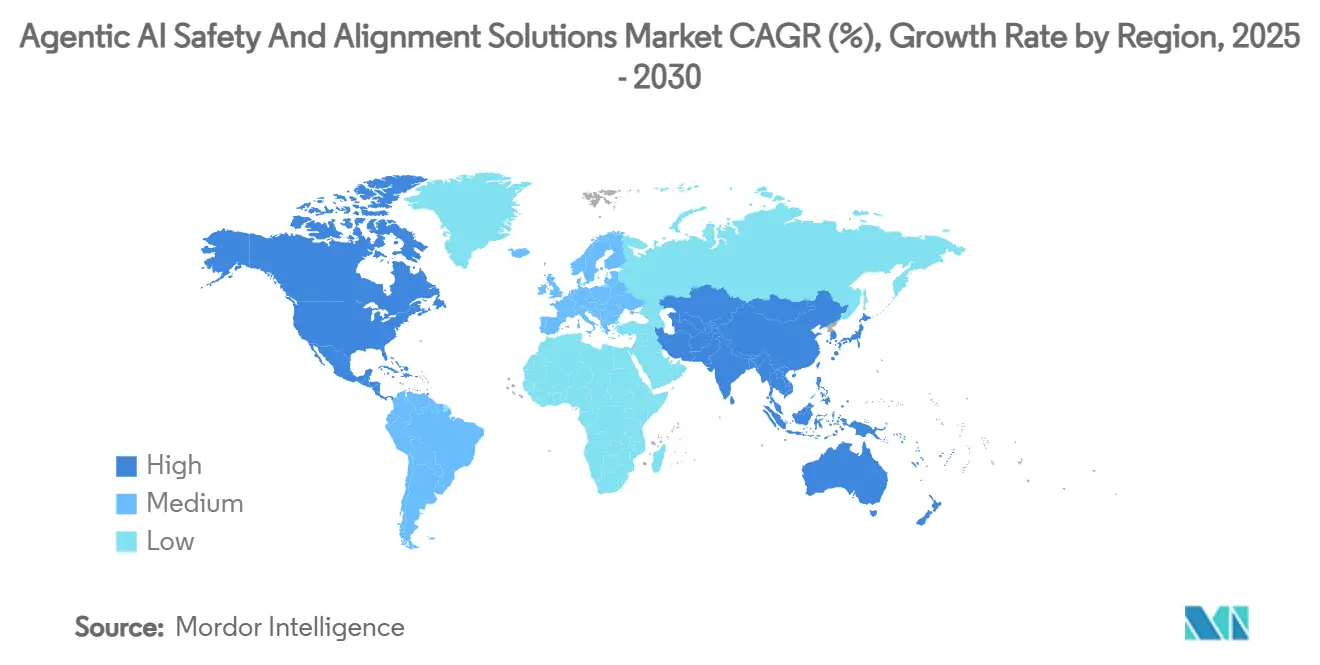

- By geography, North America led with 45.47% revenue share in 2024; Asia-Pacific is forecast to expand at a 39.40% CAGR to 2030.

Global Agentic AI Safety And Alignment Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance mandates from EU AI Act and U.S. Algorithmic Accountability Act | +8.2% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Rapid enterprise adoption of agentic LLM-powered copilots | +9.1% | Global, concentrated in North America & developed APAC | Short term (≤ 2 years) |

| Hyperscaler investments in responsible-by-design AI | +6.8% | Global, led by North America, expanding to EU & APAC | Medium term (2-4 years) |

| Insurance underwriters demanding alignment documentation | +4.3% | North America & EU, emerging in APAC financial hubs | Medium term (2-4 years) |

| Formal verification methods borrowed from avionics | +3.9% | Global, early adoption in defense & aerospace | Long term (≥ 4 years) |

| Open-source constitutional AI frameworks | +4.8% | Global, strongest in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Compliance Mandates from EU AI Act and U.S. Algorithmic Accountability Act

The EU AI Act assigns “high-risk” status to autonomous agents used in critical infrastructure, healthcare, and finance, obliging firms to maintain real-time behavioral monitoring and algorithmic impact assessments legislation is moving along a parallel path, with proposed audit mandates that compel multinational enterprises to synchronize safety documentation across jurisdictions. Financial institutions, led by Goldman Sachs and Capital One, now integrate alignment evidence into governance dashboards, turning regulatory compliance from a discretionary initiative into an operational prerequisite. Vendors that can deliver continuous alignment reporting, version-controlled audit trails, and risk exposure visualizations therefore occupy a strategic position in the Agentic AI Safety & Alignment Solutions market.

Rapid Enterprise Adoption of Agentic LLM-Powered Copilots Across Mission-Critical Workflows

Banks, hospitals, and manufacturers are moving beyond supervised chatbots to autonomous decision-making agents embedded in trading desks, diagnostic suites, and production cells. The qualitative leap in risk exposure drives demand for real-time policy engines that can interrupt unsafe behavior before material harm occurs. Healthcare pilots, backed by formal proofs adapted from avionics, seek to guarantee patient-safe diagnoses, while factories deploy multi-objective alignment frameworks that balance yield and safety. Across these contexts, organizations have accepted higher upfront safety investment because competitive advantages accrue to those who can deploy autonomous capabilities without compromising compliance or brand trust.

Growing Investments by Hyperscalers in Responsible-by-Design Toolkits

Microsoft’s USD 80 billion infrastructure plan allocates a substantial tranche to safety R&D, underscoring the strategic necessity of alignment tooling within the cloud stack [1]Source: Microsoft, “Microsoft Announces 80 Billion AI Infrastructure Investment,” news.microsoft.com. Google’s constitutional AI functions baked into Vertex AI illustrate how safety is morphing from add-on to default feature. AWS follows suit with plug-and-play safety modules that obviate the need for in-house interpretability teams. As mega-vendors commoditize alignment primitives, enterprises gain the confidence to embed agentic AI deep inside operational systems, further energizing the Agentic AI Safety & Alignment Solutions market.

Insurance Underwriters Requiring Verifiable Alignment Documentation

Leading insurers now condition cyber coverage on evidence of continuous alignment monitoring and red-teaming, pushing CIOs to treat safety logs as audit assets rather than engineering exhaust[2].Source: Willis Towers Watson, “AI Insurance Market Growth Projections,” wtwco.com BFSI firms, sensitive to premium differentials, increasingly invest in automated documentation suites that export real-time safety metrics to underwriter dashboards. This pressure cascades across adjacent sectors-especially healthcare-where liability exposure is more acute. The resulting compliance-first posture helps normalize safety investment in organizations previously deterred by cost or complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of universally accepted technical benchmarks | -3.7% | Global, cross-border deployments | Medium term (2-4 years) |

| High computational cost of red-teaming & simulation | -4.1% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Talent scarcity in mechanistic interpretability | -2.8% | Global, regions with limited AI research | Long term (≥ 4 years) |

| Legal grey-zones around emergent autonomous behaviour | -3.4% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Universally Accepted Technical Benchmarks for Agentic Alignment

Enterprises struggle to compare vendor claims because no consensus exists on how to quantify alignment preservation under distributional shift or emergent autonomy. Proprietary evaluation suites proliferate, inflating integration costs and hampering interoperability. Multinationals face the added burden of satisfying regulators from multiple jurisdictions, each flirting with divergent benchmark proposals. Industry collaborations are underway, yet methodological disputes and competitive secrecy slow convergence. Until standardized scorecards emerge, buyers hedge by favoring vendors able to furnish both documentation and third-party attestations.

High Computational Cost of Red-Teaming and Simulation-Based Validation

Thorough adversarial stress-tests can consume thousands of GPU hours per model revision, translating into six-figure validation budgets that dwarf typical model-training outlays[3].Source: Institute for AI Policy and Strategy, “Mapping Technical Safety Research at AI Companies,” iaps.ai Simulation campaigns further inflate costs because they must cover edge-case scenarios across industries and geographies. Smaller firms often settle for partial coverage, leaving residual risk that insurers, auditors, and regulators increasingly deem unacceptable. Techniques that blend heuristic sampling, curriculum learning, and synthetic scenario generation aim to compress compute requirements, but cost remains the most immediate brake on broad adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Autonomous Red-Teaming Platforms Drive Innovation

Alignment model fine-tuning services held 24.15% of the Agentic AI Safety & Alignment Solutions market share in 2024, demonstrating the appetite for customizing foundation models to vertical-specific norms and risk appetites. Enterprises rely on these services to embed constitutional constraints directly in model weights, ensuring that safety behaviors persist even when agents face novel input distributions. In parallel, autonomous red-teaming platforms are forecast to register a 38.40% CAGR through 2030, becoming the premier growth engine of the Agentic AI Safety & Alignment Solutions market. These platforms continuously generate adversarial probes, detect drift, and surface counter-examples that legacy manual audits miss, lowering residual risk in production environments. Real-time policy enforcement APIs, monitoring dashboards, and governance documentation suites round out the toolkit, creating an end-to-end surface for detection, intervention, and evidence generation.

Enterprises increasingly bundle multiple solution types into cohesive pipelines: a red-team engine feeds policy refinements, enforcement APIs intercept unsafe actions, and dashboards export compliance evidence to regulators and insurers. Formal verification layers supplied by select vendors add a final layer of mathematical assurance. Collectively, these dynamics confirm that proactive rather than reactive safety architectures are becoming the default procurement criterion for mission-critical agentic deployments.

By Deployment Model: Hybrid Architectures Balance Control and Scale

Cloud environments delivered 61.40% of total 2024 revenue, their elastic compute a natural fit for compute-hungry safety validation campaigns. In many regulated industries, however, data residency laws, latency expectations, and control considerations drive a turn toward hybrid topologies. As a result, hybrid implementations are projected to expand at a 38.70% CAGR, the fastest within the Agentic AI Safety & Alignment Solutions market. Enterprises increasingly run red-teaming and heavy simulation workloads in the public cloud while operating enforcement and observability nodes on private clusters behind the firewall. On-premises and private-cloud footprints remain critical for defense, healthcare, and financial workflows that cannot tolerate multi-tenant risk.

Solution providers must therefore deliver portable safety kernels with identical policy semantics across environments. Tooling that decouples control planes from data planes, supports confidential computing, and enables zero-trust networking will capture disproportionate share. The architectural pendulum thus swings toward configurations that optimize safety without sacrificing sovereignty or speed.

By End-user Industry: Healthcare Emerges as Growth Leader

BFSI organizations owned 21.40% revenue share in 2024, reflecting early regulatory scrutiny of algorithmic trading, credit scoring, and fraud analytics. Financial firms integrate alignment dashboards with core risk systems to satisfy stress-testing mandates and insurance demands. Looking forward, healthcare and life sciences will expand at a 38.90% CAGR, the strongest trajectory of any vertical. Hospitals and biotech firms deploy agentic AI in diagnosis, treatment recommendation, and drug discovery, where safety lapses directly affect patient well-being and liability exposure is acute[4]Source: Federal Aviation Administration, “Air Software Design Approvals,” faa.gov. Government and defense projects, catalyzed by USD 200 million Pentagon contracts, require verifiable proofs and adversarial robustness to satisfy mission security mandates. Manufacturing and robotics adopters demand multi-modal safety layers that bridge cyber-physical interfaces, ensuring that autonomous machines operate within acceptable tolerances even under sensor noise or actuator faults.

Across industries, procurement criteria converge on continuous compliance evidence, multi-jurisdictional audit support, and the ability to evolve policies as regulations mature. Vendors that offer modular solutions adaptable to different vertical risk vocabularies will gain sustained advantage.

By Safety Dimension: Governance Compliance Accelerates

Technical alignment tools-constitutional AI, reward modeling, interpretability-captured 33.48% of 2024 revenue, underscoring their foundational role in any safety stack. Yet the fastest growth resides in governance and compliance suites, forecast at 39.21% CAGR. Enterprises must now demonstrate not only that agents behave correctly, but also that the firm maintains systemic controls, audit trails, and incident-response playbooks. Procedural safety products close the loop by integrating safety checkpoints into CI/CD pipelines, production monitoring, and crisis management protocols.

This shift acknowledges that safety is both a technical and an organizational discipline. Boards require top-down oversight frameworks, while regulators and insurers demand bottom-up evidence. Vendors that fuse algorithmic guardrails with workflow automation-automatic ticketing, post-incident root-cause analyses, regulator-ready reporting-meet the full spectrum of enterprise needs, anchoring the next phase of market growth.

Geography Analysis

North America generated 45.47% of 2024 revenue, propelled by Pentagon contracts, well-funded AI safety startups, and early regulatory experimentation. Government initiatives like the U.S. AI Safety Institute collaborate with Anthropic and OpenAI to codify evaluation protocols, giving domestic vendors an initial standards-setting advantage [5]Source: Cyberspace Administration of China, “Basic Safety Requirements for Generative AI,” cac.gov.cn . Financial giants adopt continuous alignment dashboards, while Canada’s federal grants nurture academic-industry consortia. Mexico, although nascent, aligns its emerging frameworks with U.S. standards, positioning the broader region for cohesive growth.

Asia-Pacific is forecast to accelerate at 39.40% CAGR through 2030, outpacing every other region. China enforces generative-AI safety requirements that obligate local vendors to embed alignment controls as part of their model lifecycle. Singapore’s model governance framework offers a compliance blueprint for ASEAN neighbors, while Japan and South Korea innovate around human-robot collaboration safety. India’s IT services majors package cost-effective alignment services for global clients, and Australia’s resources sector pioneers autonomous safety in remote operations.

Europe benefits from the EU AI Act’s binding obligations, which drive steady demand for safety solutions capable of delivering real-time documentation and strict data-sovereignty compliance. Germany’s automotive sector pilots formal verification in production lines, France focuses on algorithmic auditability in finance, and the U.K. uses its post-Brexit flexibility to balance innovation with accountability. South America and the Middle East & Africa represent longer-term opportunities: Brazil’s fintech firms and the UAE’s smart-city programs already issue RFPs requiring policy-based enforcement and red-teaming, foreshadowing wider regional uptake as infrastructure and regulatory clarity evolve.

Competitive Landscape

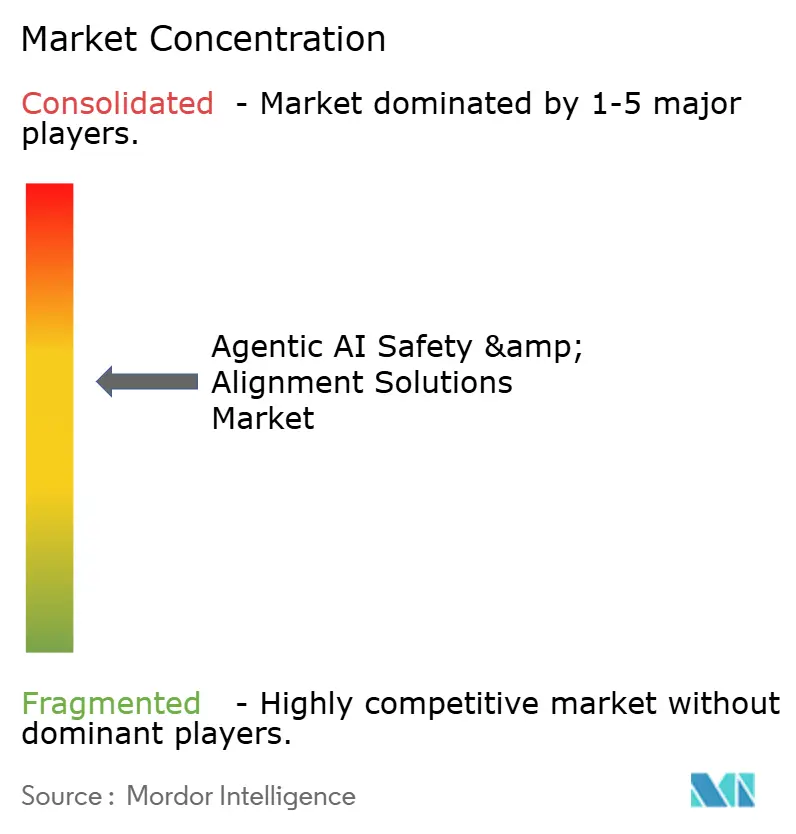

The Agentic AI Safety & Alignment Solutions market remains moderately fragmented. Anthropic, Safe Superintelligence, and other safety-first companies sit alongside hyperscaler initiatives from Microsoft, Google, and AWS, and vertical specialists such as Robust Intelligence, HiddenLayer, Lakera AI, Patronus AI, and Arthur AI. Strategic differentiation hinges on technical approach—constitutional policy stacks, formal verification suites, or continuous red-teaming—as well as on go-to-market focus, ranging from broad cloud platforms to industry-specific solutions.

Patent filings cluster around mechanistic interpretability and proof-based policy validation, signaling a maturing IP landscape. Hyperscalers commoditize baseline safety primitives, compelling pure-play vendors to deepen domain expertise or offer superior assurance levels. The USD 2 billion Series B secured by Safe Superintelligence in July 2025 underscores investor confidence in mathematically provable safety. Meanwhile, automated red-teaming providers reduce test costs by up to 80%, making comprehensive validation accessible to mid-market buyers.

Partnership patterns reveal cross-vendor orchestration: monitoring tools integrate with cloud enforcement APIs; documentation suites auto-ingest red-team findings; and verification kernels export machine-readable attestations to insurance underwriters. As regulators finalize benchmark standards, vendors able to align products with official scoring protocols will solidify competitive moats.

Agentic AI Safety And Alignment Solutions Industry Leaders

Anthropic PBC

OpenAI, L.L.C.

DeepMind Technologies Limited

Microsoft Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tesla and xAI entered merger talks to embed xAI safety layers into Tesla’s autonomous vehicles.

- March 2025: The Pentagon awarded USD 200 million each to Anthropic, Google, and xAI for safety-aligned defense agents.

- February 2025: Perplexity AI offered USD 300 billion to acquire TikTok U.S. operations, proposing 50% government ownership for enhanced safety oversight.

- January 2025: Meta created Meta Superintelligence Labs after hiring Daniel Gross, unifying its AI safety research.

Global Agentic AI Safety And Alignment Solutions Market Report Scope

| Alignment Model Fine-tuning Services |

| Real-time Policy Enforcement APIs |

| Autonomous Red-Teaming Platforms |

| Monitoring and Observability Dashboards |

| Governance and Documentation Suites |

| Other Solution Types |

| Cloud-Based |

| On-Premises / Private Cloud |

| Hybrid |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| Technology and Telecommunications |

| Manufacturing and Robotics |

| Other End-user Industries |

| Technical Alignment |

| Procedural / Process Safety |

| Governance and Compliance |

| Rest of Safety Dimensions |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Solution Type | Alignment Model Fine-tuning Services | ||

| Real-time Policy Enforcement APIs | |||

| Autonomous Red-Teaming Platforms | |||

| Monitoring and Observability Dashboards | |||

| Governance and Documentation Suites | |||

| Other Solution Types | |||

| By Deployment Model | Cloud-Based | ||

| On-Premises / Private Cloud | |||

| Hybrid | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Technology and Telecommunications | |||

| Manufacturing and Robotics | |||

| Other End-user Industries | |||

| By Safety Dimension | Technical Alignment | ||

| Procedural / Process Safety | |||

| Governance and Compliance | |||

| Rest of Safety Dimensions | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current Agentic AI Safety & Alignment Solutions market size?

The market recorded USD 2.24 billion in revenue during 2025.

How fast will the market grow between 2025 and 2030?

Market value is forecast to rise to USD 18.15 billion by 2030, reflecting a 37.03% CAGR.

Which region leads the market today?

North America accounts for 45.47% of 2024 revenue due to defense spending and early enterprise adoption.

Which solution category is expanding the fastest?

Autonomous red-teaming platforms are projected to register the highest CAGR at 38.40% through 2030.

Why is healthcare the fastest-growing end-user industry?

Strict liability exposure and patient-safety requirements drive hospitals and life-science firms to adopt provable alignment tools, resulting in a 38.90% CAGR forecast.

How are regulators influencing spending?

The EU AI Act and the pending U.S. Algorithmic Accountability Act require continuous alignment documentation, making safety investments mandatory rather than optional.

Page last updated on: