Feed Prebiotics Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Market Size (2025) | USD 2.98 Billion |

| Market Size (2030) | USD 3.83 Billion |

| Growth Rate (2025 - 2030) | 5.13% CAGR |

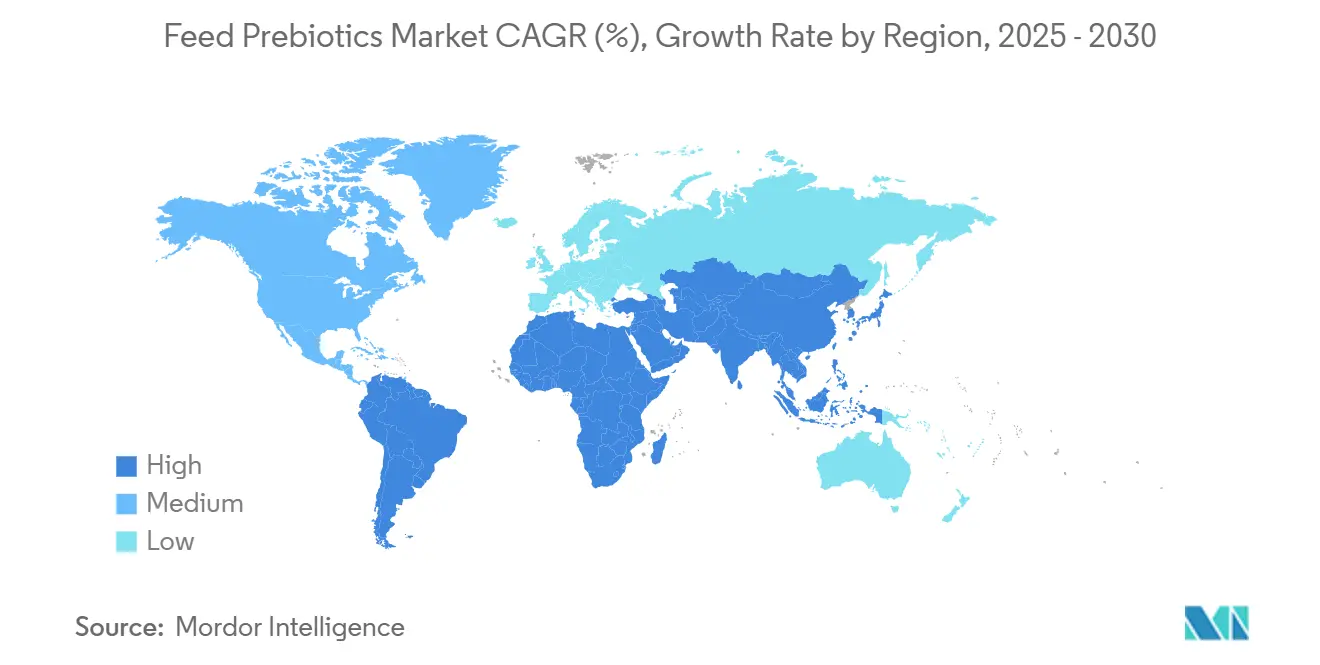

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

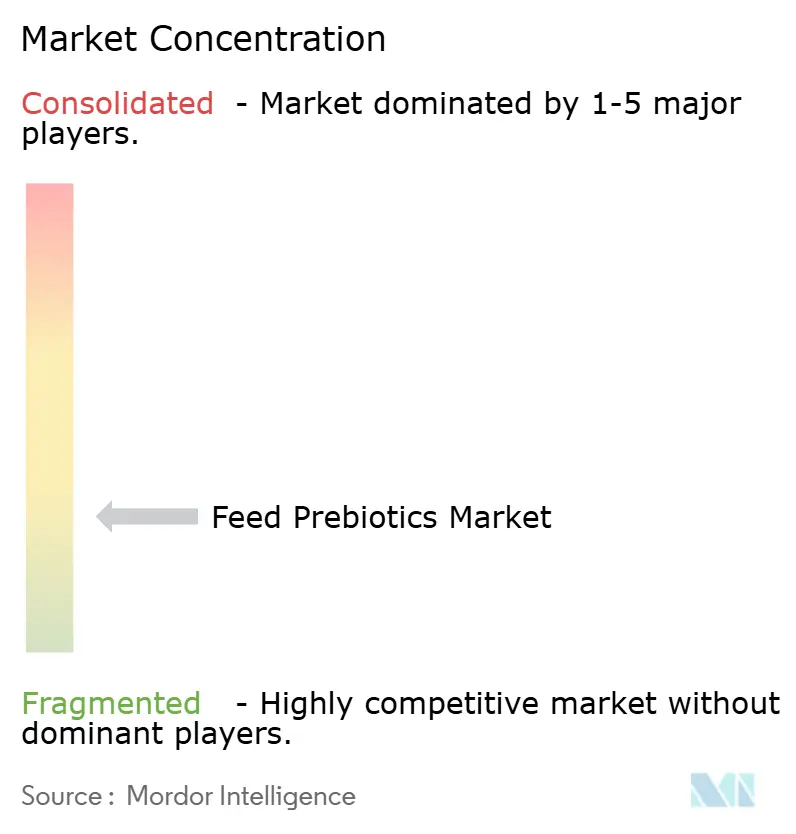

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Prebiotics Market Analysis by Mordor Intelligence

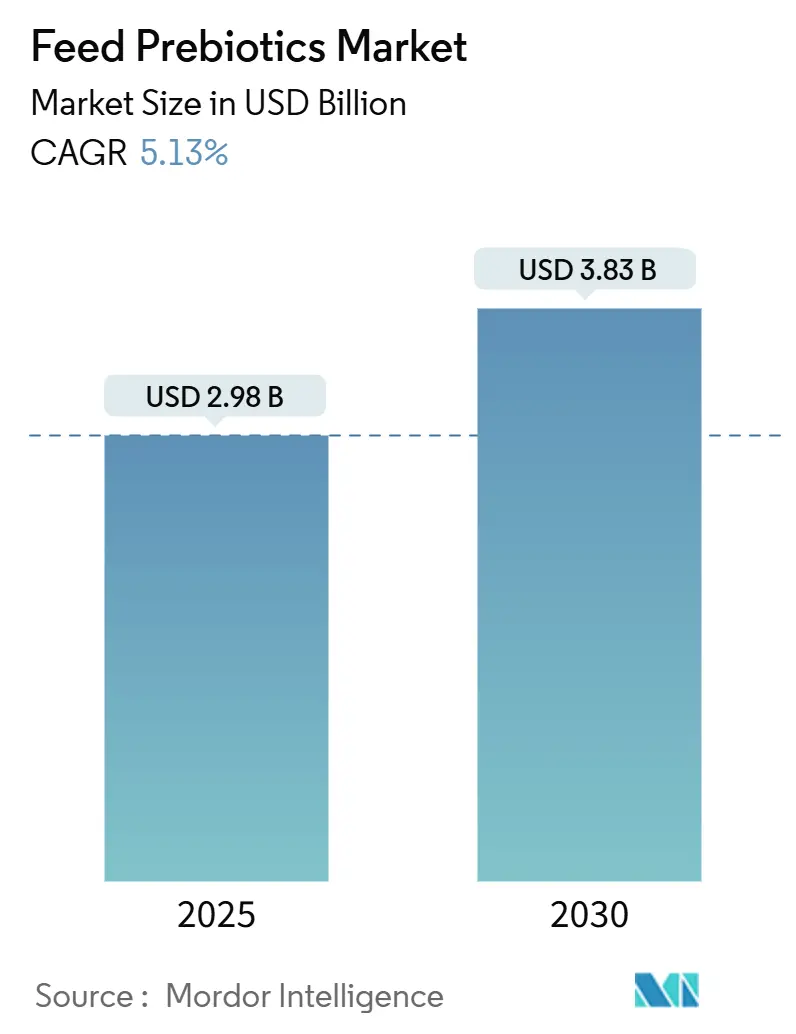

The feed prebiotics market size is USD 2.98 billion in 2025 and is projected to reach USD 3.83 billion by 2030, representing a 5.13% CAGR over the forecast period. The upward trajectory is driven by stringent global rules restricting the use of antibiotic growth promoters, rising demand for antibiotic-free meat, and ongoing cost reductions achieved through innovations in enzymatic production. The rapid industrialization of poultry and aquaculture farming in the Asia-Pacific, combined with proactive compliance in North America, has further strengthened the link between gut-health solutions and productivity targets, positioning the feed prebiotics market for sustained expansion. Mounting consumer pressure on food-service majors and retail chains to eliminate medically important antibiotics, paired with vertical integration strategies among major producers, continues to unlock new commercial opportunities.

Key Report Takeaways

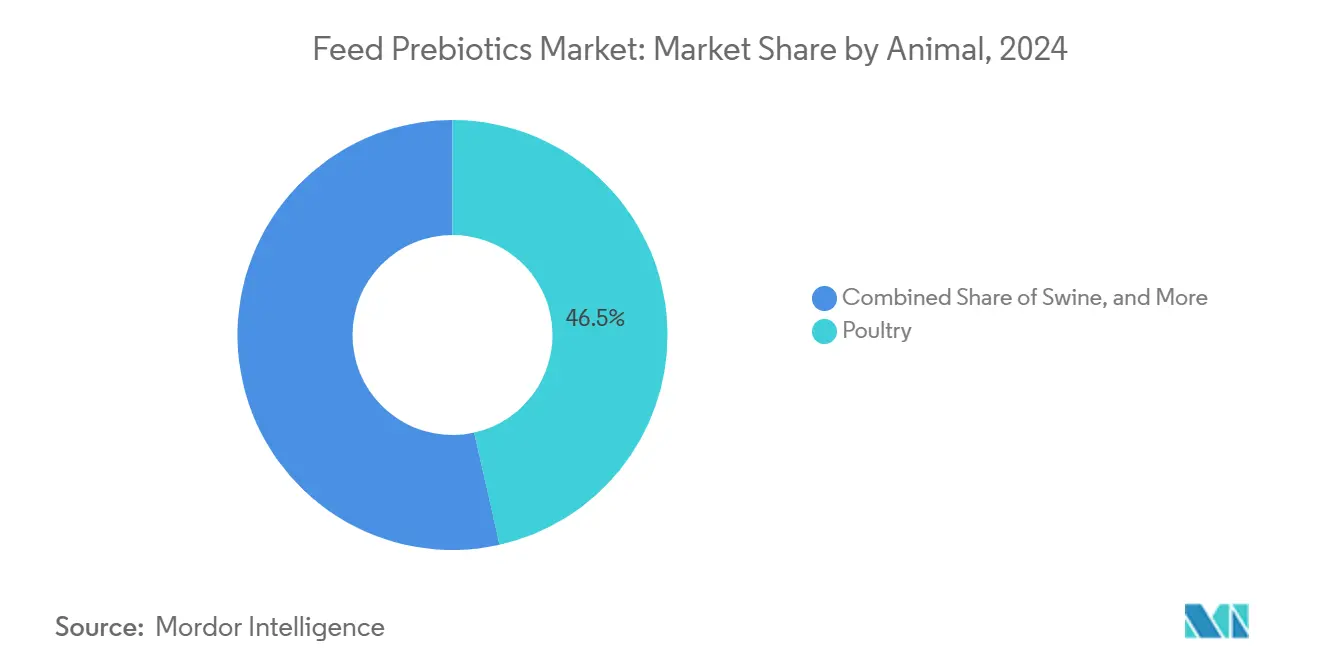

- By animal, poultry led with a 46.5% feed prebiotics market share in 2024 and is advancing at a 5.40% CAGR through 2030.

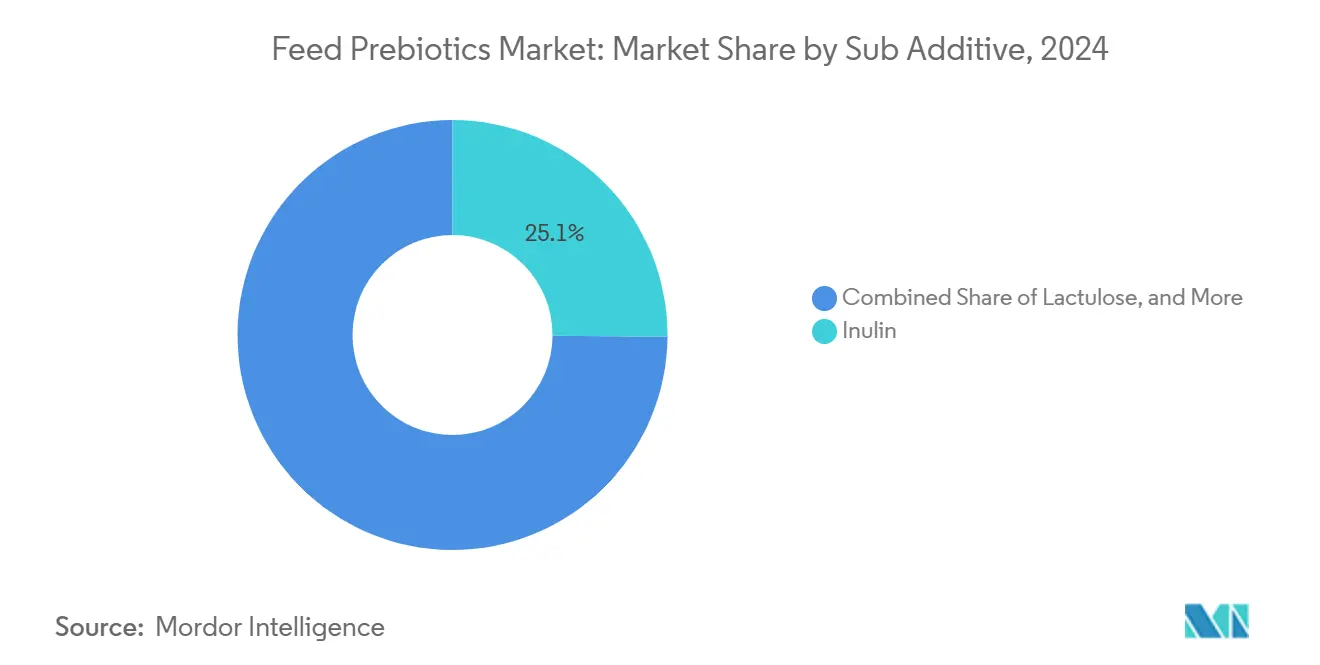

- By sub-additive, inulin accounted for 25.1% of the feed prebiotics market size in 2024 and is projected to expand at a 5.37% CAGR between 2025 and 2030.

- By geography, Asia-Pacific captured 31.6% revenue share in 2024, and North America is forecast to record the fastest regional CAGR at 4.82% through 2030.

Global Feed Prebiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on antibiotic growth-promoters | +1.8% | Global, with strongest impact in Europe, North America, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Intensifying industrial poultry and aqua farming in Asia-Pacific | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa and North America | Long term (≥ 4 years) |

| Demand for antibiotic-free meat from food-service majors | +0.9% | North America and Europe, expanding to urban centers globally | Short term (≤ 2 years) |

| Enzymatic Production Innovations Reduce Manufacturing Costs | +0.7% | Global, with manufacturing concentration in North America and Europe | Medium term (2-4 years) |

| Valorization of agro-industrial waste into prebiotic feedstocks | +0.5% | Global, with highest impact in agricultural regions | Long term (≥ 4 years) |

| Precision-biotics that target microbial metabolic pathways | +0.4% | North America and Europe initially, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Antibiotic Growth-Promoters

Regulators have systematically removed antibiotic growth promoters from feed, forcing formulators to adopt functional substitutes that protect performance. The Food and Drug Administration (FDA) Veterinary Feed Directive raised oversight costs, the European Union fully banned antimicrobial growth promoters, and China’s colistin prohibition opened an estimated USD 400 million annual window for prebiotic solutions [1]Source: UNITED STATES FOOD AND DRUG ADMINISTRATION, “Veterinary Feed Directive,” FDA.GOV. As Brazil tightens residue monitoring, prebiotics now compete head-to-head with legacy additives on total cost once compliance risk is priced in. This regulatory tightening extends beyond developed markets, with Brazil's Ministry of Agriculture implementing stricter residue monitoring protocols that favor feed additives with zero withdrawal periods. The cascading effect of these regulatory changes has fundamentally altered feed formulation economics, making prebiotics cost-competitive with traditional growth promoters when factoring in compliance and risk management costs.

Intensifying Industrial Poultry and Aqua Farming in Asia-Pacific

High-density livestock operations in the Asia-Pacific are turning to precision prebiotic programs to maintain feed efficiency under biosecure conditions. China rebuild emphasizes gut microbiome management, while Vietnam’s 8.2 million metric tons aquaculture sector uses prebiotic-enhanced rations to offset water-quality stress. India’s poultry industry, which is expanding at an annual rate of 8%, incorporates prebiotics to meet export protocols for antibiotic-free chicken. This industrialization trend extends beyond the Asia-Pacific region, with South American operations adopting similar approaches to meet growing domestic protein demand while maintaining export competitiveness.

Demand for Antibiotic-Free Meat from Food-Service Majors

Major food service corporations have implemented comprehensive antibiotic-free sourcing policies that directly influence feed additive selection throughout their supply chains. McDonald's commitment to source antibiotic-free chicken globally by 2027 has created contractual requirements for suppliers to demonstrate alternative gut health management strategies, with prebiotics representing the most technically viable solution [2]Source: MCDONALD’S CORPORATION, “Antibiotic Policy Update 2024,” MCDONALDS.COM. European retail chains have implemented similar requirements, with Tesco and Carrefour establishing supplier scorecards that evaluate antibiotic reduction efforts and reward the adoption of prebiotics through preferential sourcing agreements. This corporate policy alignment has created a premium market segment where prebiotic-supplemented products command 5-8% price premiums, justifying the additional feed costs associated with prebiotic inclusion.

Enzymatic Production Innovations Reduce Manufacturing Costs

Advances in enzymatic biorefinery technology have fundamentally altered the cost structure of complex oligosaccharide production, making previously expensive prebiotic compounds economically viable for mainstream feed applications. DSM's proprietary enzyme platform for xylo-oligosaccharide production has achieved a 30% cost reduction since 2024, primarily through improved substrate utilization and reduced processing time. The scalability of enzymatic processes has also enabled the production of specialized prebiotic blends optimized for specific animal species and production stages, creating opportunities for product differentiation and premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price-sensitivity of feed formulators | -0.8% | Global, with strongest impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Efficacy variability across livestock species and diets | -0.6% | Global, with particular challenges in diverse production systems | Medium term (2-4 years) |

| Insufficient randomized field trials for novel Beta-MOS | -0.4% | North America and Europe, where regulatory approval requires extensive data | Long term (≥ 4 years) |

| Competition from probiotics and phytogenics for budget share | -0.5% | Global, with intense competition in premium feed segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price-Sensitivity of Feed Formulators

The inherent price sensitivity of feed formulation decisions creates significant barriers to the adoption of prebiotics, particularly in markets where livestock producers operate on thin margins and prioritize immediate cost savings over long-term performance benefits. Feed typically accounts for 60-70% of total production costs in intensive livestock operations, making formulators extremely cautious about ingredient substitutions that increase per metric ton feed costs without a demonstrable return on investment. This price sensitivity has forced prebiotic manufacturers to develop lower-inclusion-rate products and combination formulations that deliver functionality at reduced cost per metric ton of feed.

Efficacy Variability across Livestock Species and Diets

The variable efficacy of prebiotic compounds across different livestock species, production systems, and dietary compositions has created skepticism among feed formulators, limiting the development of standardized application protocols. Research conducted by the University of Illinois demonstrated that fructo-oligosaccharide supplementation improved feed conversion efficiency by 12% in corn-soy diets but showed no significant benefit in wheat-based formulations, highlighting the complex interactions between prebiotic compounds and basal diet composition. This variability has led to conservative adoption patterns, where producers implement small-scale trials before committing to full-scale prebiotic programs, slowing market penetration and limiting volume growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Inulin Dominates Through Dual Functionality

Inulin retained a 25.1% share of the feed prebiotics market in 2024, leading segment growth with a 5.37% CAGR to 2030. The compound's bifidogenic properties stimulate the growth of beneficial bacteria in the gut microbiome, while its natural sweetness improves feed intake, particularly in weaning applications where feed transition stress can compromise animal performance. Fructo-oligosaccharides are driven by extensive research validation and established manufacturing infrastructure, while galacto-oligosaccharides are gaining traction in premium aquaculture applications due to their stability in aquatic environments.

Mannan-oligosaccharides continue to demonstrate strong performance in poultry applications, leveraging their pathogen-binding properties to reduce Salmonella and E. coli colonization, while xylo-oligosaccharides are emerging as cost-effective alternatives derived from agricultural waste streams. The development of enzymatic production processes has enabled the commercial viability of novel β-mannan oligosaccharides, which demonstrate enhanced binding affinity for specific pathogenic bacteria strains.

By Animal: Poultry Sector Drives Market Leadership

Poultry accounted for 46.5% of the feed prebiotics market size in 2024 and is projected to grow at a 5.40% annual rate. Broiler integrators report consistent feed conversion gains and lower mortality when prebiotics replace antibiotic growth promoters, which is particularly critical during 35-day production cycles. Layer operations are increasingly adopting prebiotic programs to maintain consistency in egg production and shell quality under intensive housing conditions, while the growing specialty poultry segment utilizes premium prebiotic formulations to meet organic and antibiotic-free certification requirements.

Ruminant applications, although smaller in market share, demonstrate significant growth potential as dairy operations seek alternatives to ionophore feed additives, which are facing regulatory scrutiny. The aquaculture segment represents the fastest-growing animal category, with shrimp farming operations adopting prebiotic-enhanced feeds to address water quality challenges and reduce disease pressure in intensive production systems.

Geography Analysis

The Asia-Pacific region maintains market leadership with a 31.6% feed prebiotics market share in 2024, reflecting its dominant livestock production base and the rapid industrialization of animal agriculture systems, which prioritize efficiency and biosecurity. China's post-African Swine Fever reconstruction has emphasized gut health management, with large-scale operations investing heavily in prebiotic programs to reduce pathogen susceptibility and maintain production targets under enhanced biosecurity protocols.

North America leads global growth at 4.81% CAGR through 2030, driven by stringent regulatory enforcement and technological innovation that positions the region as a testing ground for next-generation prebiotic applications. The United States market benefits from the FDA's implementation of the Veterinary Feed Directive, which has effectively eliminated routine antibiotic use and created structural demand for alternative gut health solutions. Prebiotics represent the most technically validated option for maintaining production efficiency.

Europe demonstrates steady market development, supported by established regulatory frameworks and consumer preferences for sustainable animal production, with particular strength in the premium and organic segments, which justify higher feed costs through product differentiation. The European Food Safety Authority's ongoing review of feed additive authorizations has consolidated market share toward proven prebiotic compounds, while the region's advanced research capabilities continue to drive innovation in targeted oligosaccharide applications.

Competitive Landscape

The feed prebiotics market exhibits a low concentration, with specialized nutrition companies and established feed additive manufacturers competing primarily on product efficacy, technical support capabilities, and regulatory compliance, rather than price alone. The competitive dynamics are increasingly influenced by companies' ability to demonstrate consistent animal performance outcomes through field trials and provide species-specific formulation guidance, which differentiates proven prebiotic products from generic oligosaccharide suppliers.

DSM-Firmenich AG, Biochem Zusatzstoffe Handels- und Produktionsgesellschaft mbH, Vetanco SA, Land O'Lakes, Inc., and Alltech, Inc. collectively controlled a significant share of the 2024 value, achieving scale economies through vertical integration and multi-species R&D pipelines [3]Source: INTERNATIONAL FEED INDUSTRY FEDERATION, “Global Feed Production Survey 2024,” IFIF.ORG. Their competitive moat extends beyond product catalogs to on-farm advisory services that lock in customer loyalty.

Emerging opportunities exist in precision nutrition applications where companies like Kemin Industries and BENEO leverage their specialized prebiotic portfolios to address specific gut health challenges across different livestock species and production systems. The market has witnessed an increased focus on product differentiation through proprietary prebiotic blends and targeted delivery systems, with companies such as Novus International and Adisseo developing species-specific formulations that optimize prebiotic efficacy for specific animal categories.

Feed Prebiotics Industry Leaders

Alltech, Inc.

Land O'Lakes, Inc.

DSM-Firmenich AG

Vetanco SA

Biochem Zusatzstoffe Handels- und Produktionsgesellschaft mbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: De Heus Animal Nutrition established a new animal feed factory in Punjab. The facility, constructed with an investment of USD 17 million, ranks among India's largest and most technologically advanced feed manufacturing units. The factory has an installed capacity of 180 thousand metric tons and features dedicated production lines for feed prebiotics.

- August 2025: DSM Nutritional Products has committed USD 50 million to expand xylo-oligosaccharide capacity at Delft, targeting the Asian aquaculture market.

- March 2024: Alltech inaugurated a USD 40 million prebiotic plant in Thailand to serve the poultry and aquaculture customers of Southeast Asia.

Global Feed Prebiotics Market Report Scope

| Fructo-oligosaccharides |

| Galacto-oligosaccharides |

| Inulin |

| Lactulose |

| Mannan Oligosaccharides |

| Xylo Oligosaccharides |

| Other Prebiotics |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Australia | |

| Philippines | |

| Rest of Asia-Pacific | |

| Middle East | Iran |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | Egypt |

| Kenya | |

| South Africa | |

| Rest of Africa |

| Sub Additive | Fructo-oligosaccharides | |

| Galacto-oligosaccharides | ||

| Inulin | ||

| Lactulose | ||

| Mannan Oligosaccharides | ||

| Xylo Oligosaccharides | ||

| Other Prebiotics | ||

| Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East | Iran | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What growth rate is projected for the feed prebiotics market to 2030?

The feed prebiotics market is forecast to expand at a 5.13% CAGR through 2030.

Which region currently dominates demand for livestock prebiotics?

Asia-Pacific accounts for 31.6% of global demand due to its large livestock base and rapid farm industrialization.

Why are poultry producers the biggest users of prebiotics?

Poultry farms rely on prebiotics to maintain feed conversion and meet antibiotic-free standards in fast 35-day cycles.

How have enzyme technologies affected prebiotic pricing?

Enzymatic biorefineries have lowered mannan- and xylo-oligosaccharide costs 15-20% since 2024, improving affordability.

Page last updated on: