Feed Probiotics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

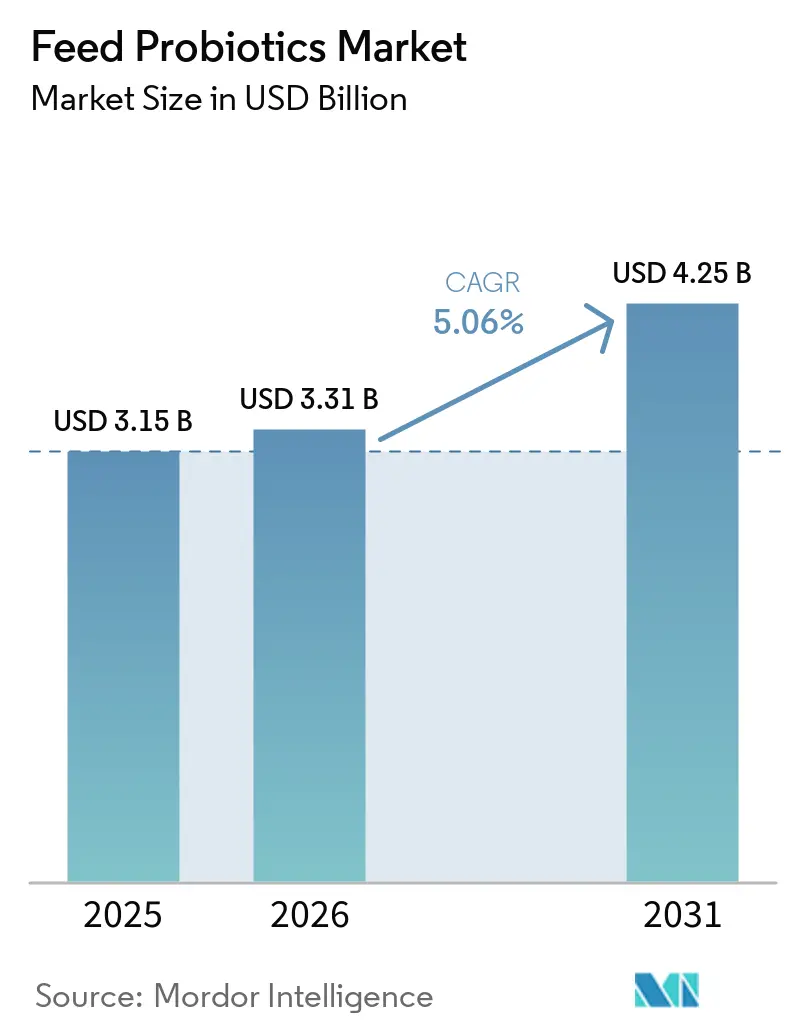

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 4.25 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Probiotics Market Analysis by Mordor Intelligence

The feed probiotics market size was valued at USD 3.15 billion in 2025 and is projected to grow from USD 3.31 billion in 2026 to USD 4.25 billion by 2031, with a CAGR of 5.06% during 2026 to 2031. This growth is driven by the shift among livestock producers away from antibiotic growth promoters (AGPs) and the implementation of stricter regulations on antimicrobial use in feed programs across major producing countries. Additionally, the increasing scale of poultry, swine, ruminant, and aquaculture systems is boosting demand for consistent feed efficiency and gut health solutions to maintain profit margins. Suppliers with comprehensive biosolutions portfolios are gaining a competitive advantage as customers prefer purchasing probiotics alongside enzymes and other nutritional tools from a single vendor. The market is also benefiting from advancements such as heat-stable Bacillus products that remain viable during pelleting processes and new regulatory approvals that expand the range of commercial strains available for various animal categories. These factors are contributing to the steady growth of the feed probiotics market, favoring companies that excel in fermentation capabilities, regulatory expertise, and field support.

Key Report Takeaways

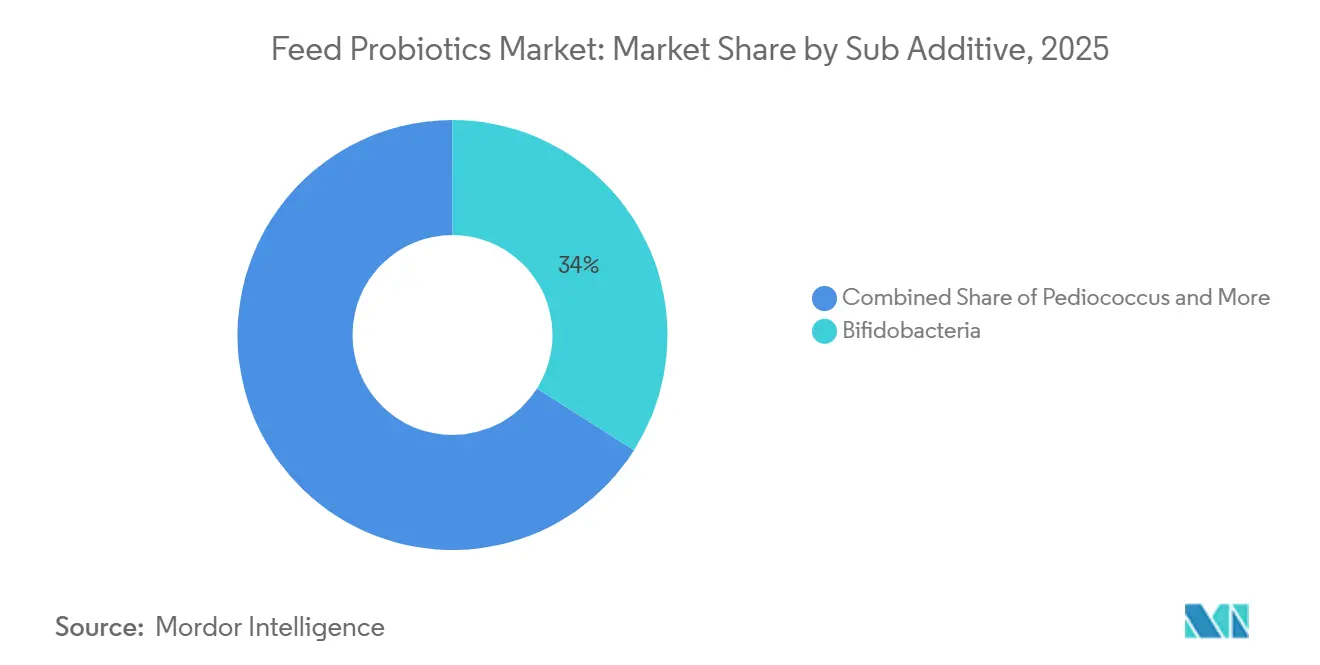

- By sub additive, feed probiotics market share for bifidobacteria accounted for the largest 34.0% in 2025, and the bifidobacteria market size is projected to grow at the fastest 5.4% CAGR from 2026 to 2031.

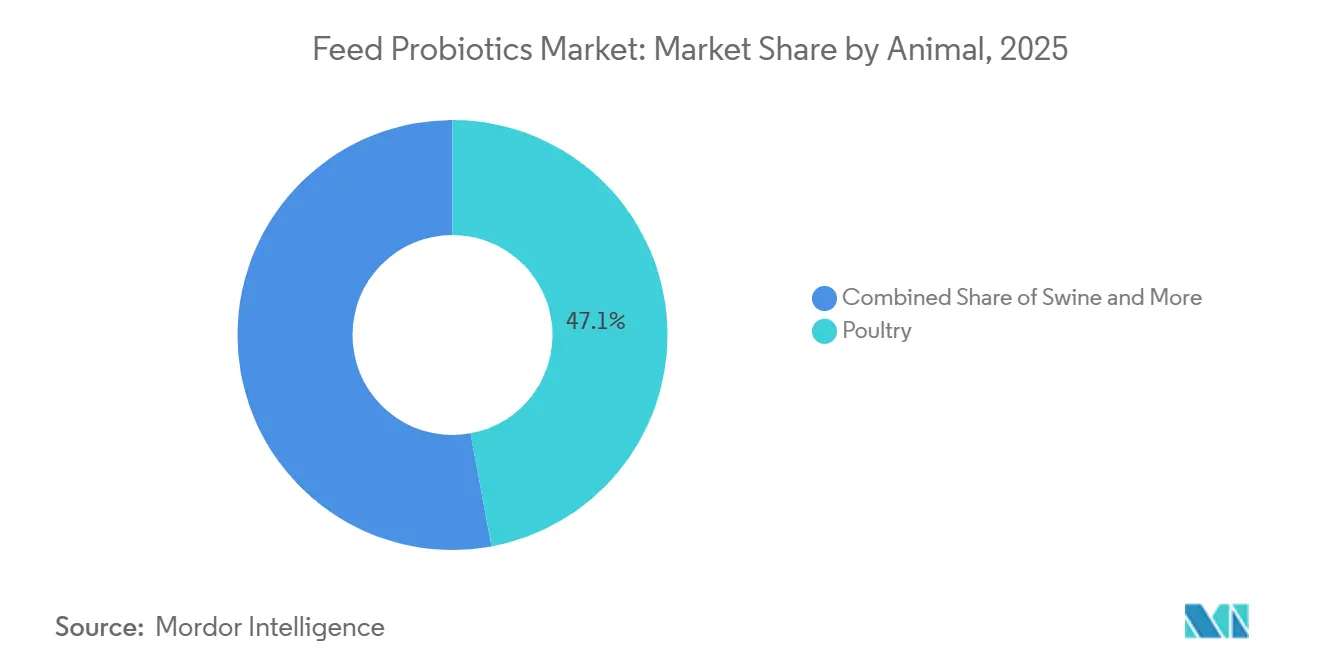

- By animal, the feed probiotics market share for poultry held the largest 47.1% in 2025, and the poultry market size is forecast to expand at the fastest 5.2% CAGR from 2026 to 2031.

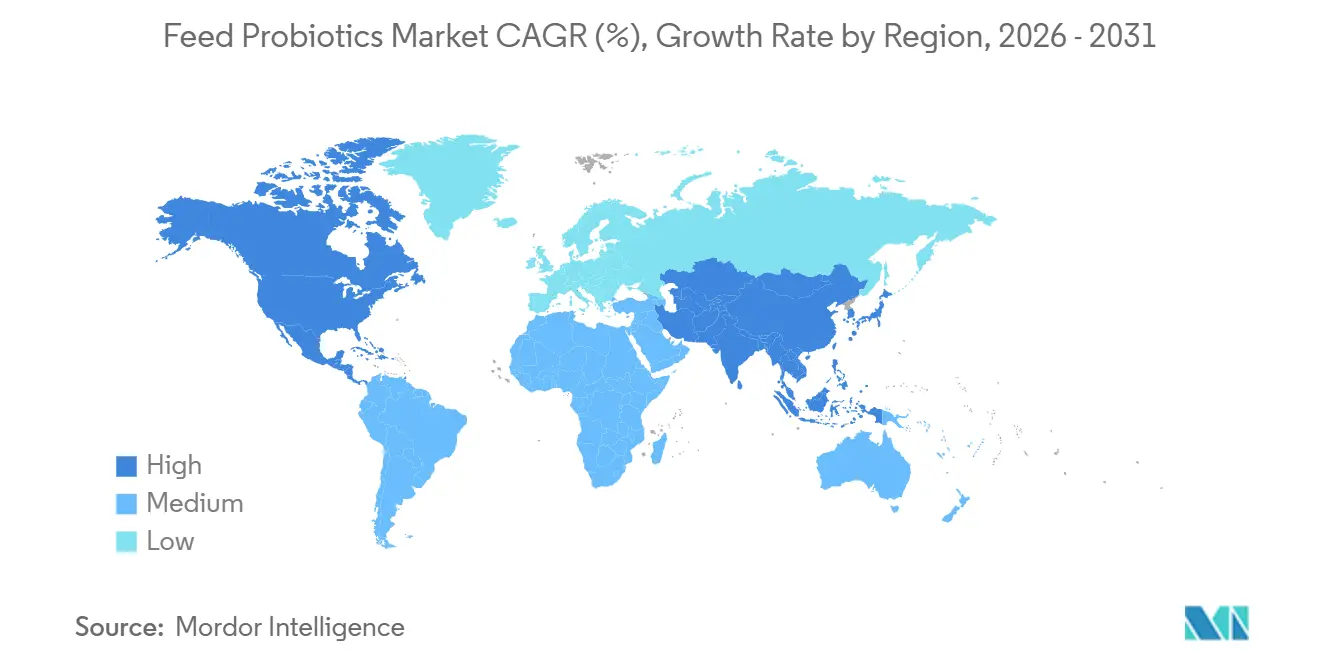

- By geography, the feed probiotics market share for Asia-Pacific accounted for the largest 32.5% in 2025, and the feed probiotics market size for North America is projected to grow at the fastest 5.5% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Feed Probiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antibiotic-growth-promoter restrictions and antibiotic-free production | +1.5% | Global | Medium term (2-4 years) |

| Poultry production scale and feed efficiency focus | +1.2% | Global, led by Americas and Asia-Pacific | Short term (≤ 2 years) |

| Asia-Pacific livestock and aquaculture intensification | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Better heat-stable Bacillus and dry-format formulations | +0.7% | Global | Medium term (2-4 years) |

| Carbon-intensity reduction and Scope 3 pressure in animal protein | +0.5% | North America and European Union, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shrimp disease management and water-quality programs | +0.4% | Asia-Pacific and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Antibiotic-Growth-Promoter Restrictions and Antibiotic-Free Production

Restrictions on antibiotic growth promoters are driving increased demand in the feed probiotics market, as livestock producers seek non-antibiotic alternatives to support gut health and production performance. The Food Safety and Standards Authority of India (FSSAI) has announced restrictions, effective April 1, 2025, banning the use of several medically important antibiotics in food-producing animals[1]Source: Food Safety and Standards Authority of India (FSSAI), “First Amendment Regulations, 2024 on Antibiotic and Crop Contaminant Limits,” fssai.gov.in.. This regulatory change is encouraging the adoption of probiotic-based feed additives as replacement solutions. The demand for Bacillus- and Lactobacillus-based probiotics is rising, as these products enhance feed efficiency, digestive stability, and animal health without relying on antibiotic growth promoters.

Poultry Production Scale and Feed Efficiency Focus

The scale of poultry production continues to drive strong demand in the feed probiotics market, as broiler operations rely heavily on feed efficiency and production optimization. According to the United States Department of Agriculture (USDA) Foreign Agricultural Service (FAS), global chicken meat production is projected to reach 110.7 million metric tons by 2026, reflecting a 3% increase from the previous year[2]Source: Food Safety and Standards Authority of India (FSSAI), “Food Safety and Standards (Contaminants, Toxins and Residues) First Amendment Regulations, 2024,” fssai.gov.in. This growth is primarily attributed to expansions in China, Brazil, and the United States. The rising poultry output at this level is increasing the demand for probiotic feed additives, which support gut health, enhance nutrient utilization, and ensure production consistency in intensive broiler systems.

Asia-Pacific Livestock and Aquaculture Intensification

The Asia-Pacific region continues to be a significant driver of growth in the feed probiotics market, driven by the rapid expansion of livestock and aquaculture production. This growth is increasing the demand for feed efficiency and animal-health solutions. According to the Organisation for Economic Co-operation and Development (OECD)-Food and Agriculture Organization (FAO) Agricultural Outlook 2025–2034, India and Southeast Asian countries are projected to contribute 39% of global food consumption growth by 2034, up from 32% in the previous decade[3]Source: United States Department of Agriculture Foreign Agricultural Service (FAS), “Livestock and Poultry: World Markets and Trade,” April 2025, apps.fas.usda.gov. This intensification in production is fostering the wider adoption of probiotic feed additives in poultry, shrimp, fish, and livestock systems to enhance gut health, nutrient utilization, and overall production performance.

Better Heat-Stable Bacillus and Dry-Format Formulations

Advancements in heat-stable Bacillus products have addressed a significant technical challenge that previously constrained the feed probiotics market. Pelleted feed production often involves temperatures reaching up to 95°C, which can harm live microbes that are not designed to withstand heat and moisture. The launch of Novonesis A/S’s Bovacillus in the European Union in April 2026 highlights the growing importance of heat stability as a commercial standard, and it is designed for use in pellets, premixes, total mixed rations, mineral blocks, and liquid feed formats, and is specified to remain stable at temperatures up to 95°C. This development is significant because feed mills prefer products that integrate seamlessly into their standard manufacturing processes without incurring additional coating costs or handling complexities. With the introduction of more stable dry-form products, the feed probiotics market is better positioned to cater to ruminant, swine, and aquafeed users more effectively than before.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Field-level strain performance variability | -0.6% | Global | Short term (≤ 2 years) |

| Multi-jurisdiction microbial registration burden | -0.5% | Global, particularly European Union, United States, India, and Japan | Medium term (2-4 years) |

| Pelleting and storage viability losses for non-spore strains | -0.4% | Global | Short term (≤ 2 years) |

| Postbiotic and paraprobiotic substitution risk | -0.3% | European Union and North America, early-stage Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Field-Level Strain Performance Variability

Field-level performance variability poses a significant challenge for the feed probiotics market, as the efficacy of probiotics can vary widely across different commercial farming environments. A 2025 meta-analysis published in Frontiers in Animal Science by researchers from Universidad de Chile, Santiago, Chile, found that Bacillus-based probiotics increased broiler body weight gain by an average of 152 g, while Lactobacillus-based probiotics demonstrated an average improvement of 221.6 g under the analyzed trial conditions. These variations in results across probiotic strains and production environments can undermine confidence among livestock producers, limiting repeat usage and impeding the broader commercialization of feed probiotic products.

Multi-Jurisdiction Microbial Registration Burden

Multi-jurisdictional microbial registration requirements continue to act as a significant restraint on the feed probiotics market. Probiotic approvals are strain-specific and are regulated independently across major markets. For instance, in the European Union, the Commission Implementing Regulation (EU) 2025/1468 approved the use of Bacillus subtilis DSM 33862 and Lentilactobacillus buchneri DSM 12856 only after undergoing a comprehensive evaluation and regulatory review by the European Food Safety Authority (EFSA). These strain and country-specific approval processes increase compliance costs and extend commercialization timelines, particularly for smaller probiotic manufacturers with limited regulatory resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Bifidobacteria Leads in Share and Growth

The feed probiotics market share for bifidobacteria held the largest 34.0% in 2025. This dominance is attributed to their extensive commercial application in poultry, swine, calf, and aquaculture nutrition programs, where digestive stability and early-life gut health are key priorities. Suppliers are increasingly developing multi-strain probiotic formulations that combine bifidobacteria with Lactobacillus and Bacillus species to enhance microbial stability and feed performance across various animal systems. Additionally, the category benefits from established regulatory acceptance in major livestock-producing countries, facilitating adoption by integrated feed manufacturers and large-scale animal protein producers globally.

The feed probiotics market size for bifidobacteria is forecast to grow at the fastest 5.4% CAGR from 2026 to 2031. This growth is driven by an increasing emphasis on microbiome management in young animals, particularly in calf starters, nursery pig diets, hatchery nutrition programs, and aquaculture feeds. Producers are focusing on probiotic solutions that enhance digestive efficiency and support antibiotic-reduced production systems without compromising productivity. Competitive strategies are shifting toward scientifically validated strain combinations and heat-stable formulations that align with commercial feed processing requirements. These developments are promoting broader adoption of bifidobacteria-based products across established livestock industries and emerging aquaculture sectors worldwide.

By Animal: Poultry Leads in Scale and Growth

The feed probiotics market share for poultry accounted for the largest 47.1% in 2025. Poultry remains the leading consumer segment due to the high feed efficiency, rapid production cycles, and reduced antibiotic dependence required in broiler and layer systems within intensive farming operations. Large commercial poultry producers increasingly adopt probiotic supplementation to enhance digestive performance, ensure flock consistency, and maintain production stability under high-density conditions. Broiler systems are particularly significant, as even minor improvements in feed conversion and bird performance yield substantial operational value across multiple annual production cycles. Additionally, layer operations contribute to consistent demand through long-cycle nutritional management and global gut-health optimization programs.

The poultry market size is projected to grow at the fastest 5.2% CAGR from 2026 to 2031. This growth is driven by increasing demand for poultry meat, the continued expansion of integrated broiler systems, and the rising adoption of antibiotic-reduced production models in major producing countries. Probiotic suppliers are enhancing poultry-focused product portfolios by introducing heat-stable strains, water-soluble formats, and multi-species microbial combinations tailored for modern feed manufacturing systems. While aquaculture and swine applications are also experiencing steady growth, poultry remains the primary focus of technical investment and commercial development due to its production scale and faster adoption cycle globally.

Geography Analysis

Asia-Pacific accounted for the largest geographic share of the feed probiotics market, holding 32.5% in 2025. This dual leadership is attributed to the region's dominance in both aquaculture and terrestrial livestock categories. According to the United States Department of Agriculture (USDA), China remains the largest single-country demand center for probiotics in the region, driven by its position as the world's second-largest chicken meat producer, forecasted at 17.3 million metric tons in 2026. In Southeast Asia, shrimp-producing nations such as Thailand, Vietnam, Indonesia, and the Philippines represent a concentrated demand for probiotics, with acute hepatopancreatic necrosis disease (AHPND) biosecurity programs driving the use of Bacillus and Lactobacillus solutions in feed and pond-water applications.

North America is projected to grow at the fastest 5.5% CAGR from 2026 to 2031 and ranks as a technically advanced and high-value market, with the United States accounting for the world's largest single-country chicken meat production. This growth is supported by large commercial livestock operations, widespread adoption of precision nutrition programs, and rising demand for antibiotic-reduced animal production systems. According to the United States Department of Agriculture Foreign Agricultural Service, United States chicken meat production is forecast to increase from 21.7 million metric tons in 2025 to 22.2 million metric tons in 2026, creating a significant commercial base for probiotic feed additives in poultry production. Additionally, large integrated feed and livestock companies are investing in direct-fed microbial programs to improve feed efficiency and optimize gut health.

South America continues to contribute meaningful commercial demand through export-oriented poultry and swine production systems, particularly in Brazil and Argentina. Europe remains a mature region supported by long-standing antimicrobial reduction policies, advanced feed manufacturing standards, and strong regulatory oversight for microbial products. Meanwhile, the Middle East and Africa are gradually increasing their adoption of feed probiotics, driven by expanding poultry integration, aquaculture investments, and compound feed production in selected countries. Key demand centers in this region include Saudi Arabia, Turkey, South Africa, and Egypt, where commercial livestock operators are focusing on feed efficiency, digestive stability, and non-antibiotic nutritional solutions to support modern intensive animal production systems.

Competitive Landscape

The feed probiotics market reamined moderately fragmented structure where multinational suppliers hold stronger positions than regional manufacturers because of larger fermentation capacity, broader microbial strain libraries, and stronger regulatory capabilities. Key players such as Novozymes A/S, DSM-Firmenich AG, Evonik Industries AG, International Flavors & Fragrances Inc., and Archer Daniels Midland Company compete through advancements in strain development, technical support, and expansive distribution networks.

Competitive activity is increasingly focused on improving strain stability, feed-processing compatibility, and species-specific product positioning across poultry, swine, ruminant, and aquaculture applications. Major suppliers are investing in heat-stable Bacillus products, multi-strain microbial blends, and precision fermentation technologies tailored for commercial feed manufacturing. Additionally, companies are bolstering their technical-service networks and demonstration programs to improve customer retention and validate product performance under real-world farming conditions.

Strategy within the feed probiotics market is shifting toward integrated nutritional platforms, regional manufacturing expansion, and closer collaboration with commercial feed producers. In March 2024, Evonik Industries AG and Qingdao Vland Biotech Group Co., Ltd. commenced operations of their joint venture in China to enhance probiotics production and regional supply capabilities for livestock nutrition. Furthermore, larger companies are expanding digital farm-support programs and microbiome-based nutritional services to strengthen product differentiation. Competitive advantage increasingly hinges on securing regulatory approvals, achieving consistent large-scale manufacturing, and demonstrating measurable performance in intensive commercial production environments.

Feed Probiotics Industry Leaders

Novonesis A/S

DSM-Firmenich AG

Evonik Industries AG

International Flavors & Fragrances Inc.

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Commission Implementing Regulation (European Union) 2026/1037 authorized the use of Enterococcus lactis NCIMB 10415 as a feed additive for all animal species within the European Union. This regulatory development broadens the range of commercially available Enterococcus strains and facilitates market entry across various livestock categories in the European Union.

- April 2026: Novonesis A/S introduced Bovacillus in the European Union, marking it as the first Bacillus-based probiotic specifically registered for lactating dairy cows in the region. The product is heat-stable up to 95°C and can be used in pellets, premixes, total mixed rations, mineral blocks, and liquid feed formats.

- November 2025: Evonik Industries AG has launched an improved formulation of its Ecobiol Bacillus CECT 5940 probiotic for poultry nutrition, achieving a 46% faster outgrowth compared to earlier competitor probiotic products. This enhanced gut colonization speed improves early-life feed efficiency metrics in broilers during the crucial first days post-hatch.

Global Feed Probiotics Market Report Scope

Feed probiotics are live microorganisms incorporated into animal feed to enhance gut health, digestion, nutrient absorption, and overall animal performance. They are commonly utilized in poultry, swine, ruminants, and aquaculture to improve feed efficiency, support immunity, and facilitate antibiotic-reduced production systems. The feed probiotics market report is segmented by sub additive (bifidobacteria, enterococcus, lactobacilli, pediococcus, streptococcus, and other probiotics), by animal (aquaculture, poultry, ruminants, swine, and other animals), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Bifidobacteria |

| Enterococcus |

| Lactobacilli |

| Pediococcus |

| Streptococcus |

| Other Probiotics |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Australia | |

| Philippines | |

| Rest of Asia-Pacific | |

| Middle East | Iran |

| Turkey | |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | Egypt |

| Kenya | |

| South Africa | |

| Rest of Africa |

| By Sub Additive | Bifidobacteria | |

| Enterococcus | ||

| Lactobacilli | ||

| Pediococcus | ||

| Streptococcus | ||

| Other Probiotics | ||

| By Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East | Iran | |

| Turkey | ||

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of feed probiotics market in 2026?

The feed probiotics market size stands at USD 3.31 billion in 2026.

Which animal group creates the most demand for feed probiotics?

Poultry is the largest animal segment, with 47.1% market share in 2025.

Which sub additive is leading sales and growth?

Bifidobacteria market share led with the largest 34.0% in 2025

Why is Asia-Pacific the largest regional opportunity?

Asia-Pacific held the largest 32.5% market share in 2025 because it combines large livestock output with fast-growing aquaculture and rising protein demand, especially across China, India, and Southeast Asia.

Page last updated on: