Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

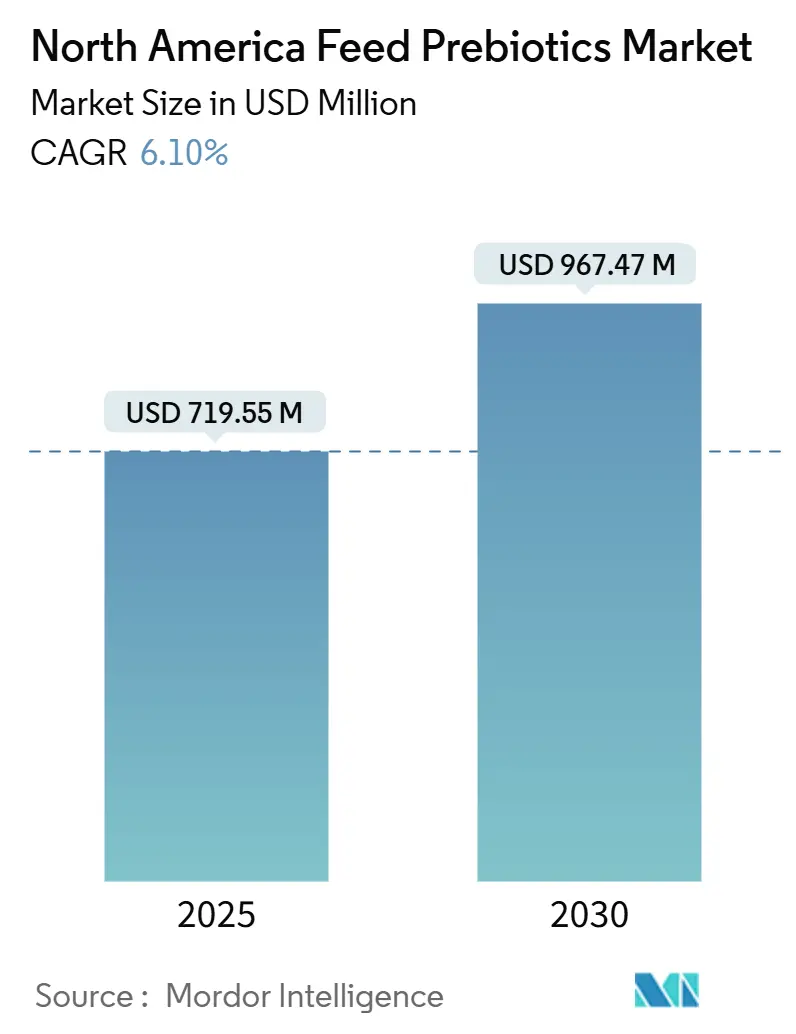

| Market Size (2025) | USD 719.5 Million |

| Market Size (2030) | USD 967.40 Million |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Feed Prebiotics Market Analysis by Mordor Intelligence

The North America feed prebiotics market size is USD 719.5 million in 2025 and is projected to reach USD 967.4 million by 2030, at a 6.10% CAGR during the forecast period (2025-2030). This growth trajectory reflects the region's accelerating shift from traditional antibiotic growth promoters toward functional gut-health solutions, driven by regulatory tightening and producer demands for sustainable livestock performance. The market's evolution demonstrates how regulatory pressure can catalyze innovation, as the Food and Drug Administration's (FDA)Veterinary Feed Directive restrictions have fundamentally altered feed additive procurement strategies across North American livestock operations [1]Source: U.S. Food and Drug Administration, “Veterinary Feed Directive,” fda.gov . Investment in heat-stable encapsulation and precision fermentation broadens product functionality while protecting margins. Strategic e-commerce channels shorten the route to independent farms, improving transparency and technical support. Producers are increasingly favoring documented gut-health solutions that can withstand pelleting temperatures and volatile raw material costs.

Key Report Takeaways

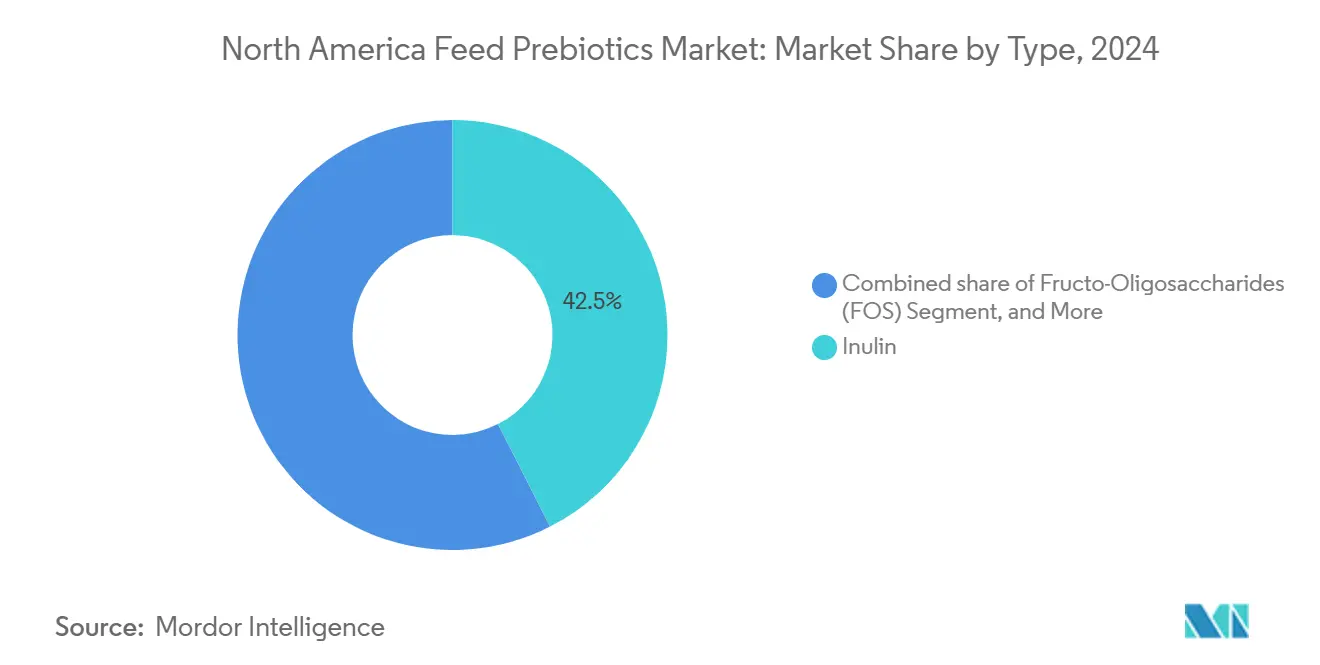

- By type, inulin led with 42.5% North America feed prebiotics market share in 2024, while MOS (Mannan-Oligosaccharides) is forecast to expand at a 9.8% CAGR through 2030.

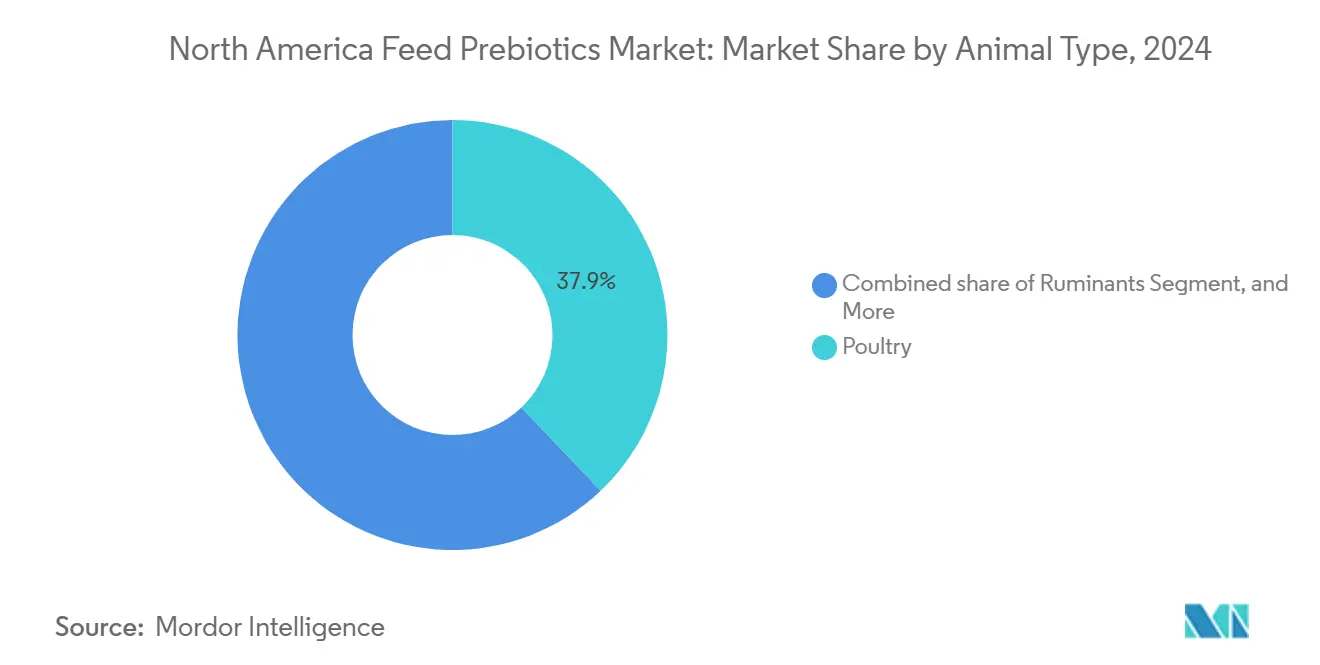

- By animal type, poultry captured 37.9% of the North America feed prebiotics market size in 2024, while aquaculture is forecast to expand at an 8.5% CAGR through 2030.

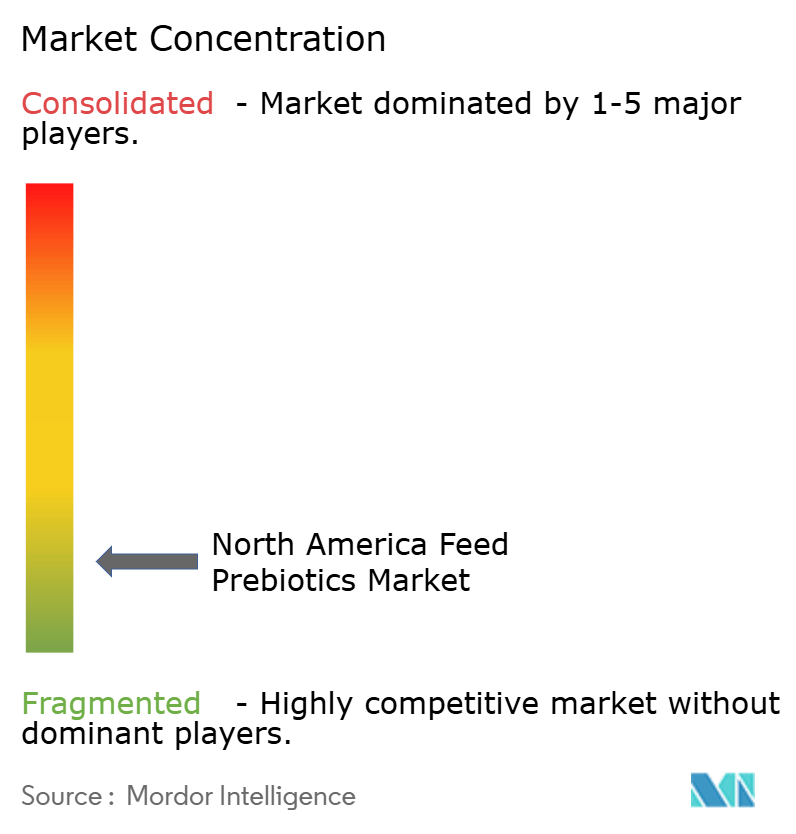

- The major players in the market studied are Cargill, Incorporated, DSM-Firmenich AG, Alltech Incorporated, Nutreco N.V., and Land O’Lakes Incorporated, confirming a moderately concentrated landscape in 2024.

North America Feed Prebiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for high-quality animal protein | +1.2% | United States and Canada, with spillover to Mexico | Medium term (2-4 years) |

| Stricter antibiotic-use regulations in livestock production | + 1.8% | United States primary, Canada secondary, Mexico emerging | Short term (≤ 2 years) |

| Rising compound-feed output and feed-mill modernization | + 1.1% | North America overall, concentrated in Midwest and Prairie provinces | Medium term (2-4 years) |

| Government incentives for gut-health additives | +0.9% | United States United States Department of Agriculture programs, Canadian provincial support | Long term (≥ 4 years) |

| Rapid adoption of heat-stable encapsulated prebiotics | +0.7% | United States poultry belt, expanding to Canada | Short term (≤ 2 years) |

| E-commerce channels enabling direct-to-farm additive sales | +0.5% | Rural United States and Western Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Quality Animal Protein

Consumer preferences for premium meat and dairy products drive livestock producers toward functional feed additives that enhance product quality and nutritional profiles. This trend particularly benefits prebiotic manufacturers as producers seek documented improvements in feed conversion efficiency and animal welfare metrics. Regulatory influence from the United States Department of Agriculture (USDA) organic standards and voluntary certification programs, such as Animal Welfare Approved, further incentivize the adoption of prebiotics. This consumer-driven pull-through effect creates sustainable demand for livestock products with documented prebiotic supplementation.

Stricter Antibiotic-Use Regulations In Livestock Production

Federal and state-level restrictions on antibiotic growth promoters have fundamentally altered North American livestock nutrition strategies, creating mandatory demand for alternative performance enhancers. The regulatory framework creates competitive advantages for early adopters who develop expertise in prebiotic formulation and application, as compliance becomes a market entry barrier. The Canadian Food Inspection Agency's alignment with Food and Drug Administration (FDA) standards, as outlined in the Feeds Regulations 2024, ensures cross-border regulatory consistency, facilitating market expansion for established prebiotic suppliers. The Food and Drug Administration (FDA) Veterinary Feed Directive, implemented in 2017 and continuously tightened, requires veterinary oversight for medicated feeds, increasing compliance costs and operational complexity for producers. State-level initiatives, including California's livestock antibiotic restrictions, create additional regulatory pressure that extends beyond federal mandates.

Rising Compound-Feed Output and Feed-Mill Modernization

North American feed mill capacity expansion and technology upgrades create infrastructure capable of handling specialized additives like encapsulated prebiotics. Feed mill consolidation among major integrators creates purchasing power that favors established prebiotic suppliers with proven supply chain reliability. Cargill, Incorporated acquisition of two United States feed mills from Compana Pet Brands in September 2024, including the modernization of the Denver facility as a flagship operation, exemplifies the industry's infrastructure investment in value-added feed production. The trend toward larger, more sophisticated feed manufacturing operations creates economies of scale that make prebiotic inclusion more cost-effective for producers.

Government Incentives for Gut-Health Additives

The United States Department of Agriculture (USDA) programs and provincial agricultural support mechanisms increasingly recognize functional feed additives as sustainability and animal welfare enhancement tools. Federal research grants through the National Institute of Food and Agriculture specifically target alternatives to antimicrobial growth promoters, creating funding opportunities for prebiotic research and commercialization. State-level initiatives, including tax incentives for livestock operations adopting verified animal welfare practices, indirectly support prebiotic adoption through cost-offset mechanisms. The proposed Innovative FEED Act could streamline approvals and reduce filing costs. Alberta and Ontario offer parallel support, giving Canadian suppliers confidence in long-term demand visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and fragmented North American regulatory landscape | -0.8% | United States, Canada, and Mexico with varying intensity | Short term (≤ 2 years) |

| Volatility in chicory-root and yeast-derivative input prices | -0.6% | North America overall, with supply chain dependencies | Medium term (2-4 years) |

| Fermentation-grade sugar bottlenecks for GOS production | -0.4% | United States and Canada production centers | Medium term (2-4 years) |

| Limited ROI data for small-scale poultry producers | -0.3% | Rural United States and smaller Canadian operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex and Fragmented North American Regulatory Landscape

The termination of the Food and Drug Administration's (FDA) formal agreement in October 2024 creates regulatory uncertainty, which delays new product approvals and increases compliance costs for manufacturers of prebiotics. Differing requirements across the Food and Drug Administration's (FDA), Canadian Food Inspection Agency's (CFIA), and Secretariat of Agriculture, Livestock, Rural Development, Fisheries, and Food's (SAGARPA) jurisdictions force companies to navigate multiple approval pathways, which extend the time-to-market and inflate development costs. Mexico's NOM-012-SAG/ZOO-2020 implementation introduces additional complexity, as the oversight requirements of Secretariat of Agriculture, Livestock, Rural Development, Fisheries and Food/ National Agro-Alimentary Health, Safety and Quality Service (SAGARPA/SENASICA) differ from those established in the United States and Canada [2]Source: Servicio Nacional de Sanidad, “NOM-012-SAG/ZOO-2020,” senasica.gob.mx. Divergent data requirements extend time-to-market and inflate consulting costs. Novel fermentation molecules face the steepest hurdles, which can depress near-term pipeline launches.

Volatility In Chicory-Root and Yeast-Derivative Input Prices

Raw material price fluctuations for key prebiotic feedstocks create margin pressure and supply chain uncertainty that constrains market expansion. Chicory root availability is influenced by European agricultural conditions and competing demand from food and beverage applications, resulting in price volatility that affects inulin and FOS production costs. Yeast derivative pricing reflects broader dynamics within the fermentation industry, including competition from biofuel and pharmaceutical applications that can outbid feed additive manufacturers during supply constraints. BENEO’s capacity build in Chile diversifies sourcing yet foreign exchange swings add hedging expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Inulin Dominance Faces MOS (Mannan-Oligosaccharides) Challenge

Inulin captured 42.5% of the North America feed prebiotics market size in 2024, benefiting from established chicory supply and a well-documented safety profile. Suppliers invest in precision fermentation to tailor carbohydrate chain length for species-specific efficacy. Meanwhile, Xylo-Oligosaccharides (XOS) and lactulose remain niche due to higher costs and tighter regulatory vetting. Fructo-Oligosaccharides (FOS) and Galacto-Oligosaccharides (GOS) occupy specialized niches in poultry and dairy applications, respectively, with FOS particularly valued for its dual prebiotic and sweetening properties. Production costs and regulatory approval timelines currently limit the use of xylo-oligosaccharides (XOS), whereas lactulose primarily serves pharmaceutical-adjacent applications with limited feed market penetration.

MOS (Mannan-Oligosaccharides) is projected to record a 9.8% CAGR through 2030. This shift reflects the demand for ingredients that withstand pelleting and support immune modulation. The competitive shift toward MOS (Mannan-Oligosaccharides) reflects its documented immune-modulating properties and heat stability advantages in pelleted feeds. Layn Natural Ingredients' expansion of biotechnology facilities for precision-fermented ingredients, including their new Galacan beta-glucan alternative, demonstrates industry movement toward engineered prebiotic molecules with enhanced bioavailability.

By Animal Type: Poultry Leadership Drives Innovation

Poultry applications account for 37.9% of the North America feed prebiotics market size in 2024, reflecting the sector's advanced nutrition management and documented ROI (Return on Investment) capabilities. The poultry sector's leadership stems from integrator-driven adoption of precision nutrition strategies and standardized performance measurement protocols. Swine operations are showing an increasing adoption of nursery diets, particularly for those transitioning away from zinc oxide and antibiotic growth promoters.

Aquaculture emerges as the fastest-growing segment, with an 8.5% CAGR, driven by regulatory restrictions on medicated feeds and the expansion of North American fish farming operations. Aquaculture growth reflects the expansion of salmon farming in Atlantic Canada and increasing regulatory pressure to reduce antibiotic use in fish production systems. As humanization trends spill into pet aisles, branded GOS and FOS achieve retail visibility, indirectly supporting the scale of feed-grade production.

Geography Analysis

The United States dominates the North American feed prebiotics market with the largest share of 80% in 2024, driven by advanced livestock integration, regulatory pressure from the Food and Drug Administration (FDA's) Veterinary Feed Directive, and sophisticated feed mill infrastructure capable of handling specialized additives [3]Source: U.S. Food and Drug Administration, “Veterinary Feed Directive,” fda.gov . United States market leadership reflects early adoption of antibiotic alternatives following federal restrictions and state-level initiatives that create mandatory demand for functional feed ingredients.

Canada represents an emerging market, supported by the expansion of livestock sectors in Alberta and Ontario, as well as regulatory alignment with United States standards through the CFIA Feeds Regulations 2024. The country's prairie provinces benefit from their proximity to grain production and established feed mill networks, which facilitate the adoption of prebiotics in cattle and swine operations. Canadian market development reflects provincial agricultural support programs that incentivize sustainable production practices, including the adoption of functional feed additives.

Mexico projects strong growth 8.8% CAGR through 2030, opportunity with increasing regulatory sophistication under Secretariat of Agriculture, Livestock, Rural Development, Fisheries and Food/ National Agro-Alimentary Health, Safety and Quality Service (SAGARPA/SENASICA) oversight and expanding poultry and swine production capacity. The country's livestock sector modernization includes adoption of international nutrition standards and quality control protocols that facilitate prebiotic integration. Mexican market development benefits from United States-Mexico-Canada Agreement (USMCA) trade provisions that reduce barriers for feed additive imports while encouraging technology transfer from the United States and Canadian suppliers.

Competitive Landscape

The North America feed prebiotics market is moderately concentrated, with the top global and regional players competing fiercely with local players. The focus on quality, through extensive investment in product R&D, is the most widely adopted strategy among leading players worldwide. The major investments are directed toward product-line expansions and the innovation of new products to expand the customer base. The major players in the market studied are Cargill, Incorporated; DSM-Firmenich AG, Alltech Incorporated; Nutreco N.V., and Land O’Lakes Incorporated.

Mid-tier firms, including Lesaffre, ADM, and EW Nutrition, specialize in yeast cell walls and plant extracts that target immunity, often gaining share in aquaculture and specialty livestock. Smaller disruptors use precision fermentation to create customized oligosaccharide profiles, narrowing gaps in functional specificity. Technology barriers such as encapsulation know-how and regulatory dossiers protect incumbents, yet e-commerce erodes traditional dealer loyalty and opens space for agile challengers.

Future competition will revolve around data-driven proof of efficacy, green-sourced inputs, and integrated additive packs that combine prebiotics with probiotics or enzymes for bundled performance claims. Suppliers able to certify life-cycle footprints and align with retailer sustainability scorecards will command price premiums.

North America Feed Prebiotics Industry Leaders

Cargill Incorporated

DSM-Firmenich AG

Alltech Incorporated

Nutreco N.V.

Land O’Lakes Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2023: Novozymes formed a partnership with Bactolife, a Danish industrial biotechnology company, to develop and launch Ablacto, a prebiotic solution that improves gut stability in piglets and reduces the severity of post-weaning diarrhea (PWD).

- May 2023: DSM and Firmenich merged and established a new company called DSM-Firmenich. The goal of this merger was to develop the company as an industry leader across flavors, fragrances, and nutritional ingredients segments, including prebiotics feed additives. The shareholders of DSM own about 65.5% of the shares in DSM-Firmenich, while Firmenich shareholders hold about 34.5%.

- February 2023: Nutreco and the US-based company BiomEdit partnered to transform feed additives including its prebiotics range through Biome-actives. This collaboration brings together BiomEdit’s state-of-the-art microbiome discovery platform and Nutreco’s customer access and distribution capabilities.

North America Feed Prebiotics Market Report Scope

Feed prebiotics is non-digestable dietary fibres that promote the growth of beneficial gut bacteria, enhancing animal health and feed efficiency. The North America Feed Prebiotics Market is segmented by Type (Inulin, Fructo-Oligosaccharides, Galacto-Oligosaccharides, Xylo-Oligosaccharides, Mannan-Oligosaccharides, Lactulose, and Other Types), Animal Type (Ruminants, Poultry, Swine, Aquaculture, and Other Animal Types), and Geography (United States, Canada, Mexico, and Rest of North America). The report offers market size and forecasts in terms of value (USD) and volume (Metric Tons) for all the above segments.

By Type

| Inulin |

| Fructo-Oligosaccharides (FOS) |

| Galacto-Oligosaccharides (GOS) |

| Xylo-Oligosaccharides (XOS) |

| MOS (Mannan-Oligosaccharides) |

| Lactulose |

| Other Types |

By Animal Type

| Poultry |

| Ruminants |

| Swine |

| Aquaculture |

| Other Animals |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Inulin |

| Fructo-Oligosaccharides (FOS) | |

| Galacto-Oligosaccharides (GOS) | |

| Xylo-Oligosaccharides (XOS) | |

| MOS (Mannan-Oligosaccharides) | |

| Lactulose | |

| Other Types | |

| By Animal Type | Poultry |

| Ruminants | |

| Swine | |

| Aquaculture | |

| Other Animals | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North America feed prebiotics market?

It stands at USD 719.5 million in 2025 and is projected to reach USD 967.4 million by 2030

Which ingredient type is growing fastest in feed prebiotics?

Mannan-Oligosaccharides lead with a projected 9.8% CAGR through 2030.

Why are United States producers adopting prebiotics rapidly?

Stricter antibiotic regulations and proven feed-conversion benefits drive rapid adoption.

Which animal segment holds the largest share?

Poultry commands 37.9% of 2024 revenue across North America.

Page last updated on: