Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

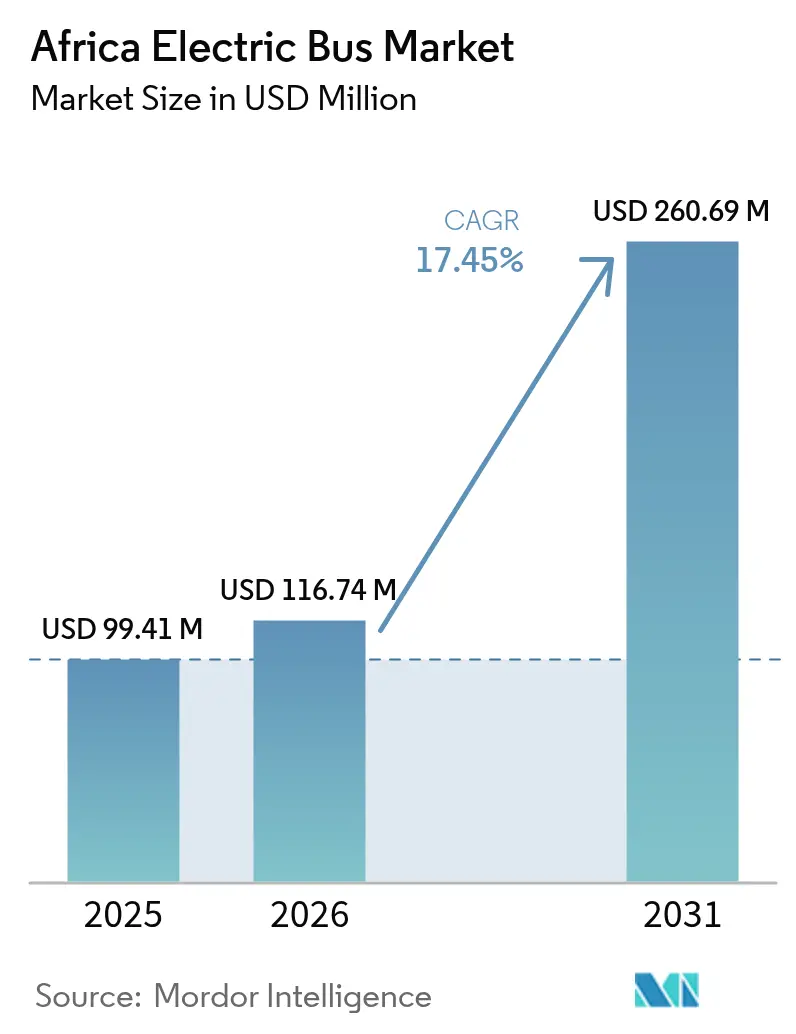

| Base Year Market Size (2025) | USD 99.41 Million |

| Market Size (2026) | USD 116.74 Million |

| Market Size (2031) | USD 260.69 Million |

| Growth Rate (2026 - 2031) | 17.45% CAGR |

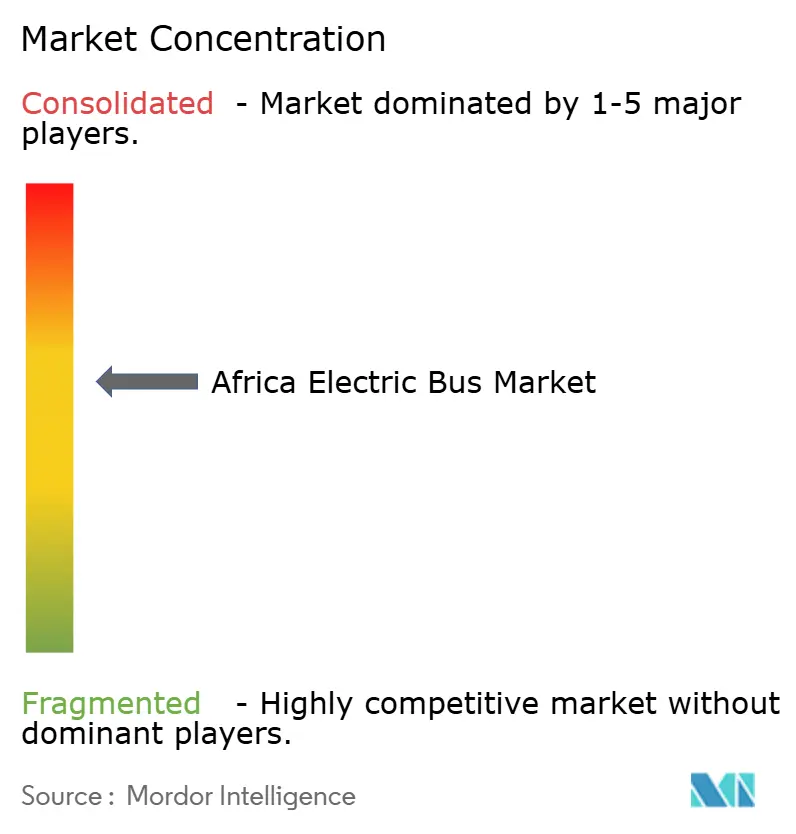

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Electric Bus Market Analysis by Mordor Intelligence

The Africa electric bus market size is expected to grow from USD 99.41 million in 2025 to USD 116.74 million in 2026 and is forecast to reach USD 260.69 million by 2031 at 17.45% CAGR over 2026-2031. Fleet operators are accelerating purchases as lithium-ion battery pack prices reduce, total cost of ownership (TCO) parity is expected by 2027, and carbon-credit revenues begin to close remaining funding gaps. Declining battery costs, government procurement targets, and localized Chinese OEM assembly plants are the three strongest growth catalysts. Solar-powered depot charging is mitigating grid-reliability risks across South Africa, Kenya, and Rwanda, while Article 6 carbon markets are improving project bankability for private operators. Competitive intensity remains moderate as BYD, Yutong, and King Long scale knock-down assembly, and local innovators such as Roam and IZI tailor chassis, suspension, and cooling systems to African road and climate conditions.

Key Report Takeaways

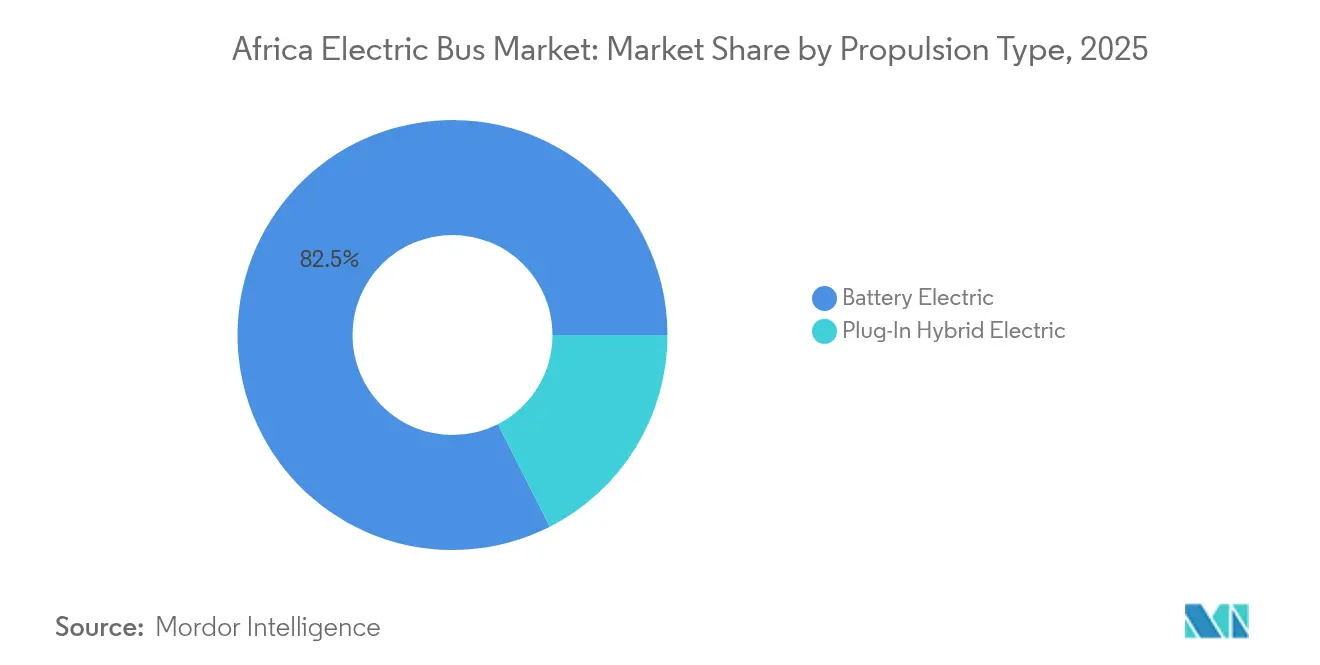

- By propulsion type, battery electric buses held 82.48% of the Africa electric bus market share in 2025, and will grow with the fastest CAGR of 20.98% by 2031.

- By consumer type, government procurement captured 61.55% of the Africa electric bus market size in 2025, while fleet operators are advancing at an 17.84% CAGR to 2031.

- By bus length, the standard (9–14 m) segment accounted for 56.32% share of the Africa electric bus market size in 2025, whereas mini buses (below 9 m) are expanding at a 19.18% CAGR through 2031.

- By charging mode, depot/overnight charging led with 68.62% of the Africa electric bus market share in 2025; opportunity/in-route charging is projected to register an 18.39% CAGR between 2026-2031.

- By battery capacity, 201-400 kWh led with 52.88% of the Africa electric bus market share in 2025; while buses with less than or equal to 200 kWh battery will expand at a 18.79% CAGR by 2031.

- By country, South Africa dominated with 41.98% revenue share in 2025; the Rest of Africa segment is forecast to grow at an 18.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Electric Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling Battery Prices, TCO Parity | +4.2% | South Africa, Kenya | Medium term (2-4 years) |

| Government E-Bus Procurement Programs | +3.8% | Kenya, Nigeria, Rwanda, South Africa, Morocco | Short term (≤ 2 years) |

| Chinese OEM CKD Expansion | +3.1% | South Africa, Morocco, Egypt | Medium term (2-4 years) |

| Solar-Powered Depot Charging Microgrids | +2.4% | Rural and semi-urban Sub-Saharan Africa | Long term (≥ 4 years) |

| Urban Demand for Clean Transport | +2.2% | Lagos, Cairo, Johannesburg, Casablanca | Short term (≤ 2 years) |

| Carbon-Credit Monetization Under Article 6 | +1.8% | Ghana, Kenya, Rwanda | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Falling Battery Prices and TCO Parity By 2027

Global average Li-ion battery pack prices fell to USD 139/kWh in 2023 and further to ~USD 115/kWh in 2024 and are forecast to reduce further by 2026, pushing the Africa electric bus market toward operating-cost parity with diesel buses [1]“Lithium-ion Battery Cost Trajectory and Implications for E-Mobility,” African Development Bank, afdb.org. Roam’s Nairobi pilots show maintenance costs falling and fuel savings rising versus diesel fleets. Morocco’s Renault- and Stellantis-anchored supply chain positions the country to localize battery module assembly, while Egypt’s 1 GW Obelisk solar park with 200 MWh of storage signals continent-wide familiarity with stationary battery systems.

Government E-Bus Procurement Programs and Subsidies

Kenya’s 2024 Electric Mobility Draft Policy introduces green number plates, duty exemptions, and estimates that dormant renewable capacity could power 7,000 buses daily [2]“Draft National Electric Mobility Policy,” Ministry of Roads and Transport Kenya, mot.go.ke. Nigeria’s October 2024 roadmap prefers Gross-Cost-Contract structures that shift capex risk to private consortia. Rwanda waived VAT on locally built buses, enabling IZI’s Impala E30 roll-out, while Ghana grants eight-year import-duty holidays for assembled EVs.

Rapid Expansion of Chinese OEM CKD Assembly Plants in Africa

BYD’s 120-unit Cape Town program is the anchor project for a potential knock-down plant serving all of SADC. Yutong is shipping 723 electric buses to Morocco in 2025 and is scouting CKD sites alongside Tractafric Motors [3]“Morocco Export Ceremony Press Release,” Yutong Bus, yutong.com. Egypt’s MCV-Volvo complex offers a ready supply base for further Chinese localization moves. CKD kits cut landed cost 15-25% and accelerate technician up-skilling via on-site assembly training.

Emergence of Solar-Powered Depot Charging Using Off-Grid Microgrids

South Africa’s first off-grid bus depot combines 2.5 MWp of solar PV with 4 MWh of batteries, ensuring uninterrupted service during load-shedding. Kenya’s renewable grid allows smaller city depots to run entirely on behind-the-meter solar plus lithium storage. The World Bank is supporting hybrid solar-grid microgrids in Gambia and Senegal to enable similar schemes. Operators report significant electricity-cost reduction versus grid-only charging.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Grid Capacity | -2.8% | Nigeria, South Africa, Ghana | Short term (≤ 2 years) |

| High Upfront Cost and Constrained Budgets | -2.1% | All regions, acute in West and Central Africa | Medium term (2-4 years) |

| Lack of Battery-Recycling Infrastructure | -1.4% | Central and West Africa | Long term (≥ 4 years) |

| Scarcity of Skilled EV-Maintenance Workforce | -1.2% | Rural and secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Grid Capacity and Unreliable Power Supply

Load-shedding in South Africa and frequent blackouts in Nigeria force operators to install backup diesel gensets or delay expansion, raising opex. The World Bank’s USD 1.6 billion West Africa Regional Electricity Market Program will add cross-border transmission by 2028, yet most depots still require islanded microgrids to guarantee service.

High Upfront Cost and Constrained Municipal Budgets Post-COVID

Electric buses cost 40-60% more than diesel units upfront, stretching city budgets already weakened by pandemic-era revenue losses. Abuja, Accra, and Dakar have all deferred BRT upgrades since 2023. Gross-Cost-Contract tenders and multilateral guarantees are helping, but procurement skills remain thin at municipal level.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Battery Electric Dominance Drives Market Evolution

Battery electric buses held 82.48% market share in 2025, and the segment is forecast to grow at a 20.98% CAGR. This dominance is rooted in lower drivetrain complexity and the accelerating decline in lithium-ion pack prices. BYD’s Cape Town fleet has already cut operating costs significantly compared with equivalent diesel routes, underscoring the economic pull.

Plug-in hybrids account for the residual share, mainly in long-distance or grid-constrained corridors, yet their relevance is expected to wane as energy-density improves and solar-charged depots proliferate. Municipalities gravitate toward pure battery platforms to maximize air-quality gains and simplify maintenance. Policy support—such as Kenya’s excise duty exemptions—further tilts new tenders toward zero-emission fleets.

By Consumer Type: Government Leadership Enables Private-Sector Growth

Government agencies commanded 61.55% of 2025 demand as public procurement frameworks kickstarted network electrification. Abuja’s 100-unit pilot and Addis Ababa’s 4,800-bus import plan showcase scale benefits. Private fleet operators are quickly closing the gap; the segment is projected to grow 17.84% annually through 2031 as asset financiers bundle vehicles, chargers, and carbon-credit revenues into pay-per-kilometer contracts.

Early adopters such as Roam demonstrate that optimized duty cycles, dynamic pricing, and outsourcing of depot energy management can yield positive cash flow from year one. As a result, the Africa electric bus market share attributable to private operators is expected to climb significantly by 2030.

By Bus Length: Standard Buses Lead While Mini Segment Accelerates

Standard 9–14 m models delivered 56.32% of 2025 revenues, underpinning BRT trunk corridors in Cairo, Johannesburg, and Lagos. High passenger throughput and predictable depot returns keep this format central to government tenders. Yet mini buses (below 9 m) are growing fastest at 19.18% CAGR, favored for feeder services and narrow peri-urban roads where turning radius and axle weight limits are critical.

IZI’s Impala E30 and Roam’s 33-seat City Shuttle illustrate how localized chassis and composite bodies can slash curb weight, enabling less than/equal to 200 kWh battery packs without sacrificing range. Consequently, the Africa electric bus market size for mini buses could grow between 2026 and 2031 as ride-sharing cooperatives electrify informal routes.

By Charging Mode: Depot Charging Dominance with Opportunity Upside

Depot-based overnight charging covered 68.62% of delivered units in 2025 thanks to simpler infrastructure and the ability to tap surplus off-peak generation. Solar-plus-battery systems in Cape Town and Nairobi have driven energy costs down 30-40%. Opportunity charging, while still niche, will scale at an 18.39% CAGR as pantograph-equipped stops in Casablanca and Dakar extend daily range and cut battery-size requirements.

Grid reinforcements under the West Africa Power Pool, paired with Section 14 feed-in-tariff reforms, allow operators to monetize midday solar overproduction by feeding back excess, further enhancing the Africa electric bus market economics.

By Battery Capacity: Mid-Range Packs Balance Performance and Cost

The 201-400 kWh class held 52.88% share in 2025, delivering 200-250 km real-world range and optimal TCO for urban duty cycles. Less than/Equals to 200 kWh packs will expand at 18.79% CAGR as energy-density climbs above 330 Wh/kg and route-based charging gains traction.

Above-400 kWh batteries remain tailored to intercity services such as Johannesburg-Pretoria shuttles but face diminishing cost advantage as opportunity charging networks densify. With pack prices falling by 2026, the Africa electric bus market size for less than/equals to 200 kWh pack configurations is expected to eclipse by 2030.

Geography Analysis

South Africa’s 41.98% share in 2025 reflects early mover advantage: Golden Arrow’s 120-bus BYD fleet, Autel’s 240 kW fast chargers, and the nation’s first solar-microgrid depot keep Cape Town services running during Stage-5 load shedding. Morocco’s share is anchored by its Tangier and Kenitra auto zones producing 60% of Renault and Stellantis African output. Yutong’s 723-bus export contract, combined with ONCF’s e-bus pilot in Rabat, positions the kingdom for significant annual growth.

Egypt blends large-scale demand with manufacturing potential. MCV already builds Volvo-branded city buses, and government subsidies covering local EV production costs shorten payback periods. The 1 GW Obelisk solar park guarantees low-carbon electricity, critical for opportunity charging economics.

Rest-of-Africa demand is burgeoning and is projected to underpin an 18.11% CAGR by 2031. Nigeria finalizes its Gross-Cost-Contract template, Ghana’s eight-year duty waiver is live, and Ethiopia received 100 Golden Dragon units in 2025, inaugurating East Africa’s largest e-bus operation. Cross-border power-pooling and standardized CKD incentives under AfCFTA are expected to knit these pockets of demand into a cohesive continental growth engine.

Competitive Landscape

Chinese OEMs dominate volume but face rising competition from localized African ventures. BYD, Yutong, King Long, and Golden Dragon collectively supplied a notable share of 2024 deliveries, leveraging cost-efficient supply chains and integrated drivetrain platforms. BYD’s Autel-backed charging hub in Cape Town evidences its solution-provider strategy.

Local startups are differentiating via market-specific engineering. Roam’s Nairobi factory welds lighter bus frames using locally sourced steel and integrates battery packs optimized for high-ambient temperatures. Rwanda’s IZI employs modular composite bodies to reduce weight and simplify repairs.

Strategic partnerships define the competitive narrative: BYD-Golden Arrow, Yutong-Tractafric Motors, Golden Dragon-Belayneh Kinde Group, and Autel-City of Cape Town exemplify turnkey ecosystems bundling vehicles, chargers, maintenance, and financing. Carbon-credit origination is an emerging moat. Operators able to verify emission reductions under Article 6 can offer 5-10 cents/km lower effective pricing, giving them an edge in competitive tenders.

Africa Electric Bus Industry Leaders

BYD Auto Co., Ltd.

Zhengzhou Yutong Bus Co., Ltd.

King Long United Automotive Industry Co., Ltd

Zhongtong Bus Holding Co., Ltd

Kiira Motors Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Autel Energy installed 150–240 kW MaxiCharger DC Fast units at South Africa’s largest bus-charging hub, enabling Cape Town to deploy 120 e-buses by December 2025.

- September 2025: Yutong dispatched the first batch of 723 electric buses to Morocco in partnership with Tractafric Motors and the Ministry of Transport.

- April 2025: Xiamen Golden Dragon delivered 100 electric buses to Addis Ababa-based Belayneh Kinde Group, inaugurating East Africa’s largest e-bus operation.

- April 2025: Golden Arrow Bus Service began operating its first tranche of new BYD units, with over 100 additional buses scheduled for Western Cape routes in 2025.

Africa Electric Bus Market Report Scope

An electric bus, also known as an e-bus, is a bus that does not use a traditional IC engine for propulsion and is entirely electric. The onboard electric motor of an E-bus is powered by onboard batteries or a set of batteries. Electric buses are considered environmentally friendly because they emit no pollutants. They are also more cost-effective than traditional gasoline/diesel buses.

The electric bus market is segmented by vehicle type, consumer type, and country.

The Electric Bus Market is segmented by vehicle type into battery electric and plug-in hybrid electric. By consumer type, the market is segmented into government and fleet operators. By Country, the market is segmented into South Africa, Morocco, Egypt, and Rest of Africa. The report covers the market size and forecast in value (USD Million) for all the above segments.

By Propulsion Type

| Battery Electric |

| Plug-In Hybrid Electric |

By Consumer Type

| Government |

| Fleet Operators |

By Bus Length

| Mini (Below 9 m) |

| Standard (9-14 m) |

| Articulated (Above 14 m) |

By Charging Mode

| Depot / Overnight Charging |

| Opportunity / In-Route Charging |

By Battery Capacity

| ≤200 kWh |

| 201-400 kWh |

| Above 400 kWh |

By Country

| South Africa |

| Morocco |

| Egypt |

| Rest of Africa |

| By Propulsion Type | Battery Electric |

| Plug-In Hybrid Electric | |

| By Consumer Type | Government |

| Fleet Operators | |

| By Bus Length | Mini (Below 9 m) |

| Standard (9-14 m) | |

| Articulated (Above 14 m) | |

| By Charging Mode | Depot / Overnight Charging |

| Opportunity / In-Route Charging | |

| By Battery Capacity | ≤200 kWh |

| 201-400 kWh | |

| Above 400 kWh | |

| By Country | South Africa |

| Morocco | |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

How fast will electric bus revenues grow across Africa?

Revenues are forecast to climb from USD 99.41 million in 2025 to USD 116.74 million in 2026 and USD 260.69 million by 2031, reflecting a 17.45% CAGR over 2026-2031.

Which countries are leading adoption?

South Africa holds 41.98% of 2025 sales, followed by Morocco and Egypt, while Kenya, Rwanda, and Ethiopia are scaling fastest.

What battery size is most common?

Packs rated 201–400 kWh account for 52.88% of units because they balance range and upfront cost for typical city routes.

Why are mini electric buses gaining popularity?

Mini buses below 9 m are expanding at a 19.18% CAGR due to their suitability for feeder routes and their lower infrastructure demands.

Page last updated on: