Nigeria Data Center Cooling Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

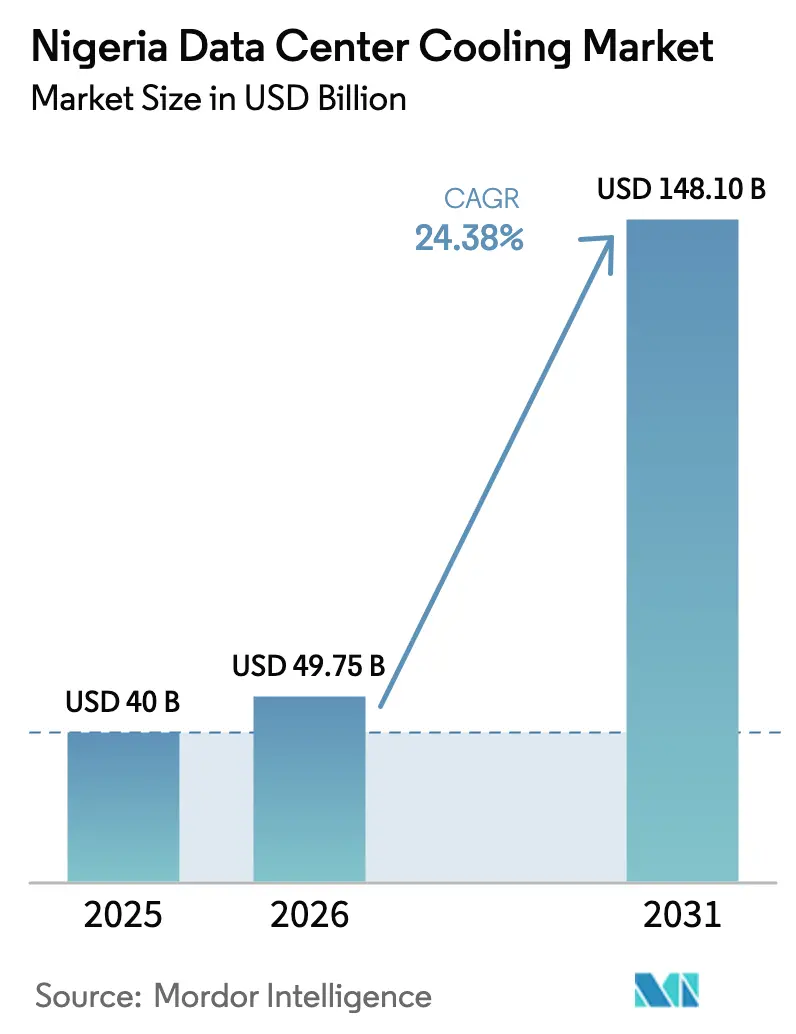

| Base Year Market Size (2025) | USD 40 Billion |

| Market Size (2026) | USD 49.75 Billion |

| Market Size (2031) | USD 148.1 Billion |

| Growth Rate (2026 - 2031) | 24.38% CAGR |

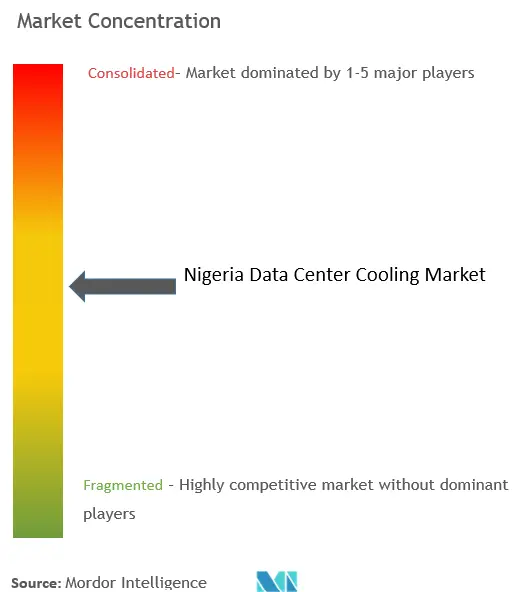

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Data Center Cooling Market Analysis by Mordor Intelligence

The Nigeria data center cooling market size was valued at USD 40 million in 2025 and estimated to grow from USD 49.75 million in 2026 to reach USD 148.1 million by 2031, at a CAGR of 24.38% during the forecast period (2026-2031). At the national level, sustained hyperscale capital spending, supportive fiscal incentives and an expanding fibre backbone are the primary forces enlarging the Nigeria data center cooling market. Diesel price shocks following fuel-subsidy removal, together with grid unreliability, sharpen the focus on energy-efficient thermal architectures that stabilise operating costs. Air-based systems still dominate installed capacity, yet liquid technologies are gaining traction as AI and machine-learning deployments push rack densities well beyond the limits of conventional room-level cooling. Finally, global suppliers are deepening local footprints through acquisitions and training alliances that answer the chronic shortage of certified technicians.

Key Report Takeaways

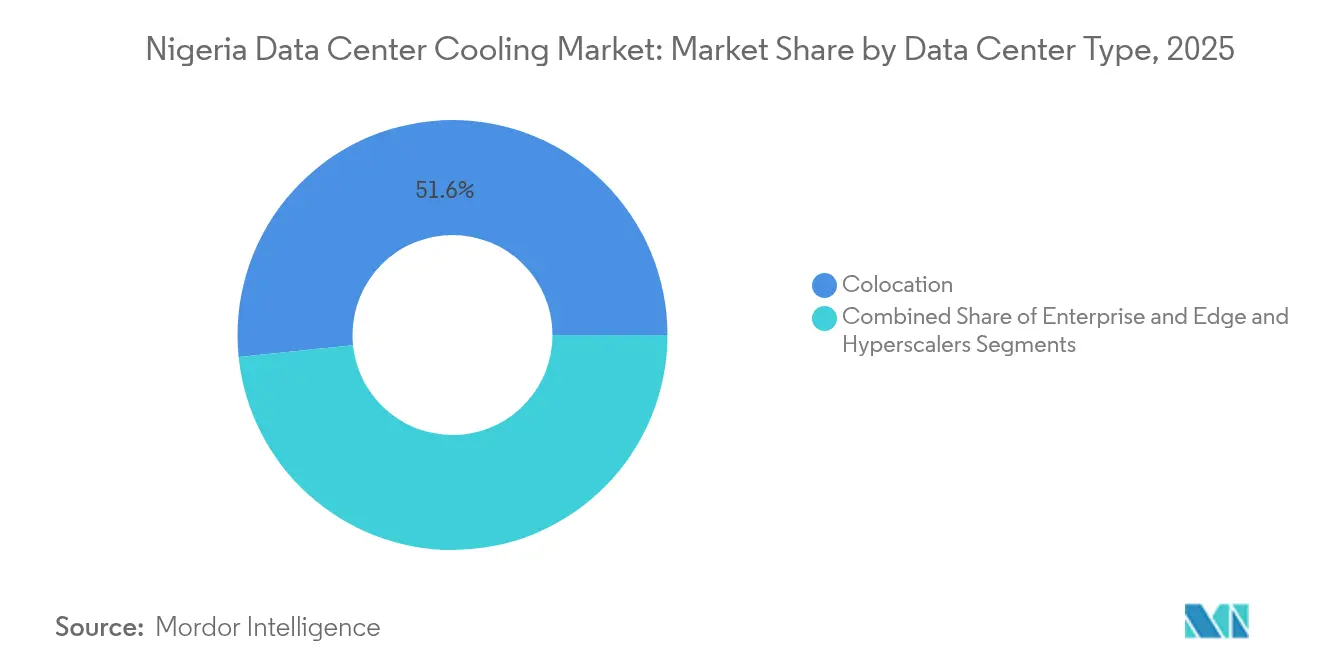

- By data center type, colocation led with 51.63% of Nigeria data center cooling market share in 2025, while hyperscalers are projected to grow at a 27.1% CAGR through 2031.

- By tier type, Tier 3 facilities accounted for 62.55% share of the Nigeria data center cooling market size in 2025; Tier 4 sites are positioned to expand at a 26.7% CAGR between 2026-2031.

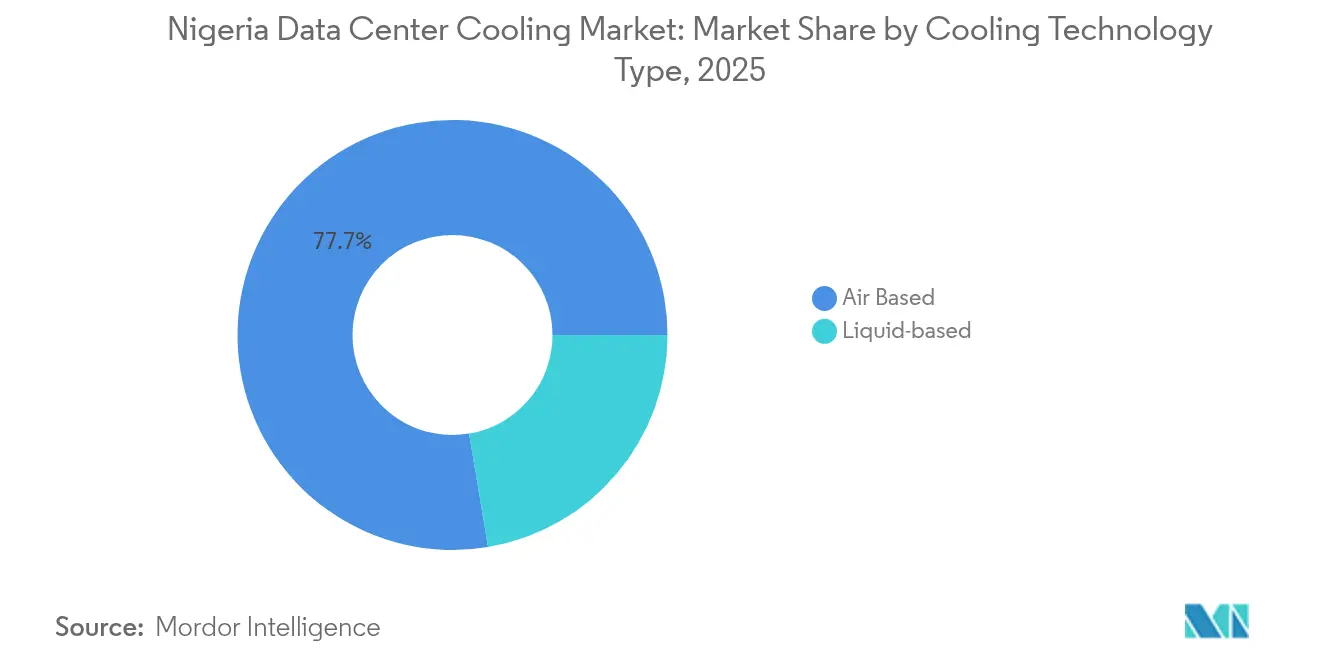

- By cooling technology, air-based systems commanded 77.65% share of the Nigeria data center cooling market size in 2025; liquid-based solutions are set to post a 28.3% CAGR to 2031.

- By component, equipment captured 84.70% of Nigeria data center cooling market size in 2025, whereas services should register the fastest 26.6% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Data Center Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hyperscale builds by global cloud providers | +6.2% | Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Government tax-holidays for pioneer status data-center projects | +4.8% | National (early gains in Lagos, Abuja) | Short term (≤2 years) |

| Accelerated fibre landing stations and subsea cable expansions | +5.1% | Coastal states, mainly Lagos and Akwa Ibom | Medium term (2-4 years) |

| Gradual fuel-subsidy removal lifts diesel prices, favouring liquid cooling | +3.9% | National, most acute in Lagos | Short term (≤2 years) |

| Meteorological advantage of Harmattan coastal winds | +2.3% | Coastline from Lagos to Calabar | Long term (≥4 years) |

| Growing AI/ML workloads from Lagos fintech hubs | +4.7% | Lagos metropolitan area | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Hyperscale Builds by Global Cloud Providers

Rapid capacity additions by Microsoft, Huawei, and other cloud majors are reshaping power-and-cooling specifications across the Nigeria data center cooling market. New facilities are designed for 30-50 kW rack densities that make liquid cooling economically compelling. Digital Realty’s Lagos carrier-neutral campus, located close to Meta’s 2Africa cable stub, exemplifies demand for 24/7 thermal reliability that meets stringent service-level agreements.[1]Digital Realty Expands Lagos Connectivity, Digital Realty, digitalrealty.com As these multinationals replicate mature-market best practices, local colocation operators are pressured to upgrade cooling to retain enterprise tenants. The resulting equipment mix shifts toward rear-door heat exchangers, pumped refrigerant economisers and immersion tanks suited to AI clusters. Hyperscaler construction therefore amplifies order volumes for high-capacity chillers and drives sustained double-digit revenue visibility for OEMs active in Nigeria data center cooling market.

Government Tax-Holidays for Pioneer Status Data-Center Projects

Nigeria awards five-year corporate tax exemptions to qualifying data-center investments,[2]Nigeria’s Fibre Rollout Starts February 2025, Punch, punchng.com lowering payback periods for thermal infrastructure that would otherwise be stretched by import VAT. The incentive encourages adoption of premium liquid-cooling assemblies that cut lifetime power bills even though their upfront cost is higher. Financial modelling shows that the pioneer relief trims effective capital charges by roughly 9-10 percentage points, creating space for operators to specify modular chillers and precision in-row units rather than basic comfort AC. Early beneficiaries include greenfield builds in Lagos’ Lekki corridor, where duty savings partially offset the 7.5% value-added tax on imported HVAC equipment. Because qualifying projects face less tax drag, the Nigeria data center cooling market can absorb more sophisticated products, accelerating technology diffusion.

Accelerated Fibre Landing Stations and Subsea Cable Expansions

Meta’s 2Africa and Google’s Equiano landings increase international bandwidth by multiples of 15-20 ×, triggering a wave of edge and carrier-neutral developments along the coastline. These low-latency nodes require compact, high-efficiency cooling footprints that fit within premium real estate parcels adjacent to beach-manholes. For operators, each incremental 10 Tbps of subsea backhaul pushes server utilisation higher, thereby hiking heat densities and reinforcing demand for advanced thermal envelopes. Consequently, pump-assisted liquid loops, heat-recovery chillers and seawater economisers are specified more frequently in edge blueprints, further propelling the Nigeria data center cooling market.

Gradual Removal of Fuel Subsidy Increases Diesel Cost, Favouring Efficient Liquid Cooling

Diesel’s 233% price surge following subsidy withdrawal magnifies operating expenses for generator-backed chillers.[3]Immersion Cooling Energy Savings, Mitsubishi Heavy Industries, mhi.com Operators now benchmark energy intensity in kilowatt-hours per rack against the embedded cost of fuel burn during outages. Immersion cooling, with up to 94% lower parasitic energy draw, becomes financially attractive despite costlier dielectric fluids. Adoption rates climb fastest in Lagos where multi-hour grid failures remain common. Liquid-ready white-space design therefore migrates from ‘nice-to-have’ to a board-level mandate across the Nigeria data center cooling market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Erratic grid stability adds redundancy cost layers | -3.2% | National, most severe in northern states | Short term (≤2 years) |

| 7.5% VAT on imported HVAC equipment | -2.1% | Nationwide | Short term (≤2 years) |

| Shortage of certified HVAC-R technicians for immersion systems | -2.8% | Lagos, Abuja | Medium term (2-4 years) |

| Lagos water-table salinity limits open-loop cooling | -1.4% | Lagos and coastal hinterland | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Erratic Grid Stability Adds Redundancy Cost Layers

Nigeria’s grid delivers only 5.4 GW on average versus an estimated 42 GW of diesel generation capacity, forcing operators into N+1 or N+2 redundancy across chillers, pumps and CRAH arrays. The duplicate hardware inflates initial capital cost by 40-60% and compresses floor space utilisation, thereby reducing the return profile for investors in the Nigeria data center cooling market. More critically, redundant liquid loops require parallel pumping stations and power supplies, complicating routine maintenance. The cumulative overhead can delay breakeven by two-plus years relative to peers in markets with stable grids.

7.5% VAT on Imported HVAC Equipment

Because advanced CRAH units, titanium heat exchangers and dielectric liquids are rarely produced locally, customs valuations immediately raise headline pricing by 7.5%. Even after pioneer tax relief, the VAT burden remains unrecoverable for many greenfield schemes, nudging operators toward longer depreciation schedules or lower-spec devices. Fiscal friction is therefore a direct dampener on unit sales volume, particularly in the entry-level segment of the Nigeria data center cooling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Drives Market Leadership

Colocation campuses secured 51.63% revenue share within the Nigeria data center cooling market during 2025 as multi-tenant business models spread cooling overheads across client portfolios. Hyperscalers, although smaller in absolute spend, are poised for a 27.1% CAGR on the back of committed rollouts by Microsoft and Huawei. Economies of scale enable colocation operators to deploy centralised chilled-water plants and hot-aisle containment that individual enterprises cannot cost-justify. In contrast, cloud majors are skipping straight to liquid footprints that sustain 30 kW-plus racks, thereby raising average-selling-price trajectories for OEMs.

Tenant-mix diversification also insulates colocation providers from single-client failure risk, allowing them to lock in multi-year operations and maintenance agreements that drive the services upswing noted across the Nigeria data center cooling market. Hyperscale newcomers remain the prime evangelists for immersion baths and rear-door exchangers, technologies that local teams increasingly seek to master.

By Tier Type: Tier 3 Dominance with Tier 4 Acceleration

Tier 3 designs, delivering 62.55% of Nigeria data center cooling market size in 2025, remain the mainstream choice because they balance redundancy with manageable capital intensity. Yet Tier 4 complexes, expanded by government projects and financial-services mandates, will surge at 26.7% CAGR. Uptime-certified Tier 4 sites mandate fully duplicated cooling trains from chillers to pump skid through to CRAHs, embedding higher-margin equipment opportunities for global vendors.

As critical bank and identity-management workloads migrate into Tier 4 halls, operators commission modular liquid chillers and battery-backed pump arrays to guarantee 99.995% availability. The pattern feeds sustained upgrade demand in Tier 3 venues that must differentiate via energy-efficiency retrofits if they are to defend occupancy rates against higher-resilience newcomers.

By Cooling Technology: Air Dominance with Liquid Acceleration

Traditional air solutions, led by CRAHs and water-cooled chillers, held 77.65% share of Nigeria data center cooling market size in 2025. However, surge growth of 28.3% in liquid solutions through 2031 reflects GPU workloads and subsidy-driven energy economics. Direct-to-chip plates and single-phase immersion tanks enable 40-50 kW rack densities, a performance air cannot match without excessive fan energy.

OEMs such as Schneider Electric now package liquid cooling in ‘reference designs’ that minimise integration risk. While familiarity biases many operators toward air, the proportion of new-build white space designed to be liquid-ready is rising sharply, signalling a structural pivot inside the Nigeria data center cooling market.

By Component: Equipment Leadership with Services Acceleration

Equipment delivered 84.70% of revenue in 2025, underlining the capital-heavy nature of cooling rollouts. Yet services are projected to compound at 26.6% as operators seek guaranteed uptime contracts and optimisation audits. Integration work around building-management-system interoperability, CFD airflow modelling and liquid-loop water treatment generates recurring fees that outpace inflation.Service complexity intensifies as liquid adoption widens, because operators must schedule dielectric-fluid replacement, pump seal inspections and leak-detection calibrations outside standard HVAC competency sets. Vendors therefore bundle remote monitoring and spare-parts guarantees, deepening their annuity streams inside the Nigeria data center cooling industry.

Geography Analysis

Lagos anchored roughly 64.20% of national demand in 2025 owing to its status as West Africa’s connectivity gateway and financial nucleus. Harmattan season offers predictable dry winds that trim compressor run-time by up to 20%, but high ground-water salinity forces operators to favour closed-loop designs. Abuja followed with about 20.55% share, benefitting from more stable grid supply even though cooler ambient temperatures are offset by absence of direct subsea cable landings. Secondary hubs such as Port Harcourt, Akwa Ibom and Kano remain embryonic yet post-forecast growth rates above the national 24.38% CAGR because fibre rollout widens last-mile reach.

Grid instability north of Latitude 10° N undercuts the economics of multi-megawatt campuses, so operators tend to position edge sites closer to Lagos’ redundant transmission corridors. Nevertheless, federal infrastructure programmes aimed at raising on-grid capacity to 15 GW within five years could unlock greenerfield options inland. Climate modelling shows that average wet-bulb temperatures in Kaduna are 2-3 °C lower than coastal benchmarks during peak summer, an edge that may translate into 4-5% lower PUE once reliable mains power materialises.

As metropolises outside Lagos strengthen backbone connectivity, enterprise and public-sector workloads will scatter geographically, spawning micro-edge pods that still demand sophisticated cooling albeit at smaller kilowatt envelopes. This decentralisation supports long-run volume growth for modular, factory-integrated cooling skids across the Nigeria data center cooling market.

Competitive Landscape

The Nigeria data center cooling market remains moderately fragmented, with no vendor exceeding 20% revenue. Global majors Schneider Electric, Vertiv and Johnson Controls anchor the premium segment, leveraging global supply chains and recent acquisitions to enrich liquid-cooling portfolios. Schneider’s USD 850 million takeover of Motivair in 2024 instantly lifted its pumping and CDU expertise, while Vertiv’s 2024 purchase of BiXin’s high-capacity chiller IP enhances options for HPC customers.

Competitive choreography now revolves around vertical integration: OEMs augment hardware with design-build-operate contracts that guarantee performance. Vertiv’s blueprint collaboration with NVIDIA demonstrates how co-engineering power and cooling accelerates sales cycles for AI deployments. Regional HVAC firms still capture brownfield retrofit work but face import-duty headwinds and skill shortages that limit scale. Emerging disruptors such as Iceotope and Asetek invest in local technician academies to overcome service-capacity bottlenecks, an approach that could win them double-digit share in liquid categories by 2028.

Because purchase decisions increasingly hinge on total cost of ownership and after-sales support rather than sticker price, vendors that finance equipment alongside energy-savings guarantees are likely to out-pace competitors. Active project pipelines suggest OEM-led financing could underwrite up to USD 75 million in new chillers and immersion systems between 2025-2027, reinforcing the Nigeria data center cooling market’s shift toward service-centric revenue models.

Nigeria Data Center Cooling Industry Leaders

Stulz GmbH

Vertiv Group Corp.

Schneider Electric SE

Daikin Industries, Ltd.

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Schneider Electric and NVIDIA announced a strategic partnership to co-engineer liquid-cooled AI factory blueprints capable of 132 kW per rack.

- May 2025: Digital Realty expanded its Lagos campus with new meet-me rooms tied directly to the 2Africa cable system.

- April 2025: Equinix commissioned the LG2.3 Lagos expansion, adding multi-tenant capacity with high-efficiency cooling.

- May 2025: Schneider Electric pledged USD 700 million for global manufacturing upgrades including cooling-equipment lines serving Africa.

- February 2025: The Nigerian government launched a nationwide fibre-optic programme to underpin edge-data-center investment.

- December 2024: Vertiv acquired BiXin Energy’s centrifugal-chiller technology to bolster HPC cooling offerings.

- December 2024: Huawei activated a new cloud region in Nigeria, requiring large-scale precision cooling.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Nigeria data center cooling market as all factory-built air and liquid systems, related controls, and on-site services that dissipate heat from racks inside purpose-built data centers located within Nigeria. Passive airflow, direct-to-chip loops, immersion baths, containment aisles, chillers, CRAH / CRAC units, rear-door heat exchangers, and the associated monitoring software are included.

Scope Exclusion: Cooling installed in telecom huts, broadcast shelters, or other non-data-center edge enclosures is not counted.

Segmentation Overview

- By Data Center Type

- Hyperscalers (owned and Leased)

- Enterprise and Edge

- Colocation

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Cooling Technology

- Air-based Cooling

- Chiller and Economizer (DX Systems)

- CRAH

- Cooling Tower (covers direct, indirect and two-stage cooling)

- Others

- Liquid-based Cooling

- Immersion Cooling

- Direct-to-Chip Cooling

- Rear-Door Heat Exchanger

- Air-based Cooling

- By Component

- By Service

- Consulting and Training

- Installation and Deployment

- Maintenance and Support

- By Equipment

- By Service

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview facility managers in Lagos and Abuja, equipment vendors covering West Africa, international design-build contractors, and local regulators. These conversations validate installed IT load, typical rack power density, diesel usage patterns, and attainable PUE, filling gaps left by secondary data and sharpening model assumptions.

Desk Research

We start with public pillars such as National Bureau of Statistics energy data, Nigerian Communications Commission capacity filings, Nigerian Meteorological Agency temperature series, customs shipment records, and white papers from the Africa Data Centre Association. Company filings, project EIA reports, and reputable press give build costs, PUE targets, and hyperscale announcements that anchor adoption timing. Select paid resources, D&B Hoovers for contractor revenues and Dow Jones Factiva for deal flow, supply financial cross-checks. This list is illustrative; many additional open and paid sources are reviewed before figures are finalized.

Market-Sizing & Forecasting

We deploy a top-down demand pool that reconstructs cooling spend from installed IT load, average rack density, prevailing PUE, and equipment ASPs. We then corroborate it with selective bottom-up supplier roll-ups and channel checks. Key variables like installed megawatts, rack power density migration, diesel price trajectories, average ambient temperature, and telecom data traffic growth feed a multivariate regression to project 2025-2030 values. Where vendor roll-ups miss smaller projects, ratios derived from building permits bridge the gap.

Data Validation & Update Cycle

Outputs pass a two-step analyst review, variance screening versus shipment data and energy benchmarks, and re-contact of experts when anomalies exceed preset bands. Reports refresh every twelve months, with interim tweaks after material policy or investment events, so clients receive the latest view.

Why Mordor's Nigeria Data Center Cooling Baseline Stands Firm

Published estimates differ because each firm picks its own scope, variables, and refresh rhythm. Some quote full mechanical infrastructure while others report only equipment or only services.

Key gap drivers here include competitors folding power hardware into cooling, applying higher ASPs from imported turnkey packages, or using 2023 builds as a base without adjusting for 2024 diesel price shocks that delayed projects. Mordor's base uses 2024 field data, treats cooling as a stand-alone cost center, and refreshes annually, which together produce a balanced 2025 number.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40 million (2025) | Mordor Intelligence | - |

| USD 104.6 million (2024) | Regional Consultancy A | Includes installation labor and generator heat recovery loops; assumes 18 kW average rack load vs our verified 11 kW |

| USD 150 million (2024) | Trade Journal B | Counts telecom shelter retrofits and uses global ASPs without local import duty discounts |

The comparison shows that, by selecting the right asset boundary and field-tested variables, Mordor Intelligence delivers a transparent baseline that decision-makers can trace to clear metrics and reproduce when new builds come online.

Key Questions Answered in the Report

What is the current size of the Nigeria data center cooling market?

The market is valued at USD 49.75 million in 2026 and is forecast to climb to USD 148.1 million by 2031.

Which cooling technology is growing the fastest?

Liquid-based solutions such as immersion and direct-to-chip cooling are projected to grow at a 28.3% CAGR through 2031 as AI workloads expand.

Why do hyperscale operators prefer liquid cooling in Nigeria?

Diesel price inflation and high-density GPU racks make energy-efficient liquid architectures more cost-effective over the facility lifecycle.

How does Lagos’ climate influence cooling design?

Harmattan winds and coastal temperatures reduce compressor run-time, enabling free-air modes that cut HVAC energy by up to 20%.

What regulatory incentive supports cooling investments?

Pioneer-status tax holidays grant up to five years of corporate income-tax relief for qualifying data-center projects, lowering payback periods on advanced cooling gear

What limits wider adoption of immersion systems?

A shortage of certified HVAC-R technicians prolongs commissioning timelines and raises labour costs, slowing rollout speed despite strong demand.

Page last updated on: