Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

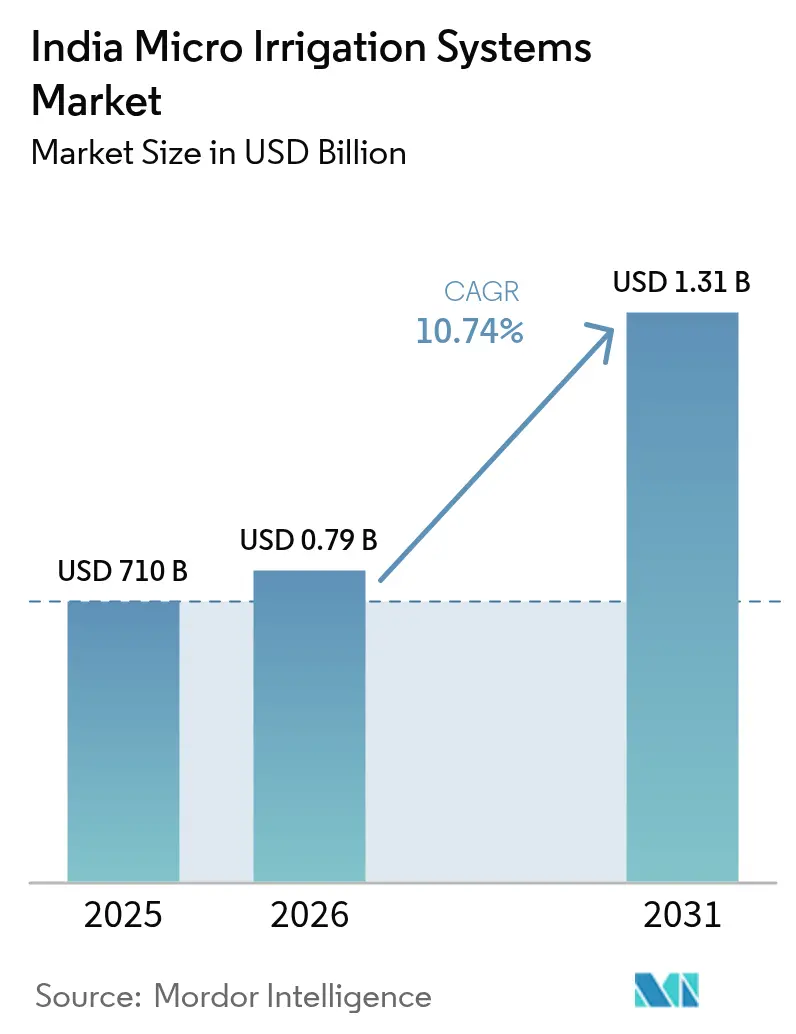

| Base Year Market Size (2025) | USD 710 Billion |

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 10.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Micro Irrigation Systems Market Analysis by Mordor Intelligence

India micro irrigation systems market size in 2026 is estimated at USD 786.25 million, growing from 2025 value of USD 710 million with 2031 projections showing USD 1.31 billion, growing at 10.74% CAGR over 2026-2031. Mounting groundwater stress, larger budgetary allocations for the Pradhan Mantri Krishi Sinchayee Yojana (PMKSY), and rapid digitization of farm practices are accelerating adoption. Subsidies covering up to 95% of equipment cost in priority districts are shortening payback periods, while the PM-KUSUM solar-pump program is lowering operating outlays. The bundling of Internet of Things (IoT)-enabled fertigation is driving the penetration of premium products. The competitive landscape remains moderately fragmented, with established players competing alongside emerging technology providers. Nevertheless, high capital intensity, emitter-clogging risks, and patchy after-sales support keep penetration below its potential among smallholders.

Key Report Takeaways

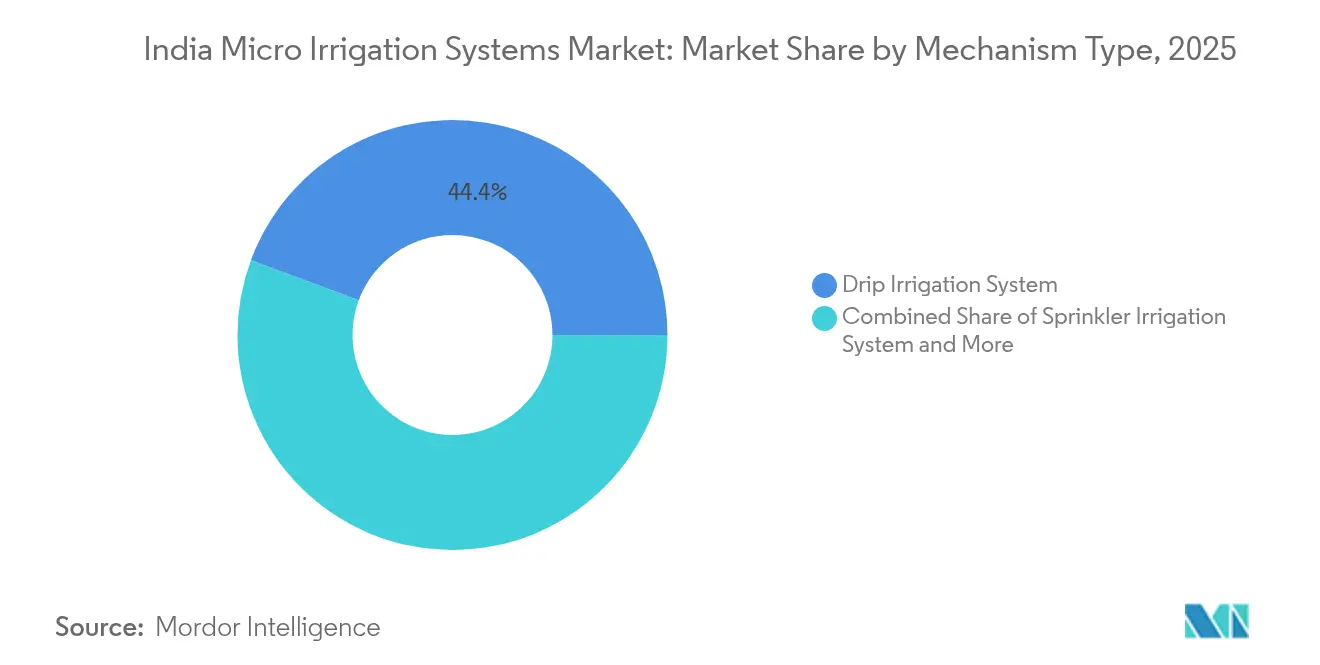

- By mechanism type, drip irrigation retained a 44.35% share in the Indian micro irrigation systems market in 2025, while fogging systems are projected to post the fastest 16.98% CAGR through 2031.

- By application, field crops accounted for 36.25% of the India micro irrigation systems market size in 2025, whereas turfs and ornamentals are advancing at an 17.66% CAGR to 2031.

- By end user, open field farms held 60.20% of revenue in 2025, while vertical farms are set to expand at a 19.05% CAGR during 2026-2031.

- By state, Maharashtra commanded a 19.60% of the India micro irrigation systems market share in 2025, while Tamil Nadu is forecast to grow at a 12.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Micro Irrigation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Subsidies Are Scaling Micro Irrigation Adoption | +3.2% | Nationwide, stronger in Maharashtra, Karnataka and Gujarat | Medium term (2-4 years) |

| Accelerating Groundwater Stress in West-Central India | +2.8% | Maharashtra, Gujarat, and Madhya Pradesh | Long term (≥ 4 years) |

| Rapid Shift to Fertigation in Fruit Belts | +2.1% | Karnataka, Maharashtra, Tamil Nadu, and Andhra Pradesh | Medium term (2-4 years) |

| Solar-Powered Pump Bundling Cuts Operating Expenditure | +1.9% | Rajasthan, Gujarat, and Maharashtra | Short term (≤ 2 years) |

| Peri-Urban Export-Oriented Horticulture Clusters | +1.5% | Tamil Nadu, Karnataka, Maharashtra, and Andhra Pradesh | Medium term (2-4 years) |

| Ag-Fintech Buy-Now-Pay-Later (BNPL) Models Easing Capital Expense | +0.8% | Smallholder farming districts nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Subsidies Are Scaling Micro Irrigation Adoption

The Union Budget 2025-26 lifted the agriculture allocation to USD 21.1 billion (INR 1.75 trillion).[1]Source: Press Information Bureau, “Agriculture Budget 2025-26,” pib.gov.in The Micro Irrigation Fund has approved USD 569 million ( INR 4,724.74 crore) in low-interest loans that states leverage for 50%–95% equipment subsidies. The Cabinet-cleared Modernisation of Command Area Development and Water Management scheme added USD 192 million (INR 1,600 crore) for pressurized pipe networks, cutting conveyance losses by 25%. Demonstration plots under the Per Drop More Crop initiative show 50%–90% water savings, encouraging peer adoption. Together, these fiscal tools compress payback to fewer than three seasons for high-value crops and enlarge the India micro irrigation systems market.

Accelerating Groundwater Stress in West-Central India

Annual withdrawals near 230 billion cubic meters have lowered aquifers by 1.5 centimeters per year, curbing streamflow into the Bay of Bengal by 1,200 cubic meters per second. Maharashtra irrigates just 18% of its farmland despite having India’s highest dam density, exposing a stark demand-supply gap. Policy responses such as Punjab’s ban on water-intensive hybrid paddy underscore a nationwide pivot toward efficient irrigation. Farmers in depletion hotspots now view precision watering as insurance against pumping-ban risk, boosting the India micro irrigation systems market.

Solar-Powered Pump Bundling Cuts Operating Expenditure

Diesel pumps account for one-third of an irrigator’s variable cost. PM-KUSUM covers 60% of solar pump capital cost and offers another 30% as institutional credit, leaving farmers to pay only 10% upfront. Solar-driven drip layouts slash daytime pumping expenditure to zero and extend irrigated command beyond erratic grid supply. Studies in Rajasthan show solar-drip packages cutting greenhouse gas emissions by 80% and water use by 40%.[2]Source: Food and Agriculture Organization, “Solar-Powered Irrigation Systems,” fao.org Cheaper running cost makes precision watering viable even for water-hungry sugarcane, widening the adoption base.

Peri-Urban Export-Oriented Horticulture Clusters

Cooperatives such as Mahagrapes enable smallholders to meet stringent residue limits and traceability norms for Europe through collective post-harvest infrastructure. Cluster programs in Tamil Nadu subsidize 50% of greenhouse and drip costs, targeting grape, pomegranate, and cut-flower export lanes. Hydroponic units around Bengaluru supply premium retailers, fueling an India micro irrigation systems market upswing in turfs and ornamentals. Consistent grade standards achievable only with precision watering secure price premiums that offset higher capital outlays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Installation Cost | -2.1% | Nationwide, sharper for smallholders | Short term (≤ 2 years) |

| Frequent Clogging and Maintenance Issues | -1.8% | Districts with poor water quality | Medium term (2-4 years) |

| Fragmented After-Sales Service Network | -1.3% | Eastern and central India | Medium term (2-4 years) |

| Emerging Groundwater Extraction Caps in Dark-Zone Blocks | -1.0% | Rain-fed regions with low banking density | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation Cost

Complete drip packages cost between USD 361-361,000 (INR 30,000-30 lakh) depending on acreage and automation, a heavy lift for the 86% of farmers who own under two hectares.[3]Source: IDBI Bank, “Financing Minor Irrigation Schemes,” idbibank.in Even after a 50% subsidy, the payback for cereals can exceed five years, deterring adoption. Declining hardware costs and volume discounts are narrowing the gap, but demand elasticity remains sensitive to credit availability, slowing India micro irrigation systems market growth.

Frequent Clogging and Maintenance Issues

Emitter blockage from suspended solids and dissolved salts reduces uniformity below the 85% threshold, hurting yields. Regular acid flushing and filter replacement add 8%–10% to annual operating cost. Tube-settler retrofits shorten sedimentation time from two hours to 20 minutes, cutting blockage by 70%. Lumpy service coverage means many farmers cannot access timely repairs, capping system life at six years against the rated 10-year span.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mechanism Type: Drip Systems Underpin Growth Momentum

Drip irrigation retained a 44.35% India micro irrigation systems market share in 2025, delivering 12%–84% water savings and 20%–50% yield gains across cereals, cotton, and horticulture. Smart automation players such as Jain Irrigation Systems Ltd’s JAIN LOGIC integrate soil-moisture telemetry and weather data, lifting water-productivity ratios by 30%. Sprinkler sets continue serving broadacre staples where uniform canopy wetting is critical, but growth trails fogging, which is rising 16.98% CAGR to 2031 on greenhouse demand. Fogging enables sub-4°C canopy cooling, vital for lettuce and exotic herbs grown inside vertical farms. IoT-ready controllers across all mechanisms add predictive maintenance capabilities, further expanding the India micro irrigation systems market size for premium kits.

Commercial greenhouse operators report significant output increases and substantial extra water savings after upgrading to sensor-controlled solenoid valves. Continuous research and development in anti-clog labyrinth design, pressure-compensating emitters, and UV-resistant polymers is extending field life, bolstering total cost-of-ownership economics. Consequently, the India micro irrigation systems market is shifting from simple gravity-fed lateral lines toward data-centric, low-maintenance architectures.

By Application Type: Field Crops Anchor Demand While Specialty Niches Surge

Field crops seized a 36.25% share of the India micro irrigation systems market in 2025, buoyed by state incentives for sugarcane and pulses. Demonstrations in capsicum show 29.8%–46.5% yield lifts under drip fertigation, creating spillover uptake into maize and oilseeds. Turfs and ornamental plants, while beginning from a smaller foundation, are projected to experience an 17.66% compound annual growth rate (CAGR) until 2031 as stadiums, golf courses, and lawns in gated communities contend with water usage regulations. Mixed vegetable hydroponic units in peri-urban areas adopt micro sprinklers to fine-tune root-zone humidity, improving shelf life for retailers.

Plantation crops, including coffee and cardamom, rely on low-pressure micro-sprinklers that halve leaf-wilting during dry spells. Orchards and vineyards represent a premium segment where micro irrigation delivers measurable quality improvements and export compliance, with fertigation enabling yield increases of 25-30% in fruit crops. The application diversity creates market resilience, as different segments respond to varying drivers from food security policies to urban development and export market demands.

By End User: Open Field Dominates but Vertical Farms Scale Fast

Open-field holdings accounted for 60.20% of revenue in 2025 owing to PMKSY’s 94 lakh-hectare coverage of cereals and pulses. Water stress and subsidy visibility spur farmers to retrofit lateral lines alongside existing tube wells, keeping the India micro irrigation systems market resilient. Greenhouses capitalize on assured off-take contracts with modern retail and input-cost amortization over high margins, while vertical farms record a 19.05% CAGR on rising demand for pesticide-free produce. The hydroponics subsegment reached scale in 2022 and is projected to grow fivefold by 2031, catalyzing uptake of fogging and nutrient film techniques.

Greenhouses use micron filters and UV-stabilized piping to extend equipment life, a must for export-compliant tomatoes and bell peppers. Vertical-farm operators adopt closed-loop drip fed by smart nutrient dosing to maintain parts-per-million precision. Urban land scarcity and rising cold-chain costs position multilayer farms within city limits as a viable model, further expanding the India micro irrigation systems market.

Geography Analysis

Maharashtra accounted for 19.60% of the India micro irrigation systems market in 2025, driven by state top-ups that supplement central subsidies by 15%. Yet, with only 18% of its cultivated area under irrigation, significant growth potential remains. Initiatives such as desilting reservoirs and channeling canal water under the Ramthal Integrated Drip Irrigation Project underscore strong policy commitment. Sugarcane belt conversions to subsurface drip are saving 45% water and 30% energy, freeing quota for horticulture expansion.

Tamil Nadu’s 12.64% CAGR through 2031 reflects its export-oriented banana and grape clusters adopting fertigation and high-density planting. The state disburses an extra 25% subsidy for precision irrigation inside greenhouses, making capex comparable with flood systems over five years. Karnataka and Gujarat, both facing falling water tables, promote solar pump-drip bundles that remove diesel-price volatility, widening coverage among millet growers.

Andhra Pradesh and Telangana are accelerating under horticulture corridor projects, while Rajasthan installs off-grid solar pumps to irrigate cumin and seed-spice crops. Madhya Pradesh’s medium-term growth hinges on revamping its fragmented dealer networks. Collectively, diverging water stress profiles and subsidy regimes create a fragmented adoption landscape, but coordinated national programs keep the total India micro irrigation systems market growth on track.

Competitive Landscape

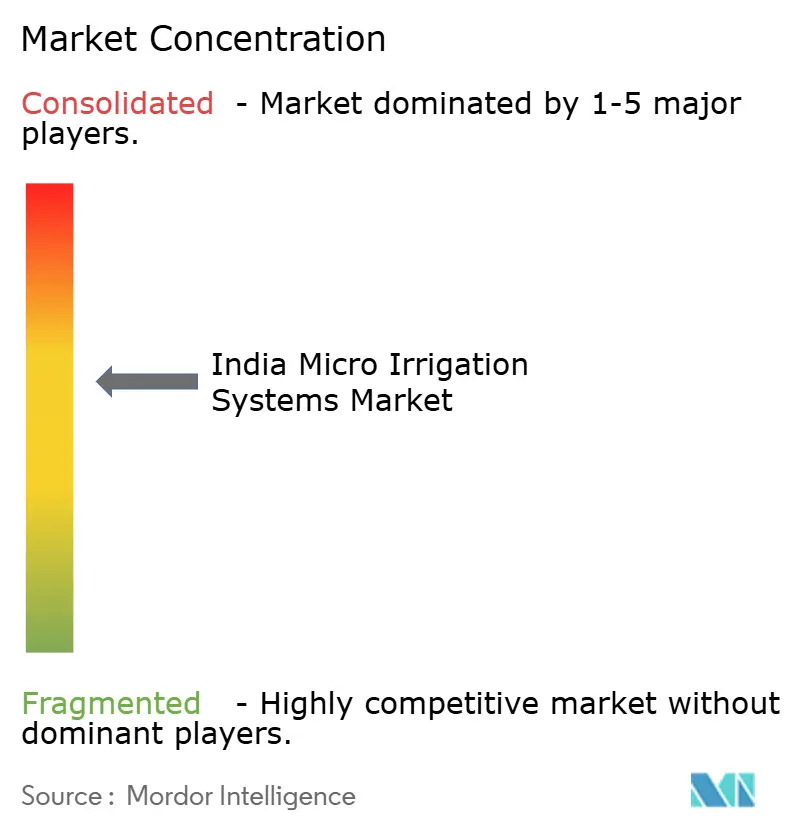

The competitive arena remains moderately fragmented, the top five firms together control a significant share of revenue in 2024. Jain Irrigation Systems Ltd merged its international arm with Rivulis in March 2023, forging a USD 750 million global giant with strong downstream polymer integration. Netafim Irrigation India Pvt Ltd added digital farming to its suite in August 2024, offering remote sensor monitoring and agronomic advisory. Mahindra EPC Irrigation Ltd rebounded to USD 31.6 million (INR 262.33 crore) revenue in FY 2024 on cross-selling through Mahindra & Mahindra Ltd’s tractor dealer network.

Startups such as Fasal integrate micro-climate analytics with drip controllers and have raised funding across several rounds. Domestic polymer pipe majors like Supreme Industries Ltd and Captain Polyplast Ltd leverage backward integration to mitigate polyvinyl-chloride price swings. Service innovation rather than hardware alone is emerging as a differentiator: Netafim’s turnkey model bundles land survey, design, installation, and life-cycle support, raising switching barriers.

Pricing discipline is likely to tighten as players seek volume, but subsidy disbursement delays keep working-capital cycles long. Intellectual property filings in pressure-compensated micro-sprinklers and anti-biofouling emitters indicate rising Research and Development intensity. Overall, technological convergence and financing partnerships are reshaping the India micro irrigation systems market in favor of full-stack solution vendors.

India Micro Irrigation Systems Industry Leaders

Jain Irrigation Systems Ltd

Netafim (Orbia Advance Corporation)

Mahindra & Mahindra Ltd

Rivulis (Temasek)

Kothari Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Uttar Pradesh government has initiated a pilot drip irrigation project for sugarcane farmers across 45 districts. The project covers 25,000 hectares and aims to benefit 20,000-25,000 marginal farmers. The government provides a subsidy of up to 90% on drip irrigation equipment and plans to expand micro-irrigation coverage to 3 million hectares based on the pilot project outcomes.

- April 2025: The Eluru district administration in Andhra Pradesh aims to implement micro-irrigation systems across 8,500 hectares during 2025-26. The initiative provides subsidies up to 100% for small farmers from the Scheduled Castes and the Scheduled Tribes.

- April 2025: The Union Cabinet approved the Modernisation of Command Area Development and Water Management scheme with USD 192 million (INR 1,600 crore) allocation for pressurized pipe networks.

India Micro Irrigation Systems Market Report Scope

Micro irrigation can be defined as the application of water at low volume and frequent intervals under low pressure to plant root zones. The water is irrigated through drippers, sprinklers, foggers, and other emitters on the surface or subsurface of the land.

The micro irrigation in India market is segmented by mechanism (drip irrigation system, sprinkler irrigation system, and other irrigation systems), application (field crops, plantation crops, orchards, vineyards, and turfs and ornamentals), end users (open field and greenhouse), and states. The report offers market sizing in terms of value in USD.

By Mechanism Type

| Drip Irrigation System |

| Sprinkler Irrigation System |

| Fogging |

By Application Type

| Field Crops |

| Plantation Crops |

| Vegetable Crops |

| Orchards and Vineyards |

| Turfs and Ornamentals |

By End User

| Open Field Farms |

| Greenhouses |

| Vertical Farms |

By State

| Rajasthan |

| Maharashtra |

| Andhra Pradesh |

| Karnataka |

| Gujarat |

| Tamil Nadu |

| Madhya Pradesh |

| Uttar Pradesh |

| Telangana |

| Rest of India |

| By Mechanism Type | Drip Irrigation System |

| Sprinkler Irrigation System | |

| Fogging | |

| By Application Type | Field Crops |

| Plantation Crops | |

| Vegetable Crops | |

| Orchards and Vineyards | |

| Turfs and Ornamentals | |

| By End User | Open Field Farms |

| Greenhouses | |

| Vertical Farms | |

| By State | Rajasthan |

| Maharashtra | |

| Andhra Pradesh | |

| Karnataka | |

| Gujarat | |

| Tamil Nadu | |

| Madhya Pradesh | |

| Uttar Pradesh | |

| Telangana | |

| Rest of India |

Key Questions Answered in the Report

What is the current value of the India micro irrigation systems market?

The market is valued at USD 786.25 million in 2026 and is projected to reach USD 1.31 billion by 2031.

How fast is adoption growing in Tamil Nadu?

Tamil Nadu leads growth with a 12.64% CAGR through 2031, fueled by export-oriented horticulture clusters and extra state subsidies.

Which mechanism type commands the largest share?

Drip irrigation systems hold 44.35% of revenue in 2025 due to superior water-use efficiency and adaptable designs.

Why are solar pumps important for precision irrigation?

Solar-powered pumps cut operating costs by eliminating diesel use, making micro irrigation more affordable and reducing greenhouse emissions.

Page last updated on: