Aerospace Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

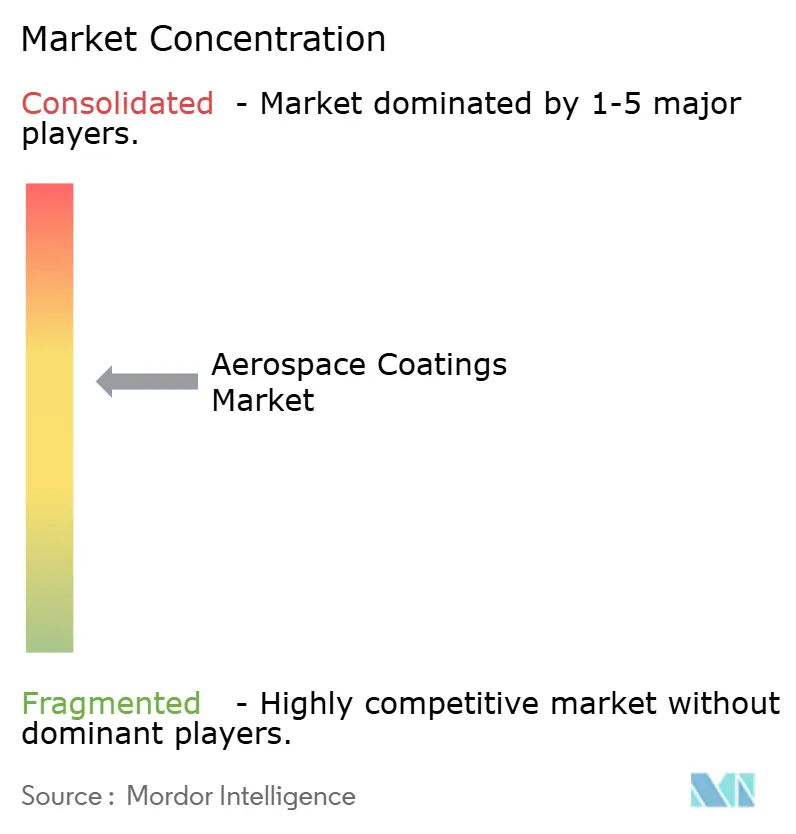

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Coatings Market Analysis by Mordor Intelligence

The Aerospace Coatings Market size is projected to be USD 1.14 billion in 2025, USD 1.19 billion in 2026, and reach USD 1.45 billion by 2031, growing at a CAGR of 4.03% from 2026 to 2031. Composite airframes, stricter volatile-organic-compound rules, and a backlog of deferred heavy maintenance together reinforce a steady demand trajectory. Epoxy-based primers dominate because they bond to carbon-fiber structures that now comprise roughly one-half of next-generation wide-body airframes. Solvent-borne chemistries still lead on legacy military and commercial lines because the certification risk of re-formulating outweighs environmental cost savings. Regionally, North America remains the largest production hub, while Asia-Pacific records the fastest growth as China’s C919 and India’s incentive-linked manufacturing add new paint-shop capacity. Competitive pressure intensifies as scale suppliers invest in water-borne and chromate-free systems to retain qualification advantages.

Key Report Takeaways

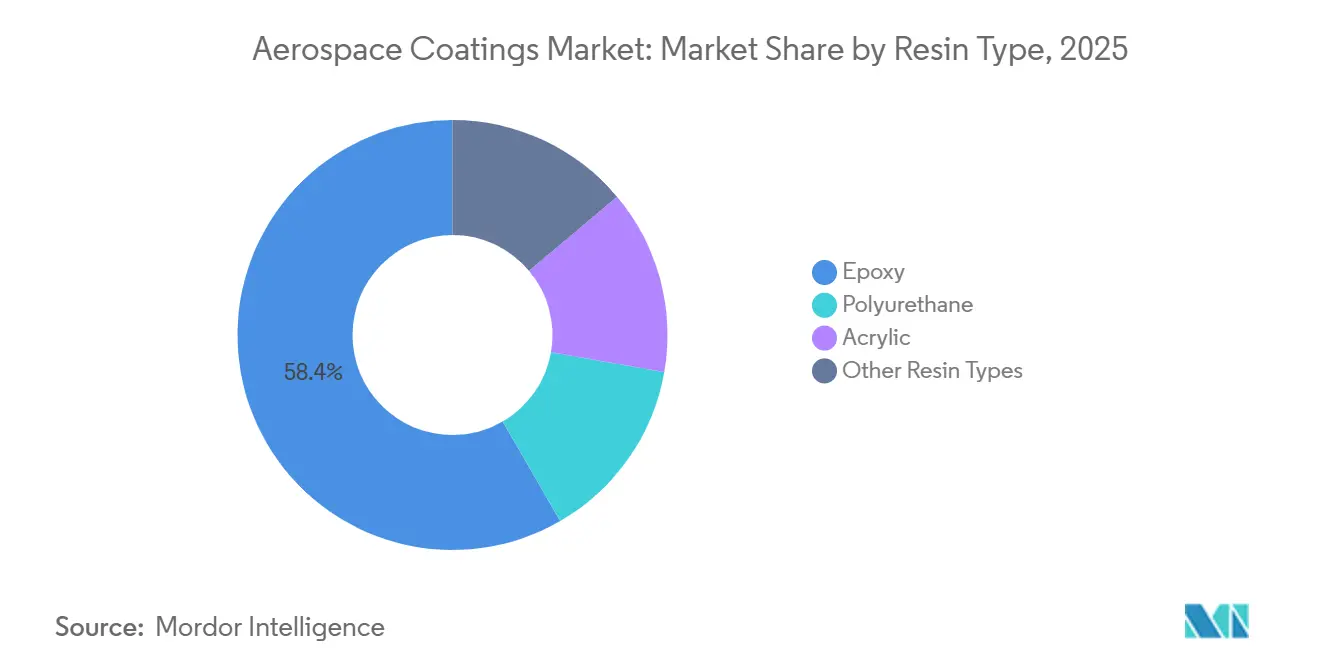

- By resin type, epoxy captured 58.36% of the aerospace coatings market share in 2025 and continues to lead the segment, with a projected CAGR of 4.22% through 2031.

- By technology, solvent-borne systems held 54.41% share of the aerospace coatings market size in 2025, while water-borne alternatives are advancing at a 4.18% CAGR to 2031.

- By end user, original-equipment-manufacturer applications accounted for a 51.55% share in 2025, whereas maintenance, repair, and operations showed the strongest momentum at 4.34% CAGR through 2031.

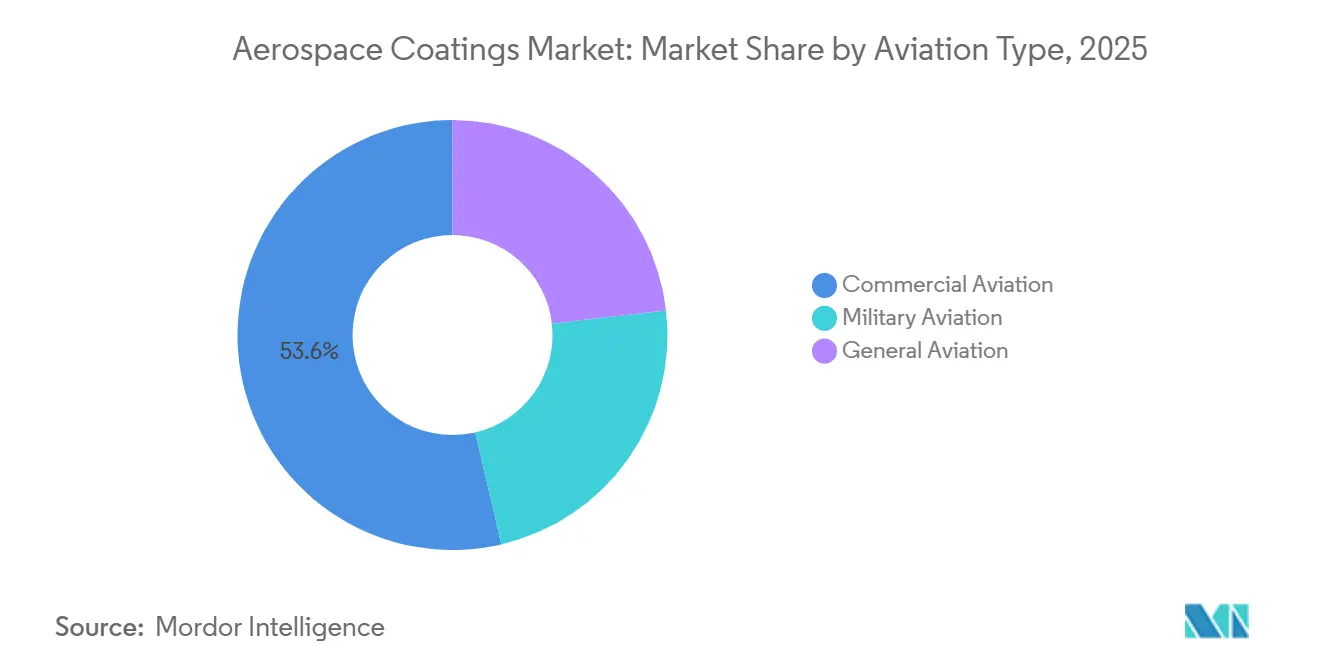

- By aviation type, commercial aviation dominated with a 53.64% share in 2025 and is also expanding at a 4.27% CAGR through 2031.

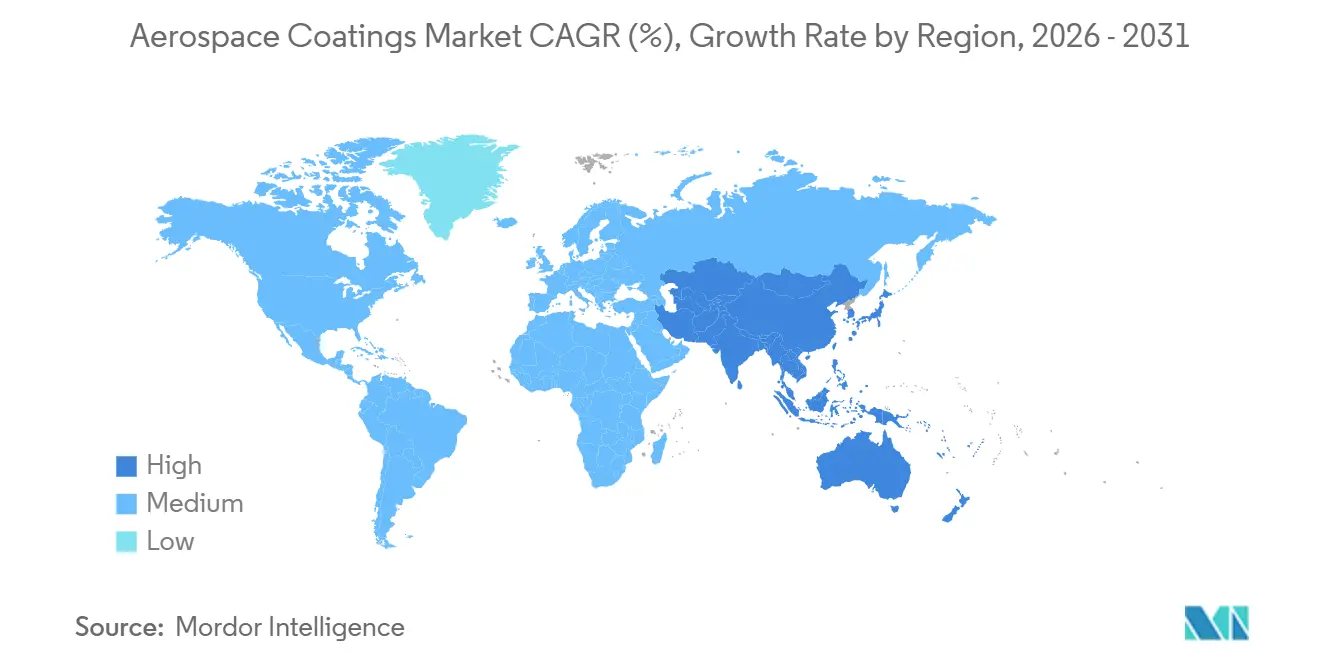

- By geography, North America led with 40.05% of revenue in 2025; Asia-Pacific is set to grow fastest at 3.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerospace Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising production rates of commercial aircraft | +1.2% | Global, centered on North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Increasing use of composites in aircraft manufacturing | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Increasing demand for air travel | +1.0% | Global, highest momentum in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Accelerating maintenance, repair and overhaul demand for aging fleets | +0.8% | North America and Europe core, rising in Asia-Pacific | Short term (≤ 2 years) |

| Increase in manufacturing of aircraft in emerging economies | +0.6% | Asia-Pacific primary, South America secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Production Rates of Commercial Aircraft

In 2025, families like the 737 MAX and A320neo, both single-aisle aircraft, averaged high monthly airframe completion rates. With Airbus projecting a significant number of deliveries for the year, the uptick in build rates translates to heightened volumes of primer and topcoat. This is due to wide-body aircraft requiring more surface coverage compared to their narrow-body counterparts. However, ongoing supply-chain challenges, particularly in titanium forgings and composite prepregs, have led to deferrals in some paint-booth slots, resulting in delayed recognition into later quarters. As a workaround, existing spray lines are operating on dual shifts. This is a temporary measure until the new automated booths, which come with lead times of 18 to 24 months, become operational. Furthermore, the surge in throughput amplifies the demand for quality assurance, especially in areas like in-line color matching and film thickness monitoring.

Increasing Use of Composites in Aircraft Manufacturing

Carbon-fiber structures now make up a significant portion of the weight in Boeing's 787 and Airbus's A350, a notable increase from older aluminum fuselages[1]“Commercial Market Outlook 2025-2044,” Boeing, boeing.com. Epoxy primers, now standard, utilize chromate-free inhibitors. These primers effectively bond with hydroxyl-rich fiber surfaces while steering clear of galvanic corrosion. Formulators incorporate triazole and rare-earth additives to meet required benchmarks. While conductive top coats, which ensure surface resistivity stays low, add to material costs, they're essential for lightning-strike dissipation. Room-temperature-cure epoxy, which bonds without the need for autoclave heat, further enhances composite repairs in service. However, it's worth noting that only a select few suppliers possess current FAA approvals.

Increasing Demand for Air Travel

Global passenger traffic is forecast to grow in 2026, up from two years earlier. Asia-Pacific generates a significant portion of that traffic yet remains under-represented in the aerospace coatings market because OEM airframes are still largely produced in the United States and Europe. Load factors approached high levels in 2024, signaling capacity additions just as OEM order backlogs stretch to a decade. Airlines, therefore, intensify repaint cycles to preserve aesthetics and comply with corrosion directives, shifting orders toward fast-cure top coats that command service premiums.

Accelerating Maintenance, Repair and Overhaul Demand for Aging Fleets

In 2024, the global commercial fleet showed an increase in service age, prompting repaint programs that had been delayed during pandemic-induced groundings. Current FAA airworthiness mandates dictate that heavy checks require complete paint removal, ultrasonic inspection, and re-application every eight to ten years. While each repaint utilizes less material than a factory application, the elevated labor costs associated with aircraft-on-ground penalties amplify revenue per liter. Facilities in Asia-Pacific, particularly in Singapore, Hong Kong, and Guangzhou, now manage a significant portion of the world's heavy maintenance volume. These facilities predominantly import primers and top-coats from North American and European formulators, which are notably on the approved-vendor lists.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns of volatile organic compound emissions | -0.7% | Global, strictest in North America and European Union | Short term (≤ 2 years) |

| Lengthy certification cycles for new chemistries | -0.5% | Global, driven by FAA and EASA standards | Long term (≥ 4 years) |

| Early substitution risk from next-generation fluoropolymer films | -0.3% | North America and Europe first adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Concerns of Volatile Organic Compound Emissions

U.S. regulations limit primer volatile-organic-compound content and top coats. The European Union plans to implement these same limits by 2028[2]“Industrial Emissions Directive,” European Union, europa.eu. Adhering to these standards increases raw material costs as formulators shift to slower-evaporating solvents. Consequently, paint-shop cycle times extend, leading to reduced throughput. While water-borne alternatives can more readily meet these regulations, they require humidity-controlled booths, which produce higher wastewater loads, posing a challenge for smaller maintenance operations. This financial hurdle is driving a trend of consolidation, favoring larger MRO houses with more robust cash flows.

Lengthy Certification Cycles for New Chemistries

Gaining FAA and EASA approvals involves extensive testing like salt-spray, thermal-cycle, and fluid-resistance assessments. Once a coating secures a spot on a type-certificate data sheet, any switch incurs significant re-validation costs. This financial commitment encourages minor adjustments—like adopting non-chromate corrosion inhibitors—over complete polymer changes. Meanwhile, smaller niche formulators are focusing on aftermarket radome and conductive-primer segments, where airline engineers wield influence, allowing them to sidestep OEM procedures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Anchored in Composite Compatibility

Epoxy held 58.36% of the aerospace coatings market share in 2025, and the segment is expected to grow at a 4.22% CAGR to 2031, underscoring a robust demand, particularly in composite-rich fuselages. Polyurethanes, securing the second position, are the top choice for airlines seeking ultraviolet-stable top coats. However, it's worth noting that as suppliers incorporate light-stabilizer packages, the prices of these raw materials are on the rise.

Acrylics, prized for their dielectric properties, cater to specialty radome niches. Yet, their limited chemical resistance curtails wider adoption. Meanwhile, the silicone and fluoropolymer families are experiencing sluggish growth. This is largely due to emerging PFAS restrictions, which pose challenges for OEM qualification. Furthermore, the lengthy certification timelines, often spanning several years, act as a deterrent for disruptive newcomers. As a result, the existing resin hierarchies remain firmly entrenched, at least until the next regulatory cycle.

By Technology: Solvent-Borne Systems Retain Share Despite Environmental Headwinds

Solvent technologies accounted for 54.41% of revenue in 2025, supported by established performance records on military fleets and legacy narrow-body lines. Water-borne systems are advancing at a 4.18% CAGR through 2031 because they meet evolving emission limits without booth-air incineration.

Adoption hurdles linger. Water-borne films cure more slowly in high humidity and produce extra wastewater. Powder coating stays confined to landing-gear and cabin parts because the 180 °C bake impeded composites. MIL-PRF specifications that date back decades ensure a baseline of demand that shields solvent chemistries from rapid displacement.

By End User: Maintenance, Repair and Operations Segment Accelerates on Deferred Backlog

OEM production lines generated 51.55% of the aerospace coatings market revenue in 2025 on the strength of primer-heavy factory paint stacks. The MRO channel is growing at a 4.34% CAGR as airlines clear the delayed heavy-check pipeline left from 2020-2022. While each repaint consumes less material, hourly charges are rising, driven by aircraft-on-ground penalties for wide-body planes.

MRO growth also reflects the wave of 2010-2015 deliveries that now reach their first major repaint window. Asia-Pacific repair centers capitalize on labor arbitrage, though they still import most coating volumes from long-qualified U.S. and European suppliers.

By Aviation Type: Commercial Programs Underpin Long-Term Volume

Commercial aircraft captured 53.64% of spending in 2025 and holds the top growth profile at 4.27% CAGR on the back of single-aisle production. Military orders are more uneven as budget cycles shift; nevertheless, stealth top coats can carry triple the unit price of civil gloss whites.

General aviation is expanding at a sluggish pace, primarily due to its fragmented nature. Over 15 OEMs collectively produce units annually, which curtails potential economies of scale. In contrast, commercial wide-body builds are seeing a surge in demand. This is largely because their larger fuselages necessitate more paint area, bolstering the market share of commercial programs through 2031.

Geography Analysis

North America supplied 40.05% of revenue in 2025, reflecting Boeing assembly in Washington State and an extensive legacy MRO sector. Domestic labor rates, however, motivate carriers to ferry jets to Asia for heavy paint work, tempering volume growth in the region. Europe holds the second-largest position thanks to Airbus' final-assembly lines in Toulouse and Hamburg and to aggressive emission rules that push technical innovation.

Asia-Pacific is the fastest-expanding region at 3.22% CAGR, driven by Chinese and Indian manufacturing initiatives and by its role as a global transit hub. COMAC aims for local content but continues to import essential epoxy primers until domestic suppliers obtain FAA or EASA approvals. However, the Middle East's high concentration of wide-body operators bolsters the demand for coatings, particularly ultraviolet-resistant top coats essential for desert climates.

Tariff regimes and currency swings influence procurement decisions in emerging markets. Brazilian real depreciation, for instance, raises imported resin costs and prolongs reliance on proven solvent-borne systems despite regulatory pressure elsewhere.

Competitive Landscape

The aerospace coatings market is moderately consolidated. Vertical resin integration and proximity to final assembly plants underpin their competitive moat. Certification costs cement decade-long supply positions once a spec is achieved. Niche challengers win share in radome, radar-absorbent, or conductive-primer specialties where faster qualification pathways exist. Technology focus now centers on chromate-free primers, ultra-durable polyurethanes, and digital color-matching tools that reduce waste. Regulatory momentum against PFAS creates white-space for fluorine-free top coats. European suppliers lead early development through joint programs with Airbus, positioning themselves to benefit if new REACH limits tighten after 2028. Meanwhile, U.S. defense programs sustain demand for traditional solvent polyurethanes specified under MIL-PRF-85285, slowing the pace of wholesale reform in that sub-segment.

Aerospace Coatings Industry Leaders

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

BASF SE

Axalta Coating Systems, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: AkzoNobel Aerospace Coatings opened a new color blending and distribution facility in Dubai to cater to the Middle East market. The facility is expected to provide local blending for Aerobase, Aerodur 3001, and Eclipse products, reducing lead times for airlines, OEMs, and MROs.

- May 2025: PPG announced plans to invest USD 380 million to establish a new aerospace coatings and sealants manufacturing facility in Shelby, North Carolina. Construction is scheduled to begin in October 2025 and is projected to be completed in the first half of 2027.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the aerospace coatings market as all factory-applied or maintenance paints, primers, and clear coats that protect fixed-wing and rotary aircraft exteriors and critical interior structures from corrosion, UV, temperature, and wear, while also contributing to livery aesthetics.

(Scope Exclusion) Standalone decorative films and cabin soft-trim dyes that do not provide functional protection are excluded.

Segmentation Overview

- By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Other Resin Types (Silicone, Fluoropolymer, etc.)

- By Technology

- Solvent-borne

- Water-borne

- Other Technologies (Powder,etc.)

- By End User

- Original Equipment Manufacturer (OEM)

- Maintenance, Repair and Operations (MRO)

- By Aviation Type

- Commercial Aviation

- Military Aviation

- General Aviation

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed coating formulators, airline MRO planners, and procurement managers across North America, Europe, and Asia. Conversations clarified real-world strip-and-repaint intervals, average square-meter coverage per narrow-body versus wide-body, and discounting practices that raw filings seldom disclose.

Desk Research

We began with public datasets from bodies such as the Federal Aviation Administration, Eurostat trade codes for HS 3208/3209, and fleet age statistics published by the International Air Transport Association, which reveal repaint cycles by aircraft class. Government VOC regulations, notably EPA 40 CFR Part 63 and ECHA REACH annexes, helped size the addressable shift toward water-borne chemistries. Annual reports and 10-Ks of leading air-framers and tier-one coaters were mined for delivered units, average coating weight per shipset, and price change commentary. Paid intelligence solutions, including D&B Hoovers for company financials and Dow Jones Factiva for global MRO contract news, supplied cross-checks on revenue pools. This list is illustrative; many other validated sources informed our desk assessment.

Market-Sizing & Forecasting

A top-down build starts with active fleet stock, new build projections, and repaint frequency, which are then multiplied by representative coating consumption and blended ASPs. Select bottom-up checks, OEM paint shop throughput, sampled supplier revenues, and channel margin scans tighten totals. Key variables include global RPK growth, defense expenditure trends, regional fleet age, resin price indices, and regulatory phase-outs of chromate primers. A multivariate regression, stress-tested by scenario analysis, projects these drivers to 2030, and gaps in bottom-up values are bridged with primary respondent ranges.

Data Validation & Update Cycle

Outputs undergo outlier scans against historical spend per aircraft, peer coatings ratio, and trade flows; variances trigger re-contacts before analyst sign-off.

We refresh models annually and issue interim revisions when material events, such as OEM rate adjustments, occur.

Why Mordor's Aerospace Coatings Baseline Earns Trust

Published figures differ because firms pick distinct resin scopes, treat OEM and MRO volumes unevenly, or freeze exchange rates months before updates.

Key gap drivers include some studies that fold ancillary cabin finishes into totals, others that adopt optimistic build-rate scenarios despite supply-chain caps, and many that roll forward 2017 ASPs without adjusting for recent titanium-dioxide surcharges, whereas our model re-prices every year using trade-weighted averages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.89 B (2025) | Mordor Intelligence | - |

| USD 2.48 B (2025) | Global Consultancy A | Excludes MRO volumes and updates infrequently |

| USD 1.48 B (2024) | Trade Journal B | Counts only exterior top-coats; omits primers and interior uses |

| USD 3.79 B (2024) | Industry Association C | Uses constant 2022 ASPs and assumes uniform repaint cycles |

The comparison shows that once uniform scope, fresh pricing, and mixed OEM-MRO demand are applied, Mordor's balanced baseline aligns with observable revenue trails and remains the dependable starting point for strategic decisions.

Key Questions Answered in the Report

How large is the aerospace coatings space projected to become by 2031?

It is forecast to reach USD 1.45 billion, up from USD 1.19 billion in 2026, implying a 4.03% CAGR through 2031.

Which resin family leads usage in aerospace paint systems?

Epoxy primers dominate with a 58.36% share in 2025 because they bond effectively to carbon-fiber structures and resist aviation fluids.

Why are water-borne formulations gaining traction?

They help meet new U.S. and EU volatile-organic-compound limits without incineration, and their segment is expanding at a 4.18% CAGR despite humidity-related processing hurdles.

Which region is expected to expand fastest in aerospace coating demand?

Asia-Pacific, projected at a 3.22% CAGR, is propelled by China’s C919 production ramp and India’s incentive-supported assembly lines.

Page last updated on: