Insulin Glargine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

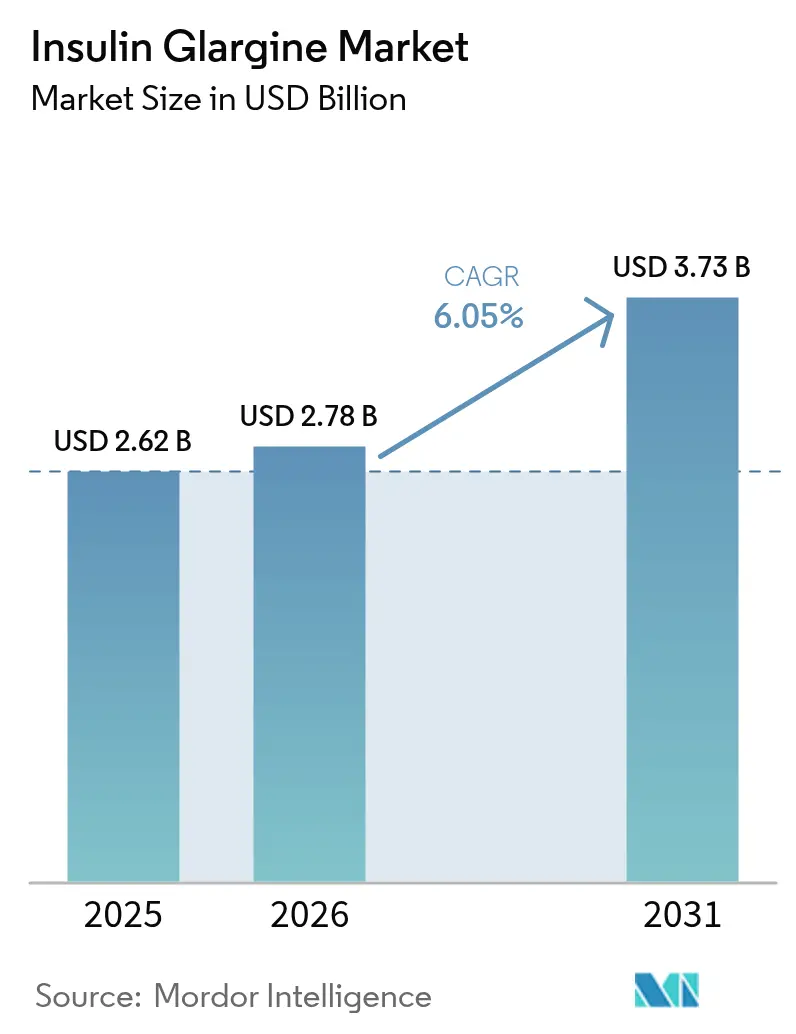

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 3.73 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulin Glargine Market Analysis by Mordor Intelligence

The Insulin Glargine Market size was valued at USD 2.62 billion in 2025 and estimated to grow from USD 2.78 billion in 2026 to reach USD 3.73 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031). This progress is unfolding as global diabetes prevalence exceeds 800 million adults, driving sustained clinical demand for once-daily basal regimens. Biosimilar competition is intensifying price deflation while expanding patient access, especially after Semglee and Rezvoglar gained interchangeability in the United States. Government price caps such as the USD 35 Medicare ceiling are steering prescriber choices toward lower-net-cost options. Meanwhile, the e-pharmacy boom accelerates last-mile distribution, and smart delivery systems sharpen product differentiation. Strategic shifts toward GLP-1 receptor agonists by legacy insulin suppliers add competitive pressure yet preserve glargine’s basal niche.

Key Report Takeaways

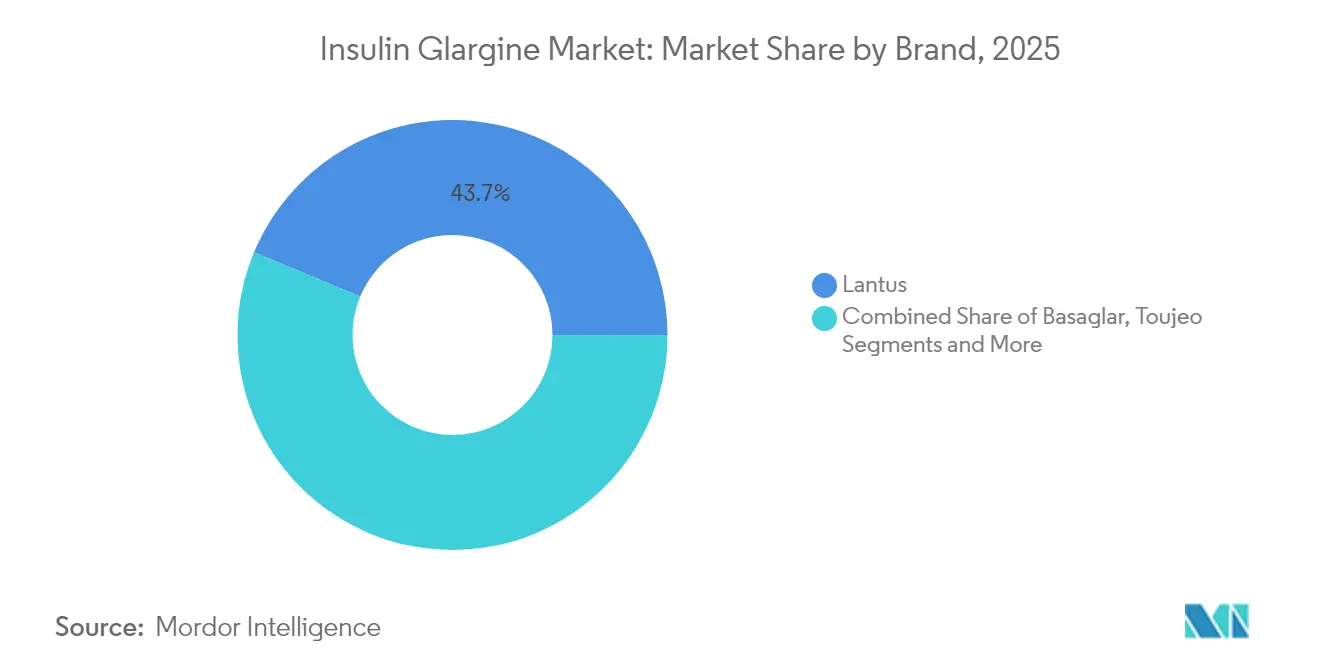

- By brand, Lantus led with 43.72% of the insulin glargine market share in 2025. Glargine Biosimilars are expanding at an 8.25% CAGR through 2031.

- By concentration, U100 formulations captured 70.85% of the insulin glargine market size in 2025. U300 products are forecast to advance at a 6.95% CAGR between 2026-2031.

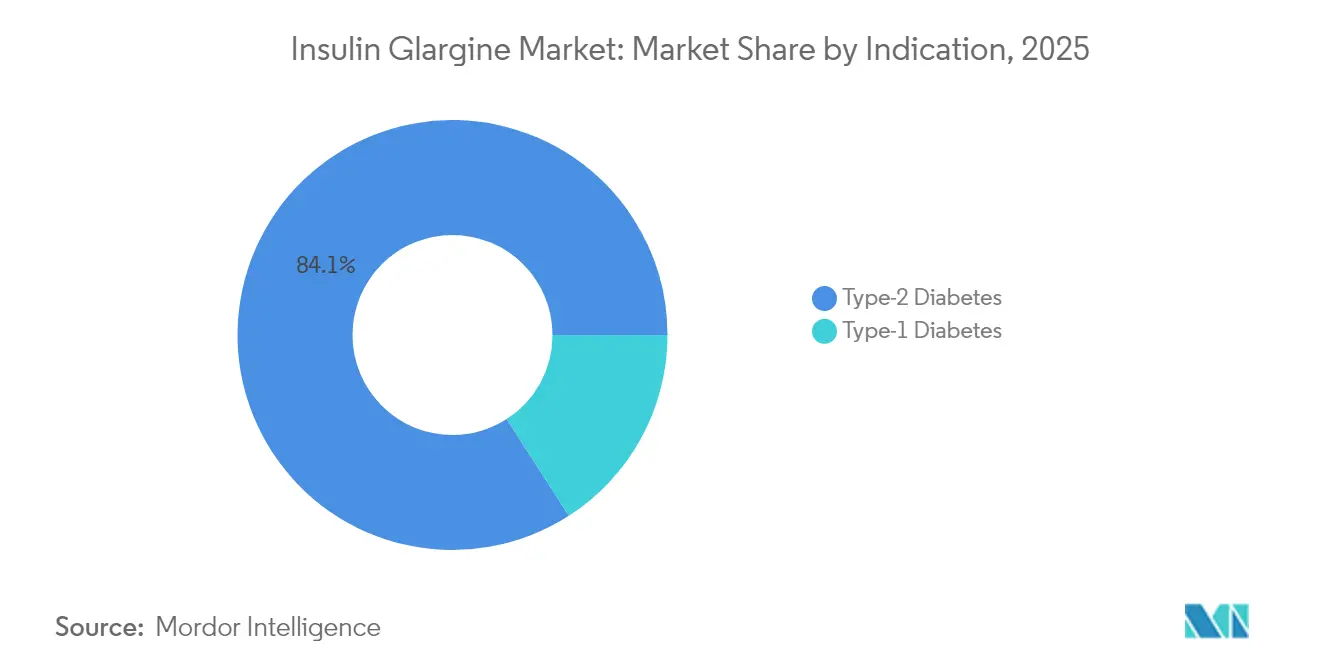

- By indication, type-2 diabetes accounted for 84.10% of volume in 2025. Type-1 diabetes applications are rising at a 6.88% CAGR to 2031.

- By distribution channel, retail pharmacies held 37.95% share of the 2025 value pool. Online pharmacies are projected to climb at an 8.05% CAGR through 2031.

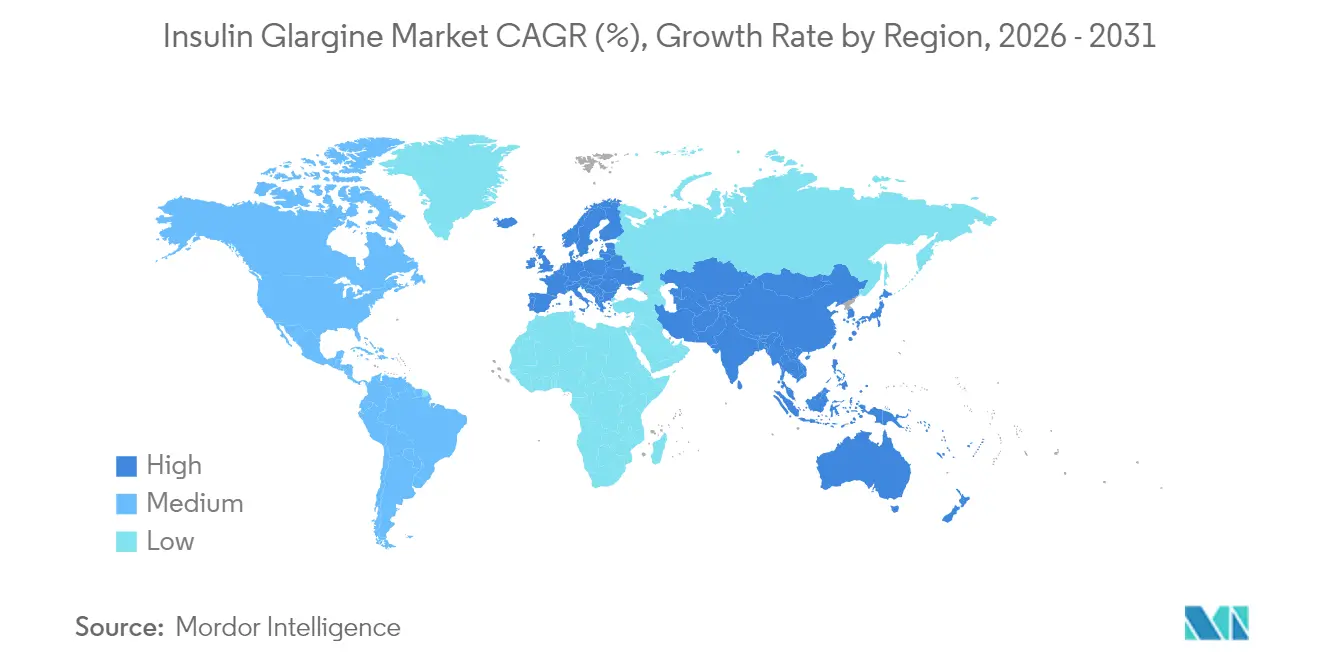

- By region, North America captured 44.98% of the insulin glargine market in 2025, whereas Asia-Pacific is expected to post the fastest growth at an 9.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insulin Glargine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence | +1.8% | Global, peak in Asia-Pacific | Long term (≥ 4 years) |

| Biosimilar insulin glargine | +1.2% | North America and EU; emerging markets next | Medium term (2-4 years) |

| e-pharmacy adoption | +0.9% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Insulin-delivery technology | +0.7% | Developed markets first | Medium term (2-4 years) |

| Government price policies | +0.6% | North America, Europe, select APAC | Short term (≤ 2 years) |

| Physician brand trust | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes

Global diabetes prevalence has quadrupled since 1990 and now affects more than 500 million adults, with projections indicating 852 million cases by 2050. Type 2 diabetes comprises 96% of cases, and two-thirds of individuals initiating basal therapy start with glargine formulations. Incidence is surging in low- and middle-income countries where 90% of untreated patients reside, magnifying unmet need. Regional spikes are steepest in the Middle East and North Africa, while Brazil could see a 400% rise to 43 million cases by 2036.[1]Source: Frontiers in Public Health, “Predicting the prevalence of type 2 diabetes in Brazil,” frontiersin.org The expanding clinical and economic burden, estimated at USD 1,015 billion in 2024, is pushing payers toward cost-effective basal options, strengthening long-run demand for glargine biosimilars.

Emergence of Biosimilar Insulin Glargine

Three FDA-approved glargine biosimilars—two interchangeable—have re-shaped formulary negotiations and unlocked automatic substitution pathways in pharmacies.[2]Source: The Medical Letter, “Rezvoglar – Another Insulin Glargine Product Interchangeable with Lantus,” medicalletter.org Biocon Biologics scaled up capacity while bilateral regulatory alignment between FDA and EMA reduced review times. Brazil streamlined approvals in 2024, enabling domestic programs that cut treatment expenditures by 55.9%. Multisource supply diminishes single-origin risks and lowers budget impact, although developers must still navigate patent thickets and meticulous quality audits.

Rapid Growth of e-pharmacy Channel Widening Home-care Access

Digital pharmacies are dismantling logistical barriers by connecting prescriptions, refill reminders, and remote consultations, trends reinforced during pandemic-era telehealth expansion. The channel’s 8.32% CAGR mirrors the broader digital health surge. Medicare Part D’s 2025 payment-smoothing policy further supports online fulfillment by reducing upfront costs. Data collected via e-pharmacies generate insights into adherence and real-world outcomes, providing actionable feedback to manufacturers. Nevertheless, temperature-controlled shipping raises operating hurdles that favor scale players with dedicated cold-chain networks.

Technological Advancements in Insulin Delivery

Next-generation delivery platforms integrate continuous glucose monitoring with connected pens and miniature patch pumps, fostering personalized dosing. Medtronic’s InPen upgrade received FDA clearance in late 2024, enabling real-time recommendations. Canada and the EU approved once-weekly insulin icodec in 2024, signaling regulatory openness to extended-interval analogs. India’s authorization of inhalable insulin reflects regional appetite for needle-free formats. Collaborative ventures such as PharmaSens–SiBionics aim to commercialize wearable patch pumps. These innovations allow pharmaceutical players to add value beyond molecule parity, shielding margins as biosimilars commoditize the drug substance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High insulin cost | -1.4% | Global, acute in low-income states | Short term (≤ 2 years) |

| Complex approval pathways | -0.8% | Emerging markets | Medium term (2-4 years) |

| Shift to ultra-long analogs | -0.6% | High-income markets first | Long term (≥ 4 years) |

| Injection reluctance | -0.5% | Global, cultural variability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Insulin Therapy

Even after the Medicare cap, affordability gaps persist because 20% of beneficiaries lack Part D coverage and remain exposed to high out-of-pocket spending. US insulin prices still average nearly 10 times OECD levels. Globally, 19.5% of surveyed patients ration doses due to financial strain. Supply shocks compound the issue, illustrated by South Africa’s 2024 pen shortages amid GLP-1 production swings. These cost and availability challenges cap near-term volume growth even as prevalence climbs.

Complex Regulatory and Approval Pathways

Biosimilar developers confront divergent global requirements: the FDA typically demands switching studies, whereas the EMA has begun granting waivers when analytical comparability is robust. Some emerging regulators lack expertise to evaluate intricate biologics, extending approval cycles and deterring local entry. Interchangeability legislation varies widely, adding extra studies and labeling revisions that inflate budgets. Manufacturing audits differ in scope, with some regions requiring site-specific inspections beyond WHO prequalification. While the International Council for Harmonisation is working toward convergence, full alignment remains several years away, delaying broad biosimilar uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Brand: Biosimilars Chip Away at Lantus Leadership

Lantus held 43.72% of 2025 revenue, anchoring the insulin glargine market through longstanding clinical trust and formulary placement. However, glargine biosimilars are leveraging interchangeability to capture switching prescriptions at an 8.25% CAGR. Basaglar, designated a follow-on biologic, exploits value-tier pricing, while Toujeo differentiates with U300 dosing. Soliqua/Suliqua combines glargine with lixisenatide to address multi-drug regimens. Second-generation biosimilars from Gan & Lee and Biomm are entering tender systems in Latin America, indicating accelerating commoditization. Originators respond by bundling devices, digital coaching, and co-pay assistance.

Physician surveys suggest confidence in biosimilar immunogenicity is rising, supported by post-marketing surveillance. Payers are mandating step-therapy that prioritizes lower-net-cost glargine biosimilars before covering originators, accelerating displacement. Nonetheless, clinical inertia favors brands with decades of safety records in vulnerable populations such as pregnant women. Marketing focus is therefore pivoting from molecule attributes to ecosystem value, including smart pen compatibility, digital titration support, and integrated glucose dashboards, tactics intended to protect share in a price-rationalizing landscape.

By Concentration: U100 Prevails yet U300 Gains Momentum

U100 products represented 70.85% of 2025 volume and remain the standard initiation strength worldwide. Familiar insulin-to-carbohydrate ratios and established dosing algorithms give clinicians confidence. However, U300 variants like Toujeo posted a 6.95% CAGR as reduced injection volume and flatter pharmacokinetic curves appealed to adherence-challenged cohorts. Clinical evidence shows lower nocturnal hypoglycemia and tighter fasting glucose ranges with U300 regimens.

Biosimilar developers are expanding portfolios to include both strengths, ensuring formulary parity with originators. Device manufacturers are updating cartridge specifications for dual-strength compatibility, reducing barriers to adoption. Cost differentials remain a restraint: U300 per-unit prices average 18% higher than U100, although lower volume requirements narrow the annual therapy gap. Patient education is critical because dosing confusion can lead to accidental under-treatment. Overall, concentration diversification underscores the ongoing evolution from molecule exclusivity toward holistic treatment experience.

By Indication: Type-2 Diabetes Drives the Bulk of Demand

Type-2 diabetes generated 84.10% of 2025 glargine utilization, making it the anchor indication for commercial forecasts. Progressive β-cell decline necessitates basal coverage once oral agents lose efficacy. Real-world data show two-thirds of basal starts use glargine owing to once-daily scheduling and lower hypoglycemia versus NPH insulin. Meanwhile, type-1 diabetes usage is rising 6.88% annually because of earlier diagnosis and wider CGM access that prompts tighter targets. The insulin glargine market share attributed to type-1 remains smaller but strategic, offering predictable lifetime demand.

Therapeutic protocols for type-1 combine basal glargine with rapid analogs in multiple-daily-injection or hybrid closed-loop systems. Poor glycemic control in Brazil, with average HbA1c near 9%, highlights unmet optimization potential. Pediatric specialists value glargine’s safety record, while weekly icodec may eventually alter basal patterns for adolescents. In type-2 cohorts, combination fixed-dose products integrating GLP-1 agonists may temper stand-alone basal volume, yet affordability concerns will sustain demand for cost-efficient glargine biosimilars over the forecast horizon.

By Distribution Channel: Retail Pharmacies Hold Ground amid Digital Surge

Retail outlets controlled 37.95% of 2025 value, supported by counseling services and patient loyalty programs. Hospital pharmacies cater to complex cases requiring frequent titration, but online platforms are expanding at 8.05% CAGR as legislation normalizes home delivery of temperature-sensitive biologics. The insulin glargine market size handled by e-pharmacies could surpass USD 640.7 million by 2031 under current penetration trends. Leading digital players invest in insulated packaging and data-logging sensors to meet cold-chain mandates. Integration with CGM dashboards allows automated refill prompts based on real-time usage.

Policy changes add momentum: Medicare’s cost-spreading rules reduce up-front expense, encouraging auto-refill enrollment. In rural Asia, smartphone penetration combines with same-day courier networks to bridge access gaps. Still, stringent storage regulations raise hurdles for smaller e-commerce entrants. Physical pharmacies counter by expanding drive-through pickups and pharmacist-led titration clinics, aiming to retain high-value chronic customers through convenient hybrid models.

Geography Analysis

North America persisted as the largest contributor, with 44.98% market share in 2025, benefiting from high diabetes prevalence and premium pricing. The region’s early adoption of biosimilar interchangeability promotes competitive discounts yet preserves substantial volume, while the USD 35 Medicare cap broadens access. Canada’s universal-coverage legislation could further expand treated populations, particularly among low-income seniors. Innovation pipelines for smart delivery devices are concentrated in Silicon Valley and Minneapolis, reinforcing North America’s leadership in integrated care ecosystems.

Europe displayed balanced market maturity and cost-containment rigor. Harmonized EMA guidelines implemented in 2024 shorten biosimilar review times, intensifying tender competition. Western countries such as Germany and France anchor revenue, while Central and Eastern Europe post higher growth from rising diagnosis rates and healthcare investment. Weekly icodec obtained EMA approval, signaling Europe’s receptiveness to paradigm-shifting basal regimens. National procurement agencies increasingly bundle insulin with CGM subsidies, creating holistic tender parameters that reward suppliers offering device integration.

Asia-Pacific remains the fastest-growing (9.05%) territory through 2031, driven by explosive prevalence and policy interventions to alleviate affordability barriers. China’s insulin tender program cut average glargine prices almost in half, boosting treated lives despite compressing unit margins. India unlocked needle-free delivery approvals and domestic manufacturing capabilities, widening therapeutic options. Southeast Asian e-pharmacy start-ups leverage smartphone ecosystems to deliver insulin within hours, bypassing under-resourced rural clinics. However, fragmented regulatory capacity and reimbursement heterogeneity slow cross-border launches, compelling suppliers to tailor country-specific market access strategies.

Competitive Landscape

The insulin glargine market exhibits moderate consolidation dominated by Sanofi, Novo Nordisk, and Eli Lilly. Biosimilar challengers such as Biocon Biologics and Gan & Lee are narrowing the gap by winning hospital tenders and securing interchangeability where available. Originators hedge revenue erosion by investing in GLP-1 franchises and next-generation analogs. Sanofi earmarked an extra EUR 1 billion for French biologics manufacturing in 2024, a move expected to double monoclonal antibody capacity and support insulin innovations. Novo Nordisk accelerates weekly basal trials while leveraging obesity drug windfalls to subsidize insulin discounts. Eli Lilly’s Rezvoglar launch illustrates the strategy of internal biosimilar competition to defend share.

Device partnerships broaden the competitive field. Medtronic’s Smart MDI ecosystem, Tandem-Abbott closed-loop collaboration, and PharmaSens–SiBionics wearable pumps illustrate cross-sector alliances. As payers emphasize outcome-based contracts, suppliers integrating drugs, devices, and data will command negotiating leverage. Local manufacturers in Latin America secure PDP agreements to supply public systems, exemplified by Biomm’s tie-up with Fiocruz for Brazilian glargine production, a template for emerging-market self-sufficiency.

Pricing battles are tempered by cost inflation in sterile-fill facilities and raw materials. Therefore, companies focus on operational excellence and differentiated patient-support programs instead of across-the-board price cuts. Real-world evidence platforms track hypoglycemia rates and adherence, offering value-demonstration tools in negotiations. Overall, competitive intensity will heighten as biosimilar penetration deepens, yet meaningful differentiation persists in delivery technology, wrap-around services, and geographic reach.

Insulin Glargine Industry Leaders

Sanofi Aventis

Novo Nordisk AS

Biocon

Eli Lilly and Company

Julphar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Gan & Lee Pharmaceuticals obtained Pakistan DRAP approval for its insulin glargine cartridge, becoming the Marketing Authorization Holder.

- March 2025: Fiocruz and Biomm partnered to produce insulin glargine for Brazil’s SUS under the Productive Development Partnerships program.

- February 2025: Gan & Lee received Malaysian NPRA registration for its insulin glargine injection and prefilled pen.

- May 2024: Sanofi committed an additional EUR 1 billion to expand French biomanufacturing capacity for biologics, including insulin formulations.

Global Insulin Glargine Market Report Scope

Insulin glargine is a long-acting type of insulin used to treat type 1 and type 2 diabetes mellitus in both adults and children. It provides a steady level of insulin in the body for 24 hours and helps control blood sugar levels. The global insulin glargine market is segmented by type (Lantus, Basaglar, Toujeo, Soliqua/Suliqua, Insulin Glargine Biosimilars) and geography (North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa). The report offers the value (in USD million) and volume (in million mL) for the above segments. This report will provide a segment-wise breakdown (value and volume) for all the countries covered under the table of contents.

| Lantus |

| Basaglar |

| Toujeo |

| Soliqua / Suliqua |

| Glargine Biosimilars |

| U100 |

| U300 |

| Type-1 Diabetes |

| Type-2 Diabetes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Brand | Lantus | |

| Basaglar | ||

| Toujeo | ||

| Soliqua / Suliqua | ||

| Glargine Biosimilars | ||

| By Concentration | U100 | |

| U300 | ||

| By Indication | Type-1 Diabetes | |

| Type-2 Diabetes | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the insulin glargine market?

The insulin glargine market size reached USD 2.78 billion in 2026 and is forecast to climb to USD 3.73 billion by 2031.

How fast is biosimilar glargine growing compared with originators?

Biosimilar alternatives are expanding at an 8.25% CAGR through 2031, notably outpacing the overall 6.05% industry rate as interchangeability drives switching.

Which concentration is gaining momentum in basal insulin therapy?

U300 formulations are recording a 6.95% CAGR thanks to smaller injection volumes and flatter pharmacokinetic profiles that appeal to adherence-focused clinicians.

How are government policies affecting insulin affordability?

Initiatives such as the USD 35 Medicare cap and Chinas volume-based procurement have lowered net prices, widening patient access while compressing manufacturer margins.

Which region shows the highest growth potential?

Asia-Pacific leads future growth because of rising diabetes prevalence, expanding healthcare coverage, and regulatory actions to cut insulin prices.

What technological trends are reshaping basal insulin use?

Integration of smart pens, CGM-linked dosing algorithms, and wearable patch pumps is enhancing adherence and offering new differentiation levers beyond molecule parity.

Page last updated on: