Head And Neck Cancer Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

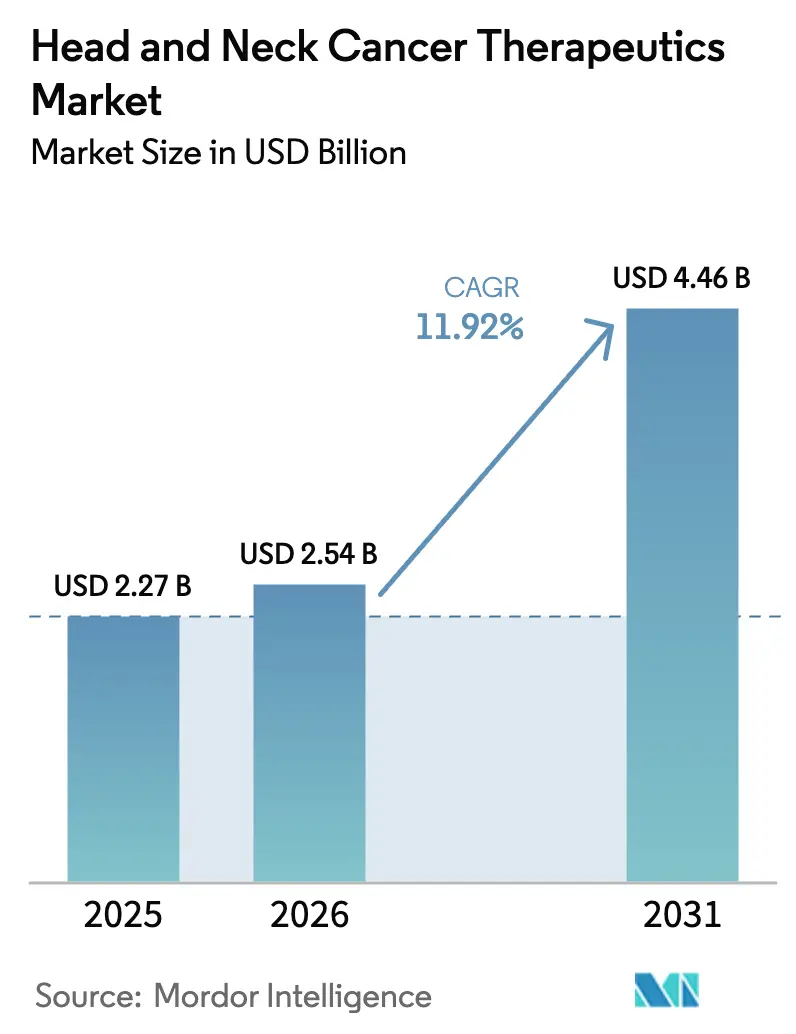

| Market Size (2026) | USD 2.54 Billion |

| Market Size (2031) | USD 4.46 Billion |

| Growth Rate (2026 - 2031) | 11.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

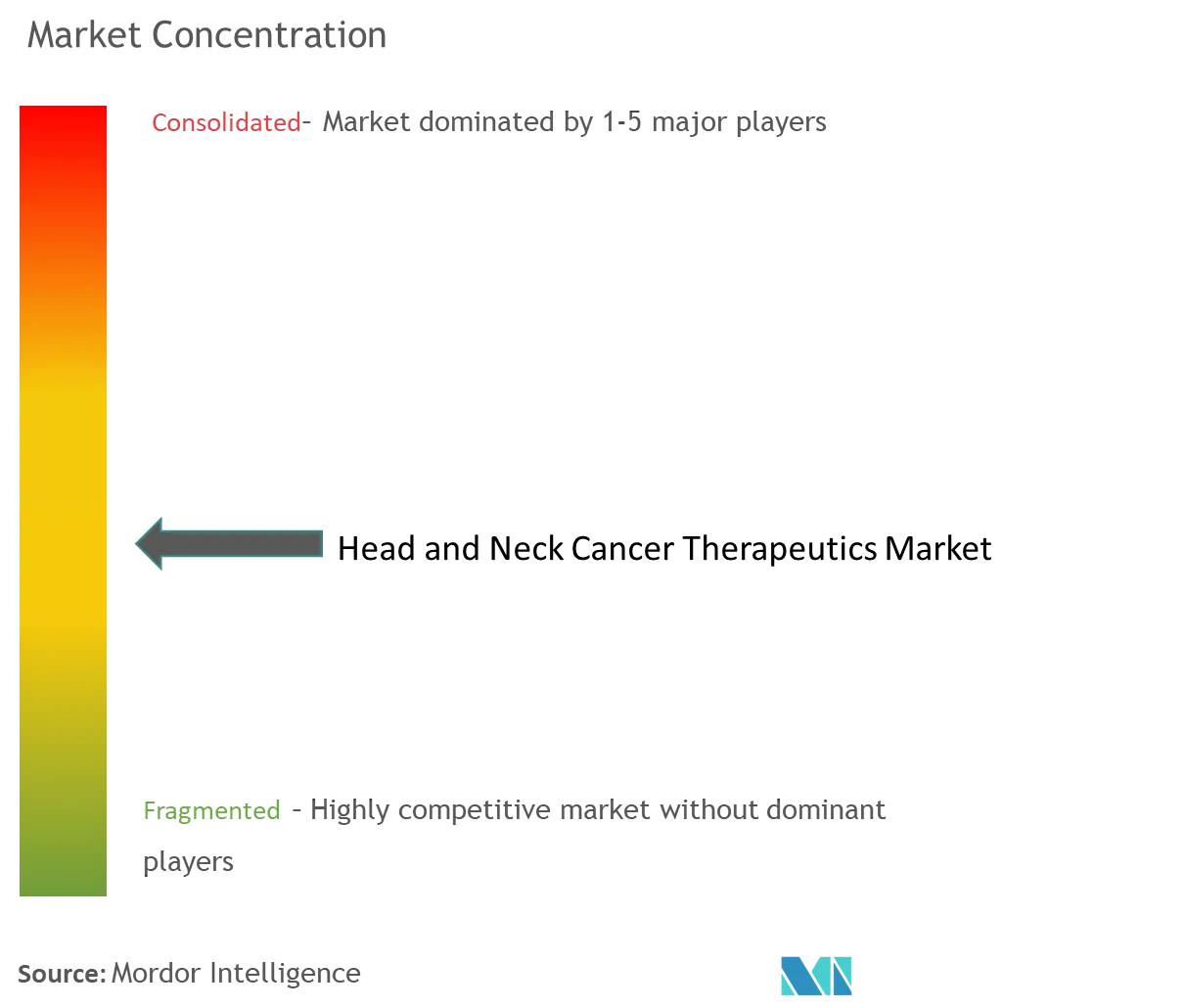

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Head And Neck Cancer Therapeutics Market Analysis by Mordor Intelligence

Head and Neck Cancer Therapeutics market size in 2026 is estimated at USD 2.54 billion, growing from 2025 value of USD 2.27 billion with 2031 projections showing USD 4.46 billion, growing at 11.92% CAGR over 2026-2031. Enhanced regulatory support for immunotherapies, a widening pool of HPV-positive oropharyngeal cases, and the mainstreaming of precision oncology are the core growth levers for the Head and Neck Cancer Therapeutics market[1]Sava, Jordyn. "FDA Approvals & Designations in Oncology: February 2025 Highlights." Targeted Oncology, targetedonc.com . North American payors are reimbursing high-value combinations earlier in treatment lines, while Asia-Pacific’s aggressive HPV vaccination programs enlarge the future addressable population. The June 2025 U.S. approval of peri-operative pembrolizumab for locally advanced disease illustrates how curative-intent use cases now complement palliative indications, reinforcing momentum for the Head and Neck Cancer Therapeutics market[2]Source: Refinitiv StreetEvents, "Q3 2024 Merck & Co Inc Earnings Call " Merck & Co Inc, q4cdn.com . Concurrently, AI-driven imaging achieves diagnostic accuracies up to 100%, enabling earlier patient capture into the Head and Neck Cancer Therapeutics market.

Key Report Takeaways

- By geography, North America controlled 41.88% of the Head and Neck Cancer Therapeutics market share in 2025, whereas Asia-Pacific is advancing at 14.05% CAGR through 2031.

- By drug class, PD-1/PD-L1 inhibitors held 38.52% revenue share in 2025, while FGFR inhibitors post the fastest 13.34% CAGR to 2031 for the Head and Neck Cancer Therapeutics market.

- By indication, oropharyngeal cancer captured 27.21% of the 2025 Head and Neck Cancer Therapeutics market size, and nasopharyngeal cancer is expanding at 13.47% CAGR between 2026-2031.

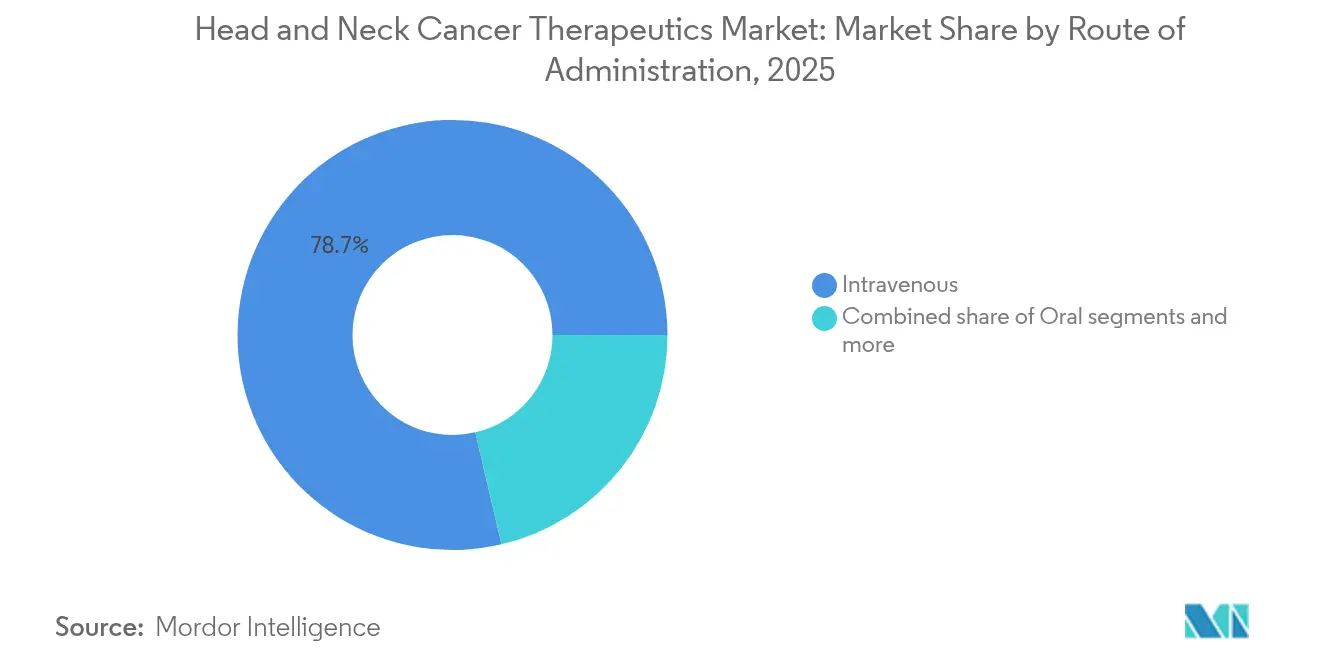

- By route of administration, intravenous therapies accounted for 78.66% of the 2025 Head and Neck Cancer Therapeutics market size, whereas oral products are rising at 13.62% CAGR.

- By end user, hospitals generated 57.85% revenue in 2025, while specialty cancer centers are forecast to lead growth with a 13.86% CAGR for the Head and Neck Cancer Therapeutics market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Head And Neck Cancer Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of HPV-positive oropharyngeal cancers | +2.1% | Global, concentration in North America & Europe | Medium term (2-4 years) |

| Shift toward first-line PD-1/PD-L1 immunotherapies | +2.8% | Global, led by North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Expanding reimbursement & guideline inclusion | +1.9% | North America & EU core, gradual APAC adoption | Medium term (2-4 years) |

| Growing uptake of EGFR-targeted combination regimens | +1.4% | Global, stronger in developed markets | Long term (≥ 4 years) |

| AI-enabled ENT imaging for earlier detection | +0.8% | North America & EU initially, spreading to APAC | Long term (≥ 4 years) |

| Adult-male HPV catch-up programs in Asia-Pacific | +1.2% | APAC core, spillover to emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of HPV-Positive Oropharyngeal Cancers

HPV16/18 strains now underlie roughly 70% of oropharyngeal malignancies in developed economies, redefining therapeutic pathways. HPV-positive tumors demonstrate three-year overall-survival above 85% when pembrolizumab is layered onto backbone regimens, materially outpacing HPV-negative outcomes. The April 2025 breakthrough-therapy designation for petosemtamab plus pembrolizumab specifically targets this cohort, cementing biomarker-guided care. Younger patient demographics expand lifetime-value potential for the Head and Neck Cancer Therapeutics market as better baseline performance status encourages combination use. Screening policies that mandate HPV testing before therapy initiation have become ubiquitous in tertiary centers, standardizing precision-medicine protocols within the Head and Neck Cancer Therapeutics market.

Shift Toward First-Line PD-1/PD-L1 Immunotherapies

Checkpoint-inhibitor combinations now headline first-line standards across several tumor subtypes, replacing platinum-only chemotherapy in most Western guidelines. Pembrolizumab’s peri-operative nod in June 2025 repositions immunotherapy from palliative to curative settings, opening incremental revenue lanes within the Head and Neck Cancer Therapeutics market. Companion diagnostics using PD-L1 combined-positive-score thresholds refine patient selection and optimize payor investment. Real-world evidence has shown durable progression-free-survival gains, offsetting high acquisition costs in value-assessment models. Penpulimab-kcqx’s April 2025 approval for nasopharyngeal carcinoma demonstrates expanding global embrace, broadening the addressable Head and Neck Cancer Therapeutics market outside traditional Western strongholds.

Expanding Reimbursement & Guideline Inclusion

National Comprehensive Cancer Network and parallel European guidelines now list dual-checkpoint or checkpoint-chemotherapy mixes as preferred regimens, smoothing access across high-income systems. Long-term economic models illustrate that durable responses can yield favorable incremental cost-effectiveness ratios, encouraging payors to green-light high ticket therapies within the Head and Neck Cancer Therapeutics market. Coverage, however, remains uneven in low- to middle-income economies, birthing a two-tier treatment landscape that companies attempt to bridge with tiered pricing. Outcome-based contracts are gaining traction, especially for regimens exceeding USD 150,000 annually, presenting new commercial frameworks for the Head and Neck Cancer Therapeutics market. HTA bodies in Asia-Pacific are also fast-tracking decisions when local epidemiology validates high unmet need, shortening time-to-market for new entrants.

Growing Uptake of EGFR-Targeted Combination Regimens

Combining cetuximab with PD-1/PD-L1 blockade re-educates the tumor micro-environment by boosting T-cell infiltration, overriding historical monotherapy limitations. Multiple phase 3 trials indicate additive or even synergistic benefit, stimulating fresh investment into EGFR strategies inside the Head and Neck Cancer Therapeutics market. Biomarker-guided stratification using EGFR expression levels could solidify a precision positioning for legacy assets and elongate their revenue tails. Early adopters among academic centers report improved objective-response-rates without proportionate toxicity surge, encouraging broader community-oncology uptake. Combined-regimen momentum is expected to carve additional market share for the Head and Neck Cancer Therapeutics market through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of IO & targeted drugs | -1.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Severe treatment-related toxicities | -1.2% | Global, all modalities | Medium term (2-4 years) |

| Limited biomarker-testing infrastructure | -0.9% | Primarily APAC & emerging markets | Long term (≥ 4 years) |

| Tumor genetic heterogeneity driving rapid FGFR resistance | -0.7% | Global, advanced disease | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of IO & Targeted Drugs

Annual combination-therapy costs regularly top USD 150,000, straining hospital budgets and national insurance schemes, particularly in resource-constrained settings. Supportive-care expenses balloon when grade 3-4 immune toxicities demand hospitalization, deepening financial toxicity for patients and systems alike. Biosimilar penetration remains minimal for recently launched checkpoint inhibitors, keeping prices elevated and limiting affordability in the Head and Neck Cancer Therapeutics market. Emerging payor models now feature risk-sharing clauses where manufacturers rebate when outcomes fall short, but adoption is still nascent outside Europe. Without aggressive cost-containment mechanisms, budget impact concerns can slow therapy roll-out even in guideline-endorsed settings for the Head and Neck Cancer Therapeutics market.

Severe Treatment-Related Toxicities

Checkpoint inhibitors unleash grade 3-4 immune-mediated events in up to 25% of recipients, including pneumonitis and endocrinopathies that require prompt specialist management. Community oncology practices often lack immunotoxicity expertise, prompting patient transfers to tertiary centers and concentrating demand within high-resource hubs in the Head and Neck Cancer Therapeutics market. Toxicity anxiety among elderly and auto-immune-prone cohorts can delay initiation or cause early discontinuation, eroding real-world adherence. Health-system burden rises when long-term steroid use triggers complications that necessitate hospitalization, dragging down cost-effectiveness ratios. Manufacturers are investing in predictive-toxicology algorithms to pre-empt severe events, but commercial deployment remains early-stage for the Head and Neck Cancer Therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: PD-1/PD-L1 Inhibitors Secure Leadership but FGFR Inhibitors Accelerate

The PD-1/PD-L1 category retained 38.52% market share in 2025 on the strength of pembrolizumab and nivolumab uptake, confirming the central role of immunotherapy in the Head and Neck Cancer Therapeutics market. Pembrolizumab alone delivered USD 29.5 billion in cross-oncology sales during 2024, underscoring practitioner confidence and wide formulary inclusion. EGFR antibodies keep a foothold due to cetuximab’s accepted role in combination protocols, and VEGF blockade remains a niche salvage option, while multikinase inhibitors see narrowing utility amid more selective entrants. FGFR alterations occur in roughly 15% of tumors, positioning selective FGFR inhibitors for 13.34% CAGR, the swiftest within the Head and Neck Cancer Therapeutics market. Resistance emerges within 12 months due to bypass mutations, prompting exploration of combination regimens to preserve benefit. The competitive intensity led Exelixis to cease zanzalintinib development in July 2025, spotlighting the crowded nature of FGFR programs.

In the long run, incremental innovation—such as next-generation T-cell engagers that synergize with checkpoint backbones—could recalibrate segment shares inside the Head and Neck Cancer Therapeutics market. Pricing power likely remains strongest for differentiated biologics that secure breakthrough or orphan designations and deliver measurable survival gains in biomarker-defined populations. Patent-expiry risk spurs originators to invest in new combinations and alternative delivery formats, ensuring lifecycle extension within the Head and Neck Cancer Therapeutics market. Selective degradation of oncogenic proteins via PROTACs and immune-stimulating antibody conjugates represent upcoming developmental horizons that could reshuffle competitive hierarchies. Even so, commercial success will hinge on demonstrating superiority against entrenched immunotherapy anchors that remain the revenue core of the Head and Neck Cancer Therapeutics market.

By Indication: HPV-Driven Oropharyngeal Dominance and Nasopharyngeal Upswing

Oropharyngeal tumors commanded 27.21% of the 2025 Head and Neck Cancer Therapeutics market size on the back of escalating HPV-positive incidence and higher responsiveness to immunotherapy. Younger patient cohorts accept aggressive multi-modality regimens, raising per-patient spend and reinforcing revenue density for the Head and Neck Cancer Therapeutics market. Oral cavity tumors still generate sizable absolute volumes, yet anatomical complexity and frequent comorbidities mute survival gains, limiting premium-pricing scope.

Nasopharyngeal carcinoma boasts the fastest 13.47% CAGR through 2031, catalyzed by penpulimab-kcqx’s first-line approval and endemic prevalence in Southeast Asia, widening therapy demand within the Head and Neck Cancer Therapeutics market. Epstein-Barr virus biology creates distinct immunologic vulnerabilities that companies are exploiting via tailored vaccine and T-cell approaches. Salivary-gland malignancies, though rare, fetch orphan-pricing premiums that outweigh low incidence, contributing profit-rich niches inside the Head and Neck Cancer Therapeutics market. Increasing molecular classification means HPV status, PD-L1 expression, and FGFR alterations are now primary treatment determinants, diluting the historical dominance of strict anatomical labels in the Head and Neck Cancer Therapeutics market.

By Route of Administration: IV Infusion Prevails but Oral Pills Ascend

Intravenous delivery represented 78.66% market share in 2025, enabled by established infusion infrastructures and the biologic nature of most checkpoint inhibitors, cementing revenue stability for the Head and Neck Cancer Therapeutics market. Hospitals and specialty centers invest heavily in infusion suites, ensuring capacity for combination regimens and complex toxicity management. Subcutaneous reformulations could shave chair time and marginally expand catchment areas for the Head and Neck Cancer Therapeutics market, though systemic rollout awaits conclusive pharmacokinetic parity data.

Oral products are advancing at 13.62% CAGR, propelled by selective kinase inhibitors whose chemical properties support adequate bioavailability, giving rise to at-home care models inside the Head and Neck Cancer Therapeutics market. Patient convenience drives strong adherence in younger, working-age demographics, while tele-pharmacy services ensure compliance monitoring. Drug–drug-interaction risks and variable absorption necessitate rigorous education for both clinicians and patients, tempering wholesale migration from IV to oral delivery in the Head and Neck Cancer Therapeutics market. Advances in oral immunomodulators remain early-stage due to stability challenges, suggesting IV will hold primacy through much of the forecast window for the Head and Neck Cancer Therapeutics market.

By End User: Hospital Dominance but Specialty Centers Sprint Ahead

Hospitals generated 57.85% of 2025 revenues owing to integrated surgical, radiation, and medical oncology services that manage complex regimens typical of the Head and Neck Cancer Therapeutics market. Multidisciplinary tumor boards encourage aggressive combination use, supporting higher average selling prices. Academic-center leadership in clinical trials provides early access to investigational agents, reinforcing hospital centrality for the Head and Neck Cancer Therapeutics market.

Specialty cancer centers, however, show a 13.86% CAGR as patients prefer high-throughput facilities with oncology-specific workflows, fueling concentrated demand within the Head and Neck Cancer Therapeutics market. Dedicated infusion suites, point-of-care diagnostics, and on-site compounding shorten wait times and enhance satisfaction, drawing referrals from community clinics. Retail and online pharmacies increasingly distribute oral agents, yet their reach is circumscribed by cold-chain mandates and payer-preferred-site policies within the Head and Neck Cancer Therapeutics market. Hub services that bundle financing assistance and adherence monitoring are critical for unlocking potential beyond bricks-and-mortar infusion settings for the Head and Neck Cancer Therapeutics market.

Geography Analysis

North America remained the top revenue generator with 41.88% share in 2025, buoyed by comprehensive insurance cover and robust clinical-trial pipelines anchoring the Head and Neck Cancer Therapeutics market. Early FDA approvals create first-mover advantages for manufacturers, while real-world evidence networks accelerate guideline adoption. Yet heightened payer scrutiny over $150-k-plus combination regimens imposes rebate pressure, making value-based contracts widespread across the Head and Neck Cancer Therapeutics market.

Asia-Pacific is charting a 14.05% CAGR, the fastest globally, as public-sector funding expands oncology capacity and endemic nasopharyngeal disease lifts demand for specialized immunotherapy in the Head and Neck Cancer Therapeutics market. Japan’s reinstated HPV-vaccination program targets over 1 million women, forecasting reduced future burden yet concurrently heightening screening awareness that channels current patients toward therapy. China and India scale genomic-testing labs, but urban–rural disparities still limit precision-medicine reach, tempering uptake for the Head and Neck Cancer Therapeutics market. Regional governments are piloting outcome-linked reimbursement for high-cost drugs, potentially smoothing affordability barriers over the medium term.

Europe experiences steady growth supported by harmonized regulatory pathways and centralized HTA evaluations that fast-track payer decisions once cost-effectiveness is proven for the Head and Neck Cancer Therapeutics market. However, price renegotiations post-launch are routine, requiring manufacturers to prepare volume-based discounts. Latin America and Middle East/Africa remain nascent but attractive, as multinational drug makers deploy tiered pricing and public-private partnership models to extend the Head and Neck Cancer Therapeutics market footprint.

Competitive Landscape

The Head and Neck Cancer Therapeutics market is moderately consolidated; Merck, Bristol Myers Squibb, and Eli Lilly together captured significant 2024 revenues, leveraging blockbuster checkpoint-inhibitor franchises. High clinical-development costs and biologics manufacturing complexity deter rapid new-entrant penetration, safeguarding incumbents’ share. Nonetheless, biotech innovators armed with bispecific antibodies and cell-therapy modalities are securing breakthrough designations that could reshape competitive order within the Head and Neck Cancer Therapeutics market.

Strategic acquisitions center on mechanism diversification; Merck’s USD 680 million buyout of Harpoon Therapeutics grants it T-cell-engager technology that complements pembrolizumab’s PD-1 blockade, reinforcing portfolio breadth for the Head and Neck Cancer Therapeutics market. Artificial-intelligence platforms delivering 85-100% accuracy in detecting oral premalignant lesions are forging diagnostic alliances with therapy developers, promising earlier pipeline-drug introduction points. Meanwhile, companies pursue geographic white space by tailoring pricing to middle-income markets and embedding local manufacturing to circumvent import tariffs, thereby deepening the global Head and Neck Cancer Therapeutics market.

Investment in real-world-evidence platforms remains pivotal as payors demand proof of durability outside trial settings for high-cost regimens in the Head and Neck Cancer Therapeutics market. Portfolio positioning around biomarker-defined subsets—HPV status, PD-L1 CPS, FGFR alterations—will likely dictate pricing headroom and competitive survivability through 2030 for the Head and Neck Cancer Therapeutics market.

Head And Neck Cancer Therapeutics Industry Leaders

-

Eli Lilly and Company

-

Sanofi

-

Merck & Co., Inc.

-

Clinigen Limited

-

Bristol-Myers Squibb Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Exelixis discontinued zanzalintinib development for advanced head and neck cancer amid intensifying FGFR-inhibitor competition.

- June 2025: FDA approved peri-operative pembrolizumab following KEYNOTE-689 event-free-survival success

Global Head And Neck Cancer Therapeutics Market Report Scope

Head & neck cancer refers to various malignant tumors that form in or near the mouth, nose, larynx, lips, sinuses, and salivary glands. Different drug categories can be used individually or in combination to treat head and neck cancer.

The head and neck cancer therapeutics market is segmented By Type (Chemotherapy, Immunotherapy, and Targeted Therapy), Route of Administration (Injectable and Oral), Distribution Channel (Retail & Specialty Pharmacies, Hospital Pharmacies, and Online Pharmacies), and Geography (North America (United States, Canada, and Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, and Rest of Middle East and Africa), and South America(Brazil, Argentina, and Rest of South America)). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| PD-1/PD-L1 Inhibitors |

| EGFR Inhibitors |

| VEGF/Angiogenesis Inhibitors |

| Multikinase Inhibitors |

| Others |

| Oral Cavity Cancer |

| Oropharyngeal Cancer |

| Nasopharyngeal Cancer |

| Laryngeal & Hypopharyngeal Cancer |

| Salivary Gland & Others |

| Intravenous |

| Oral |

| Others |

| Hospitals |

| Specialty Cancer Centers |

| Retail & Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Drug Class | PD-1/PD-L1 Inhibitors | |

| EGFR Inhibitors | ||

| VEGF/Angiogenesis Inhibitors | ||

| Multikinase Inhibitors | ||

| Others | ||

| By Indication | Oral Cavity Cancer | |

| Oropharyngeal Cancer | ||

| Nasopharyngeal Cancer | ||

| Laryngeal & Hypopharyngeal Cancer | ||

| Salivary Gland & Others | ||

| By Route of Administration | Intravenous | |

| Oral | ||

| Others | ||

| By End User | Hospitals | |

| Specialty Cancer Centers | ||

| Retail & Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the 11.92% compound annual growth of the Head and Neck Cancer Therapeutics market?

Rising HPV-positive oropharyngeal incidence, first-line adoption of PD-1/PD-L1 combinations, expanded reimbursement, AI-enabled early detection tools, and APAC HPV vaccination programs collectively accelerate demand.

Why does Asia-Pacific outpace other regions despite lower current share?

Rapid healthcare investment, endemic nasopharyngeal cancer, and government-funded HPV vaccination generate a 14.05% CAGR that eclipses mature-market growth rates.

What limits wider FGFR-inhibitor adoption?

Quick resistance onset linked to tumor heterogeneity often truncates benefit within a year, compelling developers to explore combination regimens for durability.

How significant are immunotherapy-related toxicities?

Grade 3-4 immune-related adverse events affect up to one-quarter of patients and can prompt permanent discontinuation, necessitating specialized multidisciplinary care teams.

Where does artificial intelligence add value today?

Deep-learning ENT imaging systems reach up to 100% diagnostic accuracy for early oral lesions, allowing clinicians to intervene sooner and improve long-term outcomes.

Page last updated on: