Lithotripsy Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

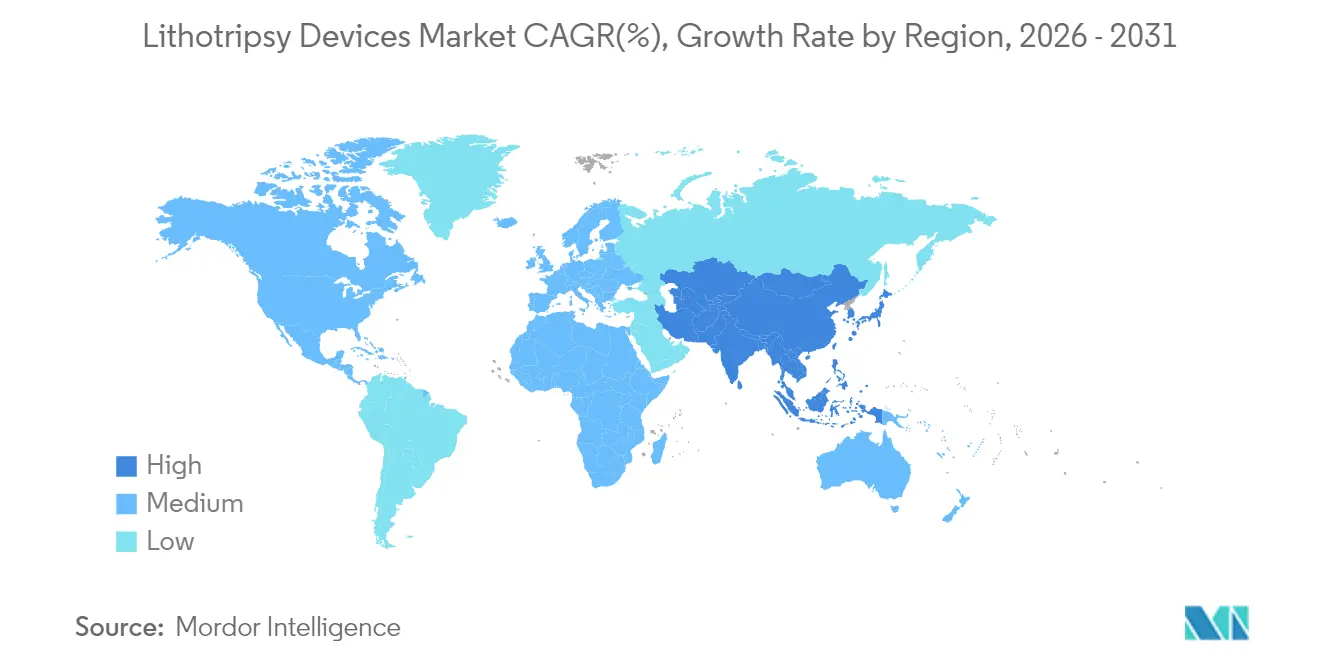

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

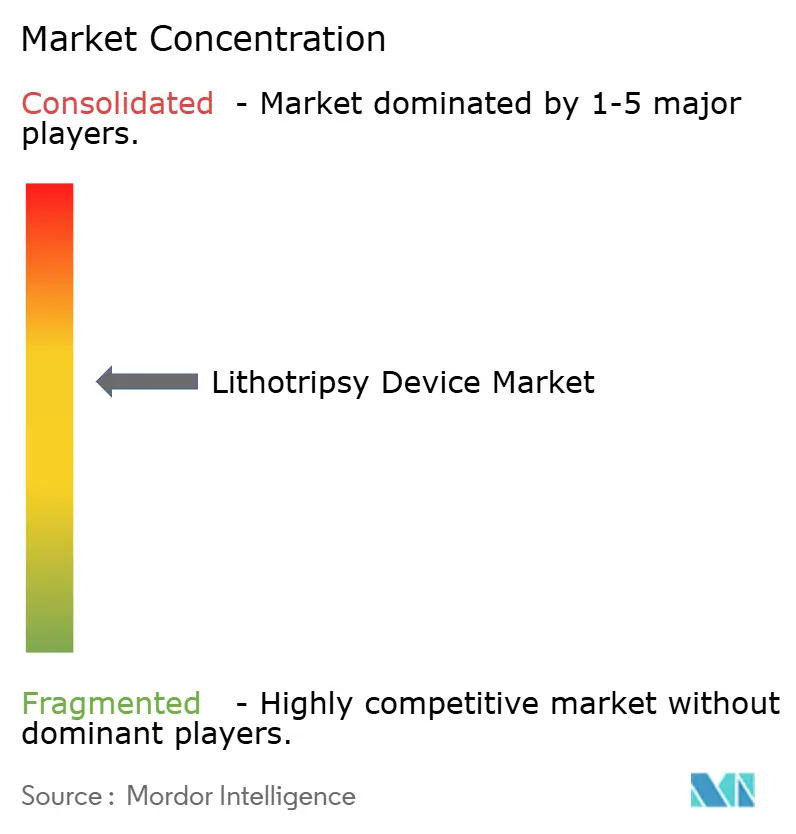

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lithotripsy Device Market Analysis by Mordor Intelligence

The lithotripsy device market size is expected to grow from USD 1.75 billion in 2025 to USD 1.84 billion in 2026 and is forecast to reach USD 2.36 billion by 2031 at 5.10% CAGR over 2026-2031. The value trajectory signals an industry pivot from traditional extracorporeal shock-wave systems toward precision-guided, minimally invasive platforms that simplify workflows and raise stone-clearance rates. Growth is reinforced by advanced imaging integration, the commercial rollout of thulium-fiber and other next-generation lasers, and expanding ultrasound-based technologies that permit anesthesia-free treatment. Portable solutions are broadening point-of-care capacity, while favorable reimbursement revisions in large economies continue to shift volumes from inpatient suites to ambulatory surgical centers. Asia Pacific’s infrastructure build-out, combined with regulatory modernization, is unlocking new demand pockets and diversifying geographic revenue streams within the lithotripsy device market.

Key Report Takeaways

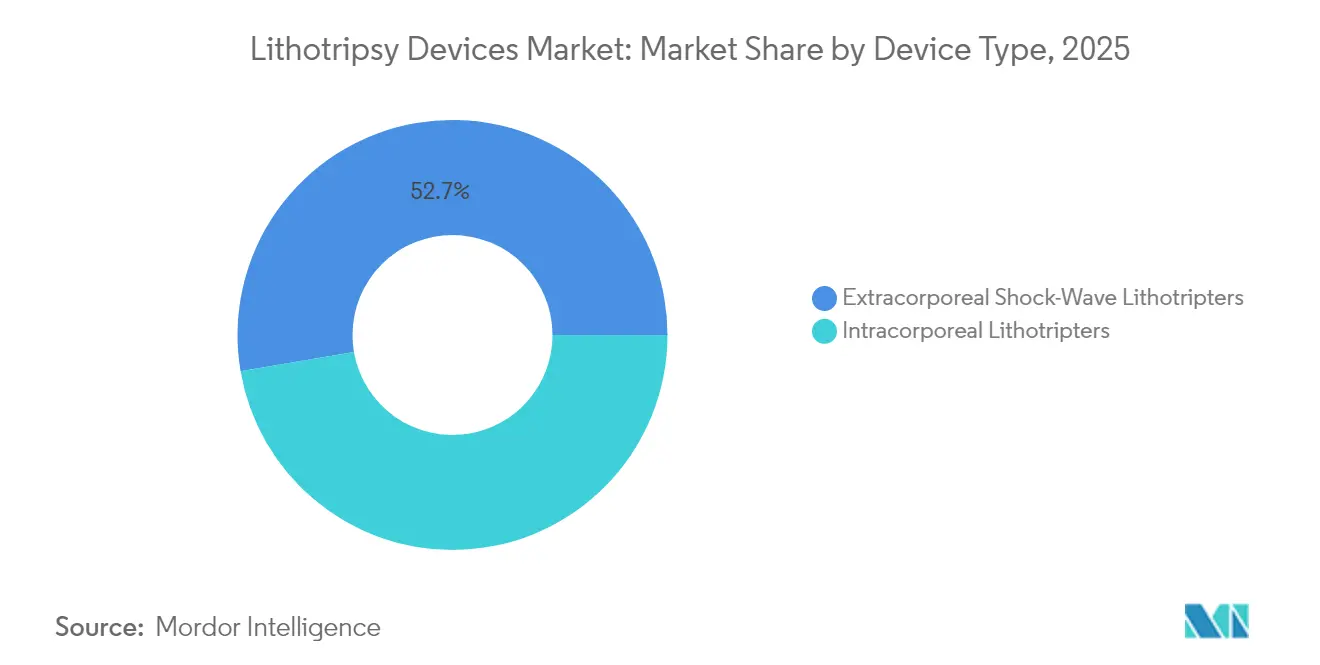

- By device type, extracorporeal shock-wave lithotripters led with 52.70% of lithotripsy device market share in 2025, while intracorporeal platforms are projected to grow at a 5.74% CAGR through 2031.

- By modality, stand-alone systems held a 65.05% share of the lithotripsy device market size in 2025, whereas portable units are advancing at a 6.08% CAGR to 2031.

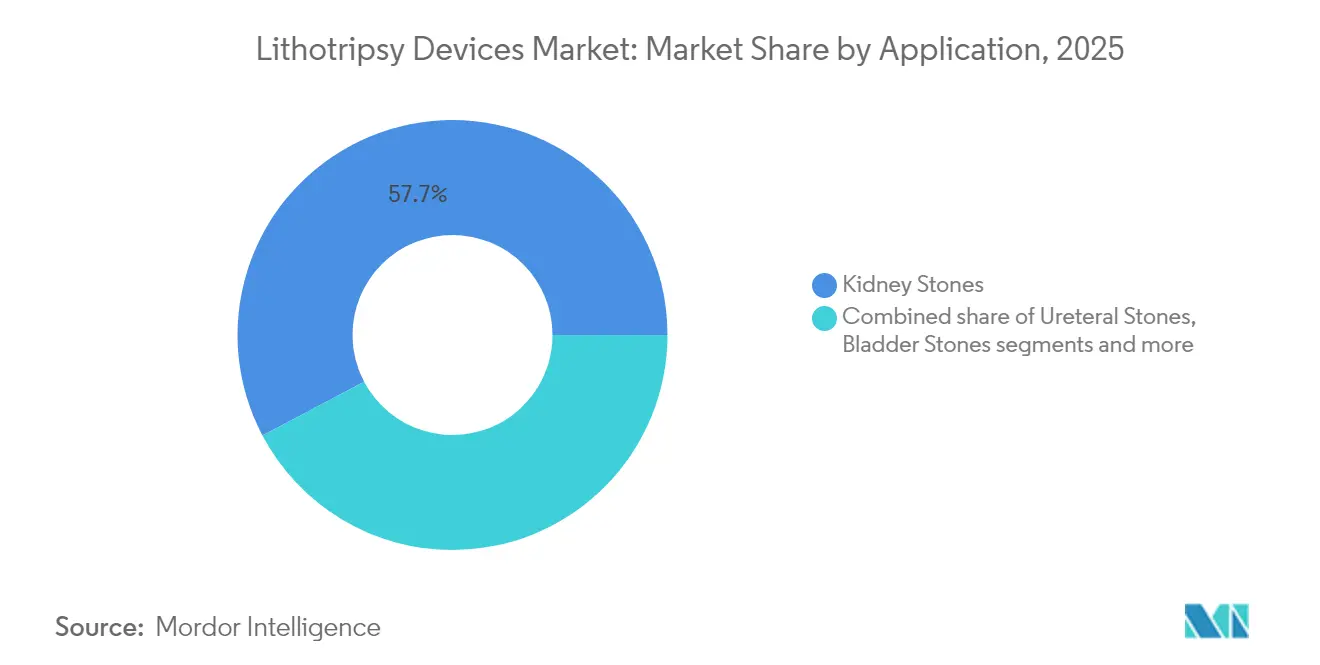

- By application, kidney stones accounted for 57.74% of the lithotripsy device market size in 2025; pancreatic stone treatment is the fastest-growing application at a 6.62% CAGR through 2031.

- By end user, hospitals commanded 51.10% of the lithotripsy device market size in 2025, but ambulatory surgical centers are expanding at a 6.86% CAGR to 2031.

- By geography, North America captured 32.21% of lithotripsy device market share in 2025, while Asia Pacific is forecast to accelerate at a 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Lithotripsy Device Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global incidence of kidney and urinary tract stones | +1.2% | Global, with higher impact in North America and Europe | Long term (≥ 4 years) |

| Continuous technology evolution toward non-invasive, high-precision lithotripsy platforms | +1.8% | Global, led by North America and Asia Pacific | Medium term (2-4 years) |

| Rising adoption of day-care/ambulatory stone-management procedures | +1.1% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Expansion of healthcare infrastructure and surgical capacity in emerging economies | +0.9% | Asia Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Broadening reimbursement coverage for stone-fragmentation treatments across major markets | +0.7% | North America and Europe primarily | Short term (≤ 2 years) |

| Integration of advanced imaging and navigation systems enhancing procedural success | +0.6% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Global Incidence of Kidney and Urinary Tract Stones

Stone disease prevalence is climbing across every major region due to diet shifts, sedentary habits, and dehydration patterns that potentiate mineral crystallization in urinary tracts. Shock-wave lithotripsy still posts 50–75% success among eligible patients, yet its limitations open room for modern devices that can address harder stones and wider patient profiles. Clinical trials report 88% fragmentation and nearly 49% stone-free status with burst-wave ultrasound, illustrating efficacy gains over legacy systems.[1]Source: Applied Radiology, “Portable Ultrasound Technology Found Safe, Effective for Treating Urinary Stones,” appliedradiology.com Market demand consequently favors solutions that secure higher clearance in fewer sessions, reinforcing steady volume growth within the lithotripsy device market.

Continuous Technology Evolution Toward Non-Invasive, High-Precision Platforms

Thulium-fiber lasers, vortex-beam ultrasound, and optimized energy-delivery algorithms are rewriting device specifications and clinical protocols. Olympus’s SOLTIVE platform lowers procedure time by 20% and boosts fragmentation efficiency by 33% compared with Holmium YAG lasers.[2]Source: Olympus Medical Americas, “SOLTIVE SuperPulsed Laser System Shortens Kidney Stone Procedure Time,” medical.olympusamerica.com Boston Scientific’s MOSES 2.0 reduces retropulsion by 50% and enables 90% same-day discharge, making it attractive for outpatient workflows.[3]Source: Boston Scientific, “MOSES 2.0 Technology for Lithotripsy,” bostonscientific.com Academic prototypes such as Lithovortex showcase low-cost ultrasound designs that promise non-invasive fragmentation for broader patient cohorts. These advances help providers elevate outcomes while trimming anesthesia use, fueling premium-priced system demand across the lithotripsy device market.

Rising Adoption of Day-Care/Ambulatory Stone-Management Procedures

Ambulatory surgical centers (ASCs) receive incremental reimbursement support, including new pass-through codes for single-use ureteroscopes, which make outpatient stone removal economically viable. Ultrasound modalities capable of anesthesia-free treatment suit emergency departments and rapid-turnover clinics, slashing resource utilization while preserving outcomes. Consequently, device vendors are intensifying R&D into compact, plug-and-play systems that migrate lithotripsy volumes from inpatient suites to ASCs, expanding the lithotripsy device market footprint.

Expansion of Healthcare Infrastructure and Surgical Capacity in Emerging Economies

China’s policy drive to resolve hospital debt and revive procurement is restoring device purchasing budgets. India’s 2024 marketing code introduces clearer compliance standards, encouraging foreign entrants and transparent competition. Japan’s rapid uptake of thulium-fiber lasers underscores how Asia Pacific buyers adopt advanced platforms soon after launch. Robust infrastructure investment thus helps lift procedural capacity, drawing global manufacturers deeper into emerging-market channels and reinforcing CAGR expansion for the lithotripsy device market.

Restraints Impact Analysis of Lithotripsy Device Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse post-ESWL complications | -0.8% | Global, with higher impact in cost-sensitive regions | Medium term (2-4 years) |

| Availability of URS / PCNL alternatives | -1.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| High upfront and lifecycle costs of lithotripsy systems limiting capital purchases | -1.2% | Global, particularly emerging markets and smaller healthcare facilities | Long term (≥ 4 years) |

| Reimbursement disparities and budget constraints in cost-sensitive regions | -0.9% | Asia Pacific, MEA, and South America primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse Post-ESWL Complications

Stone street formation and other side effects from shock-wave therapy remain clinical concerns, especially for lower-pole renal stones where flexible ureteroscopy achieves 90.2% stone-free rates versus ESWL’s 61.5%. Manufacturer exits from the ESWL segment and clinician shifts toward endoscopic modalities illustrate growing selectivity. Although burst-wave refinements may revitalize extracorporeal offerings, safety perceptions continue to cap ESWL spend within the lithotripsy device market.

High Upfront and Lifecycle Costs of Lithotripsy Systems

Capital intensity restricts procurement, with small hospitals deferring purchases or opting for rental models. EDAP TMS sold only 2 lithotripters in Q1 2024 versus 4 in the prior year, underscoring budget headwinds. The NIH summarizes that device reimbursement demands robust clinical evidence, adding time and expense to market entry. Leasing services, such as HealthTronics’ fleet, partly mitigate barriers but underline persistent affordability challenges that drag on lithotripsy device market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Lithotripsy Device Market Segment Analysis

By Device Type:

Intracorporeal Systems Gain Precision EdgeExtracorporeal shock-wave units captured 52.70% of lithotripsy device market share in 2025, yet intracorporeal platforms are forecast to rise at 5.74% CAGR through 2031. Laser-based systems, especially thulium-fiber models, fragment stones twice as quickly at half the power of earlier lasers, a performance win that has shifted hospital investment priorities. Electromagnetic ESWL devices keep traction in high-volume centers because of their procedural familiarity, while piezoelectric variants carve out specialized niches where precise energy targeting is essential.

Intracorporeal advances dovetail with the broader surgical trend toward precision and minimal tissue insult. Laboratory evidence shows 92% fragmentation under optimized settings, widening clinical acceptance of these tools. Ultrasonic lithotrites with aspiration enhance percutaneous workflows, and pneumatic devices persist in difficult cases needing mechanical impact. Collectively, these dynamics lift the intracorporeal portion of the lithotripsy device market while pushing vendors to diversify portfolios beyond legacy extracorporeal units.

By Modality:

Portable Systems Transform Point-of-Care TreatmentStand-alone suites held 65.05% of the lithotripsy device market size in 2025, anchored by well-equipped hospital units handling complex cases with integrated imaging. Yet portable and tabletop designs are pacing the modality race with a 6.08% CAGR. Break Wave ultrasound shows how mobility and anesthesia-free performance can broaden access to emergency departments and rural clinics. The Lithovortex prototype amplifies this shift by packaging vortex-beam capability into an affordable footprint suited for budget-restricted settings.

Operational flexibility is critical. Portable systems shorten room turnover, fit multi-department use, and lower facility overhead, making them popular with ASC administrators aiming for strong throughput. Vendors are thus engineering hybrid configurations—compact enough for transport yet robust enough to integrate with fluoroscopy—ensuring continued relevance across multiple care environments within the lithotripsy device market.

By Application:

Pancreatic Stones Drive Specialized GrowthKidney stones accounted for 57.74% of the lithotripsy device market size in 2025, but pancreatic stone treatment is advancing quickest at 6.62% CAGR as gastroenterologists embrace endoscopic ultrasound-guided lithotripsy. Bile-duct management also benefits from electrohydraulic energy delivered via cholangioscopes, adding procedure types to hospital offerings.

Ureteral and bladder applications remain staples in urology departments, where flexible scopes and laser fibers yield high stone-free ratios. Salivary-duct stone removal, though niche, is gaining traction in ENT settings thanks to miniaturized lithotripters. The widening array of anatomical indications is expanding device utilization hours, underpinning broader revenue prospects for the lithotripsy device market.

By End User:

Ambulatory Centers Lead Migration TrendHospitals retained 51.10% usage share in 2025, but ambulatory surgical centers (ASCs) are on a 6.86% CAGR trajectory. Transitional Pass-Through payments for single-use scopes lower capital thresholds, helping ASCs add stone-management lines without ballooning budgets. Specialty clinics concentrate domain expertise, streamlining scheduling and post-operative care.

Hospital systems are responding with hybrid care models that intertwine inpatient resources and outpatient efficiency, ensuring they remain referral hubs for complex presentations. Urgent-care sites and mobile units, grouped under “Others,” extend reach into communities with limited specialist access. Across these settings, demand converges on devices that marry clinical sophistication to workflow simplicity, reinforcing the growth outlook for the lithotripsy device market.

Geography Analysis

North America Lithotripsy Device Market

North America accounted for 32.21% of lithotripsy device market share in 2025, supported by transparent reimbursement pathways and a dense ASC network. Hospitals exploit Medicare coding stability to justify equipment refresh cycles, while vendors enjoy receptive early-adopter physician bases. The region’s robust after-sales service networks further safeguard utilization uptime, sustaining replacement demand.

Europe Lithotripsy Device Market

Europe follows with mature yet steadily modernizing health systems. National health funds encourage minimally invasive interventions, accelerating adoption of newer lasers and portable ultrasound. Cross-border purchasing frameworks support multicountry tenders that often favor vendors offering comprehensive training and maintenance, a factor strengthening pan-regional product footprints.

APAC, MEA and South America Lithotripsy Device Market

Asia Pacific is forecast to grow at 7.18% CAGR thanks to infrastructure expansion, regulatory reforms, and rising per-capita income. Japan’s USD 40 billion medical-device sector is investing heavily in IoT-enabled equipment that maximizes operating-room productivity. China’s debt-relief strategy is unblocking hospital CAPEX budgets, and India’s conduct code is fostering market transparency. Middle East & Africa plus South America trail in absolute value but are accelerating as new private hospitals and public-sector projects equip operating theaters, broadening the global footprint of the lithotripsy device market.

Regulatory Landscape

In the United States, extracorporeal shock wave lithotripters fall under FDA Class II device regulation (21 CFR 876.5990) and typically proceed through the 510(k) pathway, with FDA guidance shaping evidence requirements around shockwave generation, targeting/localization, and associated imaging components. For safety and performance demonstration, manufacturers commonly align technical files with FDA-recognized consensus standards such as IEC 60601-2-36 for extracorporeally induced lithotripsy equipment.

In Europe, lithotripsy systems are governed by the EU Medical Device Regulation (MDR) (EU) 2017/745, which remains in force as of January 2026, and many systems are assessed under MDR classification rules that often place them in Class IIb. Regulatory monitoring intensified after the European Commission released COM(2025)1023 on 16 December 2025 proposing amendments to MDR annexes, keeping conformity-assessment planning, clinical evaluation documentation, and legacy-device transition management in focus for suppliers selling across EU member states.

Competitive Landscape

The lithotripsy device market shows moderate fragmentation with technology-rich incumbents and a pipeline of venture-backed challengers. Olympus booked JPY 175,038 million (USD 1.17 billion) in Therapeutic Solutions revenue in Q2 FY2025 on strong SOLTIVE sales that captured hospital attention for shorter case times.

EDAP TMS channels roughly 10% of revenue into R&D, nurturing high-frequency ESWL refinements and next-generation focal therapy platforms. Dornier MedTech, Karl Storz, Cook Medical, Siemens Healthineers, and Storz Medical all hedge portfolios across extracorporeal and intracorporeal solutions, ensuring coverage of diverse procedural segments.

White-space innovators include Avvio Medical and Stone Clear. Portfolio breadth, M&A agility, and post-purchase service capabilities remain decisive factors as competitors jostle for mindshare among surgeons and procurement committees.

Lithotripsy Device Industry Leaders

EDAP TMS

DirexGroup

Boston Scientific Corporation

Cook Medical LLC

Olympus Corp.

- *Disclaimer: Major Players sorted in no particular order

Lithotripsy Device Market Companies Covered in this Report

- Advanced MedTech (Dornier MedTech)

- Boston Scientific

- Siemens Healthineers

- Olympus Corp.

- EDAP TMS

- Storz Medical

- Karl Storz

- Beckton Dickinson

- Cook Group

- DirexGroup

- EMS Electro Medical Systems

- Lumenis

- Richard Wolf

- WIKKON (Guangzhou)

- Allengers Medical Systems

- Teleflex

- Nidhi Meditech Systems

- SonoMotion

- Elmed Medical Systems

Market Opportunities and Future Outlook

Non-invasive, anesthesia-sparing ultrasound lithotripsy and adjunct fragment-management technologies open space for systems engineered around outpatient throughput and point-of-care deployment, rather than fixed-suite workflows. SonoMotion reported in May 2026 that its Break Wave pivotal S.O.U.N.D trial met primary endpoints supporting ultrasound-based stone fragmentation without anesthesia, and it also received FDA clearance for a next-generation Break Wave device with a smaller footprint intended for ambulatory and multi-department placement constraints. These steps keep near-term commercialization and procurement discussions centered on portability, room turnover, and reduced anesthesia burden.

Laser platform refresh and consolidation are another opportunity area as providers modernize intracorporeal toolchains for ureteroscopy and PCNL efficiency. BD introduced the Elyra Thulium Fiber Laser System in May 2026 in two configurations positioned for stone dusting workflows and reduced stone migration, while published work on pulsed thulium:YAG platforms adds options for buyers comparing ablation efficiency, retropulsion behavior, and service models. In parallel, FDA Breakthrough Device Designation granted to Avvio Medical for its Enhanced Lithotripsy System (ELS) in October 2025 highlights an innovation pathway aimed at non-invasive kidney stone treatment using microbubble-enhanced acoustic cavitation, indicating differentiated technology competition across procedure setting, patient experience, and total episode cost rather than energy modality alone.

Recent Industry Developments in Lithotripsy Device Market

- May 2026: Boston Scientific reported that the FRACTURE IDE trial of its SEISMIQ 4CE Coronary Intravascular Lithotripsy catheter met primary safety and effectiveness endpoints. The readout strengthens Boston Scientifics clinical foundation for expanding intravascular lithotripsy across additional vascular indications and supports subsequent regulatory and commercialization steps for the platform.

- May 2025: Avvio Medical announced successful first-patient treatments with its investigational Enhanced Lithotripsy System (ELS) following FDA IDE approval. The milestone advanced clinical validation for a non-invasive, anesthesia-sparing approach and positioned the program for broader trial execution and competitive differentiation versus legacy shock-wave systems.

- November 2024: SonoMotion received FDA de novo clearance for the Stone Clear device, an ultrasound platform designed to externally mobilize residual fragments following lithotripsy. Clearance established a new regulated category for post-procedure fragment management and added an adjacent, workflow-oriented product lever for providers seeking fewer repeat interventions.

Lithotripsy Device Market Report Scope and Research Methodology

Market Definition and Coverage

For this report, the market covers revenues from newly manufactured lithotripsy devices used to break urinary tract stones during urology procedures, across hospital, ambulatory surgery, and specialty clinic settings, and across major regions.

Scope exclusions: This sizing does not count intravascular lithotripsy systems or devices intended only for gall-stone lithotripsy.

Segments Covered in This Report

- By Device Type

- Extracorporeal Shock-Wave Lithotripters

- Electrohydraulic ESWL

- Electromagnetic ESWL

- Piezoelectric ESWL

- Intracorporeal Lithotripters

- Laser Lithotripters

- Ultrasonic Lithotripters

- Pneumatic/Ballistic Lithotripters

- Electrohydraulic Intracorporeal

- Extracorporeal Shock-Wave Lithotripters

- By Modality

- Stand-alone Systems

- Portable / Table-top Systems

- By Application

- Kidney Stones

- Ureteral Stones

- Bladder Stones

- Bile-duct Stones

- Pancreatic Stones

- Salivary-gland Stones

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with urolithiasis disease burden and procedure context so the demand pool stayed realistic, then it moved to technology adoption signals that can be tracked over time. Public inputs that helped frame these assumptions included CDC health statistics, National Institutes of Health and NCBI literature, WHO health data, OECD health indicators, and selected guidance and publications from urology societies.

We also reviewed manufacturer annual reports, investor presentations, product documents, regulatory and recall updates, and reputable medical press to understand device replacement cycles and purchasing patterns. For market mapping and cross-checking, we used paid subscriptions for company financials and intelligence, news and financials, and patent databases. These sources helped validate active product pipelines and positioning. The desk sources noted above are illustrative only and not exhaustive, and many other references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test what we built from public data, especially on how ESWL and intracorporeal lithotripsy are selected in routine practice, and how capital equipment budgets translate into unit shipments. We spoke with both device-side and care-side experts, and we ensured coverage across the major demand regions so the model assumptions did not lean too heavily on one geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 41% | EMEA: 36% |

| Smaller Players: 20% | Managers: 45% | Americas: 18% |

Market-Sizing & Forecasting

The market value is reconstructed using a top-down approach, where urolithiasis prevalence, treatment seeking rates, and procedure splits are converted into a realistic equipment and disposable demand pool, then translated into revenue using typical pricing ranges. To keep results grounded, we corroborate the totals with selective bottom-up approximations, such as supplier roll-ups from sampled portfolios, channel checks on placements, and unit volume checks in higher transparency countries.

Key inputs we track include kidney stone and ureteral stone case volumes, the ESWL versus ureteroscopy mix, installed base and replacement timing for lithotripters, utilization levels in hospitals and ambulatory surgery centers, and average selling price movement by technology class (for example, laser versus shock wave systems). Where direct unit data is not visible, gaps are handled with conservative proxy steps, such as using procedure throughput bands per site and validating the chosen band through primary feedback.

For forecasting, scenario analysis is used so a base case can be separated from faster and slower adoption paths, and then the growth curve is checked against expert expectations for procedure growth, equipment refresh cycles, and expected pricing pressure. Another analyst should be able to repeat the steps with the same public indicators and the stated assumptions.

Data Validation & Update Cycle

Validation is done through cross-checks that look for inconsistencies between the model and independent signals, such as procedure volumes, device placements, and stated clinical adoption trends. If a variance looks unusual, the inputs are rechecked, assumptions are challenged in a second analyst review, and follow-up outreach is triggered with the relevant respondent types.

Reports are refreshed annually, and interim updates are made when material events can shift demand or pricing assumptions. Before delivery, an analyst completes a fresh pass on items like currency timing, recent regulatory news, and major product activity so clients receive the most current view available at that time.

Mordor Intelligence's Lithotripsy Devices Market Size Compared Against Other Published Estimates

Published market values for lithotripsy devices can vary even when the same keywords are used, since different publishers may apply different product coverage, revenue inclusion rules, and base-year conversion timing. Differences also come from how procedure trends are translated into device demand, which is why the same year can show different totals.

Some external figures are broader because they fold in non-urinary stone indications or attach service revenue to the equipment value. For Mordor Intelligence, the count is limited to newly manufactured urinary tract stone lithotripsy systems, and intravascular and gall-stone focused devices are excluded so the demand pool stays clinically comparable.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.84 B (2026) | |

| Industry Publisher A | USD 1.91 B (2025) | The figure can be lifted when factory-gate values are bundled with related services and when additional stone indications (such as pancreatic or bile duct) are included in the same market total. |

| Market Publisher B | USD 1.64 B (2024) | Using an earlier base year and a wider application list can shift the total downward or upward depending on what is treated as device revenue versus supporting components, and it also changes currency timing and inflation assumptions. |

Overall, the gap across sources is mostly explained by indication coverage and what gets counted as device revenue in the first place. When the inputs are tied back to procedure mix, placements, and realistic ASP bands, the final number stays traceable to checks that can be repeated during the next refresh.

Key Questions Answered in the Report

What technology innovations are most influencing new lithotripsy systems?

Next-generation thulium-fiber lasers, vortex-beam ultrasound, and advanced imaging integration are improving fragmentation efficiency, shortening procedure time, and reducing the need for anesthesia. These capabilities appeal to surgeons who seek faster, more predictable stone-clearance outcomes.

Why are ambulatory surgical centers increasingly choosing portable lithotripsy platforms?

Portable units fit smaller procedure rooms, require minimal setup, and allow facilities to schedule same-day cases without tying up fixed hospital theatre space. Their mobility and lower overhead align with the cost-containment goals driving outpatient care.

How are reimbursement policies shaping purchasing decisions for lithotripsy devices?

Expanded coding for single-use endoscopes and clearer payment pathways for ultrasound-based stone management are helping providers justify capital investment. Conversely, gaps in coverage for older extracorporeal systems can delay replacement cycles.

Which clinical applications are expanding beyond traditional kidney-stone treatment?

Providers are increasingly applying lithotripsy to pancreatic, bile-duct, and salivary-gland stones. Success in these niche areas is encouraging vendors to design accessories and energy-delivery modes tailored to gastroenterology and ENT workflows.

What role does device service and maintenance play in vendor selection?

Hospitals and clinics favor manufacturers with reliable service networks and flexible leasing or rental options. Strong after-sales support minimizes downtime, which is critical for high-volume stone-management programs.

How are emerging markets influencing product design?

Facilities in developing regions prioritize systems that are compact, energy-efficient, and easy to operate without extensive infrastructure. Manufacturers are responding by offering hybrid platforms that combine robust performance with simplified user interfaces.

Page last updated on: