Activated Carbon Fiber Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

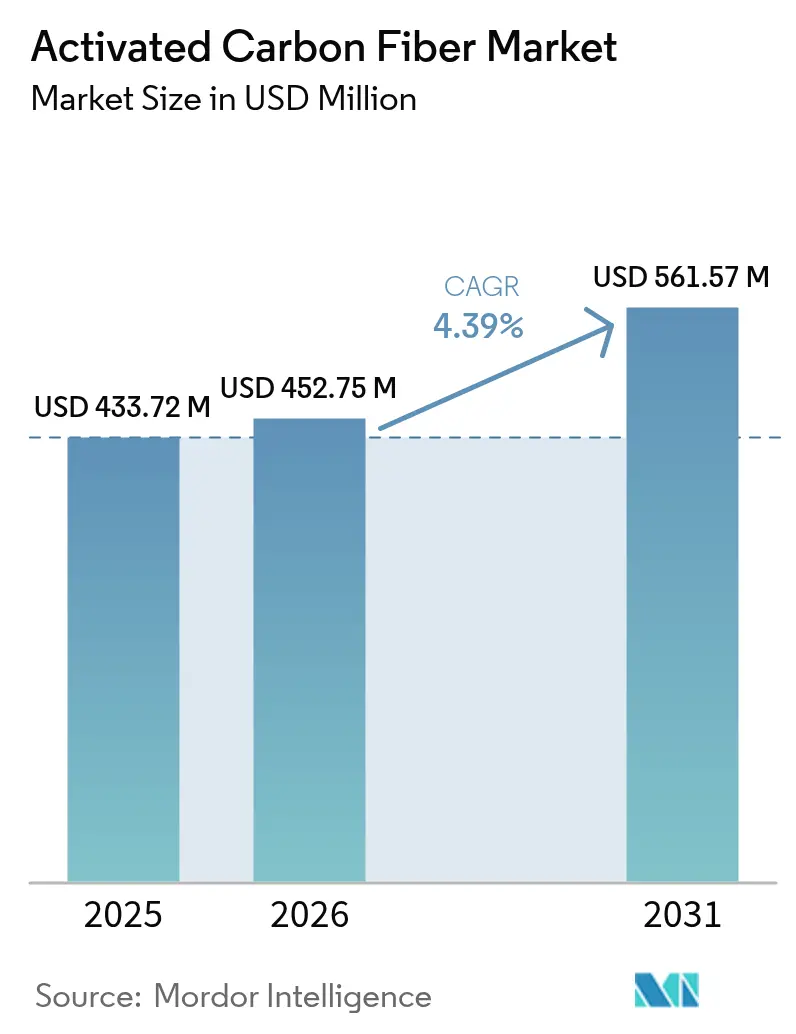

| Market Size (2026) | USD 452.75 Million |

| Market Size (2031) | USD 561.57 Million |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Activated Carbon Fiber Market Analysis by Mordor Intelligence

The Activated Carbon Fiber market size is expected to grow from USD 433.72 million in 2025 to USD 452.75 million in 2026 and is forecast to reach USD 561.57 million by 2031 at 4.39% CAGR over 2026-2031. This steady trajectory reflects a material that thrives in niches where high volumetric efficiency, rapid adsorption-desorption cycles, and strict environmental compliance outweigh price sensitivity. Demand intensifies as semiconductor fabs, sterilization facilities, and chemical processors turn to advanced adsorbents that help them meet tightening air-quality laws without expanding equipment footprints. Medical applications register the fastest uptake as hospitals adopt point-of-use filters and personal protective textiles designed for stringent indoor-air targets[1]U.S. Environmental Protection Agency, “National Emission Standards for Hazardous Air Pollutants,” epa.gov. Asia-Pacific preserves cost leadership and proximity to electronics clusters, yet North America and Europe show resilience through aggressive decarbonization policies and renewed investment in domestic supply chains.

Key Report Takeaways

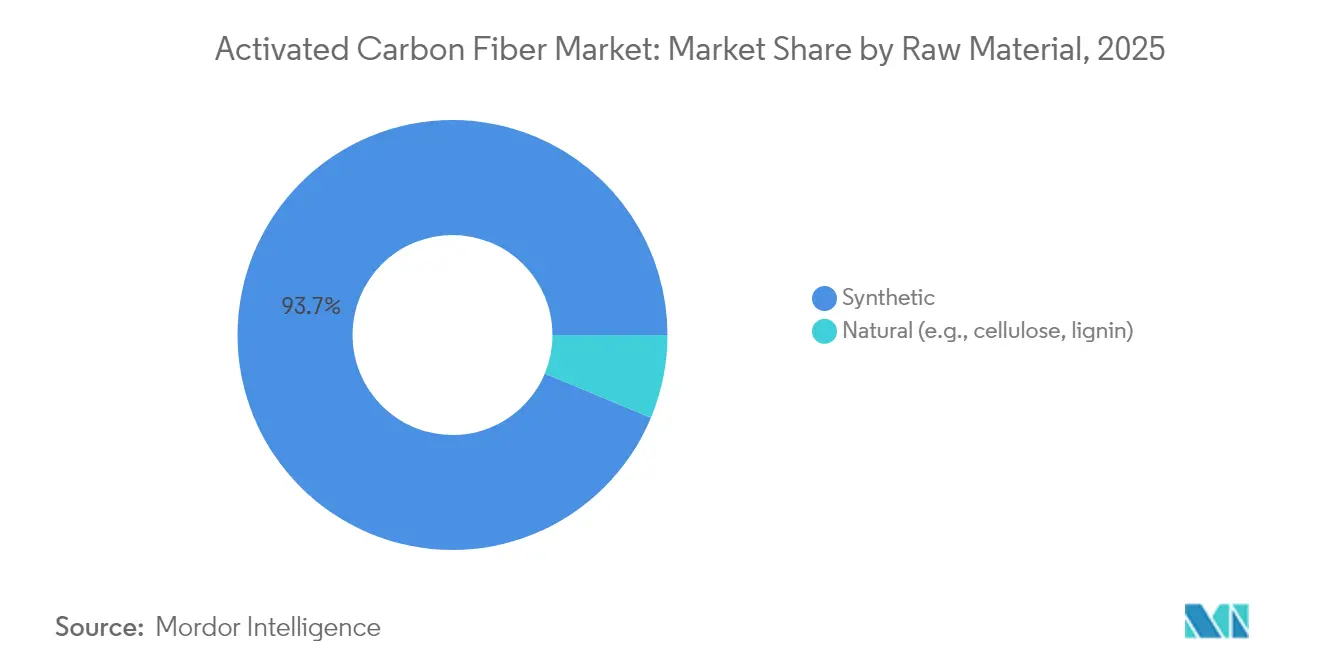

- By raw material, synthetic feedstocks held 93.72% of activated carbon fiber market share in 2025, and they are on track to grow at a 4.42% CAGR to 2031.

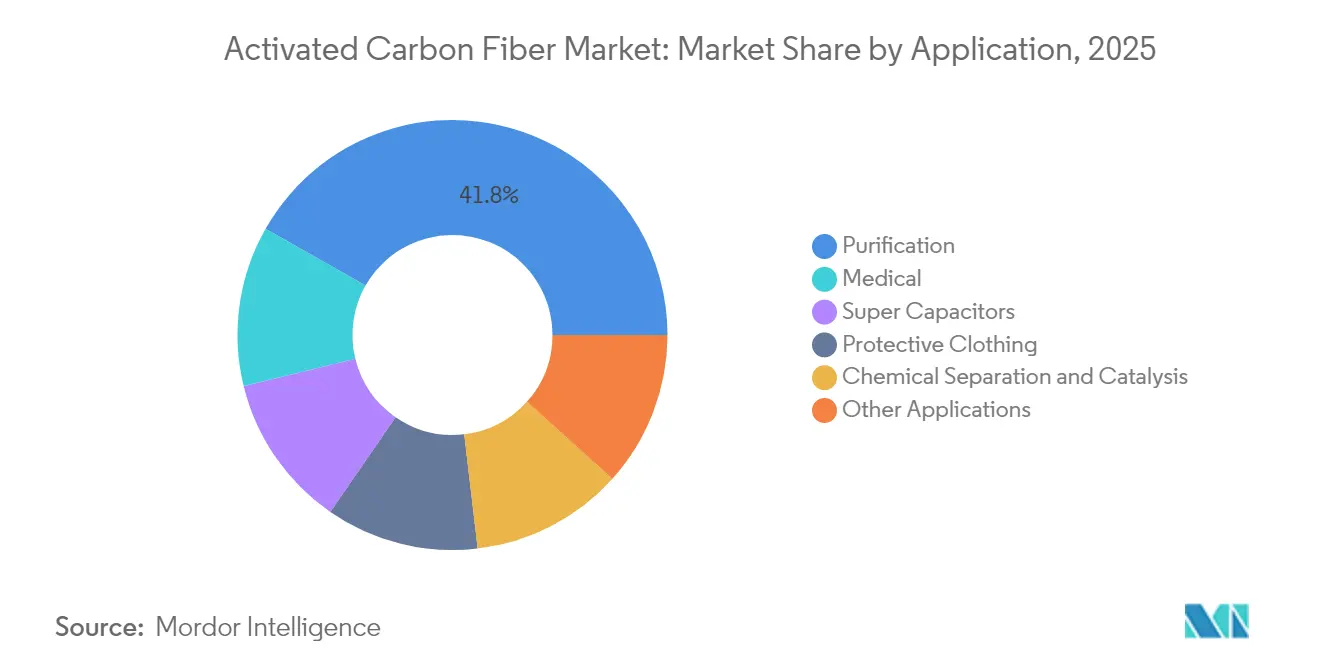

- By application, purification dominated with 41.78% of the activated carbon fiber market size in 2025, while medical uses are expanding at a 5.95% CAGR through 2031.

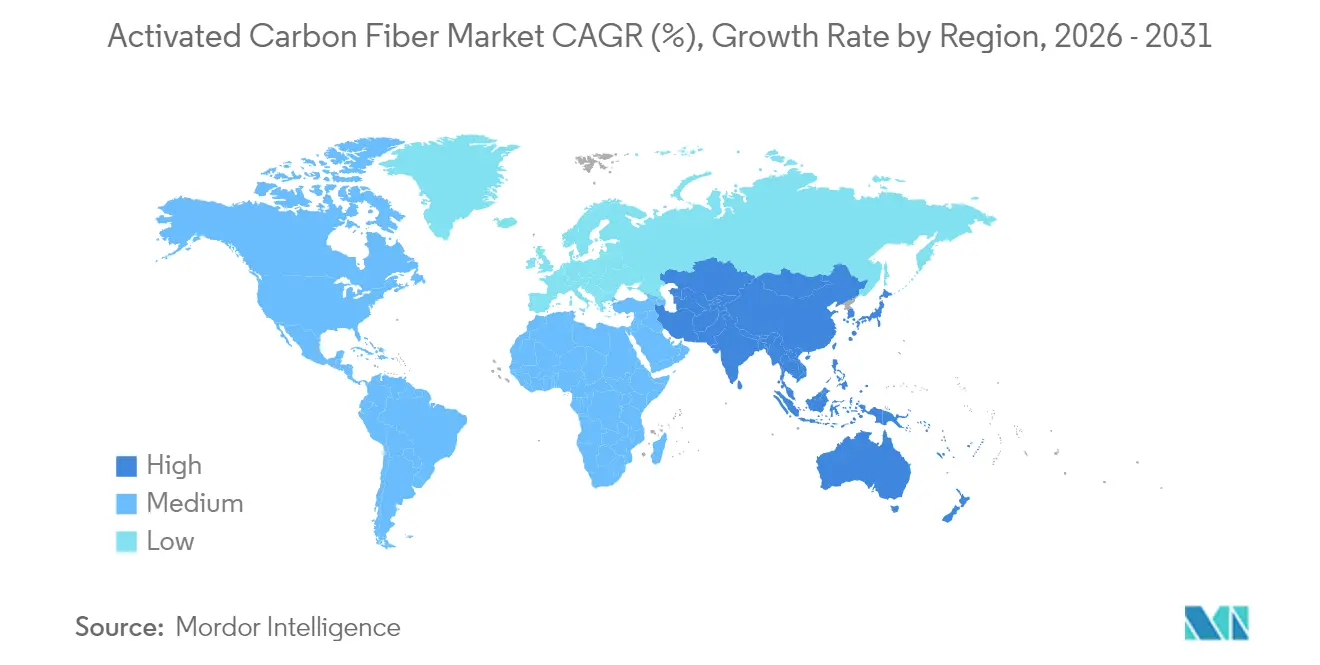

- By geography, Asia-Pacific accounted for 42.74% of activated carbon fiber market share in 2025; the same region is projected to compound at 4.96% CAGR over the outlook window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Activated Carbon Fiber Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global emission norms on VOCs | +1.2% | EU and North America lead | Medium term (2-4 years) |

| Superior adsorption-desorption kinetics | +0.8% | Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Growth in high-power supercapacitor output | +0.9% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) |

| ACF scrubbers in semiconductor fabrication | +0.6% | Asia-Pacific and North America semiconductor clusters | Short term (≤ 2 years) |

| Rise of wearable personal air-filtration | +0.4% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Emission Norms Drive Industrial Adoption

Regulators worldwide now require deeper cuts in volatile organic compound emissions, and the activated carbon fiber market benefits because the material can capture traces that escape granular carbons. The European Union’s STS BAT Conclusions, effective 2025, apply to more than 500,000 solvent-using businesses and formally list activated carbon fiber as Best Available Technology. .S. sterilization plants must now achieve a 99.99% reduction in ethylene oxide discharges under tightened National Emission Standards for Hazardous Air Pollutants. Facilities switching to fiber systems appreciate smaller bed volumes, lower pressure drop, and fewer regeneration cycles than granular beds. As enforcement timetables compress, buyers lean toward solutions that provide headroom for even stricter future rules. The result is a regulatory pull that sustains double-digit volume gains for high-spec fiber modules across regional markets.

Superior Kinetics Enable Process Intensification

Activated carbon fiber attains equilibrium adsorption in minutes, while granular media require hours, a gap that transforms process economics in continuous plants. Laboratory trials show 10- to 100-fold faster uptake thanks to accessible external surfaces that avoid internal diffusion limits. Semiconductor etch shops value this speed because rapid regeneration keeps perfluorocarbon capture online without halting production[2]Zhou Y., Li Y., Ong E., “Abatement Systems for Fluorinated Compounds,” frontiersin.org. Chemical processors retrofit smaller contactors that free up floor space and reduce auxiliary energy consumption. Faster cycles also cut steam use in desorption, lowering utility bills during volatile fuel markets. As continuous manufacturing spreads, fiber kinetics underpin a shift toward compact, modular pollution-control and separation equipment.

Semiconductor Industry Adopts Advanced Emission Control

Perfluorocarbon gases used in plasma etching present greenhouse-warming potentials thousands of times that of CO₂, forcing fabs to seek cost-effective abatement. Trials across leading 300 mm wafer lines show activated carbon fiber scrubbers capturing over 95% of key fluorinated compounds at ambient conditions, eliminating the need for energy-dense combustion units. Rapid cycling limits downtime and keeps tool utilization high, a critical economic driver in capital-intensive fabs. As the chip sector ramps in Japan, South Korea, and the United States under national subsidy programs, fiber systems gain share as they align with net-zero corporate road-maps.

Growth of Wearable Personal Air-Filtration Textiles

Consumers facing wildfire smoke, urban smog, and pandemic threats demand portable clean-air solutions. Activated carbon fiber weaves provide thin, flexible, and highly adsorptive layers compatible with fashion apparel and respirators. Research teams have developed fabrics that combine ultraviolet blocking, antibacterial performance, and 24-hour adsorption stability. Early adopters in Europe and North America purchase premium masks and jackets that incorporate multilayer fiber linings. Long-term prospects include smart garments with embedded sensors that indicate saturation, a feature impossible with traditional carbon granules. The lifestyle segment thus opens a consumer channel that adds diversification to industrial-centric demand.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upstream price swings in PAN and pitch | -0.7% | Global, acute in Asia-Pacific supply hubs | Short term (≤ 2 years) |

| Price pressure from granular and powdered carbon | -0.5% | Global, more acute in cost-sensitive deployments | Medium term (2-4 years) |

| Scarcity of continuous high-temperature lines | -0.3% | Global, limited specialist capacity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precursor Price Volatility Constrains Production Economics

Polyacrylonitrile and petroleum pitch account for up to 60% of finished fiber cost, so price spikes erode margins. The U.S. Producer Price Index for carbon and graphite products rose in May 2025, signaling broad inflation across carbon supply chains. Textile-grade PAN diverts toward mainstream fabric markets when apparel demand rebounds, squeezing availability for technical fibers. Refineries, chasing higher yields on transportation fuels, trim pitch output, and further tighten feedstock pools. Producers counter by dual-sourcing, hedging, and carrying larger safety stocks, but these strategies raise working-capital intensity. Lignin-based alternatives promise relief; however, scaling new biobased processes still faces technical hurdles.

Cost Competition Limits Market Penetration

Granular and powdered activated carbon often sells at half the unit price of fiber, limiting fiber adoption in municipal water treatment and bulk-phase odor control. Customers with relaxed performance targets lean toward lower CAPEX even if lifecycle costs rise. Emerging-economy utilities prioritize initial outlay because project finance rules favor least-cost bids. As a result, activated carbon fiber remains a premium option where kinetics, weight, or space savings justify the spend. Suppliers continue to refine pitches emphasizing smaller bed volumes, lower maintenance, and disposal advantages to convert price-sensitive buyers over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Synthetic Dominance Supports High-Spec Demand

Synthetic precursors accounted for 93.72% of the activated carbon fiber market share in 2025 and will record a 4.42% CAGR through 2031. Within this group, polyacrylonitrile fibers excel in purification, medical, and semiconductor filtration because they offer tight pore-size control and high tensile strength.

Pitch-based grades cater to energy-storage customers that require conductive matrices, while phenolic fibers serve in harsh chemical environments that demand acid resistance. Viscose derivatives, though still niche, present precise mesopore distributions that favor specialty adsorption. Natural feedstocks such as lignin and cellulose attract sustainability-minded users, yet inconsistent quality and limited commercial lines keep their combined share minor. Investment in continuous stabilization and carbonization aims to lift output and cut synthetic feedstock unit costs, reinforcing synthetic supremacy for the forecast horizon.

By Application: Medical Filters Accelerate While Purification Leads

Purification kept 41.78% of the activated carbon fiber market size in 2025, fueled by stricter air and water standards in high-population regions. Fixed-bed and rotating-drum modules anchor solvent recovery, acid gas removal, and hydrocarbon polishing across chemical, printing, and waste-processing sites.

Medical demand, though smaller, expands at a 5.95% CAGR to 2031 as hospitals embrace compact point-of-use ethylene oxide scrubbers and air-filtration panels designed for isolation rooms. Protective clothing blends ACF into multilayer suits that defend workers in cleanrooms and emergency response. Supercapacitors widen the total addressable market as automotive and grid-balancing markets favor high-power modules; suppliers that master low-resistance coating lines stand to earn premium margins. Specialty areas, including catalyst supports and odor-neutralizing consumer textiles, diversify revenue and hedge against cyclical downturns in any single segment.

Geography Analysis

Asia-Pacific captured 42.74% of the activated carbon fiber market share in 2025 and is set to post a 4.96% CAGR through 2031. China attracts capital because low-cost electric power, skilled labor, and proximity to semiconductor fabs lower delivered costs. Japanese firms such as Kuraray and Toyobo, with decades of adsorbent expertise, focus on research alliances that push fiber into carbon-neutral process routes.

North America is characterized by strict federal emissions rules converge with on-shoring of chip and battery supply chains. The EPA’s sterilization rules accelerate retrofit programs in healthcare facilities, bolstering short-cycle filter demand. Canada and Mexico contribute incremental growth as cross-border manufacturing expands. Europe delivers steady volume gains under the EU’s STS BAT Conclusions, which tighten solvent emissions across pharmaceuticals, coatings, and printing. Germany pioneers integrated solvent-recovery plants that pair fiber beds with thermal swing regeneration to improve energy efficiency. The United Kingdom and France use fiber to meet decarbonization targets in waste-to-energy and specialty chemical sites. Southern Europe, facing high electricity costs, values the lower pressure drop of fiber modules to reduce operating expenses. South America, the Middle East, and Africa remain embryonic but promising. Growth stems from refinery upgrades, mining-related air-quality mandates, and municipal drinking-water projects seeking high-flow-rate adsorbents. However, price sensitivity and limited local manufacturing constrain near-term penetration, keeping regional shares in the single digits.

Competitive Landscape

The activated carbon fiber market remains moderately fragmented because process know-how rather than scale defines entry barriers. Leading players integrate upstream to secure PAN and pitch in an environment of volatile petrochemical costs. Kuraray, Toyobo, and Osaka Gas Chemical use proprietary activation recipes that tailor pore-size distributions for VOC, dioxin, and greenhouse-gas targets. Chinese producers leverage low-cost utilities yet invest in certification and quality systems to meet export standards. Supply chains adapt to address resilience concerns. North American buyers lock multi-year off-take pacts to hedge against Asia-Pacific shipping disruption. European firms diversify precursor contracts to reduce exposure to single refineries. Vendors differentiate by offering application engineering services, real-time performance monitoring, and refurbishment programs that extend fiber life cycles.

Activated Carbon Fiber Industry Leaders

HPMS Graphite

Kuraray Co. Ltd

Osaka Gas Co. Ltd (Daigas Group)

TOYOBO CO. LTD

UNITIKA LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Researchers reported activated carbon fiber felts with 1,331 mg/g methyl iodide uptake, setting new radio-iodine capture benchmarks.

- January 2023: Toyobo enhanced K-FILTER nitrogen-desorption VOC recovery units that use activated carbon fiber elements and received an environmental technology award from the Kinki Chemical Society.

Global Activated Carbon Fiber Market Report Scope

Activated carbon fiber is commonly produced from carbon fiber by the pyrolysis of carbonaceous materials, such as polyacrylonitrile (PAN), coal tar pitch and petrol pitch, rayon, and biomass, among others. It has applications in purification, chemical separation, catalysis, protective clothing, medical, and supercapacitors, among others. The Activated Carbon Fiber Market is segmented by Raw Material (Natural and Synthetic), Application (Purification, Chemical Separation and Catalysis, Protective Clothing, Medical, Super Capacitors, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East & Africa). The report also covers the market size and forecasts for the activated carbon fiber market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Natural (e.g., cellulose, lignin) | |

| Synthetic | Pitch-based |

| PAN-based | |

| Phenolic-based | |

| Viscose-based | |

| Others |

| Purification |

| Chemical Separation and Catalysis |

| Protective Clothing |

| Medical |

| Super Capacitors |

| Other Applications |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material | Natural (e.g., cellulose, lignin) | |

| Synthetic | Pitch-based | |

| PAN-based | ||

| Phenolic-based | ||

| Viscose-based | ||

| Others | ||

| By Application | Purification | |

| Chemical Separation and Catalysis | ||

| Protective Clothing | ||

| Medical | ||

| Super Capacitors | ||

| Other Applications | ||

| Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the activated carbon fiber market?

The activated carbon fiber market size stood at USD 452.75 million in 2026 and is tracking toward USD 561.57 million by 2031.

Which raw material dominates commercial production?

Synthetic precursors, mainly polyacrylonitrile and pitch, supply 93.72% of global volume due to their consistent pore architecture and mechanical strength.

Why are medical applications growing faster than other uses?

Hospitals and PPE makers favor fiber filters to meet strict indoor air targets and sterilant emission rules, supporting a 5.95% CAGR through 2031.

Which region leads demand and why?

Asia-Pacific commands 42.74% share because it combines low-cost manufacturing with proximity to semiconductor and electronics hubs that require high-spec emission controls.

How do granular and powdered carbons compete with fiber?

Granular and powdered carbons are cheaper, so they dominate bulk treatment where contact times are long, but fiber wins in tight-footprint or high-throughput processes that demand rapid kinetics.

What technology trend could reshape future supply?

Commercialization of lignin-based precursor lines promises lower cost and reduced carbon footprints, potentially shifting feedstock economics later in the decade.

Page last updated on: