Activated Alumina Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

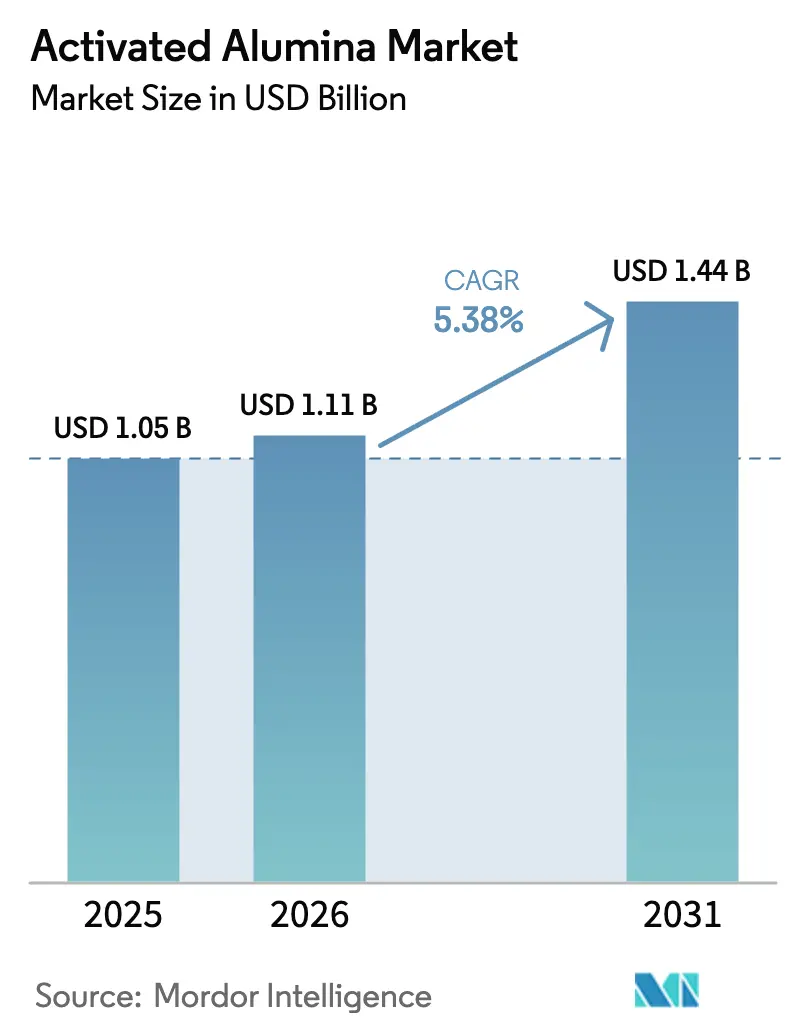

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.44 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Activated Alumina Market Analysis by Mordor Intelligence

The Activated Alumina Market size was valued at USD 1.05 billion in 2025 and estimated to grow from USD 1.11 billion in 2026 to reach USD 1.44 billion by 2031, at a CAGR of 5.38% during the forecast period (2026-2031). The activated alumina market is benefiting from tightening global water-quality rules, expanding dehydration projects in energy infrastructure, and the adsorbent’s proven ability to regenerate without large capital outlays. Desiccant demand in natural-gas processing, rising use as a fluoride-removal medium, and emerging roles in lithium-ion battery separators collectively underpin steady volume growth across both mature and nascent applications. Competitive intensity remains moderate because proprietary forming and calcination techniques allow incumbents to command attractive margins even as substitute adsorbents gain attention. Supply-side risks centered on alumina feedstock price swings are beginning to ease as new refining capacity returns, yet circular-economy programs and low-temperature regeneration technologies are opening additional revenue streams that help stabilize the activated alumina market.

Key Report Takeaways

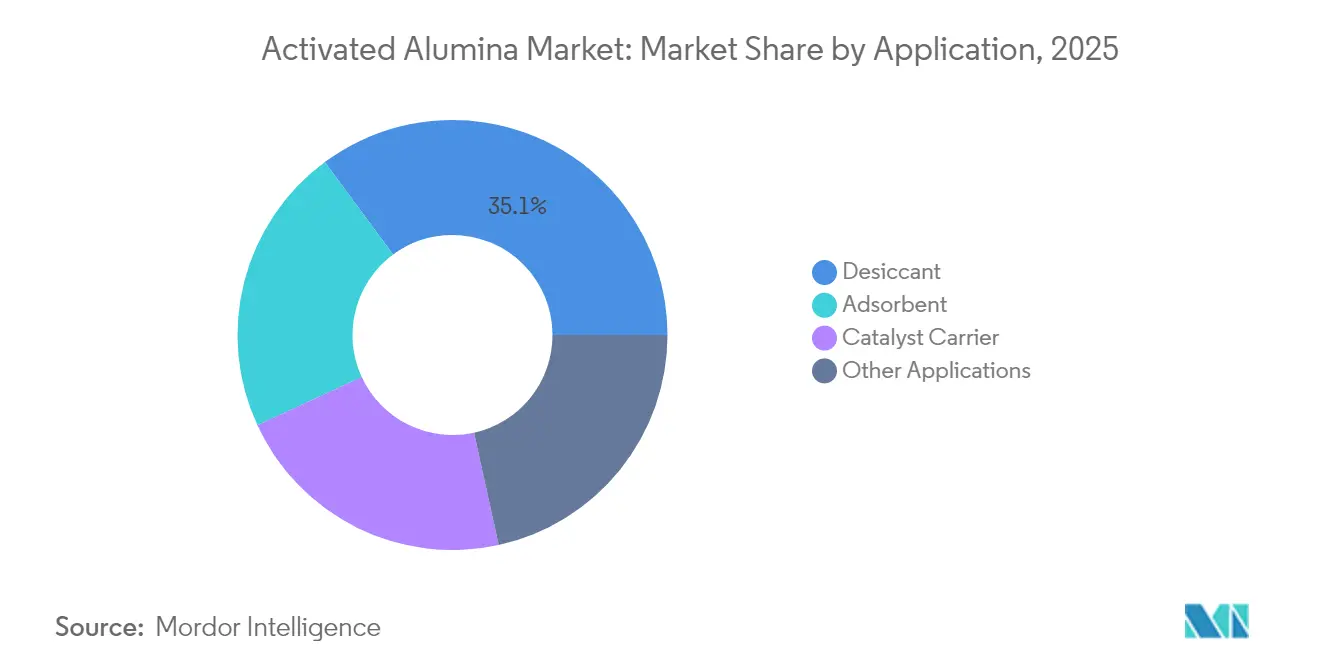

- By application, desiccant applications led with 35.12% of the activated alumina market share in 2025; adsorbent applications are projected to advance at a 5.93% CAGR through 2031.

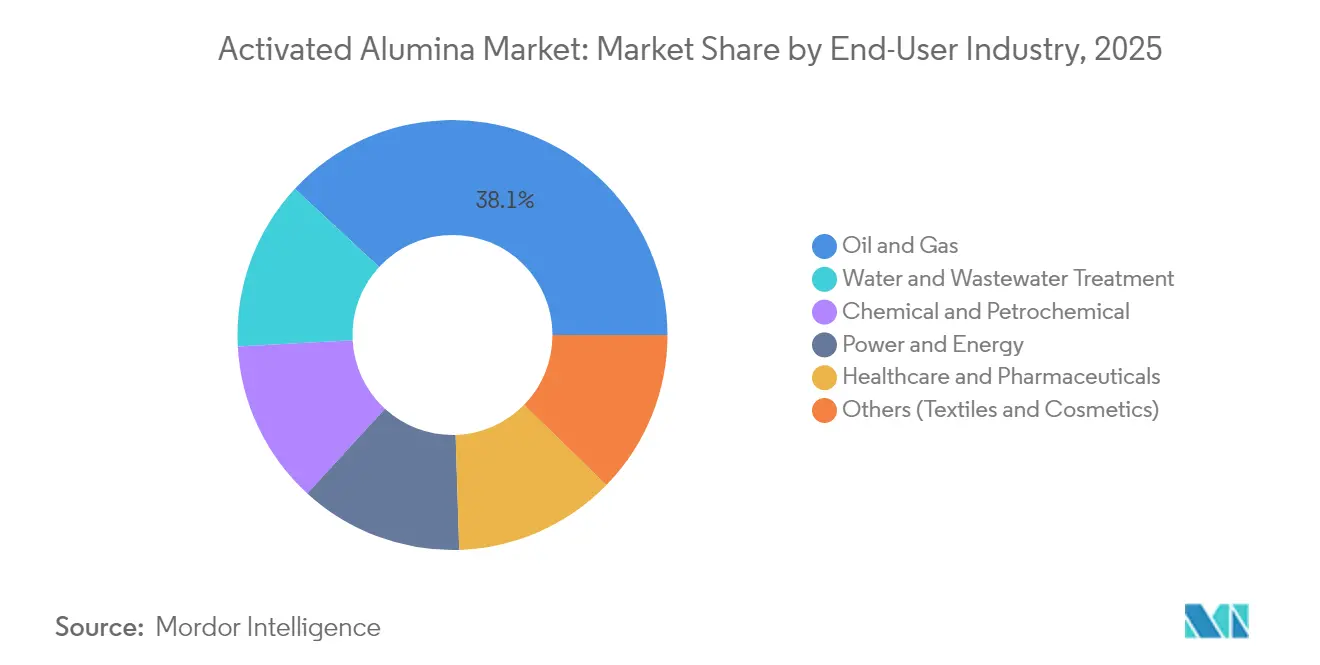

- By end-user industry, oil and gas end users commanded 38.10% share of the activated alumina market size in 2025; while water and wastewater treatment end users are set to expand at a 6.25% CAGR between 2026 and 2031.

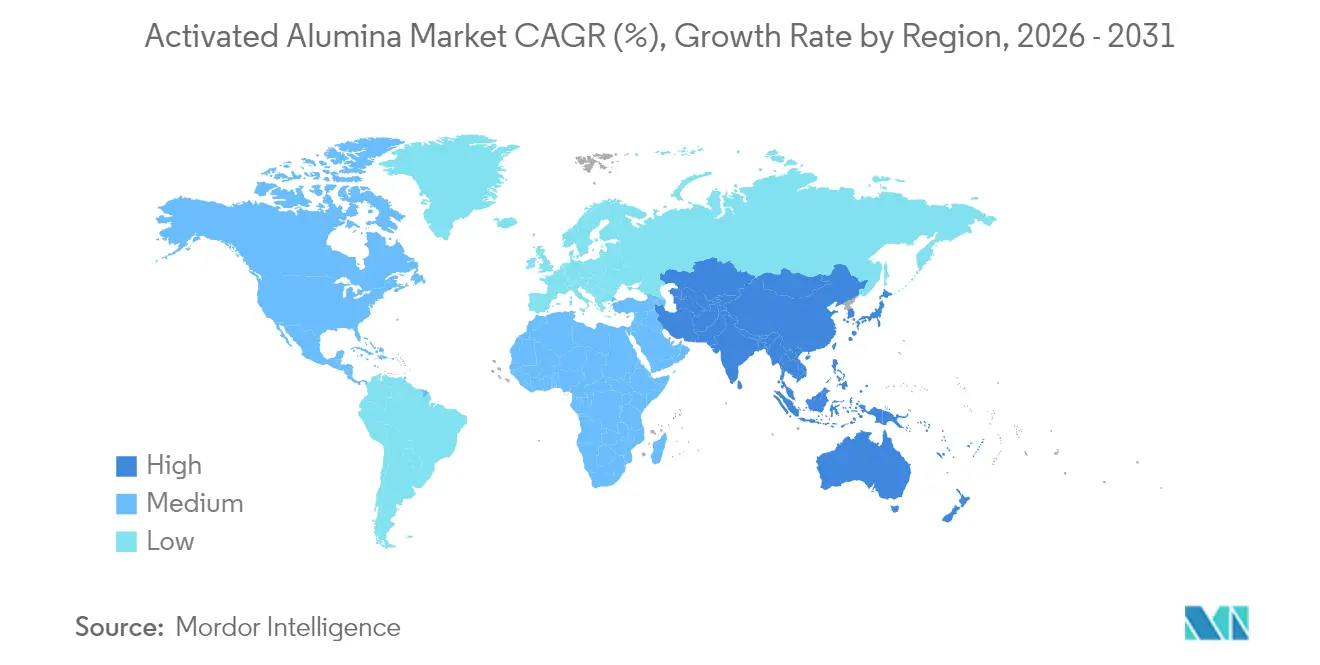

- By region, Asia Pacific captured 53.78% of the activated alumina market share in 2025 and is forecast to post a 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Activated Alumina Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for fluoride-removal media in municipal water treatment | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Expansion of natural-gas and oil-refining dehydration projects | +0.8% | APAC core, spill-over to Middle East | Long term (≥ 4 years) |

| Rising pharmaceutical catalyst and adsorbent usage | +0.6% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Integration of activated-alumina layers in Li-ion battery separators | +0.4% | APAC manufacturing hubs, global adoption | Long term (≥ 4 years) |

| Circular-economy push for regenerable adsorbents | +0.3% | Global, led by EU regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Fluoride-Removal Media in Municipal Water Treatment

Regulators finalized the United States PFAS National Primary Drinking Water Regulation in April 2024, establishing maximum contaminant levels that must be met by April 2029, which has catalyzed a broader upgrade cycle for municipal treatment plants[1]United States Environmental Protection Agency, “National Primary Drinking Water Regulation for PFAS,” epa.gov. Activated alumina outperforms single-purpose media because its amphoteric surface removes both fluoride and trace heavy metals with equal efficiency. Comparative studies demonstrate seven-fold higher fluoride adsorption on micro-crystalline alumina versus traditional silica sand, while regeneration at 150 °C preserves more than 90 % capacity over multiple cycles. Utility operators gravitate toward this proven chemistry during compressed compliance windows, pushing bulk-order volumes higher between 2025 and 2029. Vendors already positioned with turnkey feed, regenerate, and instrumentation support have begun locking in framework contracts with large water districts, reinforcing visibility in the activated alumina market. Ongoing public-health funding programs in Europe and Canada provide additional upside as those regions harmonize limits on emerging contaminants.

Expansion of Natural-Gas and Oil-Refining Dehydration Projects

Moisture management remains critical for meeting ultra-low-sulfur fuel and feedstock standards, and major licensors now specify multi-bed dehydration trains that integrate activated alumina guard layers for polar contaminant removal. Axens reports that its AxSorb series achieves outlet water levels below 0.1 ppm while simultaneously scavenging light mercaptans, a dual function that reduces vessel count and capital burden. New ethane crackers and hydrogen-ready steam-methane reformers under construction in Southeast Asia select alumina-based desiccant beds because the media regenerates on-site and accommodates swing-mode operation. As distributed LNG and CNG networks proliferate across India and China, smaller skid packages require higher adsorbent volumes per throughput unit, which further lifts the activated alumina market. The long equipment life cycle and limited performance degradation over successive regenerations sustain a predictable replacement rhythm through 2030.

Rising Pharmaceutical Catalyst and Adsorbent Usage

Regulatory emphasis on continuous manufacturing drives adoption of fixed-bed reactors packed with precious-metal catalysts supported on activated alumina. The material’s high crush strength and customizable pore structure stabilize particle dispersion, leading to double-digit yield improvements in hydrogenation and dehydration steps documented by multiple peer-reviewed studies. Facilities governed by quality-by-design protocols favor a predictable support that withstands sterilization without leaching. North American manufacturers are therefore extending supply agreements with alumina specialists to secure validated batches through 2028, which stabilizes demand in an otherwise cyclic end market. Concurrently, emerging APAC contract development organizations invest in in-house catalyst regeneration units, broadening regional pull for high-surface-area alumina grades.

Integration of Activated-Alumina Layers in Li-ion Battery Separators

Research from the Royal Society of Chemistry confirms that embedding sub-micron activated-alumina particles within polyolefin separators doubles thermal stability and inhibits lithium dendrite propagation[2]Royal Society of Chemistry, “Composite Alumina-Based Separators for Next-Gen Batteries,” rsc.org . These benefits align with the electric-vehicle sector’s move toward higher-nickel cathodes, which operate nearer to safety limits. Battery-cell makers in China, Japan, and South Korea have begun pilot-line trials that incorporate thin alumina-coated separators, potentially introducing a multi-kiloton annual demand increment from 2027 onward. Unlike passive adsorption, this use case relies on ionic conductivity enhancement and therefore commands a higher price per kilogram, offering margin expansion opportunities inside the activated alumina market. Intellectual-property barriers remain low, so traditional adsorbent suppliers with calcination expertise can pivot quickly if they achieve coating uniformity at gigafactory scale.

Restraints Impact Analysis of Activated Alumina Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of substitute adsorbents | -0.7% | Global, particularly in cost-sensitive applications | Short term (≤ 2 years) |

| Alumina feedstock price volatility | -0.5% | Global supply chain impact | Short term (≤ 2 years) |

| Emerging regulations on spent-alumina disposal and recycling | -0.4% | North America & EU, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Substitute Adsorbents

Iron-oxide nanoparticles provide 70–98 % removal efficiency for several heavy metals and permit magnetic separation, delivering operational advantages in continuous-flow systems where activated alumina requires thermal regeneration. Bio-based carbon adsorbents produced from agricultural waste also show growing appeal because their mesopore distribution favors microplastic capture. Rapid scale-up in Southeast Asia and Latin America, where cost sensitivity is acute, means local utilities may trial these alternatives before considering premium alumina grades. Suppliers inside the activated alumina market therefore reposition on versatility and total-cost-of-ownership messaging rather than absolute performance. The restraint’s near-term impact is cushioned by regulatory familiarity with alumina media, yet procurement shifts in municipal bids demonstrate that price plays an outsized role when financing constraints dominate.

Alumina Feedstock Price Volatility

Benchmark smelter-grade alumina prices have exhibited double-digit swings over the past two years, driven by refinery shutdowns, energy-price spikes, and logistical bottlenecks. Although new refining lines in Indonesia and the Middle East promise extra tonnage from 2025, uncertainty lingers because commissioning delays historically exceeded twelve months for comparable assets. Activated-alumina producers without vertical integration face margin compression unless they lock in cost-pass-through clauses or broaden low-temperature synthesis routes that reduce energy inputs. Efforts such as spray-pyrolysis processing, which achieves 99 % conversion at substantially lower furnace temperatures, remain at pilot scale but signal cost-containment paths for the medium term. Until these approaches commercialize, feedstock volatility weighs on capital-expansion decisions and tempers aggressive price-cutting tactics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Activated Alumina Market Segment Analysis

By Application:

Desiccant Dominance Drives Industrial ExpansionDesiccant uses represented 35.12% of the activated alumina market size in 2025, reflecting the medium’s status as the processing standard for bulk gas dehydration. Continuous swing-bed units regenerate alumina at 200 °C, preserving over 95 % capacity after 1,000 cycles, an economic edge that fortifies long-term contracts in LNG, CNG, and refinery operations. Incremental volume now comes from hydrogen-ready gas turbines that demand stringent dew-point control, ensuring the segment sustains a low-to-mid single-digit growth rate across the forecast period. Competitive differentiation centers on tailored pore-size distribution rather than bulk density, prompting leading suppliers to invest in advanced sol-gel routes that suppress attrition.

Adsorbent applications are on track for the fastest 5.93% CAGR through 2031 as municipalities and industrial users retrofit systems to comply with emerging contaminant thresholds. Activated alumina’s regenerability keeps lifetime operating costs lower than single-use ion-exchange resins, while its amphoteric surface allows simultaneous capture of fluoride, arsenic, and selenium. Pilot installations in the Midwest United States show 85 % lower sludge disposal volumes compared with metal-salt coagulants, a sustainability advantage that policymakers view favorably. Early-stage adoption inside lithium-ion battery separator coatings adds further upside because even a 5 % penetration would equate to thousands of tons annually. Together, these dynamics ensure the activated alumina market maintains a balanced revenue mix that buffers cyclic swings in any one end use.

By End-User Industry:

Oil & Gas Leadership Meets Water-Treatment AccelerationOil and gas operators accounted for 38.10% of the activated alumina market share in 2025, underpinned by pervasive use in dehydration and sulfur-removal trains. Stricter specifications for low-carbon fuels reinforce medium-term resilience, particularly as refineries transition toward renewable diesel and blue hydrogen that still involve moisture-sensitive steps. Catalyst-carrier demand from petrochemical complexes also channels significant tonnage because alumina’s structural stability enables high noble-metal loading at elevated temperatures.

Water and wastewater treatment exhibits the highest 6.25% CAGR heading to 2031, propelled by PFAS and fluoride directives that require multicomponent adsorption solutions. Municipalities have earmarked multi-year budgets for media replacement, accelerating tender activity in both North America and the EU. Pharmaceutical manufacturers and semiconductor fabs contribute additional orders as they replace single-pass granular activated carbon with regenerable mixed-bed systems. Across all sectors, supplier selection gravitates toward firms that offer spent-media take-back programs, an emerging differentiator in the activated alumina market.

Geography Analysis

APAC Activated Alumina Market

Asia Pacific held 53.78% of the activated alumina market share in 2025 and will likely retain pole position as CAGR reaches 6.31% through 2031. High-value projects in China’s coastal chemical parks and Southeast Asian cracker complexes require large desiccant volumes, while gigafactory build-outs across the region test alumina-coated separator films for the next generation of EV batteries. Local sourcing advantages, including proximity to bauxite deposits and integrated alumina refineries, support competitive delivered costs, ensuring that regional producers strengthen export positions to the Middle East and Africa.

North America Activated Alumina Market

North America follows with entrenched demand from natural-gas midstream assets and federally driven water-quality mandates. The PFAS rule finalized in 2024 schedules compliance by 2029, triggering a predictable spending cycle on high-capacity fluoride adsorbent beds. Advanced pilot programs in the Great Lakes region already demonstrate scalable regeneration that curbs lifecycle media consumption by up to 30%, reinforcing alumina’s cost proposition. However, planned silica-plant closures by Evonik in New York and Maryland between 2025 and 2026 point to intensified rationalization among specialty-chemical suppliers, which may tighten near-term domestic availability.

EMEA and South America Activated Alumina Market

Europe remains committed to circular-economy targets that favor regenerable adsorbents. Policy instruments such as the Industrial Emissions Directive incentivize operators to quantify life-cycle impact, which tilts procurement toward alumina over single-use resins. Investment in green alumina synthesis technologies, including low-temperature spray-pyrolysis units in Germany, signals a drive to decarbonize even specialty-chemical production. South America and the Middle East & Africa collectively add incremental volume as new gas-processing facilities and water-scarcity relief projects come online. Although their combined tonnage is modest, higher replacement rates in hard-water conditions create recurring demand that lifts the activated alumina market in these regions over time.

Mordor Intelligence provides coverage of the activated alumina market across other key regional markets, including Asia, North America, and Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The activated alumina market features moderate concentration: the top five producers control roughly 65% of global capacity, leaving room for regional challengers. BASF, Honeywell UOP, Evonik, and W. R. Grace compete mainly on proprietary forming and calcination techniques that yield differentiated pore architectures. BASF’s oil-drop Sorbead process delivers superior hydrothermal stability, enabling over 40 % longer service intervals for refinery dryers. Honeywell integrates digital twins to optimize cycle timing, cutting energy use during adsorption–regeneration swings.

Strategic asset optimization continued in 2025 when Evonik announced the phased closure of its Waterford and Havre de Grace silica plants to consolidate output at higher-efficiency hubs, freeing capital to expand specialty alumina grades for water treatment and battery separators. Meanwhile, Chinese producers leverage cost-competitive feedstock and short supply chains to supply both domestic and export markets, narrowing delivered-price gaps in Southeast Asia. Technology partnerships between Western licensors and Asian toll manufacturers are emerging to ensure quality consistency, indicating a hybrid model rather than outright commoditization.

Innovation remains a key defense as substitute adsorbents gain visibility. The Korea Institute of Energy Research demonstrated a low-temperature regeneration method that halves energy consumption for alumina-based beds, offering customers clear operational savings once commercialized. Suppliers also invest in life-cycle management services by bundling spent-media recycling and performance monitoring software. These value-added packages raise switching costs, shoring up margins within the activated alumina market even when spot prices for raw alumina fluctuate.

Activated Alumina Industry Leaders

Axens

Huber Engineered Materials

Evonik Industries AG

Honeywell International

BASF

- *Disclaimer: Major Players sorted in no particular order

Activated Alumina Market Companies Covered in this Report

- AGC Chemicals

- Arkema

- Axens

- BASF

- Clariant

- Dynamic Adsorbents Inc.

- Evonik Industries AG

- Hindalco Industries Ltd.

- Honeywell International

- Huber Engineered Materials

- Jiangsu Jingjing New Material

- KIN Filter Engineering

- Petrosadid

- Porocel (Evonik)

- Sorbead India

- Sumitomo Chemical Co. Ltd.

- W. R. Grace and Co.

- Zeochem AG

Recent Industry Developments in Activated Alumina Market

- June 2025: Hindalco Industries, part of the Aditya Birla Group, has made a major move by acquiring AluChem Companies Inc., a US-based specialty alumina manufacturer. The deal, which encompasses activated alumina, is set to strengthen Hindalco's foothold in the market.

- February 2023: Evonik announced the investment in the expansion of its fumed aluminum oxide production plant in Yokkaichi, Japan. The facility will be the company's first alumina plant in Asia. It will focus on making solutions for lithium-ion battery technology, which is used in electric car batteries. The plant is expected to be operational by 2025.

Global Activated Alumina Market Report Scope

Activated alumina is a highly porous aluminum hydroxide with a large surface area. It is used in a wide range of applications, such as catalysts, bioceramics, fluoride adsorbents, and others. It can absorb toxic materials from wastewater and aquifers. Application, end-user industry, and geography are the market segments for activated alumina. By application, the market is segmented into catalyst, desiccant, adsorbent, and other applications. By end-user industry, the market is segmented into oil and gas, water treatment, chemicals, healthcare, and other end-user industries. The report also covers the market size and forecasts in 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of revenue (USD million).

Segmentation Overview

| Adsorbent |

| Desiccant |

| Catalyst Carrier |

| Other Applications |

| Oil and Gas |

| Water and Wastewater Treatment |

| Chemical and Petrochemical |

| Healthcare and Pharmaceuticals |

| Power and Energy |

| Others (Textiles and Cosmetics) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Adsorbent | |

| Desiccant | ||

| Catalyst Carrier | ||

| Other Applications | ||

| By End-User Industry | Oil and Gas | |

| Water and Wastewater Treatment | ||

| Chemical and Petrochemical | ||

| Healthcare and Pharmaceuticals | ||

| Power and Energy | ||

| Others (Textiles and Cosmetics) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Activated Alumina Market size?

The activated alumina market size is USD 1.11 billion in 2026 and is projected to reach USD 1.44 billion by 2031.

Which application segment dominates the activated alumina market?

Desiccant applications dominate, accounting for 35.12% of global revenue in 2025.

Why is Asia Pacific leading the activated alumina market?

Asia Pacific benefits from integrated alumina refining, rapid industrialization, and strong demand in natural-gas dehydration and municipal water treatment, giving it a 53.78% share in 2025.

What growth rate is expected for water-treatment end users?

Water and wastewater treatment end users are forecast to register a 6.25% CAGR through 2031, making them the fastest-growing customer group.

Page last updated on: