Acrylic Fiber Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

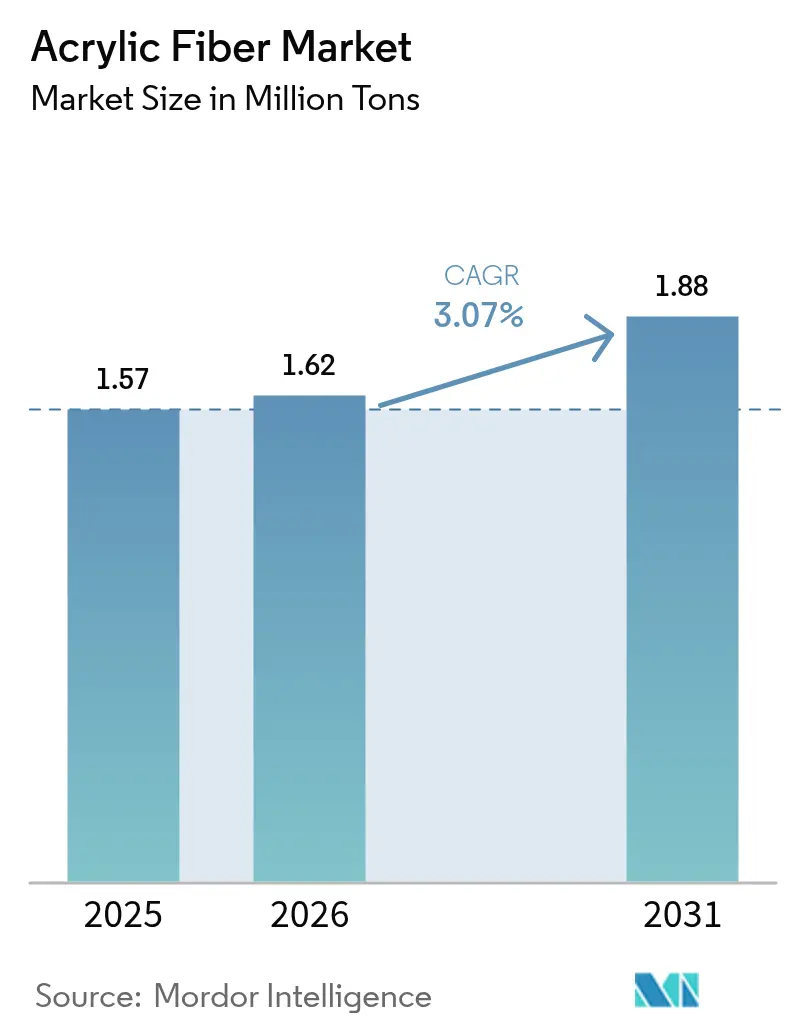

| Market Volume (2026) | 1.62 Million tons |

| Market Volume (2031) | 1.88 Million tons |

| Growth Rate (2026 - 2031) | 3.07% CAGR |

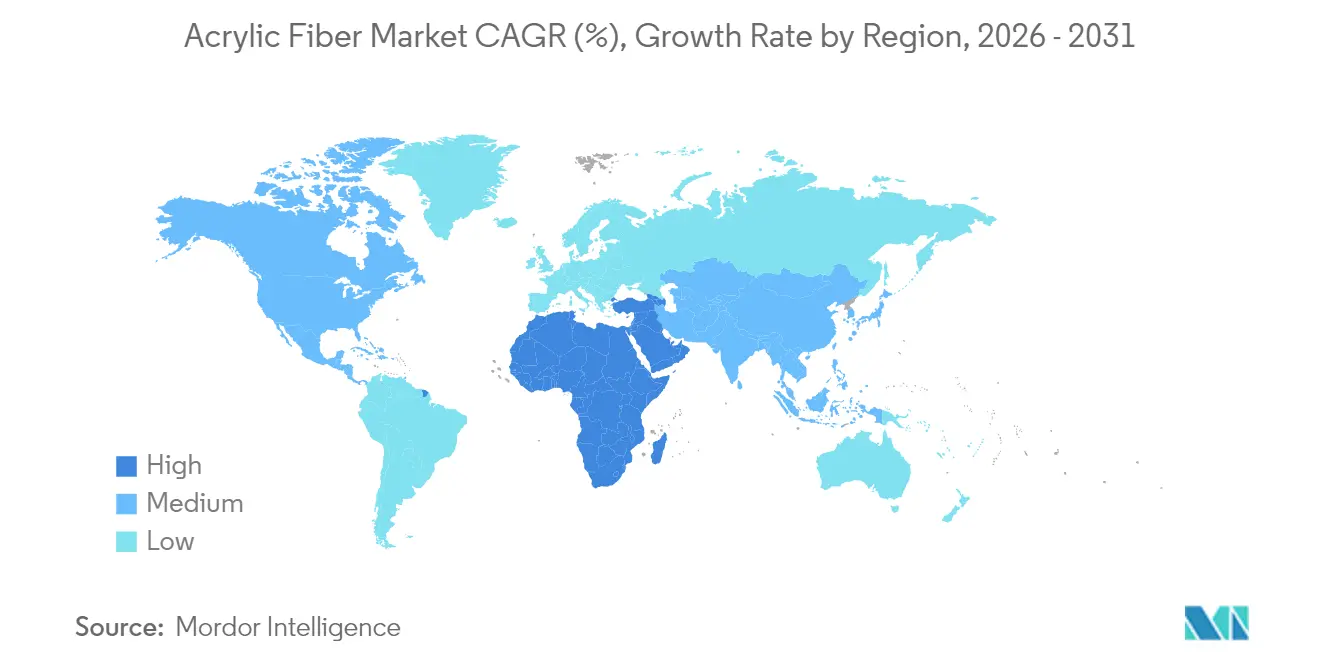

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acrylic Fiber Market Analysis by Mordor Intelligence

The Acrylic Fiber Market size was valued at 1.57 Million tons in 2025 and estimated to grow from 1.62 Million tons in 2026 to reach 1.88 Million tons by 2031, at a CAGR of 3.07% during the forecast period (2026-2031). Compliance costs tied to Extended Producer Responsibility (EPR) mandates, volatile acrylonitrile (ACN) pricing, and feedstock diversification efforts are reshaping cost structures and accelerating sustainability-linked innovation. Asia-Pacific continues to anchor global demand, while Middle East and Africa shows healthy catch-up growth as regional producers leverage local petrochemical resources. Staple fiber remains the dominant form, thanks to its versatility across apparel, home textiles, and emerging technical applications. Moderate but rising recycling premiums, coupled with propane-based ACN synthesis breakthroughs, create new opportunities for agile suppliers responding to the evolving competitive landscape.

Key Report Takeaways

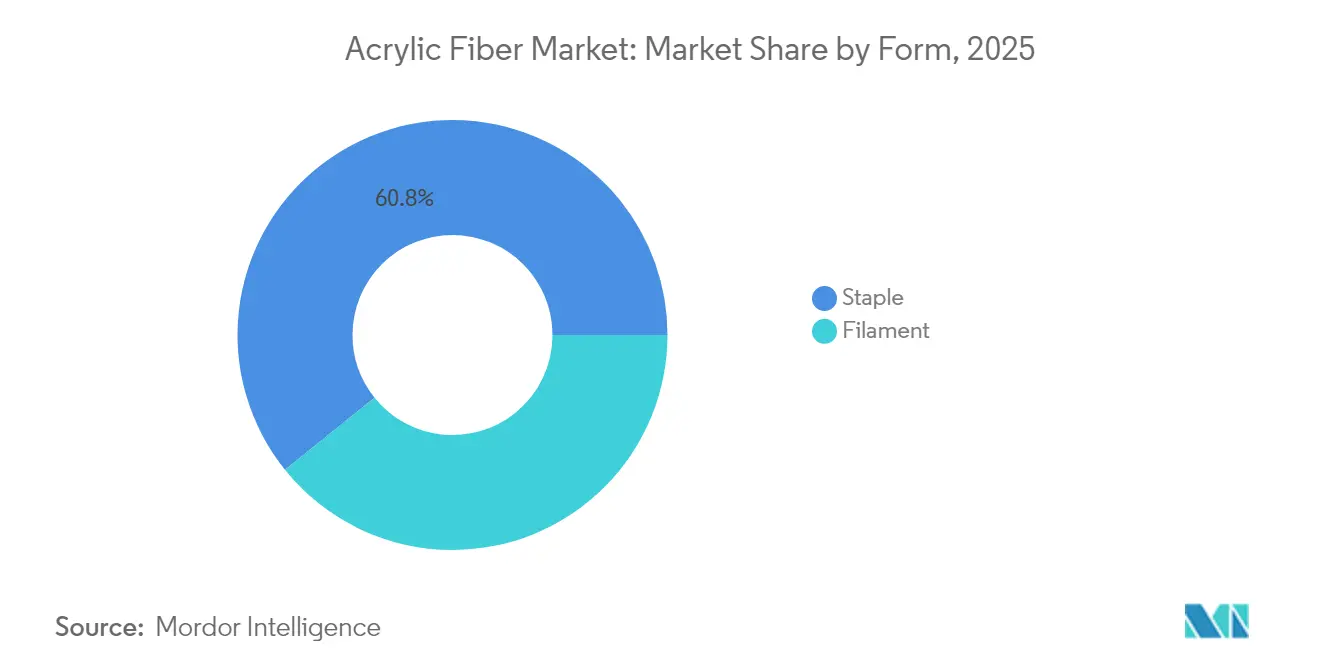

- By form, staple fiber accounted for 60.78% acrylic fiber market share in 2025 and is advancing at a 3.71% CAGR through 2031.

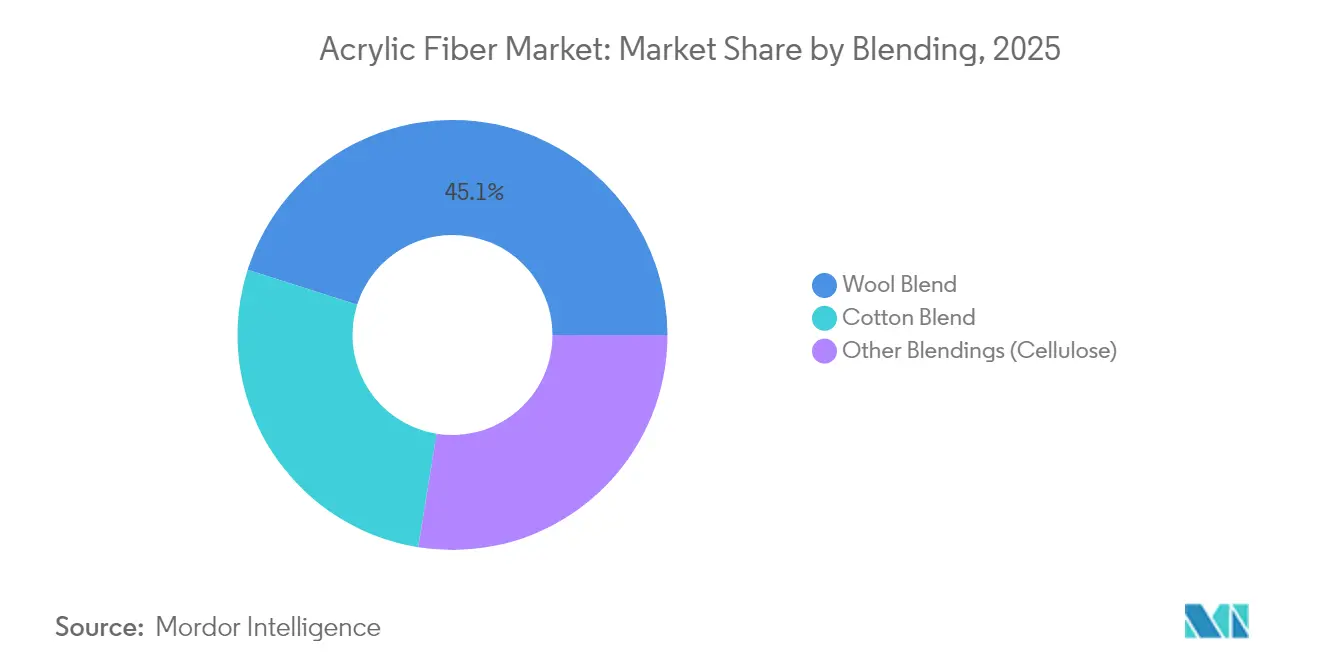

- By blending, wool blends commanded 45.10% of the acrylic fiber market size in 2025, while other blends are forecast to grow at 3.41% CAGR through 2031.

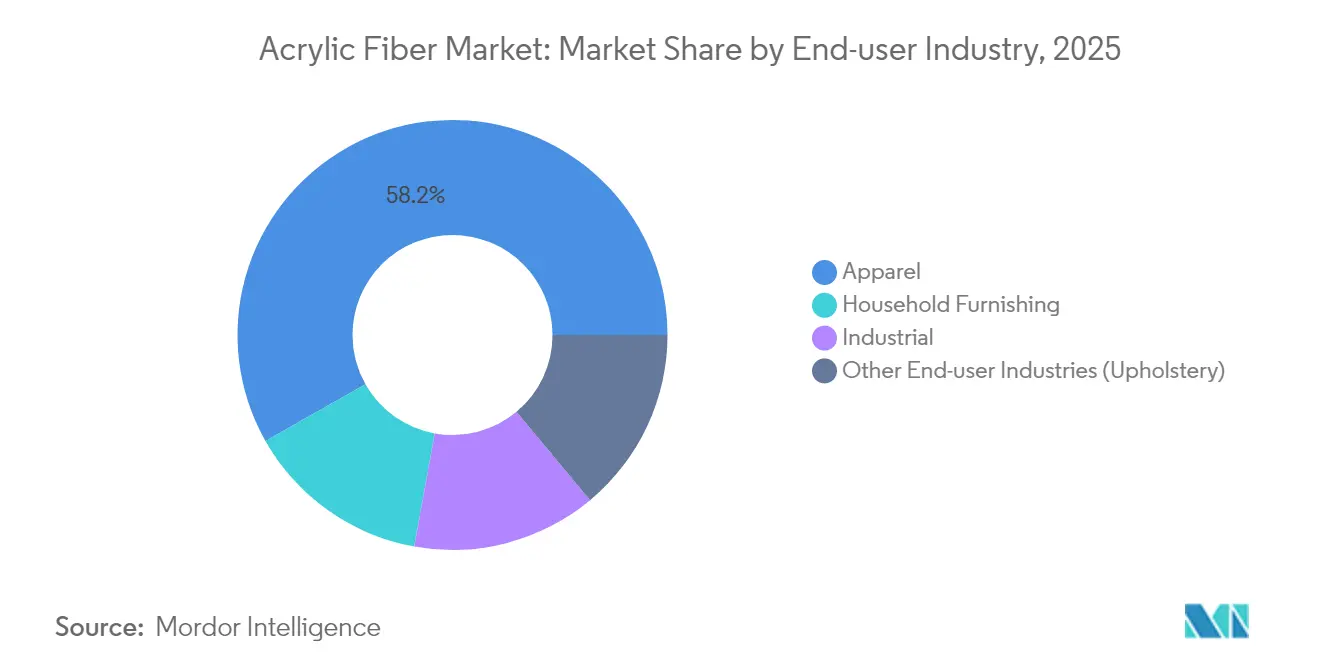

- By end-user industry, apparel led with 58.20% of 2025 volume; while other end-user industries are projected to expand at a 3.86% CAGR to 2031.

- By geography, Asia-Pacific held 68.10% share of the acrylic fiber market in 2025, whereas Middle East and Africa is on track for a 3.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acrylic Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Demand for Wool-Like Properties in Apparel | +0.8% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growth in Home-Furnishing and Carpeting Demand | +0.6% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing Industrial and Filtration Applications | +0.5% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| High-Bulk Acrylic Innovations for Lightweight Insulation | +0.4% | North America and Europe, cold-climate regions | Long term (≥ 4 years) |

| Surge in Recycled Acrylic Fiber Under Global EPR Mandates | +0.9% | EU, California, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Demand for Wool-Like Properties in Apparel

Fashion brands favor acrylic’s ability to mimic wool’s crimp, warmth, and softness while offering improved colorfastness and easy care. Bicomponent spinning now enables cashmere-like deniers that appeal to the premium casual category. Asian producers capitalize on integrated supply chains to supply finer denier yarns efficiently. In parallel, animal-welfare concerns reinforce demand for synthetic alternatives that meet the tactile expectations of knitwear consumers. The resulting pull effect underpins stable apparel volume even as competing synthetics proliferate.

Growth in Home-Furnishing and Carpeting Demand

Commercial construction rebounds and higher renovation rates sustain acrylic demand in upholstery, drapery, and contract carpeting. Built-in flame retardancy and UV stability suit hospitality and healthcare interiors that require stringent safety compliance. Solution-dyed acrylic’s vivid colorfastness commands premium decorative applications, although cost-efficient polyester continues to erode share in residential broadloom. Building codes favor inherently flame-retardant fibers, supporting acrylic adoption in public spaces where natural fibers fall short.

Increasing Industrial and Filtration Applications

Stricter air-quality rules elevate technical textile demand for acid-resistant filter media. Acrylic’s thermal stability makes it suitable for baghouse systems operating under corrosive conditions. Nanoparticle-enhanced fibers further improve adsorption of SO₂ and NOₓ, positioning the material for next-generation emission-control fabrics. Certification frameworks such as ISO 14001 accelerate adoption by heavy industry emitters aiming for compliance and ESG targets[1]ISO, “ISO 14001 Environmental Management,” iso.org .

High-Bulk Acrylic Innovations for Lightweight Insulation

Hollow-fiber and air-textured processes yield low-density fabrics that retain warmth without weight penalties. Cold-climate apparel, sleeping bags, and architectural textiles benefit from these advances. Energy-efficiency regulations in building envelopes encourage lightweight composites that use less material yet meet thermal codes, widening the addressable technical-textile space for acrylic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Cost-Efficient Polyester and Blends | -0.7% | Global, particularly in residential carpet markets | Medium term (2-4 years) |

| Stringent Environmental Rules on ACN Emissions | -0.4% | EU, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Acrylonitrile Price Volatility Tied to Propylene Supply | -0.6% | Global, with highest impact in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Cost-Efficient Polyester and Blends

Solution-dyed PET carpets outcompete acrylic on stain resistance and raw-material costs, prompting major U.S. mills to convert lines to PET. Polyester’s mature mechanical and chemical recycling infrastructure also strengthens its eco-profile relative to acrylic. Activewear and budget knitwear increasingly shift to polyester blends that match acrylic’s thermal properties at lower cost, squeezing acrylic’s share in entry-level price tiers.

Stringent Environmental Rules on ACN Emissions

New Best Available Techniques Reference (BREF) standards in the EU require tighter control of ACN off-gassing, compelling mills to invest in scrubbers and incineration upgrades. Similar proposals under the U.S. EPA’s Hazardous Organic NESHAP add capital overheads[2]U.S. EPA, “Hazardous Organic NESHAP—Proposed Amendments,” epa.gov . Compliance costs erode margins for older plants lacking efficient emission-control lines, nudging consolidation toward integrated players that can amortize upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Staple Fiber Dominance Sustains Growth

Staple fiber held 60.78% of the acrylic fiber market in 2025 and is forecast to grow at 3.71% CAGR through 2031. The segment benefits from widespread ring- and open-end-spinning capacity able to process a broad linear-density range, supporting large-volume apparel and home-textile orders. Finer denier advances help staple compete in cashmere-touch knitwear lines, expanding its premium footprint and cushioning price pressures.

Filament accounts for the balance of volume and serves narrow industrial and specialty-fabric niches such as outdoor awnings and flame-retardant uniforms. Although its CAGR trails staple, filament demand remains sticky where continuous-filament strength and even dye uptake are critical. Broader acceptance of solution-dyed technologies may unlock incremental growth, yet current competitiveness relies on niche differentiation rather than scale.

By Blending: Wool Blends Lead While Cellulose Hybrids Rise

Wool blends represented 45.10% of the acrylic fiber market size in 2025, sustained by acrylic’s ability to lower raw material costs and reduce pilling relative to pure wool products. Spinners leverage acrylic to balance hand-feel with price in mid-range sweaters and scarves, reinforcing blend stickiness.

Other blends, encompassing viscose and lyocell hybrids, are projected to expand at 3.41% CAGR, the fastest in the blending category. These combinations respond to brands’ circular-economy goals, delivering improved biodegradability without sacrificing processing versatility. Cotton-acrylic blends occupy volume mid-ground, serving T-shirts and lightweight leisurewear seeking softness and moisture management.

By End-User Industry: Apparel Retains Core Demand Amid Industrial Upswing

The apparel industry captured 58.20% acrylic fiber market share in 2025. Knitwear manufacturers highlight acrylic’s vibrant coloration, warmth, and low-shrink properties in pullovers and outer layers. Mass retailers rely on dependable supply chains from China, India, and Türkiye to keep program costs in check.

Other end-user industries are on course for a 3.86% CAGR, outpacing all other end uses. Stack-gas regulations drive demand for high-loft needle-felts and specialty baghouse cartridges where acrylic outperforms polyester under acidic fumes. Household furnishings occupy an intermediate growth path, aided by hospitality renovations that seek flame-retardant draperies and contract upholstery.

Geography Analysis

Asia-Pacific generated 68.10% of global volume in 2025, underpinned by China’s integrated naphtha-to-ACN chains and a robust downstream textile cluster. Continuous capacity additions in acrylonitrile, sometimes leveraging propane dehydrogenation routes, keep regional cash costs competitive even amid volatile propylene fundamentals. Export-oriented garment hubs in Vietnam and Bangladesh further anchor regional offtake, and regional mills increasingly target recycled-content orders to satisfy Western retailer mandates.

North America and Europe together hold under one-quarter of global volume yet excel in technical-textile innovation and sustainability compliance. U.S. demand concentrates on industrial-filtration and outdoor-performance apparel, while EU mills pivot toward recycled-acrylic and specialty filament lines that fetch higher margins. High energy prices pressure European cost curves, but near-market sourcing and stringent eco-standards sustain a resilient premium-goods niche.

Middle East and Africa is projected to grow at 3.63% CAGR through 2031. Petrochemical investments in Saudi Arabia, Egypt, and the United Arab Emirates aim to monetize abundant propane and circumvent ACN import dependence. Tailored free-zone incentives encourage downstream spinning and knitting clusters, though talent gaps and supply-chain immaturity still temper ramp-up speed. South America continues as a modest consumption basin tethered to domestic textile cycles; its producers focus on capturing regional trade bloc opportunities while mitigating currency volatility.

Competitive Landscape

The acrylic fiber market shows moderate concentration with the top five suppliers representing roughly 55% of global capacity. Aksa Akrilik, Aditya Birla, and major Chinese state-owned groups defend share via captive ACN assets and multi-region spinning hubs. Profitability, however, compressed in 2025 after ACN spikes widened variable-cost spreads; Aksa reported a 76% year-on-year profit drop, and its utilization fell to 78%. Larger Chinese complexes countered volatility by commissioning propane-based ACN pilots that hedge propylene swings and unlock incremental margin headroom.

Strategically, producers prioritize incremental process optimization, scope-3 emission reporting, and recycled-content launches over disruptive fiber inventions. Joint ventures such as DowAksa’s carbon-fiber composites signal moves down the value chain to offset commoditized staple margins. Consolidation activity—exceeding 300 petrochemical deals in 2024—suggests looming mergers of smaller standalone spinners unable to finance EPR-driven recycling lines and environmental retrofits.

Acrylic Fiber Industry Leaders

Aksa Akrilik Kimya Sanayii A.Ş.

Jilin Chemical Fiber Group Co., Ltd.

Dralon GmbH

TAEKWANG INDUSTRIAL CO., LTD.

Aditya Birla Group (Thai Acrylic Fiber)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Aditya Birla Group's Thai Acrylic Fibre partnered with FibreTrace to incorporate tracking technology into acrylic fiber production, creating a digital verification system for Regel recycled fibers. The integration embeds non-toxic, luminescent pigment identifiers into raw fibers, enabling product traceability from production to finished garment.

- September 2024: Asahi Kasei Corporation introduced LASTAN, a non-woven fabric from specialized fire-retardant acrylic fiber. The material delivers enhanced flame resistance, heat resistance, electrical insulation properties, and dimensional stability.

Global Acrylic Fiber Market Report Scope

Acrylic fibers are mainly synthetic fibers. The major raw materials used to manufacture acrylic fibers include acrylonitrile, comonomers, DMF, and additives. Acrylonitrile is the major raw material used in the production of acrylic fiber, which is about 85% of the acrylonitrile units by weight.

The acrylic fiber market is segmented by form, blending, application, and geography. By form, the market is segmented into staple and filament. By blending, the market is segmented into wool, cotton, and other blendings (cellulose). By application, the market is segmented into apparel, household furnishing, industrial, and other applications (upholstery). The report also covers the market sizes and forecasts for the market in 27 countries across major regions. For each segment, the market sizes and forecasts are provided in terms of volume (tons).

| Staple |

| Filament |

| Wool Blend |

| Cotton Blend |

| Other Blendings (Cellulose) |

| Apparel |

| Household Furnishing |

| Industrial |

| Other End-user Industries (Upholstery) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Staple | |

| Filament | ||

| By Blending | Wool Blend | |

| Cotton Blend | ||

| Other Blendings (Cellulose) | ||

| By End-user Industry | Apparel | |

| Household Furnishing | ||

| Industrial | ||

| Other End-user Industries (Upholstery) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the acrylic fiber market?

The current size of the acrylic fiber market is estimated at 1.62 million tons and expected to reach 1.88 million tons, growing at a 3.07% CAGR from 2026.

Which form dominates acrylic fiber demand?

Staple fiber leads, holding 60.78% of 2025 volume and maintaining the fastest growth trajectory through 2031.

Which region will expand fastest in acrylic fiber consumption?

Middle East and Africa is forecast to grow at 3.63% CAGR as petrochemical investments localize supply.

How do EPR mandates influence producers?

Regulations in the EU and California raise compliance costs but create premium pricing for recycled acrylic content.

Page last updated on: