Acrylate Monomers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.81 Billion |

| Market Size (2031) | USD 7.39 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acrylate Monomers Market Analysis by Mordor Intelligence

Acrylate Monomers Market size in 2026 is estimated at USD 5.81 billion, growing from 2025 value of USD 5.54 billion with 2031 projections showing USD 7.39 billion, growing at 4.95% CAGR over 2026-2031. Robust demand from low-VOC architectural paints, pressure-sensitive adhesives, and healthcare coatings is sustaining steady volume gains. Butyl acrylate remains indispensable because it strikes a balance between film hardness and flexibility, enabling formulators to meet stringent VOC limits without the use of coalescent solvents. Regulatory frameworks that cap solvent emissions, paired with tax incentives for onshoring capacity in North America, are encouraging producers to invest in continuous reactors and vacuum stripping technologies. Evolving infrastructure programs in China, India, and the ASEAN region continue to pull acrylic-acid feedstocks eastward, while capacity additions along the U.S. Gulf Coast aim to de-risk reliance on imports. Competitive priorities have shifted from headline prices to service-level agreements, technical collaboration, and residual monomer compliance, compressing margins yet stimulating innovation in UV-curable oligomers for flexible electronics.

Key Report Takeaways

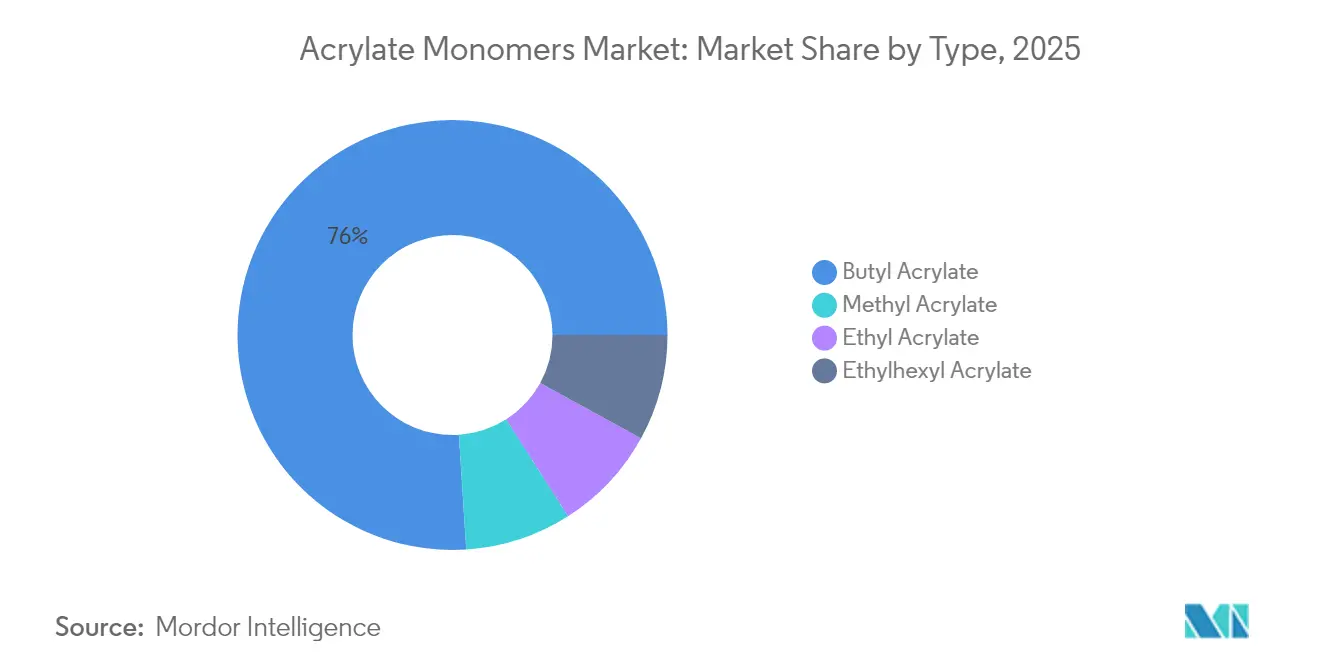

- By type, butyl acrylate captured 76.02% of the global acrylate monomers market share in 2025 and also posted the fastest 5.18% CAGR through 2031 within the acrylate monomers market.

- By application, paints and coatings held a 52.10% share of the acrylate monomers market in 2025, and are projected to advance at a 5.45% CAGR through 2031.

- By end-user sector, construction accounted for 37.05% of demand in 2025, whereas healthcare and hygiene are expanding at a 5.12% CAGR.

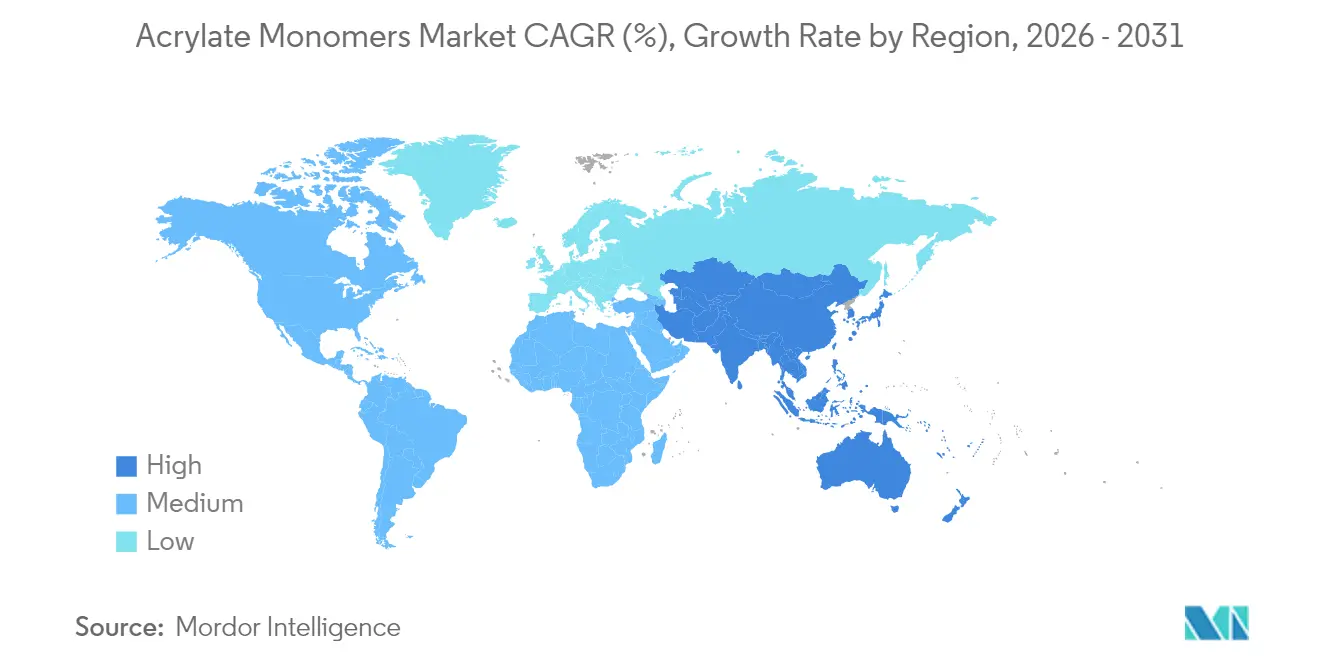

- By geography, the Asia-Pacific region commanded 44.80% of the global volume in 2025 and is forecast to grow at a 5.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acrylate Monomers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-VOC architectural coating boom | +1.8% | Global, strongest in EU and California | Medium term (2-4 years) |

| Rapid expansion of pressure-sensitive adhesive demand | +1.5% | Asia-Pacific core; spill-over to North America | Short term (≤2 years) |

| Asia-Pacific construction super-cycle | +1.3% | China, India, Vietnam, Indonesia | Long term (≥4 years) |

| Rise of UV-curable acrylate formulations for flexible electronics | +0.9% | South Korea, Taiwan, Japan, extending to China | Medium term (2-4 years) |

| On-shoring incentives and antidumping tariffs in North America | +0.7% | United States, Canada | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Low-VOC Architectural Coating Boom

Butyl-acrylate copolymers enable zero-VOC claims while preserving open time, wet-scrub durability, and alkalinity resistance, driving formulators to phase out vinyl acetate. China’s 14th Five-Year Plan mandates low-emission coatings in many of the new residential projects by 2025, accelerating local emulsion-polymer output. In India, small paint makers are adopting pre-compounded acrylic binders to bypass in-house polymerization and speed regional color launches. Third-party verification through ISO 11890 testing and LEED v4.1 credits reinforces procurement criteria that favor advanced acrylic emulsions, underscoring their suitability for use in sustainable building practices[1]International Organization for Standardization, “ISO 11890 VOC Measurement,” iso.org.

Rapid Expansion of Pressure-Sensitive Adhesive Demand

E-commerce packaging, medical tapes, and automotive trim bonding drive the use of acrylate monomer in pressure-sensitive adhesives. Ethylhexyl acrylate supplied the PSA monomer feedstock because it supports low-temperature tack in hot-melt and solvent-free formulations. Southeast Asian corrugated box production is increasing, necessitating the use of optically clear adhesive films for flexible pouches. Medical wearables rely on acrylic PSAs with residual-monomer levels under 100 ppm to meet ISO 10993 skin-sensitization thresholds. FDA guidance on extractables is pushing device makers to specify high-purity ethyl acrylate in wound-care patches.

Asia-Pacific Construction Super-Cycle

Infrastructure spending across Asia-Pacific grew in 2024, channeling acrylate monomers into waterproofing membranes, concrete sealers, and elastomeric fillers. India’s National Infrastructure Pipeline stimulates demand for butyl-acrylate emulsions in exterior insulation systems. Vietnam’s Long Son complex added acrylic-acid capacity, positioning ASEAN suppliers closer to demand centers. Prefabricated construction methods favor fast-curing acrylic sealants that tolerate shipping-induced thermal cycling. Local green-building labels such as GRIHA embed low-VOC acrylic coatings into public tenders, locking in long-term monomer offtake.

Rise of UV-Curable Acrylate Formulations for Flexible Electronics

Flexible printed circuit boards and foldable displays utilize UV-curable acrylate oligomers. Ethoxylated trimethylolpropane triacrylate and urethane-acrylate hybrids deliver high elongation and optical clarity, surpassing epoxy adhesives that yellow under blue light. Samsung Display and LG Display have qualified acrylic optically clear adhesives, securing captive demand in South Korea. Fan-out wafer-level packaging is driving the need for underfill resins that cure in under two seconds, an application well-suited to acrylate chemistry. IEC 61249 and ISO 9022 standards integrate acrylic performance metrics into supplier audits, strengthening barriers to entry.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile propylene and acrylic-acid feedstock costs | –0.6% | Global, most acute in naphtha-reliant regions | Short term (≤2 years) |

| Regulatory squeeze on residual monomer toxicity | –0.4% | EU and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Competition from next-gen polyurethane dispersions in coatings | –0.3% | Northern Europe, North America, East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Propylene and Acrylic-Acid Feedstock Costs

Propylene spot values fluctuated in 2024 due to refinery maintenance, PDH start-ups, and polypropylene market competition. Formulators are trialing bio-based methyl acrylate derived from glycerol or lactic acid. The EU’s Carbon Border Adjustment Mechanism embeds feedstock carbon intensity into procurement, encouraging the development of long-term propylene supply contracts[2]European Chemicals Agency, “REACH Candidate List,” echa.europa.eu.

Regulatory Squeeze on Residual Monomer Toxicity

The European Chemicals Agency added butyl acrylate to the REACH Candidate List in 2024. The EPA’s TSCA evaluation for methyl acrylate identified occupational inhalation as a priority pathway, prompting the implementation of engineering controls that add to production costs. Polymer plants are investing in vacuum stripping and steam distillation lines to achieve sub-100 ppm levels, consistent with ISO 11014 packaging guidance. Smaller players lacking retrofit capital are exiting commodity grades and turning to toll manufacturing of specialty oligomers. FDA extractables guidance is extending toxicity testing to acrylate-based drug-delivery devices, raising entry barriers for new suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Butyl Acrylate Retains Structural Leadership

Butyl acrylate accounts for 76.02% of the total volume and is expected to advance at a 5.18% CAGR through 2031. Continuous-reactor upgrades shorten cycle times, reducing energy consumption and enabling responsive spot market sales. Ethyl acrylate targets high-solids industrial coatings where faster cure rates justify its premium pricing. Ethylhexyl acrylate is a key component in pressure-sensitive adhesives that require low-temperature tack in medical and automotive tapes. Methyl acrylate occupies a niche in pharmaceutical intermediates and UV-curable oligomers, benefiting from rapid radical-polymerization kinetics.

Sustained investment in ISO 9001 and ISO 14001 certification is now mandatory for suppliers serving multinational paint and adhesive firms, raising entry barriers for regional producers. The acrylate monomers market continues to favor integrated players that can offer formulation assistance and residual monomer guarantees under 100 ppm. Continuous processes also provide consistent molecular-weight distribution, a key requirement for low-temperature flexibility in architectural coatings. Producers that retrofit reactors with advanced pressure control can toggle between monomer grades, maximizing asset utilization.

By Application: Paints and Coatings Dominate as Adhesives Accelerate

Paints and coatings accounted for 52.10% of the acrylate monomers market volume in 2025 and are expected to grow at a 5.45% CAGR through 2031. Automotive refinish and industrial maintenance coatings also lean on ethyl acrylate for faster drying. Adhesives and sealants are expanding as e-commerce, wearable sensors, and flexible displays proliferate.

Plastics and polymers absorb acrylate monomers, with core-shell impact modifiers improving Izod strength in lightweight automotive parts. UV-curable printing inks are transitioning to acrylate oligomers for sub-second curing on food-contact substrates that must meet EU 10/2011 migration limits. Other outlets, including textile finishes and construction chemicals, account for a small portion. ISO 11890 VOC testing and ASTM D4060 abrasion metrics standardize performance benchmarks, accelerating solvent-borne replacement.

By End-User Sector: Construction Commands Volume, Healthcare Outpaces Growth

Construction captured 37.05% of the acrylic monomers market demand in 2025, reflecting Asia-Pacific infrastructure pipelines consuming acrylic waterproofing membranes and sealants. The growing demand from the automotive and transportation sector, with EV factories specifying acrylic battery binders and underbody coatings that meet FMVSS 302 flammability standards. Ethylhexyl-acrylate PSAs in flexible pouches and corrugated boxes drive the packaging sector. Electronics and electrical applications are primarily focused on optically clear adhesives for foldable OLED screens and UV-curable underfills in semiconductor packaging.

Healthcare and hygiene are the fastest-growing end-user segments, growing at a 5.12% CAGR, buoyed by single-use medical-device coatings and superabsorbent cores in incontinence products. Aging demographics in North America and Europe are driving the expansion of chronic-disease monitoring, prompting the use of high-purity ethyl acrylate in wound-care wraps. FDA extractables guidance reinforces the pivot to low-toxicity acrylic systems.

Geography Analysis

The Asia-Pacific region held 44.80% of the acrylate monomers market volume in 2025 and is projected to grow at a 5.28% CAGR from 2026 to 2031, at the highest regional pace. China is channeling butyl-acrylate emulsions into coatings for new housing units, while the Shenzhen and Suzhou electronics clusters utilize UV-curable oligomers for foldable screens. The National Infrastructure Pipeline spending on highways, airports, and affordable housing lifts demand in India.

North America commands a significant portion of global consumption. Canada’s share concentrates on methyl acrylate for EV battery binders, supported by Strategic Innovation Fund co-grants. Mexico contributes as near-shoring drives ethylhexyl-acrylate uptake in automotive and electronics assembly, backed by USMCA rule-of-origin incentives.

Germany, France, and the United Kingdom lead Europe's demand. REACH fees and CBAM carbon levies encourage the substitution of methyl acrylate with bio-based alternatives. The Middle East and Africa share is centered on Saudi Arabian and UAE petrochemical hubs targeting export-oriented acrylic acid. ISO 9001 and ISO 14001 compliance are now mandatory credentials for suppliers entering multinational supply chains.

Competitive Landscape

The acrylate monomers market is moderately consolidated. Competition centers on service reliability, technical co-development, and guaranteed residual monomer ceilings, rather than list price. Vertical integration strategies include adhesive formulators purchasing stakes in monomer plants to secure captive supply and tariff advantages. Continuous-reactor retrofits at leading plants reduce batch cycles, trim utility costs, and enable just-in-time delivery windows of under 48 hours. Regional Chinese players have narrowed the technology gap and now sell ethylhexyl acrylate at prices below Western benchmarks, capturing a share of the Southeast Asian adhesive compound market. Margin pressure from volatile propylene prices and tighter residual-monomer rules is prompting consolidation, with smaller producers exiting commodity grades to focus on toll manufacturing of high-purity methyl acrylate for pharma intermediates. Incumbents are channeling research and development into UV-curable oligomers for flexible circuits and optically clear adhesives, segments where differentiated performance commands premiums that offset fluctuations in feedstock costs. Compliance with REACH, TSCA, ISO 10993, and IEC 61249 embeds traceability and documentation requirements throughout the supply chain, further raising the hurdles for new entrants.

Acrylate Monomers Industry Leaders

BASF SE

Arkema

Dow

LG Chem

Nippon Shokubai Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Arkema began commercial production of bio-based ethyl acrylate at its Carling, France site, achieving a 40% bio-carbon content and reducing product-carbon footprint by up to 30%.

- May 2024: Nippon Shokubai Indonesia has secured ISCC-Plus certification and is now marketing biomass-derived acrylic acid and acrylates to reduce life-cycle emissions in diapers and paints.

Global Acrylate Monomers Market Report Scope

Acrylate monomers typically feature vinyl groups, which consist of two carbon atoms double-bonded to each other and directly linked to the carbonyl carbon of the ester group. Acrylates exhibit a range of notable properties, including good absorbency, transparency, flexibility, toughness, and hardness. These acrylic acid esters find utility in numerous applications, including paints and coatings, plastics, adhesives and sealants, and printing inks.

The acrylate monomers market is segmented by type, application, and geography. By type, the market is segmented into butyl acrylate, ethyl acrylate, 2-ethyl hexyl acrylate, and methyl acrylate. By application, the market is segmented into paints and coatings, plastics, adhesives, printing inks, and other applications. The report also covers the market sizes and forecasts for the acrylate monomers market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

| Butyl Acrylate |

| Ethyl Acrylate |

| Ethylhexyl Acrylate |

| Methyl Acrylate |

| Paints and Coatings |

| Adhesives and Sealants |

| Plastics and Polymers |

| Printing Inks |

| Other Applications |

| Construction |

| Automotive and Transportation |

| Packaging |

| Electronics and Electrical |

| Healthcare and Hygiene |

| Asia-Pacifc | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Butyl Acrylate | |

| Ethyl Acrylate | ||

| Ethylhexyl Acrylate | ||

| Methyl Acrylate | ||

| By Application | Paints and Coatings | |

| Adhesives and Sealants | ||

| Plastics and Polymers | ||

| Printing Inks | ||

| Other Applications | ||

| By End-User Sector | Construction | |

| Automotive and Transportation | ||

| Packaging | ||

| Electronics and Electrical | ||

| Healthcare and Hygiene | ||

| By Geography | Asia-Pacifc | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the acrylate monomers market?

The acrylate monomers market size is expected to reach USD 5.81 billion by 2026.

Which segment holds the largest share in acrylate monomer demand?

Butyl acrylate accounts for 76.02% of the global volume due to its versatility in coatings and adhesives.

Which region leads consumption growth for acrylate monomers?

Asia-Pacific leads with 44.80% share in 2025 and a 5.28% CAGR through 2031.

Why are UV-curable acrylate formulations gaining traction?

Flexible electronics and foldable displays require fast-curing, optically clear adhesives that acrylates provide better than epoxies.

Page last updated on: