Solid-grade Thermoplastic Acrylic (Beads) Resin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

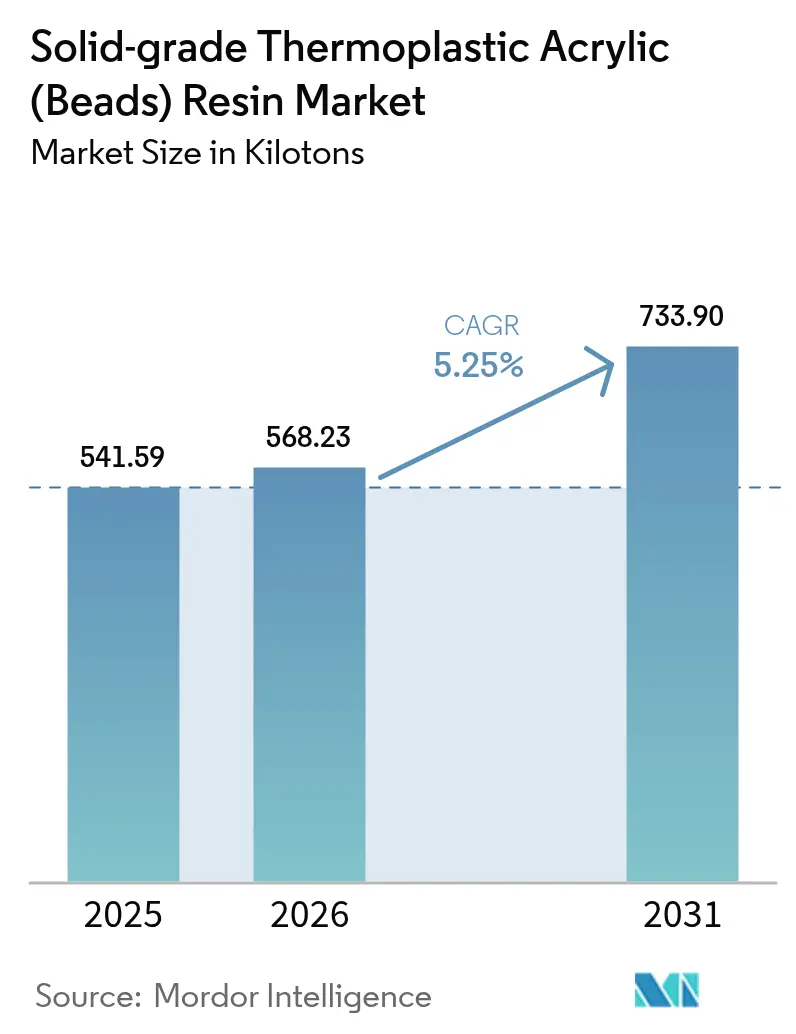

| Market Volume (2026) | 568.23 kilotons |

| Market Volume (2031) | 733.90 kilotons |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solid-grade Thermoplastic Acrylic (Beads) Resin Market Analysis by Mordor Intelligence

The Solid-grade Thermoplastic Acrylic Resin Market size is projected to be 541.59 kilotons in 2025, 568.23 kilotons in 2026, and reach 733.90 kilotons by 2031, growing at a CAGR of 5.25% from 2026 to 2031. Producers are reducing commodity methyl methacrylate (MMA) monomer production while redirecting investments toward high-margin specialty beads used in UV-curable wood finishes, 3D-printing photoresins, and thermal-management pads for electric vehicle batteries. Chemical-recycling initiatives, which reduce greenhouse gas emissions by 50%, are gaining traction, with OEMs committing to purchase recycled polymethyl methacrylate (PMMA) content. This supports premium pricing within automotive and consumer electronics supply chains. Regulatory measures, such as the European Union’s Regulation 2023/2055 and China’s GB 38507-2020, are driving the adoption of water-based, high-solid, and bead-modified UV systems that meet microplastic and VOC compliance standards. Current investment strategies focus on logistics enhancements and selective debottlenecking, rather than constructing new large-scale plants, as feedstock volatility underscores the importance of supply chain flexibility.

Key Report Takeaways

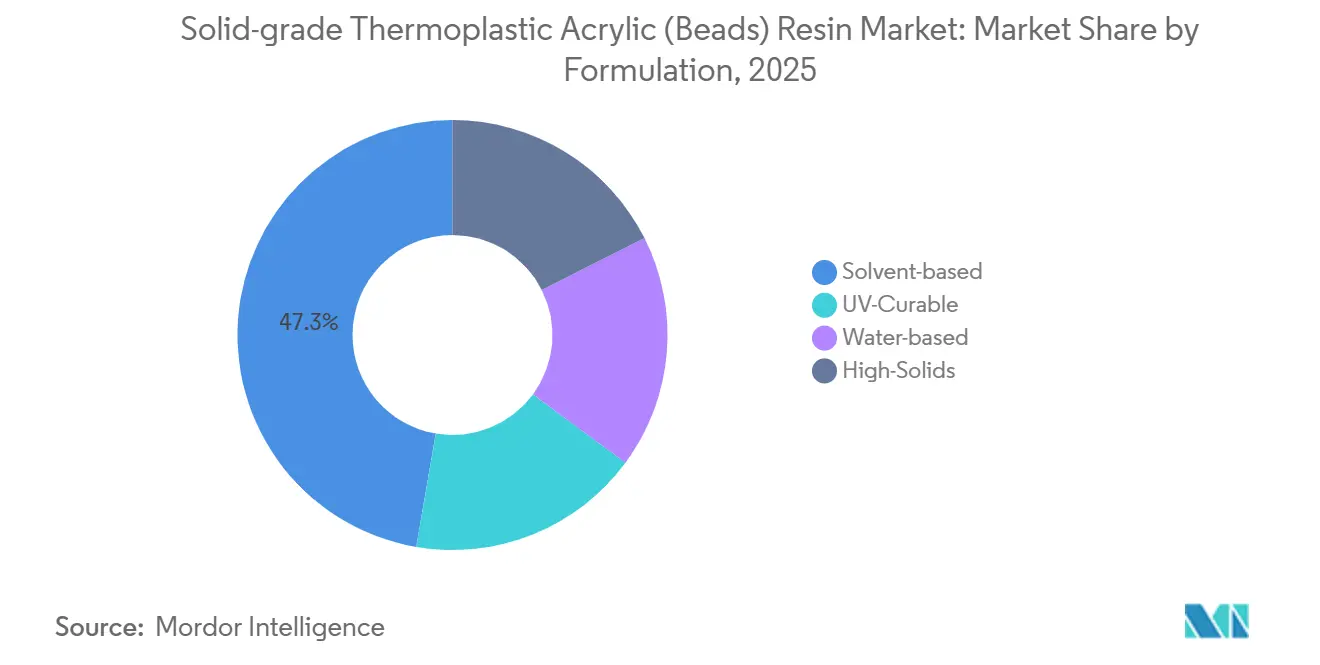

- By formulation, solvent-based held 47.31% of the solid-grade thermoplastic acrylic (beads) resin market share in 2025, while UV-curable is projected to post a 6.15% CAGR through 2031.

- By application, paints and coatings led with 53.45% of the solid-grade thermoplastic acrylic (beads) resin market share in 2025, whereas acrylic composite resins are forecast to expand at a 5.82% CAGR through 2031.

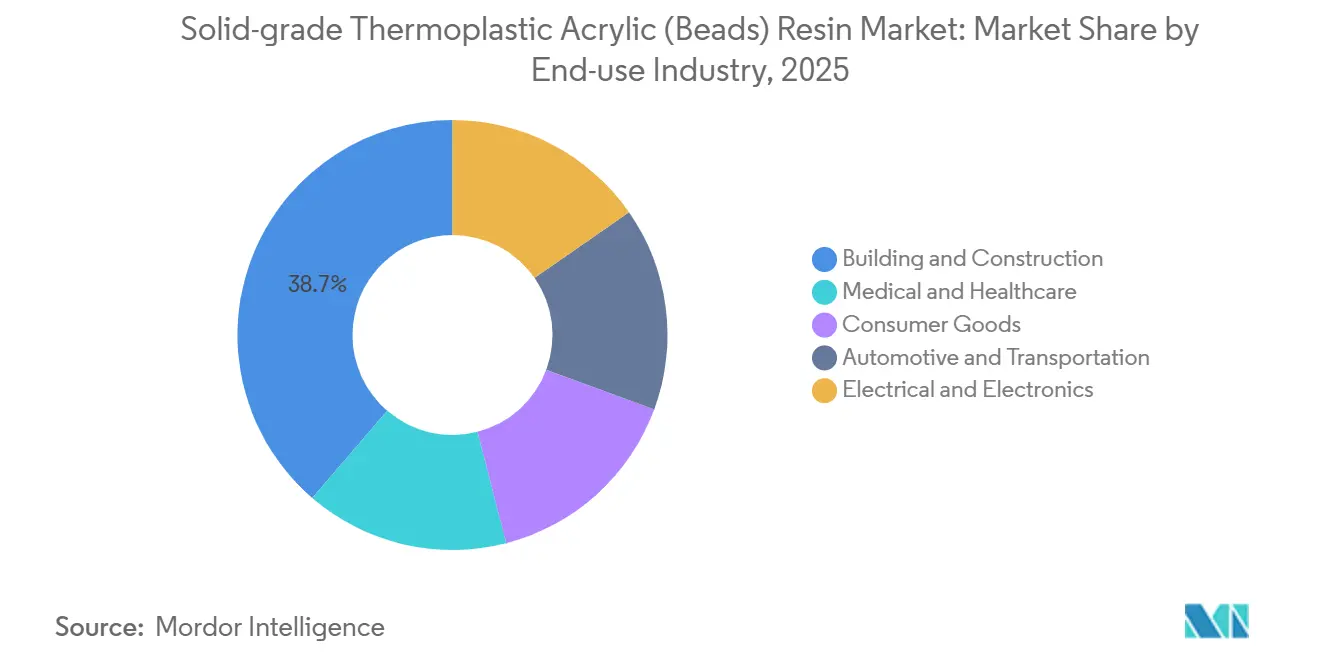

- By end-use industry, building and construction accounted for 38.70% of the solid-grade thermoplastic acrylic (beads) resin market share in 2025; automotive and transportation is expected to grow at a 5.99% CAGR through 2031.

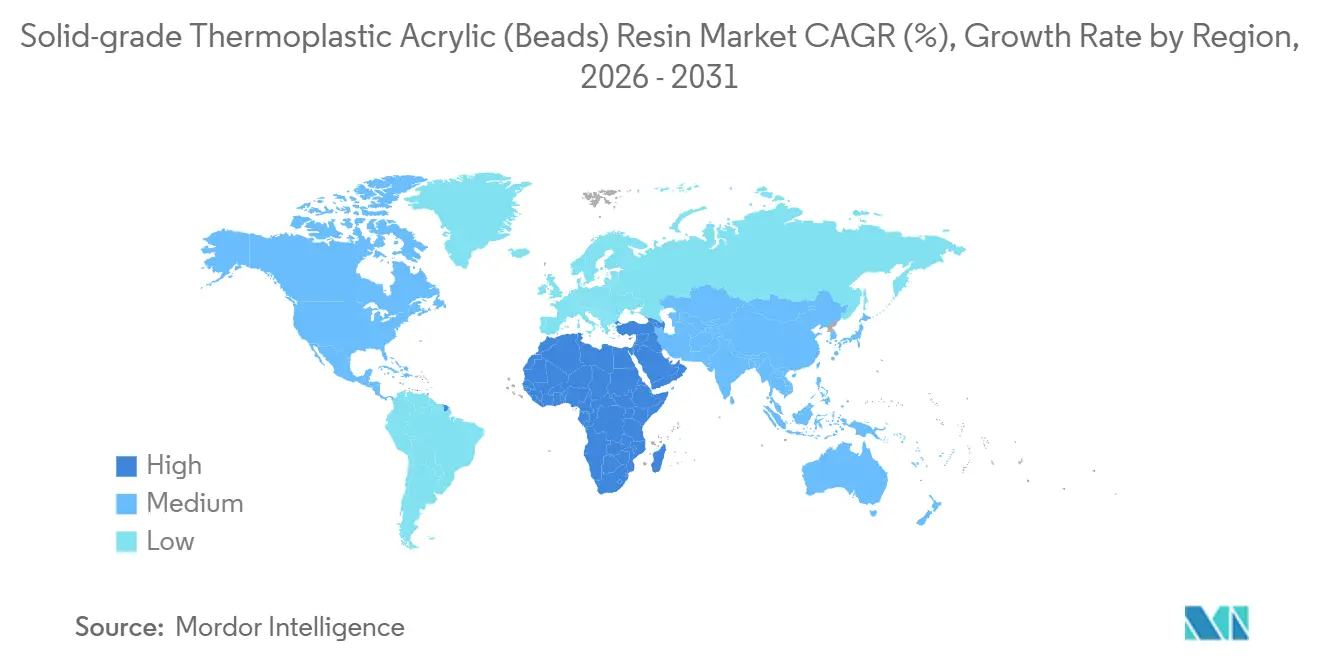

- By geography, Asia-Pacific commanded 45.38% the solid-grade thermoplastic acrylic (beads) resin market share in 2025, while the Middle-East and Africa are on track for a 5.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Solid-grade Thermoplastic Acrylic (Beads) Resin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing paints and coatings consumption in Asia and North America | +1.2% | Asia-Pacific core, North America secondary | Medium term (2-4 years) |

| Automotive shift to lightweight, transparent PMMA lighting modules | +0.9% | Global, with concentration in Germany, Japan, South Korea, United States | Medium term (2-4 years) |

| Global conversion to high-solid and powder coatings | +0.8% | North America and EU primary, spill-over to APAC | Long term (≥ 4 years) |

| 3D printing photoresin formulators adopting bead-based rheology modifiers | +0.5% | North America, Western Europe, emerging in China | Short term (≤ 2 years) |

| Integration of PMMA bead modifiers in EV battery thermal-interface materials | +0.7% | APAC core (China, South Korea), expanding to EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Paints and Coatings Consumption in Asia and North America

The architectural coatings market in the Asia-Pacific region is experiencing significant growth, with bead volumes increasing at a rate surpassing regional GDP. This expansion is driven by tier-2 and tier-3 cities reducing the per-capita paint usage gap compared to developed markets. In Saudi Arabia, the coatings market reached USD 1.55 billion in sales in 2025, with new coil lines adopting low-VOC acrylic systems to comply with green building codes. In North America, the U.S. National Emission Standards for Hazardous Air Pollutants are encouraging industrial users to transition to 65–70%-solid solvent systems, reducing booth emissions by 40%[1]U.S. Environmental Protection Agency, “National Emission Standards for Hazardous Air Pollutants,” EPA Website, epa.gov. In China, the GB 38507-2020 VOC cap of 420 g/L for industrial coatings is driving the replacement of styrene-acrylic emulsions with thermoplastic acrylic beads that dissolve in exempt solvents. These trends collectively boost demand for specialty bead chemistries, even as commodity solvent-based products lose relevance.

Automotive Shift to Lightweight, Transparent PMMA Lighting Modules

Automotive original equipment manufacturers (OEMs) are increasingly replacing glass and polycarbonate with injection-molded PMMA, which offers a 45% weight reduction and 10-year UV stability. New bead grades can withstand continuous exposure to temperatures of 150 °C, allowing proximity to LEDs without yellowing. Patent filings for paint-free PMMA/ASA alloys rose in 2024, aiming to integrate optical lenses and structural ribs in a single molding cycle. Electric vehicle platforms favor PMMA's density of 1.18 g/cm³, as every 10 kg saved extends the vehicle's range by approximately 1.5%. Although post-mold hard-coating adds USD 3 per lamp, OEMs accept the additional cost to achieve energy efficiency and design flexibility.

Global Conversion to High-Solid and Powder Coatings

Industrial coaters are transitioning from 45–55% to 65–75% solids to produce single-coat, 75-micron dry films, which reduce oven dwell time by half and double line speeds. A high-solid bead introduced in 2025 suspends in butyl acetate at 72% w/w without gelling, enabling coil coaters to eliminate flash-off zones and reclaim 8 meters of oven length. Powder coating lines utilize thermoplastic acrylic beads as flow agents to create smooth films cured below 180 °C. Additionally, bio-based bead variants containing 35% renewable carbon support formulators aiming for ISCC PLUS certification. Proposed EU packaging legislation requiring pellet-spill prevention plans will add EUR 0.12 per kilogram to handling costs, further encouraging the adoption of high-solid and powder systems that minimize bulk-pellet movements.

3D-Printing Photoresin Formulators Adopting Bead-Based Rheology Modifiers

Stereolithography resins require viscosity levels between 200–800 cP for uniform layer formation, and bead-based modifiers achieve this without causing UV scatter. Methacrylic beads functionalized with photoinitiator groups polymerize into the resin matrix, increasing tensile strength by 22% compared to silica-filled alternatives. Dental and jewelry resins containing 3–5% acrylic beads exhibit 30% less shrinkage during curing, maintaining accuracy within 50 microns. Despite a baseline demand of 1,200 tons in 2025, this niche market commands prices four to five times higher than commodity beads, attracting incremental capacity from diversified producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MMA feedstock price volatility | -0.6% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Tightening EU and China solvent-emission/microbead regulations | -0.4% | EU primary, China secondary, spillover to export-oriented ASEAN | Medium term (2-4 years) |

| Cost-competitive styrenic substitutes (ASA/ABS) | -0.3% | Automotive and electronics segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MMA Feedstock Price Volatility

MMA spot prices fluctuated significantly, rising from USD 1,650 per ton in January 2024 to USD 2,100 by September, before settling at USD 1,820 in early 2025. This 27% price variation limits formulators' ability to secure annual contracts and forces resin producers to implement rolling surcharges. The cancellation of a 350,000-tons U.S. MMA project removed a potential supply buffer, while an 80% shutdown of Singapore's capacity in September 2024 further tightened availability in Asia. Buyers are exploring methacrylic-acid esterification routes to bypass acetone cyanohydrin, but these methods involve higher costs and additional distillation steps.

Tightening EU and China Solvent-Emission/Microbead Regulations

Regulation 2023/2055, effective from October 2023, bans microplastics ≥0.01% w/w and requires industry reporting to ECHA by 2026. Acrylic beads sized 5–15 µm, commonly used as matting agents, fall under this regulation unless permanently bound in a film, necessitating costly abrasion-resistance testing. China's parallel regulations align with EU definitions but provide less clarity on grace periods, prompting exporters to adhere to the stricter EU timeline to maintain market access. Compliance costs, ranging from EUR 15,000 to 25,000 per formulation, are manageable for multinational companies but burdensome for regional blenders. This accelerates market consolidation and promotes the adoption of high-solid or UV-curable chemistries that eliminate free microbeads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Specialties Displace Commodity Solvent Grades

Solvent-based formulations retained 47.31% of the 2025 volume, as their fast drying times remain essential for legacy coil-coating and refinish lines. High-solid systems with over 65% non-volatile content are gaining market share due to their ability to reduce labor by 35% through single-coat applications. UV-curable beads are projected to grow at a CAGR of 6.15% through 2031, outpacing other categories.

The adoption of water-based chemistries is strongest in architectural coatings, particularly in regions with 50 g/L VOC limits in several U.S. states. However, adoption is slower in unheated warehouses where freeze-thaw durability is critical. Incremental capacity is being added through continuous debottlenecking rather than greenfield expansions, as demonstrated by an 8,000-tons facility in Worms, Germany, which produces beads with ±1.5 µm particle-size control for premium UV-clearcoats.

By Application: Coatings Anchor Demand, Composites Accelerate

Paints and coatings accounted for 53.45% of 2025 consumption, supported by infrastructure projects across Asia and North America. Coil-coating lines for pre-painted steel roofing require beads with glass-transition temperatures above 85 °C to prevent cracking during post-forming processes, while transportation topcoats demand HALS-stabilized beads to maintain color integrity under 500-hour UV-weathering cycles.

Acrylic composite resins used in head-up display housings, transparent electronics covers, and lightweight exterior lamp modules are forecast to grow at a CAGR of 5.82% through 2031. Specialty applications in adhesives, medical devices, and cosmetics command price premiums, influencing capacity allocation decisions.

By End-use Industry: EV-Led Automotive Closes Gap With Construction

The building and construction industry captured 38.70% of the 2025 volume, supported by Asia-Pacific’s housing developments and U.S. infrastructure upgrades. The automotive and transportation sector is expected to grow at a CAGR of 5.99% through 2031, driven by increased electric vehicle (EV) production and lighting redesigns, which boost PMMA usage in lenses, battery thermal interface materials (TIMs), and interior trim.

The electronics and electrical industries are adopting bead-modified PMMA for LED display light guides and thermally conductive adhesives in 5G base stations, where a dielectric constant of 2.6 enhances signal integrity. Medical-grade PMMA beads, which meet USP Class VI standards, command six-fold price premiums over commodity grades. Automakers’ commitments to circular content are expected to align recycled PMMA demand with EV production growth.

Geography Analysis

Asia-Pacific accounted for 45.38% of global volume in 2025, driven by China’s 180,000-ton PMMA capacity and India’s 12% annual construction growth. China’s enforcement of a 420 g/L VOC ceiling is accelerating the shift to water-based and high-solid systems, with a Jiangsu producer adding 15,000 tons of capacity in 2024 to meet demand[2]Ministry of Ecology and Environment, “VOC Regulations Accelerate Water-Based Coatings in China,” MEE Website, mee.gov.cn. Japan and South Korea are focusing on high-purity medical-grade beads, supported by a KRW 48 billion expansion scheduled for completion in 2026.

North America’s mature market benefits from reshored automotive lighting production and industrial high-solid coatings. The cancellation of a U.S. greenfield MMA plant has mitigated potential oversupply, maintaining stable margins for domestic resin producers. In Europe, cost pressures have increased following the closure of two commodity MMA plants, though Germany’s tier-1 lighting suppliers continue to drive demand for specialty grades.

The Middle-East and Africa, led by Saudi Arabia’s low-VOC construction standards, are projected to grow at a CAGR of 5.56% through 2031. Turkey’s automotive part exports to Europe and the UAE’s USD 200 billion construction pipeline through 2030 are expected to support regional demand for acrylic beads. In South America, demand is concentrated in Brazil, but currency volatility and tariffs are limiting local compounding investments.

Competitive Landscape

The solid-grade thermoplastic acrylic (beads) resin market is moderately concentrated, with the top five producers, including Röhm, Mitsubishi Chemical, LX MMA, CHIMEI, and Trinseo, controlling approximately 51% of installed capacity in 2025. Strategic shifts are evident as companies close commodity MMA plants while expanding specialty bead lines. For instance, an 80% capacity reduction in Singapore was paired with a chemical-recycling initiative that achieves 15% price premiums on recycled PMMA.

Technological advancements play a critical role. One producer filed eight patents in 2024 for bead dispersions tailored to stereolithography, targeting additive manufacturing customers. Another repurposed gas-separation bead for EV battery TIMs, showcasing cross-platform innovation that pure-play PMMA firms may struggle to replicate. Bio-based beads derived from waste glycerol entered commercial powder-coating lines in 2025, addressing sustainability requirements from original equipment manufacturers (OEMs).

Feedstock integration remains a key differentiator in margin performance. Vertically integrated producers are better positioned to manage MMA price volatility compared to merchant compounders, who require 12-18 months to recover cost increases. Continuous logistics improvements, such as automated silo loading in Germany that reduced packaging costs by 12%, highlight the focus on supply reliability over volume expansion.

Solid-grade Thermoplastic Acrylic (Beads) Resin Industry Leaders

Röhm GmbH

Trinseo

Mitsubishi Chemical Group Corporation

CHIMEI

LX MMA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Lummus Technology and Sumitomo Chemical Co., Ltd. announced the commercial availability of their advanced chemical recycling technology for polymethyl methacrylate (PMMA). This collaboration utilized Sumitomo Chemical's proprietary technology, which was successfully validated at a pilot plant in Japan to produce high-purity monomer yields.

- May 2025: Sumitomo Chemical Co., Ltd. launched high-quality chemically recycled PMMA, produced using methyl methacrylate (MMA) monomers, targeting the automotive and display industries. Key partners, such as LG Display and Nissan Motor, utilized this material for light guide plates in LCD backlights and automotive headlight lenses, respectively.

Global Solid-grade Thermoplastic Acrylic (Beads) Resin Market Report Scope

Solid-grade thermoplastic acrylic (bead) resins, such as Paraloid B-64, are durable, fast-drying polymers widely used in coatings, inks, adhesives, and road markings. These resins provide strong adhesion, chemical resistance, and a high-gloss finish.

The solid-grade thermoplastic acrylic (beads) resin market is segmented by formulation, application, end-use industry, and geography. By formulation, the market is segmented into solvent-based, water-based, high-solids, and UV-curable. By application, the market is segmented into paints and coatings, acrylic composite resins, and other applications. By end-use industry, the market is segmented into building and construction, automotive and transportation, electrical and electronics, medical and healthcare, and consumer goods. The report also covers the market size and forecasts for the solid-grade thermoplastic acrylic (beads) resin in 19 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Solvent-based |

| Water-based |

| High-Solids |

| UV-Curable |

| Paints and Coatings | Coil Coatings |

| Industrial Coatings | |

| Architectural Coatings | |

| Transportation Coatings | |

| Acrylic Composite Resins | |

| Other Applications |

| Building and Construction |

| Automotive and Transportation |

| Electrical and Electronics |

| Medical and Healthcare |

| Consumer Goods |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Formulation | Solvent-based | |

| Water-based | ||

| High-Solids | ||

| UV-Curable | ||

| By Application | Paints and Coatings | Coil Coatings |

| Industrial Coatings | ||

| Architectural Coatings | ||

| Transportation Coatings | ||

| Acrylic Composite Resins | ||

| Other Applications | ||

| By End-use Industry | Building and Construction | |

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Medical and Healthcare | ||

| Consumer Goods | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the solid-grade thermoplastic acrylic (beads) resin market?

The solid-grade thermoplastic acrylic (beads) resin market stands at 568.23 kilo tons in 2026 and is forecast to reach 733.90 kilo tons, expanding at a 5.25% CAGR from 2026.

Which formulation will grow fastest through 2031?

UV-curable is projected to register a 6.15% CAGR through 2031, outpacing water-based and high-solid systems.

Why are automotive OEMs increasing PMMA bead usage?

PMMA lenses cut lighting assembly weight by 45% and help electric-vehicle platforms improve driving range without compromising UV durability.

How do evolving microplastic rules affect acrylic bead suppliers?

EU and Chinese regulations require costly abrasion testing or a shift to high-solid systems that permanently bind beads, favoring large incumbents with in-house labs.

Page last updated on: