Acetone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.71 Billion |

| Market Size (2031) | USD 10.6 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acetone Market Analysis by Mordor Intelligence

The Acetone market size is expected to grow from USD 7.23 billion in 2025 to USD 7.71 billion in 2026 and is forecast to reach USD 10.6 billion by 2031 at 6.58% CAGR over 2026-2031. This market size trajectory is supported by acetone’s expanding role as a VOC-exempt solvent, a feedstock for methyl methacrylate (MMA) and bisphenol A (BPA) co-production, and a high-purity medium for pharmaceutical manufacturing. Electric vehicle lightweighting, personal care demand in emerging economies, and post-COVID pharmaceutical capacity additions are accelerating volume growth. At the same time, bio-acetone technologies are eroding the dominance of cumene-based supply chains, while regulatory pressures on BPA and refinery rationalizations tighten traditional feedstock availability. Competitive dynamics remain moderate as vertically integrated majors secure raw materials and downstream outlets, even as biotechnology start-ups demonstrate carbon-negative acetone routes that could re-set industry cost curves.

Key Report Takeaways

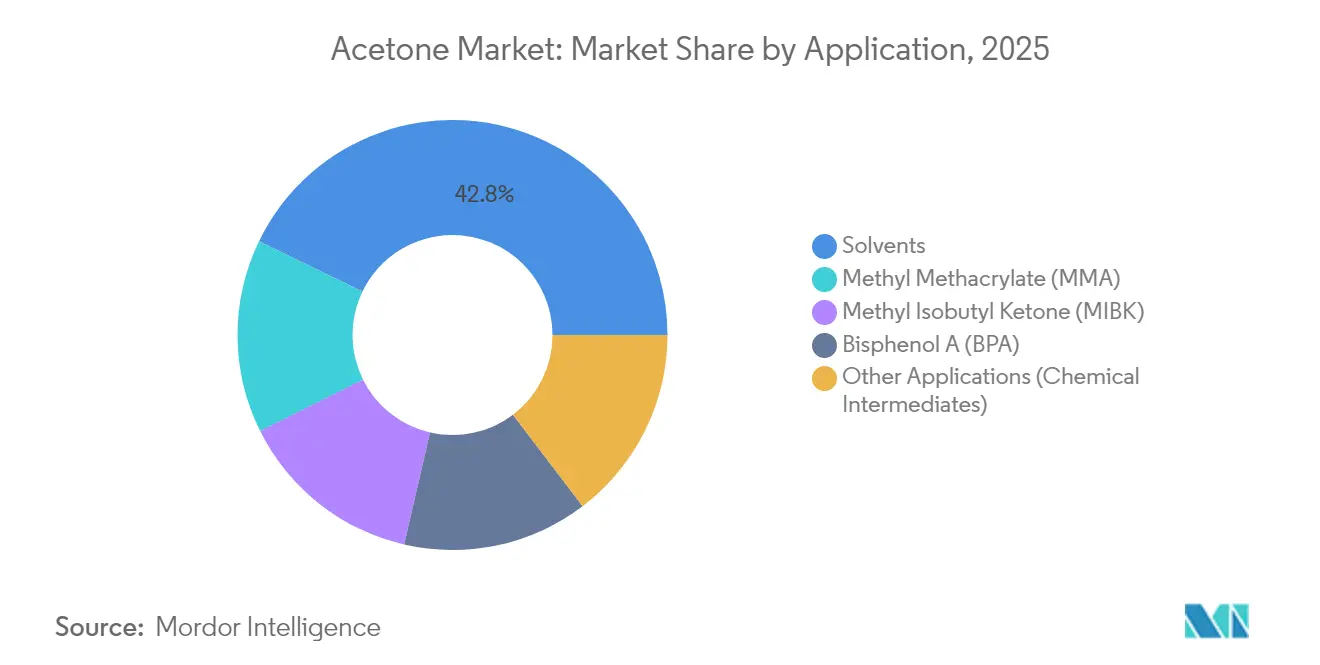

- By application, solvents led with a 42.82% revenue share in 2025, whereas methyl methacrylate is projected to advance at a 7.12% CAGR through 2031.

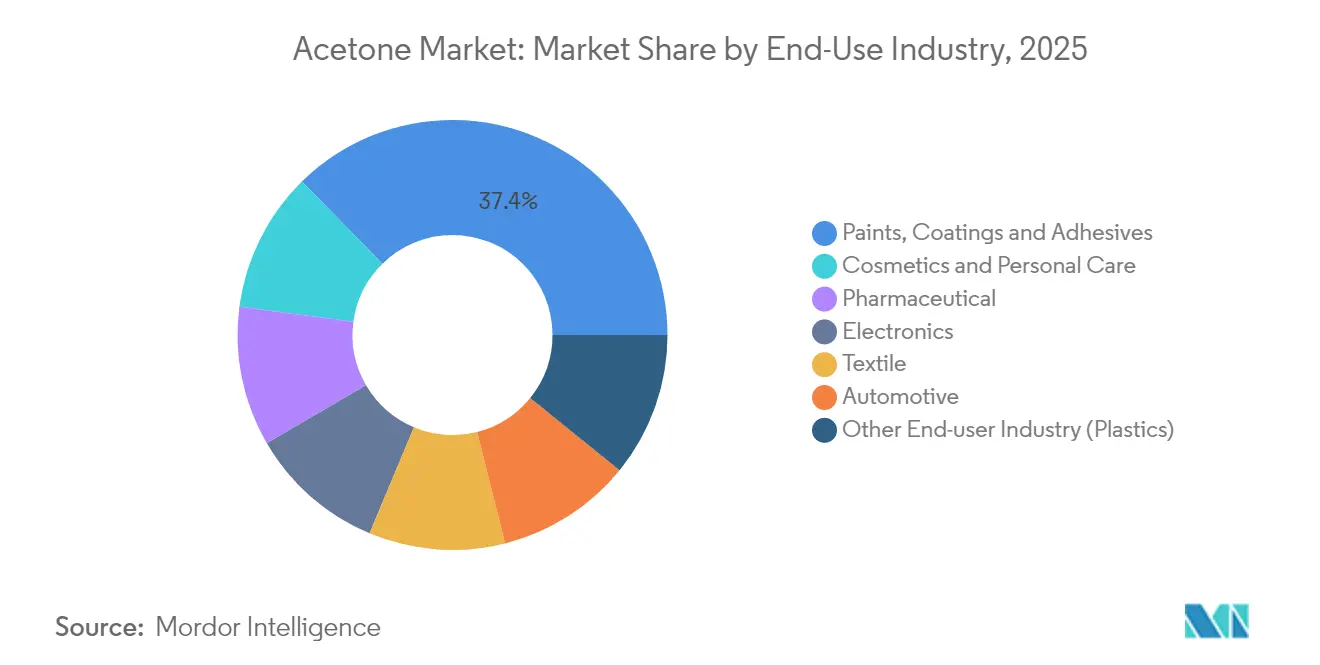

- By end-use industry, paints, coatings, and adhesives accounted for 37.35% of 2025 sales, while cosmetics and personal care are expanding at a 6.95% CAGR.

- By production process, the cumene route held 82.95% of the acetone market share in 2025, even as bio-fermentation is growing at 7.92% CAGR.

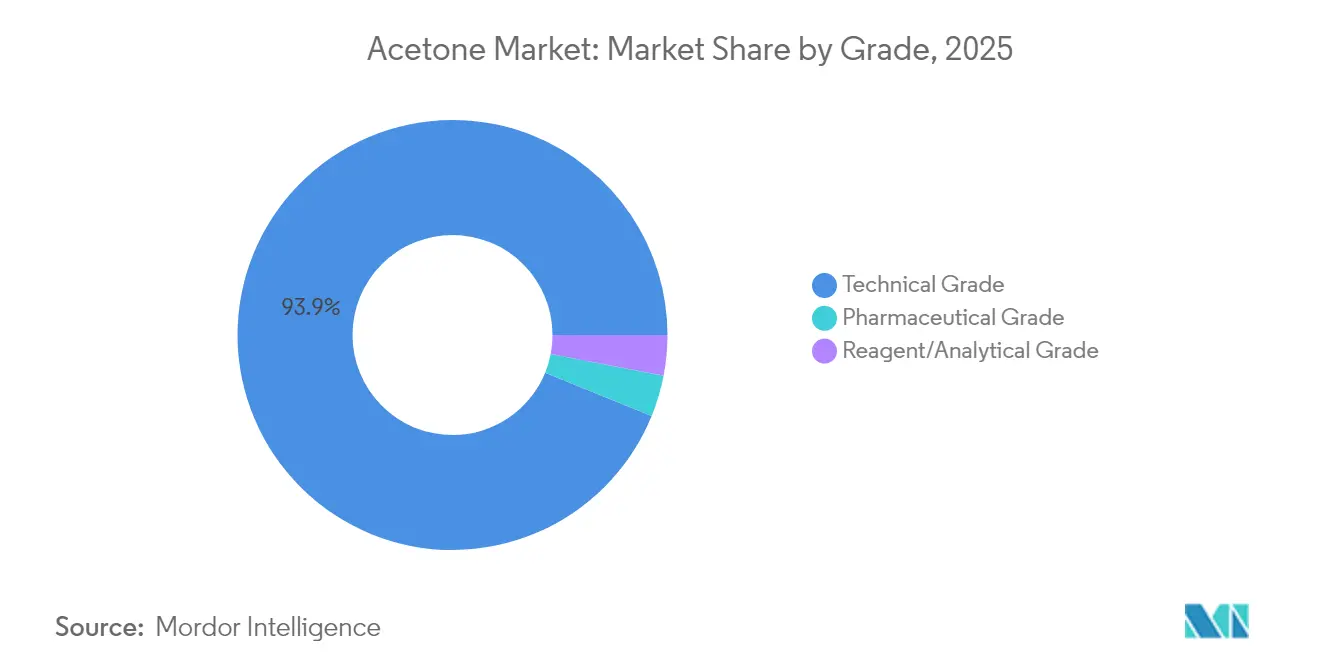

- By grade, technical quality dominated volume with 93.85%, whereas pharmaceutical grade is rising at a 7.45% CAGR on the back of API demand.

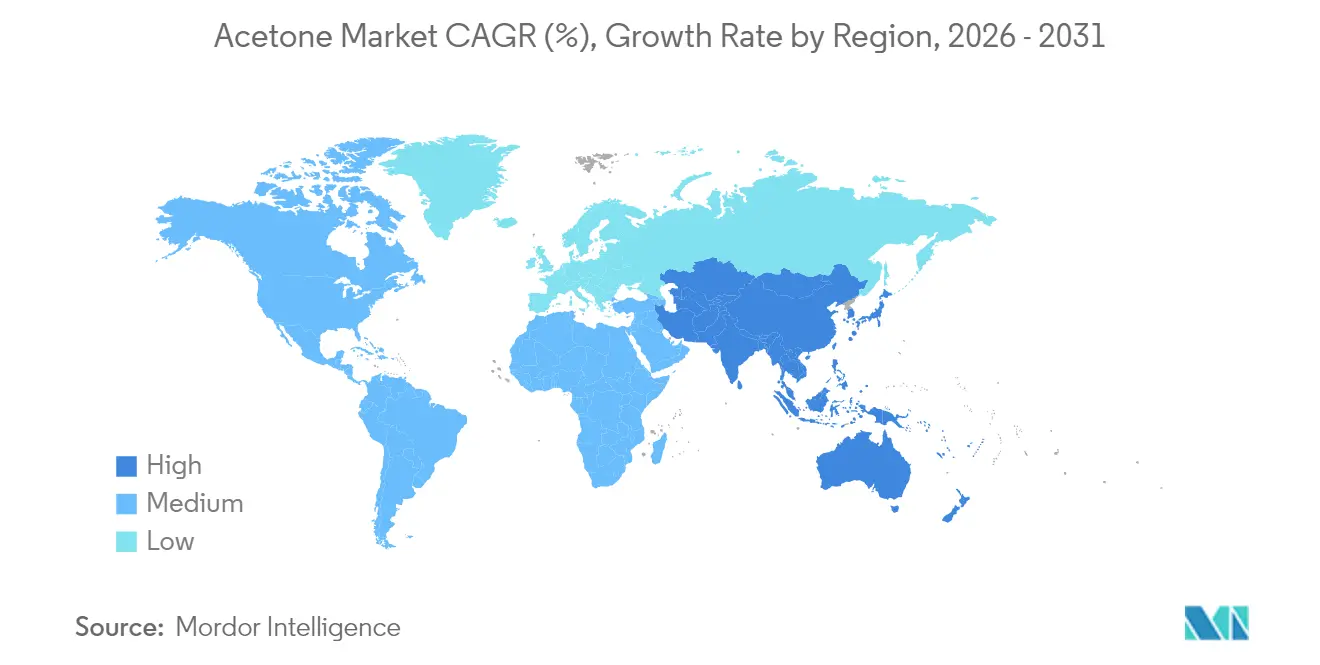

- By geography, Asia Pacific captured 42.18% of global sales in 2025 and is poised to grow at a 7.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acetone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for MMA-based acrylic sheets in EV light-weighting | +1.80% | Global, with concentration in China, North America, and Europe | Medium term (2-4 years) |

| Rising polycarbonate consumption in consumer electronics | +0.90% | Asia Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Expansion of personal-care solvent demand in Southeast Asia | +0.70% | Southeast Asia, with early gains in Thailand, Vietnam, and Indonesia | Medium term (2-4 years) |

| Growing pharmaceutical API solvent requirements post-COVID | +0.60% | Global, with emphasis on India, China, and North America | Long term (≥ 4 years) |

| Bio-acetone cost parity via waste-glycerol fermentation | +0.50% | North America and Europe, with pilot projects in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for MMA-Based Acrylic Sheets in EV Lightweighting

Electric vehicle makers are replacing glass and metal with MMA-based acrylic sheets to cut curb weight, which multiplies acetone demand because MMA consumes roughly 0.5 pounds of acetone per pound produced. The average North American auto contained USD 4,371 worth of chemistry in 2023, underscoring the material intensity of modern vehicles[1]American Chemistry Council, “2023 Automotive Chemicals Economic Impact,” americanchemistry.com . Stricter CAFE fuel-economy rules heighten the appeal of acrylic glazing over heavier substrates. Mitsubishi Chemical Group has advanced microwave-assisted PMMA recycling, creating a closed-loop premium that further strengthens downstream pull on the acetone market.

Expansion of Personal-Care Solvent Demand in Southeast Asia

Rising incomes and urbanization in Southeast Asia are reshaping beauty routines, making acetone a preferred solvent for nail polish removers and cosmetic blends. The chemical’s rapid evaporation and low dermal irritation suit premium formulations. Local producers capitalize on acetone’s VOC-exempt status, avoiding the stricter emission fees faced by alternative solvents and enhancing cost competitiveness across Thailand, Vietnam, and Indonesia.

Growing Pharmaceutical API Solvent Requirements Post-COVID

API manufacturers have built new capacity to secure supply resilience after COVID-19. Acetone’s high purity and established pharmacopeia listings make it a go-to crystallization medium. Its low boiling point allows efficient solvent recovery, cutting waste and aligning with sustainability targets. Regulatory adoption of process analytical technology (PAT) favors solvents with robust data packages, boosting demand for pharmaceutical-grade acetone.

Bio-Acetone Cost Parity via Waste-Glycerol Fermentation

Waste glycerol streams from biodiesel are now purified to over 80% glycerol, enabling cost-effective fermentation toward acetone at near-parity with petro-routes. LanzaTech’s carbon-negative pathway reports greater than 99% recovery and high-purity output, offering scope to displace cumene feed entirely. Policy signals such as the US target to source 30% of chemicals from biomanufacturing by 2040 underpin long-term scale-up opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening BPA regulations by EU & ECHA | -0.80% | Europe, with potential spillover to North America and Asia Pacific | Short term (≤ 2 years) |

| Refinery closures curbing cumene feedstock supply | -0.40% | North America and Europe, with secondary impacts in Asia Pacific | Medium term (2-4 years) |

| Emerging VOC limits on solvent use | -0.30% | Global, with stricter implementation in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening BPA Regulations by EU & ECHA

The EU enforced broad BPA restrictions in January 2025 for food-contact articles, reducing phenol-acetone co-production volumes and removing a notable outlet for acetone in Europe. Producers must pivot to MMA, solvents, or bio-routes to cushion the demand gap. Parallel debates in North America and parts of Asia may duplicate regulatory limits, compounding pressure on cumene-based operations.

Emerging VOC Limits on Solvent Use

While acetone is VOC-exempt under most rules, evolving aerosol and petro-facility standards create layered compliance duties for formulators. The EPA pushed back new aerosol coating VOC thresholds to January 2027 to refine test protocols[2]Federal Register, “National Volatile Organic Compound Emission Standards for Aerosol Coatings,” federalregister.gov . Canada forecasts 488,000 t cumulative VOC cuts from oil facilities by 2045, costing industry USD 1.2 billion[3]Government of Canada, “Regulations Respecting Reductions in the Release of Volatile Organic Compounds,” canada.ca . Downstream users invest in closed-loop emissions systems, raising capital hurdles for small firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Solvents Sustain Leadership while MMA Accelerates

Solvents held 42.82% of 2025 revenues, supported by acetone’s rapid evaporation and exemption from most VOC caps, especially in paints and adhesives. MMA is the fastest riser at 7.12% CAGR as acrylic glazing replaces glass in electric vehicles and construction. The bisphenol A segment faces regulatory drag, yet consumer electronics sustain some BPA volume through polycarbonate use. Methyl isobutyl ketone and specialty intermediates provide niche growth by leveraging acetone’s versatile reactivity.

Supply-side changes are equally stark. Automotive lightweighting magnifies MMA pull, whereas microwave PMMA recycling from Mitsubishi Chemical Group creates circular demand loops that lengthen acetone market opportunity windows. Solvent blenders prize acetone for miscibility across polarities, permitting lower VOC coatings that meet tougher emission caps without costly reformulation. Overall, application mix diversification shields the acetone market from single-segment shocks even as BPA curbs unfold.

By End-Use Industry: Personal Care Outpaces Established Segments

Paints, coatings, and adhesives consumed 37.35% of acetone in 2025 due to broad industrial adoption, yet cosmetics and personal care post the highest 6.95% CAGR to 2031. Southeast Asia’s rising middle class fuels nail polish and skincare volumes, where acetone’s low irritation profile is prized. Electronic devices channel acetone through polycarbonate resins, locking in stable demand. Automotive applications grow through MMA-based acrylic panels, while pharmaceuticals expand alongside new API plants in Asia.

Stable demand diversity bolsters resilience. Personal care formulators exploit acetone’s dual miscibility to pair water and oil actives in a single product, raising formulation flexibility. In North America and Europe, professional salon chains adopt acetone-rich removers that cut service times, boosting repeat purchase cycles. Industrial end users maintain baseline volume through architectural coatings that need fast dry times.

By Production Process: Fermentation Chips Away at Cumene Dominance

The cumene route supplied 82.95% of global output in 2025 by leveraging mature integration with phenol units. Fermentation methods, however, grow at 7.92% CAGR on the back of waste glycerol and syngas substrates. Isopropanol oxidation offers balancing flexibility for companies that already manufacture IPA, while direct propylene oxidation is pursued in technology pilots but remains niche.

INEOS deployed a heat-integrated design at its Marl complex to slice emissions in half compared to prior cumene benchmarks. In contrast, LanzaTech’s waste-gas fermentation delivers carbon-negative acetone at greater than 99% recovery, signaling the scale-up path for bio-routes. Policy incentives and consumer demand for low-carbon products imply a gradual realignment of the acetone market toward mixed feedstock portfolios.

By Grade: Pharmaceutical Purity Commands Premium Margins

Technical grade product met 93.85% of 2025 demand given its cost advantage in coatings, inks, and construction. Pharmaceutical grade expands at 7.45% CAGR as India and China add API reactors that rely on high-purity solvents. Reagent and analytical grades represent small but stable outlets tied to research spending.

API facilities favor acetone because it leaves minimal residues and allows efficient solvent recovery, aligning with green chemistry metrics. Continuous-flow reactors intensify throughput, and acetone’s predictable boiling point supports steady-state operation without equipment corrosion. Upgraded distillation trains let operators recycle acetone multiple cycles, amplifying effective supply without proportional raw material intake.

Geography Analysis

Asia Pacific captured 42.18% of 2025 volume owing to China’s vast phenol–acetone and BPA base and Southeast Asia’s expanding niche chemicals clusters. The region is projected to post a 7.25% CAGR to 2031 as local demand outstrips OECD growth. Government chemical industry roadmaps emphasize self-sufficiency and higher value products, steering capital into integrated refineries that can toggle between fuels and petrochemicals amid margin swings. China processed 14.8 million b/d of crude in 2023, underscoring feedstock availability for downstream acetone units.

North America enjoys a strong automotive and aerospace lightweighting pull, although refinery closures narrow the propylene supply for cumene. Europe faces the sharpest regulatory scrutiny on BPA but offsets some volume loss through sustainable production investments. INEOS’s Marl facility exemplifies strategy that pairs feedstock control with carbon-cuts to future-proof acetone supply.

South America’s industrialization, especially in Brazil, invites new imports as local capacity remains limited. State incentives to build chemical parks around ethanol feedstocks could spur fermentation projects over the forecast period. In the Middle East and Africa, low-cost naphtha and LPG underpin greenfield petrochemical complexes that include phenol–acetone integration, providing export-oriented supply but limited domestic pull.

Competitive Landscape

The acetone market displays moderately consolidated concentration. BASF, INEOS, and Mitsui Chemicals anchor global supply with integration from cumene through downstream acrylic monomers. BASF introduced bio-based ethyl acrylate with 40% certified bio content to capture premium demand for sustainable ingredients. INEOS expanded capacity by 750 kt of cumene in Germany while shrinking facility emissions through energy integration.

Start-ups such as LanzaTech add competitive tension by offering carbon-negative bio-acetone using waste gases at an industrial scale. M&A appetite cooled in 2024, yet nearly half of chemical executives plan to accelerate dealmaking to secure specialty assets and green technologies. Pharmaceutical-grade solvent supply and bio-feedstock platforms remain sought-after targets.

Technology innovation centers on circularity. Mitsubishi Chemical Group’s PMMA recycling recovers monomer feed that loops back to acetone-derived MMA, creating cradle-to-cradle pull on supply. Process optimizations such as advanced heat integration, improved catalysts, and closed-loop solvent management bolster cost positions while ensuring regulatory compliance, sustaining incumbent leadership even as new entrants chip away at margins.

Acetone Industry Leaders

BASF SE

INEOS

Mitsui Chemicals Inc.

Moeve

Formosa Chemicals & Fibre Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Deepak Nitrite Limited (Deepak) has approved a project to manufacture 185 KTA of Acetone, in addition to other chemicals. This capacity will be in addition to the existing 200 KTA produced by its wholly-owned subsidiary, Deepak Phenolics Limited.

- April 2023: INEOS Phenol has successfully acquired Mitsui Phenols Singapore Ltd. This acquisition encompasses the complete asset portfolio of Mitsui Phenols located on Jurong Island, Singapore. With this deal, INEOS adds over 1 million tonnes of annual capacity, which includes 185 ktpa of acetone, alongside a range of other chemicals.

Global Acetone Market Report Scope

Acetone, also known as dimethyl ketone or propanone, is a highly volatile, colorless, and flammable liquid with the chemical formula (CH3)2CO. It is the smallest and simplest ketone that is regularly used for cleaning in households, commercial operations, and laboratories. The market is segmented into application, end-user industry, and geography. By application, the market is segmented into methyl methacrylate, bisphenol A, solvents, methyl isobutyl ketone, and other applications. By end-user industry, the market is segmented into cosmetics and personal care, electronics, automotive, pharmaceutical, paints, coatings and adhesives, textile industry, and other end-user industries. The report also covers the market size and forecasts for the acetone market in 15 countries across major regions. The market sizing and forecasts for each segment have been done based on volume (kilo tons).

| Methyl Methacrylate (MMA) |

| Bisphenol A (BPA) |

| Solvents |

| Methyl Isobutyl Ketone (MIBK) |

| Other Applications (Chemical Intermediates) |

| Cosmetics and Personal Care |

| Electronics |

| Automotive |

| Pharmaceutical |

| Paints, Coatings and Adhesives |

| Textile |

| Other End-user Industry (Plastics) |

| Cumene Process |

| Isopropanol Oxidation |

| Direct Propylene Oxidation |

| Bio-based Fermentation |

| Technical Grade |

| Pharmaceutical Grade |

| Reagent/Analytical Grade |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of APAC | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Methyl Methacrylate (MMA) | |

| Bisphenol A (BPA) | ||

| Solvents | ||

| Methyl Isobutyl Ketone (MIBK) | ||

| Other Applications (Chemical Intermediates) | ||

| By End-Use Industry | Cosmetics and Personal Care | |

| Electronics | ||

| Automotive | ||

| Pharmaceutical | ||

| Paints, Coatings and Adhesives | ||

| Textile | ||

| Other End-user Industry (Plastics) | ||

| By Production Process | Cumene Process | |

| Isopropanol Oxidation | ||

| Direct Propylene Oxidation | ||

| Bio-based Fermentation | ||

| By Grade | Technical Grade | |

| Pharmaceutical Grade | ||

| Reagent/Analytical Grade | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of APAC | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the acetone market?

The acetone market is valued at USD 7.71 billion in 2026 and is projected to reach USD 10.6 billion by 2031.

Which application segment is growing fastest?

Methyl methacrylate applications lead growth, registering a 7.12% CAGR to 2031 due to electric vehicle lightweighting needs.

Why is Asia Pacific dominant in acetone demand?

Asia Pacific holds 42.18% of global volume because of China’s large phenol–acetone base and rapid industrial expansion in Southeast Asia.

How are bio-fermentation routes impacting supply?

Bio-acetone from waste glycerol and syngas is growing at 7.92% CAGR, offering carbon-negative profiles and reducing reliance on cumene.

Which grade of acetone sees the highest premium?

Pharmaceutical grade commands premium pricing and is expanding at 7.45% CAGR due to strict purity requirements in API manufacturing.

Page last updated on: