Abdominal Aortic Aneurysm (AAA) Repair Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3 Billion |

| Market Size (2031) | USD 3.99 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

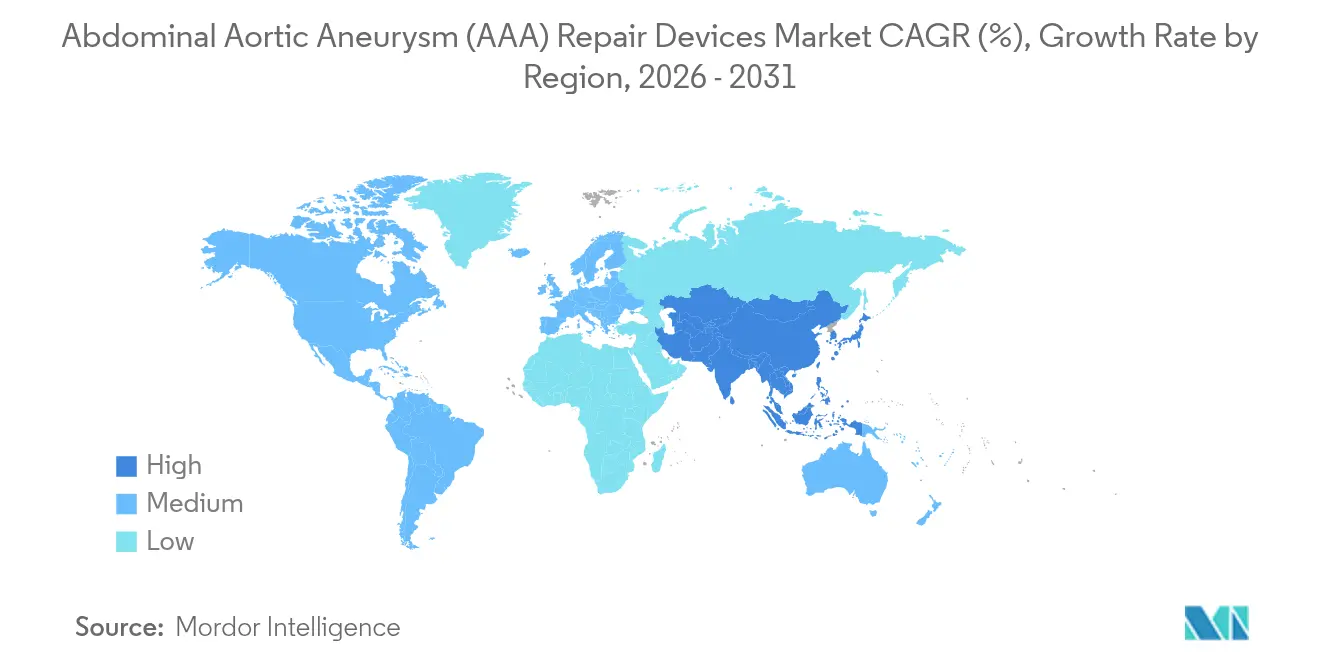

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

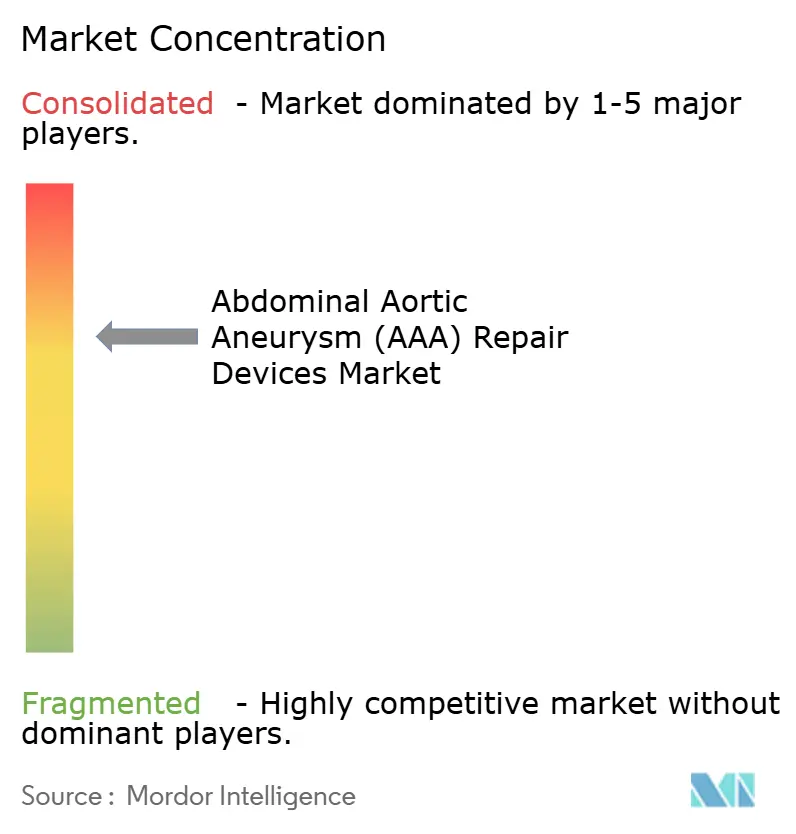

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Abdominal Aortic Aneurysm (AAA) Repair Devices Market Analysis by Mordor Intelligence

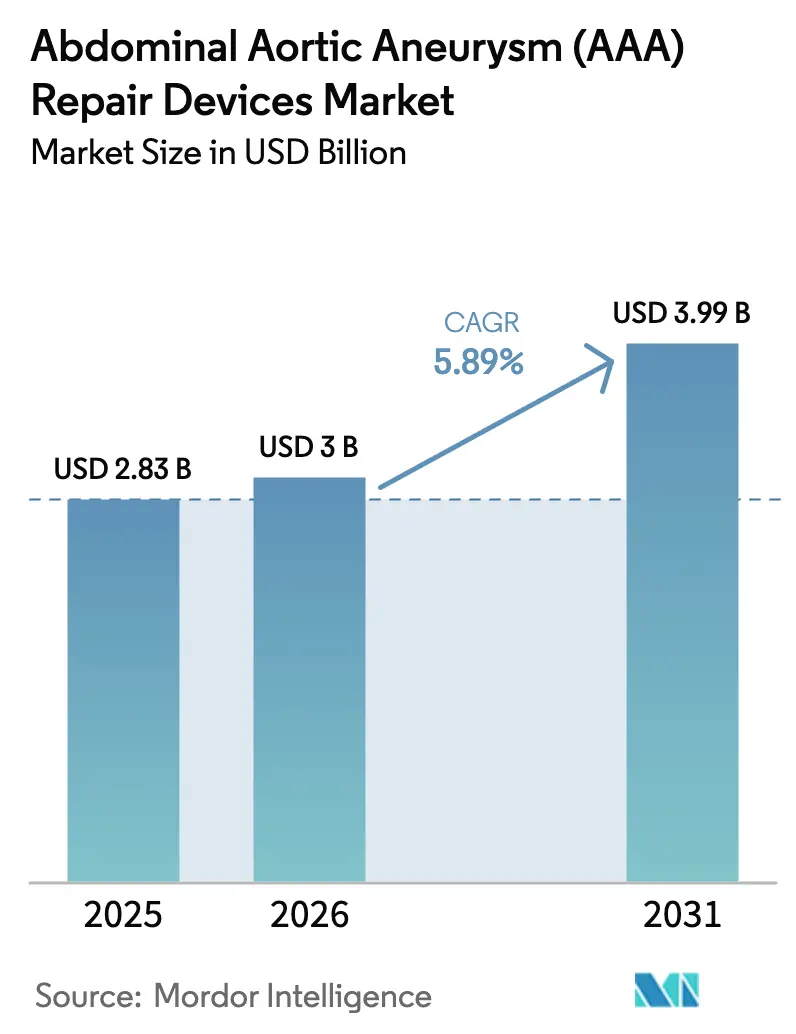

The Abdominal Aortic Aneurysm Repair Devices market size is expected to grow from USD 2.83 billion in 2025 to USD 3 billion in 2026 and is forecast to reach USD 3.99 billion by 2031 at 5.89% CAGR over 2026-2031. Steady growth reflects rising AAA prevalence among ageing, largely male smokers, the rapid mainstreaming of minimally invasive endovascular aneurysm repair (EVAR), and continuous device innovation focused on challenging anatomies. Hospitals still perform most repairs, but outpatient centres are gathering momentum as reimbursement shifts reward same-day discharge. North America retains the largest revenue share, yet Asia-Pacific is growing fastest as screening capacity, specialist training, and middle-class insurance coverage improve. Competitive intensity is increasing as integrated procedural ecosystems, covering planning software, advanced imaging, and post-repair monitoring, overtake stand-alone graft specifications as the primary purchase criteria.

Key Report Takeaways

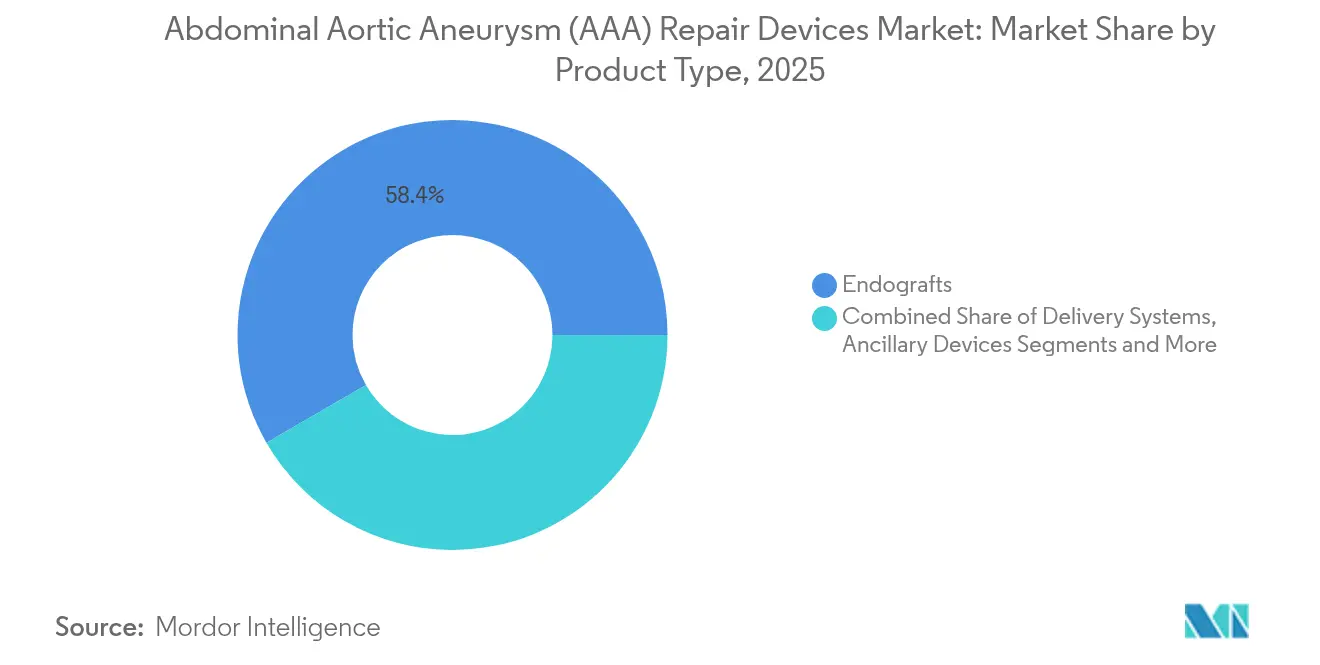

- By product type, endografts held 58.35% of abdominal aortic aneurysm repair devices market share in 2025, whereas delivery systems are projected to grow at a 6.46% CAGR through 2031.

- By procedure type, EVAR commanded 69.55% of abdominal aortic aneurysm repair devices market share in 2025 and is advancing at a 6.55% CAGR to 2031.

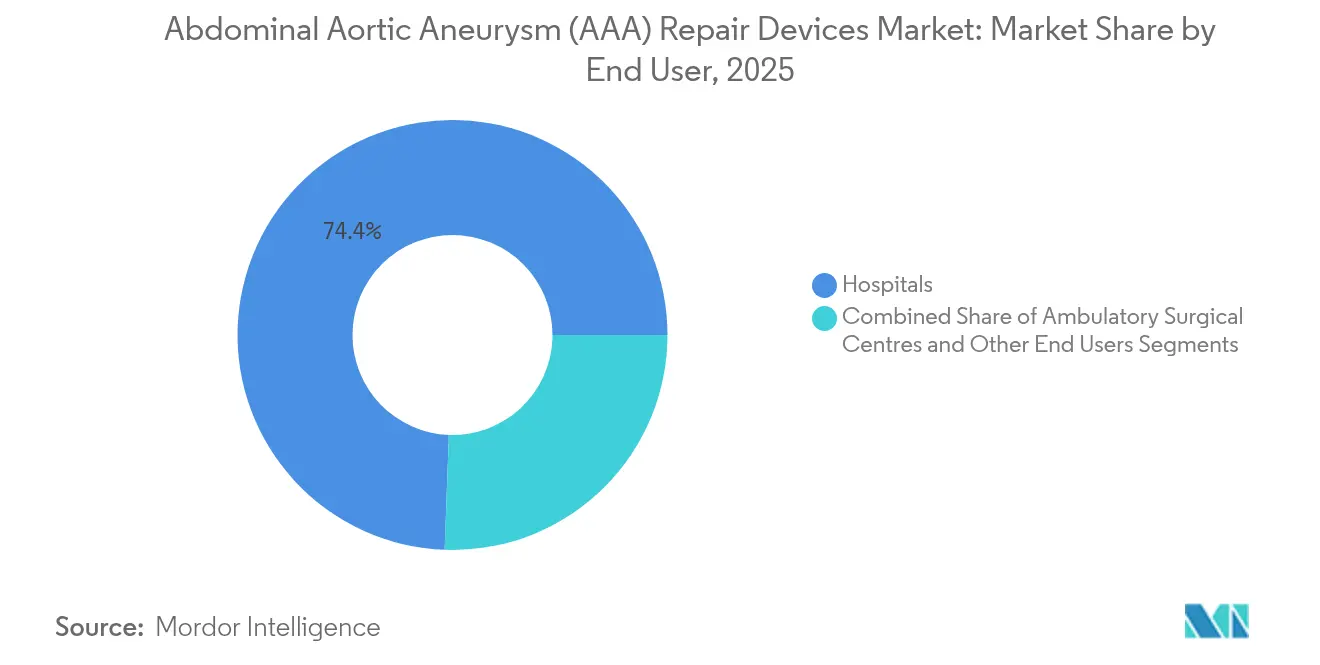

- By end user, hospitals accounted for 74.42% of the abdominal aortic aneurysm repair devices market size in 2025, while ambulatory surgical centres are forecast to expand at a 6.98% CAGR through 2031.

- By anatomy, infrarenal repairs represented 78.66% of abdominal aortic aneurysm repair devices market share in 2025; pararenal repairs are growing at 6.18% CAGR through 2031.

- By geography, North America led with 39.78% revenue share in 2025, whereas Asia-Pacific is projected to post a 6.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Abdominal Aortic Aneurysm (AAA) Repair Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of AAA In Ageing Smokers | +1.0% | North America & Europe | Long term (≥ 4 years) |

| Rapid Adoption of Minimally Invasive EVAR | +0.8% | Global, led by developed markets | Medium term (2–4 years) |

| Expansion of Organised Ultrasound Screening | +0.6% | North America, EU, expanding to Asia-Pacific | Medium term (2–4 years) |

| Continuous Device Innovations | +0.4% | Global, early uptake in developed economies | Short term (≤ 2 years) |

| AI-Based Anatomical Planning Improving Procedural Success | +0.3% | North America & EU, selective APAC markets | Short term (≤ 2 years) |

| 3-D-Printed, Patient-Specific Endografts Moving from Pilot to Market | +0.2% | North America & EU, limited global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of AAA in Ageing, Smoking Populations

Decades of high tobacco intake are surfacing as AAA diagnoses within the post-retirement male cohort, especially in Nordic and North American settings where historical smoking peaked earliest. Improved cardiac care is extending life expectancy, revealing aneurysms that would previously have gone undetected. Health systems now recognise that elective repair is far cheaper than emergency rupture management, prompting broader ultrasound outreach beyond traditional high-risk profiles. Uptake differs by socioeconomic status, with rural and low-income groups less likely to attend screening despite higher disease burden. As cohorts age, payer pressure grows to fund programmes that avert catastrophic bleeds and costly intensive-care admissions.

Rapid Adoption of Minimally Invasive EVAR Procedures

EVAR delivers lower peri-operative mortality and shorter stays, making it the preferred option for frail, multi-morbid patients. Fee-for-service markets such as the United States show higher EVAR penetration than capitated systems, underscoring the influence of reimbursement design. Device makers are extending indications to hostile necks and pararenal sacs, enlarging the addressable pool. Broader eligibility lifts procedural volume, but it also shifts competition toward solutions that minimise fluoroscopy, reduce adjunctive embolisation steps, and fit outpatient discharge pathways. Hospitals are rewriting protocols so that uncomplicated infrarenal repairs exit within 23 hours, freeing beds and labour.

Expansion of Organised Ultrasound Screening Programmes

National initiatives build on evidence that systematic screening yields cost-effectiveness ratios exceeding 10:1 compared with rupture care. The United Kingdom’s single-payer model is a template, yet participation remains uneven because travel distance and workforce gaps restrict scanning capacity. Artificial-intelligence augmentation now guides technicians in real time, reducing physician workload and enabling satellite clinics in underserved regions. Emerging Asian markets benefit most because specialist vascular surgeons are scarce, yet smartphone-linked portable probes allow rapid population coverage. Wider detection feeds a predictable pipeline of elective repairs, smoothing theatre scheduling and supporting ambulatory migration.

Continuous Device Innovations (Polymer-Sealing, Branched/Fenestrated Grafts)

Shifting from barbed stents to polymer-sealed rings allows customised conformity to irregular aortic necks, cutting Type I endoleak risk. Branched and fenestrated grafts open pararenal and thoracoabdominal segments that conventional EVAR could not treat, pushing clinical success above 95% in complex anatomies. Early adopters in the United States and Germany are blending software-guided sizing with on-table adjunctive relining to boost first-time seal. While bespoke builds raise manufacturing cost, longer durability and lower secondary-intervention rates appeal to value-based purchasers. Regulatory approval remains stringent, favouring incumbents able to fund multi-year registries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure and Implant Costs in LMICs | –0.7% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Stringent Regulatory and Post-Market Obligations | –0.5% | North America & Europe | Medium term (2–4 years) |

| Persistent Long-Term Durability Doubts | -0.4% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Supply-Chain Shortage of Medical-Grade PET/ePTFE Yarns | -0.3% | Global, with manufacturing concentration in Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure & Implant Costs Limit Adoption in LMICs

Endograft kits can cost 2–3 times open repair, placing EVAR beyond most public insurers in low- and middle-income economies.[1]Source: World Bank, “Essential Surgery: Key Messages of This Volume,” documents1.worldbank.org Attempts at price caps have prompted some suppliers to pull products, shrinking choice and raising black-market reuse concerns. Surgeons continue to perform open repairs despite higher morbidity because disposables are cheaper and widely available. Philanthropic partnerships now trial domestic graft production in India and Brazil to localise supply, yet questions persist around long-term polymer stability and surveillance infrastructure.

Stringent Regulatory Proof & Post-Market Surveillance Requirements

Device withdrawals, such as the Nellix sealing system, have tightened approval gates, extending time-to-market by up to seven years for novel grafts. The FDA’s current policy mandates prolonged registries and unique device identifiers, raising compliance costs for smaller innovators.[2]Source: FDA, “Medical Device Supply Chain and Shortages,” fda.gov Equivalent scrutiny under Europe’s MDR further inflates testing budgets, slowing pipeline refresh and reinforcing incumbent dominance. Manufacturers are responding by integrating real-world evidence platforms that harvest computed tomography data automatically, but until harmonised frameworks emerge, regulatory drag will temper replacement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Progressive Delivery-System Engineering Fuels Differentiation

The endografts segment occupies 58.35% of abdominal aortic aneurysm repair devices market share, underscoring its central therapeutic role. Delivery-system revenue, though smaller, is climbing at a 6.46% CAGR as physicians demand catheters with finer profile, enhanced torque, and positional accuracy that cut fluoroscopy minutes. The abdominal aortic aneurysm repair devices market size attached to delivery systems is therefore expanding faster than graft sales, indicating that procedural efficiency, not just sealing reliability, now drives purchasing decisions. Medtronic and W.L. Gore continue to refine nitinol stent frameworks, but challengers focus on hydrophilic-coated sheaths and steerable tips optimised for tortuous iliac routes. Hospitals value kits combining graft and catheter in a single stock-keeping unit to simplify pharmacy coding, creating cross-selling leverage for integrated suppliers.

Supply constraints around medical-grade ePTFE yarn elevate production cost, compelling firms to scout alternative fluoropolymer sources that meet burst-strength specs. Ancillary devices—balloons, snares, embolisation coils—represent a modest but resilient slice because every EVAR requires adjunctive consumables. Although the absolute abdominal aortic aneurysm repair devices market size for ancillary tools is smaller, high procedure volume secures stable cash flow. Future growth will likely hinge on all-in-one EVAR platforms bundling imaging, graft, and closure technology.

By Procedure Type: EVAR Entrenched as Default, Open Repair Reserved for Niche Indications

EVAR accounts for 69.55% of procedures and is expanding at 6.55% CAGR, reflecting its entrenchment as preferred therapy. Risk-adjusted survival gains, coupled with shorter postoperative recovery, solidify its lead among patients aged over 70. The abdominal aortic aneurysm repair devices market benefits because each EVAR utilises a premium graft kit alongside imaging and closure accessories, magnifying per-case revenue. Open surgical repair remains critical for younger or low-neck-angle patients where graft fatigue poses long-horizon failure risk. Centres with high open-volume capacity retain expertise, but many community hospitals now lack sufficient caseload to keep teams credentialed, funnelling complex open cases into regional hubs.

Reimbursement parity policies in Canada, the UK, and Australia aim to ensure that EVAR selection remains clinically justified rather than financially motivated, yet data show continued EVAR expansion as device profiles slim and instructions-for-use broaden. Secondary procedures such as endoleak relining still occur in 10-20% of cases, sustaining aftermarket demand for extension cuffs and occlusion plugs. Artificial-intelligence-guided stent sizing is reducing this rate, but longitudinal CT follow-up remains a mandated cost in guidelines.

By End User: Outpatient Centres Accelerate but Hospitals Retain Complex Case Mix

Hospitals generate 74.42% of 2025 revenue thanks to critical care support, hybrid theatres, and stock management for multi-size graft inventories. Nevertheless, same-day EVAR protocols enable ambulatory surgical centres (ASCs) to log 6.98% CAGR. Payers endorse ASCs because average EVAR cost drops by USD 2,500 per patient, equating to projected Medicare savings of USD 2.95 billion by 2028. Device makers respond with shorter sheaths and integrated closure patches that reduce haemostasis time, optimising throughput.

In the abdominal aortic aneurysm repair devices market, industry players view ASCs as strategic channels to penetrate previously underserved suburban zones, yet complex pararenal cases still funnel to tertiary centres equipped for advanced imaging. Hybrid operating rooms within university hospitals blur lines by offering outpatient scheduling flexibility while retaining cardiopulmonary bypass backup. Over the forecast horizon, device vendors will need dual-path portfolios, balancing cost-efficient kits for ASC skid-rails with multi-module, custom-fenestrated systems for academic users.

By Anatomy: Pararenal Segment Emerges as Value Driver

Infrarenal disease represents 78.66% of treated aneurysms today, an historical consequence of anatomical favourability and mature device ecosystems. The segment’s growth has plateaued, yet its absolute abdominal aortic aneurysm repair devices market size continues to dominate. Pararenal repairs, however, are advancing at 6.18% CAGR because branched and fenestrated grafts now preserve visceral flow while sealing proximally. Each pararenal case uses additional stents, raising average selling price by 35–40% compared with infrarenal EVAR Journal of Endovascular Therapy. Hospitals increasingly batch-order custom devices, creating logistic challenges related to just-in-time manufacture and patient scheduling.

Long-term data indicate comparable survival to open debranching, shifting more surgeons toward endovascular options even for younger patients, provided that post-market durability concerns resolve through polymer or expandable-ring advances. As 3-D-printed, patient-specific devices exit pilot phase, the pararenal share of abdominal aortic aneurysm repair devices market revenue will likely rise faster than case volumes.

Geography Analysis

North America anchors 39.78% of global sales, fuelled by universal ultrasound screening of men aged 65 plus and near-ubiquitous insurance cover for elective EVAR. The United States exhibits EVAR penetration of roughly 79% across all repairs, while Canada’s single-payer system emphasises cost-effectiveness yet still adopts EVAR for comorbidity-laden seniors. Academic centres now pilot AI-guided planning workstations, integrating computed tomography flow analytics that trim operating time by up to 20%.

Europe’s publicly funded structure yields high screening uptake in Scandinavia, contrasting with lower participation in southern states where health budgets prioritise acute coronary syndromes. The abdominal aortic aneurysm repair devices market size in Europe remains substantial, yet austerity measures compel negotiated device price caps and value dossiers before reimbursement clearance. Post-Brexit regulatory divergence introduces uncertainty over UK market access timelines. Meanwhile, the continent pioneers post-market registries; Germany and the Netherlands pool real-world EVAR outcomes, informing procurement policies that reward devices with lower re-intervention curves.

Asia-Pacific records the fastest CAGR at 6.86%, though starting from lower per-capita uptake. China’s top tier hospitals now perform over 12,000 EVARs annually, yet penetration across 1.4 billion citizens remains modest. India’s mix of public and self-pay means open repair still dominates outside metro hubs, but insurance expansion is lifting elective EVAR referrals. Japanese adopters demand strong durability data before switching from open repair, slowing adoption despite mature catheter infrastructure. Regional suppliers such as MicroPort tailor budget grafts to local anatomies, carving share against Western incumbents.

Competitive Landscape

The abdominal aortic aneurysm repair devices market shows moderate consolidation: Medtronic, W.L. Gore, and Cook Medical collectively hold a substantial share through broad endograft catalogues, robust clinical data, and field technical teams. Competitive differentiation is migrating from metallic framework tweaks toward ecosystem offerings comprising 3-D planning software, precision delivery sheaths, and remote case support. Medtronic’s polymer-based sealing platform, W.L. Gore’s conformable nitinol neck rings, and Cook’s fenestrated line underpin their leadership, yet each invests heavily in AI analytics to lock in surgeon loyalty.

Disruptors such as Endologix and Artivion target niches: polymer-sealing for extremely short necks and branched-arch grafts for thoracoabdominal disease, respectively. Regulatory hurdles and post-market data requirements temper their speed, but strategic partnerships such as Endologix's licensing to regional distributors broaden reach. Asian entrant MicroPort leverages domestic manufacturing cost advantage and state procurement quotas to win Chinese tenders, although global expansion depends on meeting MDR and FDA documentation demands.

Supply-chain fragility remains a shared concern. The pandemic exposed dependency on a handful of polytetrafluoroethylene yarn suppliers concentrated in East Asia. Manufacturers now dual-source critical polymers and consider vertical integration. At the same time, payers pivot toward outcome-based contracts that reimburse only when freedom-from-re-intervention thresholds are met, shifting product liability risks onto device makers and further favouring firms able to finance longitudinal registries.

Abdominal Aortic Aneurysm (AAA) Repair Devices Industry Leaders

Medtronic Plc

Cook Medical Inc.

MicroPort Scientific Corporation

W. L. Gore & Associates, Inc. (Gore Medical)

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Artivion amended agreements with Endospan to expand debt funding for the NEXUS branched stent-graft system, the first device approved specifically for aortic-arch pathology that also spans abdominal segments.

- April 2024: The UK’s “Provision of Services for People with Vascular Disease 2024” report showed fewer than one-third of vascular units met the 8-week EVAR treatment target, highlighting operational bottlenecks.

- April 2024: Gore & Associates received FDA approval to expand the indication for its Excluder conformable abdominal aortic aneurysm (AAA) endoprosthesis. The endovascular aneurysm repair (EVAR) device can now be used for patients with aortic neck angulation up to 90 degrees and a minimum length of 10 millimeters.

Global Abdominal Aortic Aneurysm (AAA) Repair Devices Market Report Scope

As per the scope of the report, Abdominal Aortic Aneurysm (AAA) repair devices are used to treat and repair abdominal aortic aneurysms, which are bulges or enlargements in the abdominal aorta, the major blood vessel that supplies blood to the abdomen, pelvis, and legs.

The abdominal aortic aneurysm (AAA) repair devices market is segmented by product type, procedure type, end user, and geography. By product type, the market is segmented as endografts, delivery systems, and ancillary devices. By procedure type, the market is segmented as open surgical repair and endovascular aneurysm repair (EVAR). By end user, the market is segmented as hospitals, ambulatory surgical centers, and others. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Endografts |

| Delivery Systems |

| Ancillary Devices |

| Others |

| Open Surgical Repair |

| Endovascular Aneurysm Repair (EVAR) |

| Hospitals |

| Ambulatory Surgical Centres |

| Other End Users |

| Infrarenal AAA |

| Pararenal AAA |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Endografts | |

| Delivery Systems | ||

| Ancillary Devices | ||

| Others | ||

| By Procedure Type | Open Surgical Repair | |

| Endovascular Aneurysm Repair (EVAR) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Other End Users | ||

| By Anatomy | Infrarenal AAA | |

| Pararenal AAA | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current abdominal aortic aneurysm repair devices market size?

The market is valued at USD 3 billion in 2026 and is projected to rise to USD 3.99 billion by 2031.

How fast is the abdominal aortic aneurysm repair devices market growing?

It is expanding at a 5.89% CAGR over 2026-2031, driven by ageing demographics, rising screening uptake, and EVAR acceptance.

Which procedure dominates global AAA repair volumes?

EVAR represents 69.55% of all repairs and continues to grow at 6.55% CAGR as device innovations address complex anatomies.

Why are ambulatory surgical centres important for future growth?

ASCs enable same-day EVAR discharge, cutting payer costs by USD 2,500 per case and stimulating a 6.98% CAGR in this channel.

Which region offers the highest growth potential through 2031?

Asia-Pacific posts a 6.86% CAGR on expanding middle-class insurance coverage, improving specialist training, and broader screening.

What are the main barriers in low-income countries?

High device prices, limited screening infrastructure, and scarce post-operative surveillance resources constrain adoption of EVAR.

Page last updated on: