Trauma Fixation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

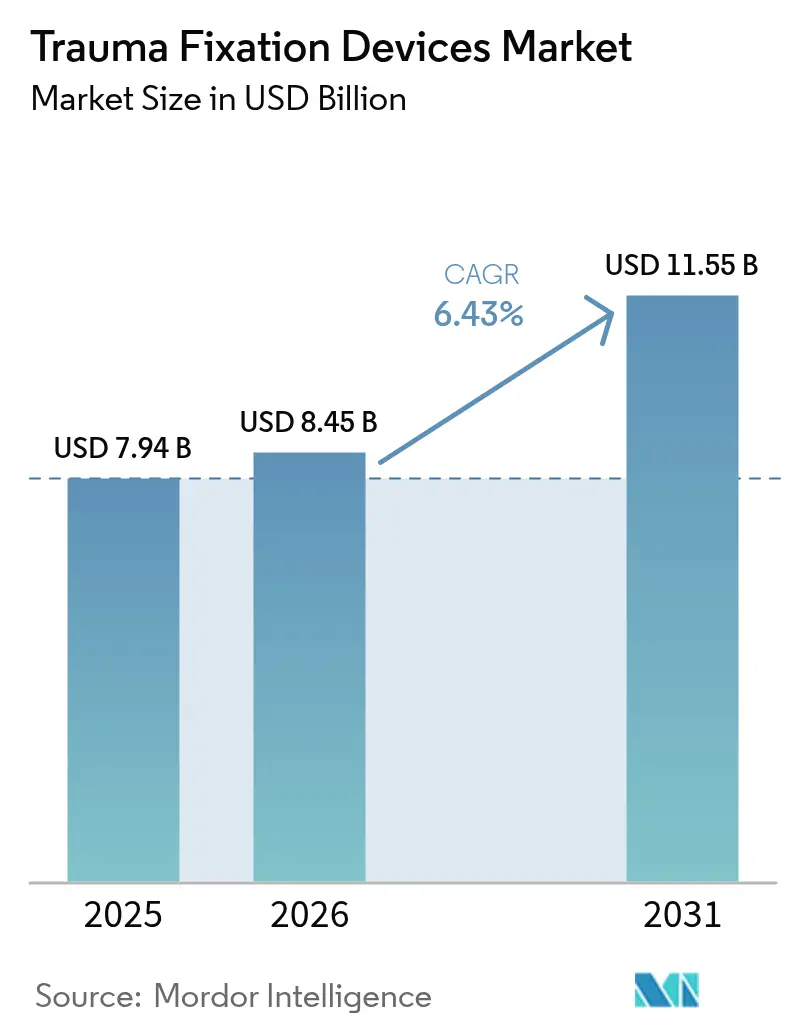

| Market Size (2026) | USD 8.45 Billion |

| Market Size (2031) | USD 11.55 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Trauma Fixation Devices Market Analysis by Mordor Intelligence

The trauma fixation devices market size is expected to grow from USD 7.94 billion in 2025 to USD 8.45 billion in 2026 and is forecast to reach USD 11.55 billion by 2031 at 6.43% CAGR over 2026-2031. Internal innovation in bioabsorbable metals, rapid adoption of drug-eluting plates and screws, and the growing preference for outpatient fracture care are the three strongest forces sustaining this momentum. Demographic pressures from osteoporosis, population ageing, and higher accident exposure in urban centers are widening the patient pool, while value-based reimbursement is shifting hospital purchasing toward implants that shorten length of stay and avert secondary removal surgery. Supply-chain risk in titanium and nitinol continues to create margin pressure but is simultaneously nudging manufacturers to explore novel alloy chemistries. Competitive strategies center on 3D-printed patient-specific hardware, antimicrobial coatings, and integrated digital surgery platforms that improve procedural speed and accuracy.

Key Report Takeaways

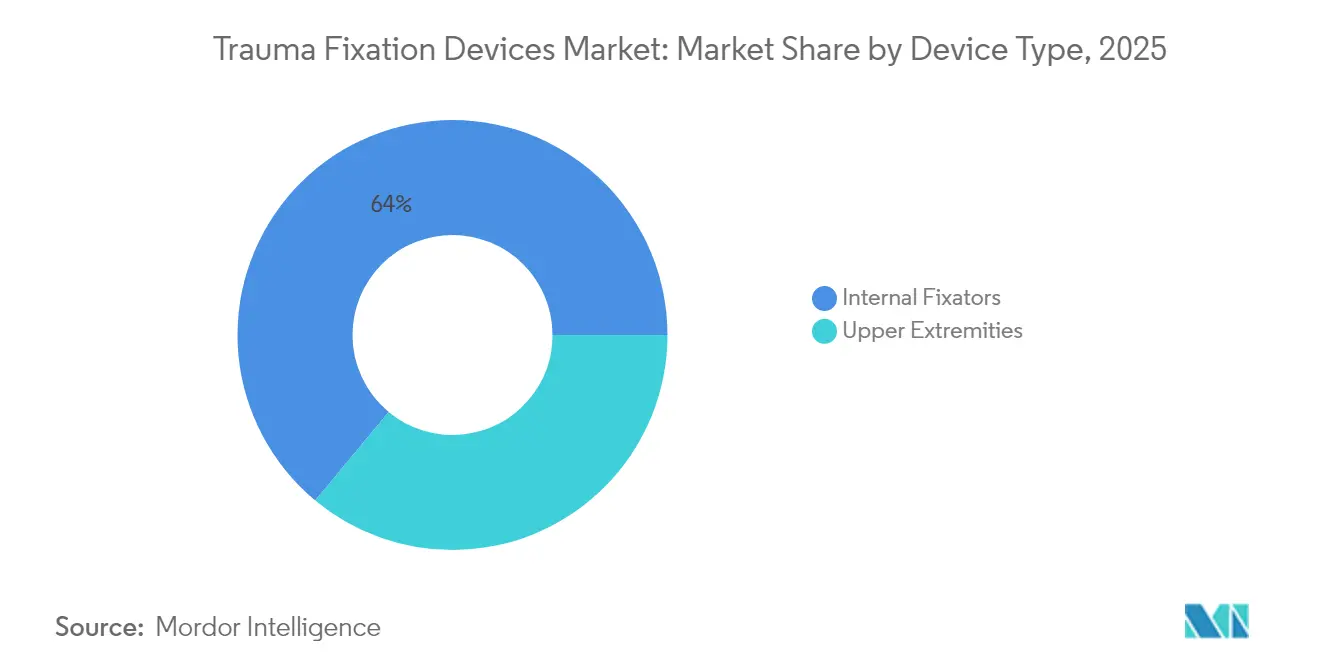

- By device type, internal fixators held 63.98% of trauma fixation devices market share in 2025 and are projected to grow at an 8.05% CAGR through 2031.

- By surgical site, upper extremities commanded 55.12% of the trauma fixation devices market size in 2025; lower extremities are set to expand at an 8.62% CAGR between 2026-2031.

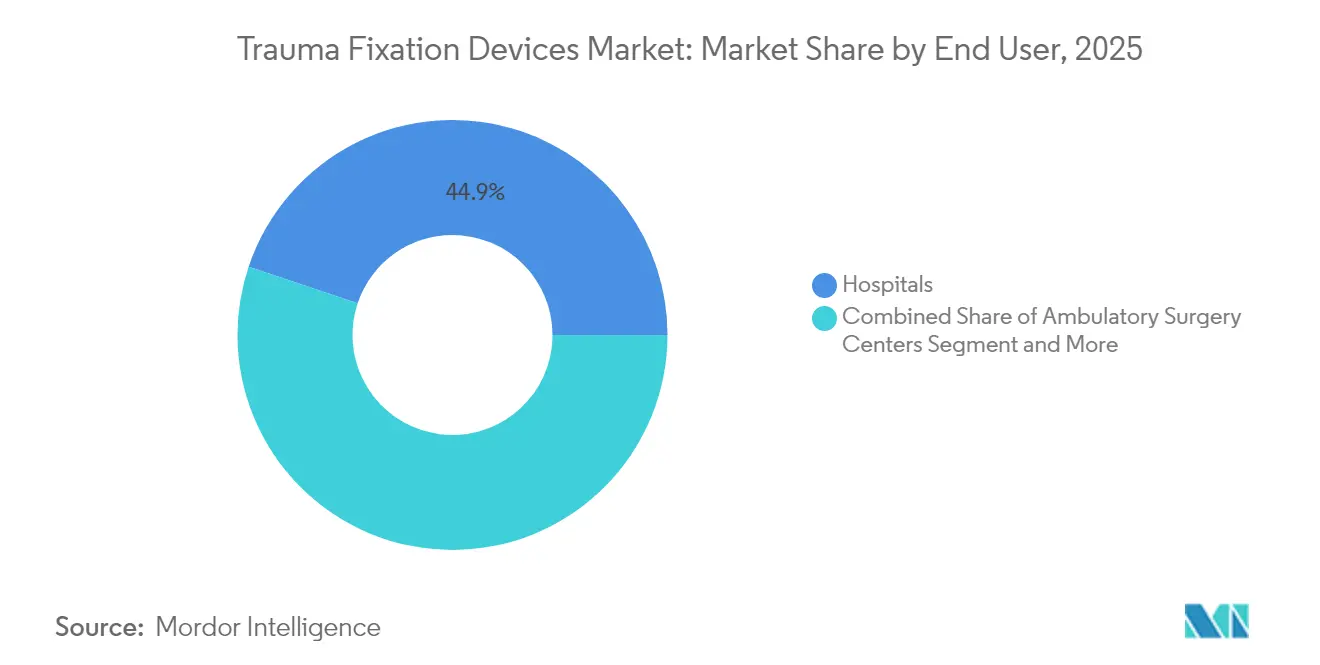

- By end user, hospitals captured 44.86% revenue in 2025, whereas ambulatory surgery centers will post the fastest 7.71% CAGR to 2031.

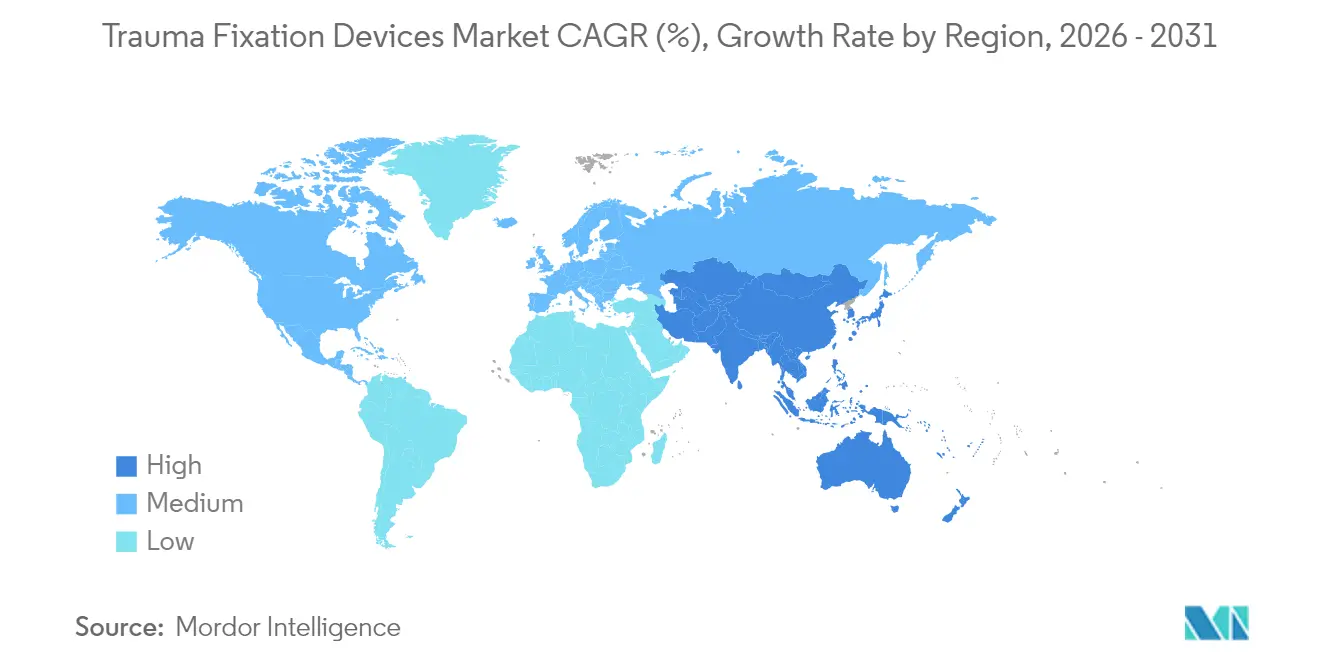

- By geography, North America led with a 39.05% slice of the market in 2025; Asia-Pacific is growing fastest at a 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Trauma Fixation Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of osteoporosis | +1.2% | North America & Europe | Long term (≥ 4 years) |

| Increasing road-traffic trauma | +0.8% | Asia-Pacific, spill-over to MEA | Medium term (2-4 years) |

| Growing geriatric population | +1.5% | Global, developed economies | Long term (≥ 4 years) |

| Advances in bioabsorbable materials | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Orthobiologic-enhanced fixation | +0.6% | North America & EU | Short term (≤ 2 years) |

| Modular reusable external fixators in EMs | +0.4% | APAC & MEA emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Bone-Degenerative Diseases & Osteoporosis

Global osteoporosis affects an estimated 500 million people and is reshaping demand for fixation solutions tailored to compromised bone quality[1]David Oldani, “Epidemiology of Osteoporosis and Fragility Fractures,” Osteoporosis Foundation, osteoporosis.foundation. Fragility fractures now drive hospital admissions that once stemmed from high-energy trauma, prompting device makers to integrate bone-building pharmaceuticals directly into screws and plates. Health systems in the United States incur annual fracture costs above USD 25 billion, forcing payers to fund preventive implants that avert refracture. Manufacturers are therefore racing to validate bioactive constructs that strengthen osseointegration while gradually off-loading stress to healing bone. The trend is most visible in North America and Europe where aging curves are steepest and reimbursement supports premium implants. Over the long term, this driver is expected to add 1.2 percentage points to the trauma fixation devices market CAGR.

Increasing Incidence of Road Traffic Accidents & Trauma Injuries

WHO records show injuries claim 4.4 million lives each year, with Asia-Pacific bearing the heaviest load as motorization outpaces safety infrastructure[2]World Health Organization, “Improving Care of the Injured,” who.int. Expanding urban sports cultures and industrial workplaces add further fracture complexity, demanding modular fixation systems capable of stabilizing multiple bones in a single session. Device makers are introducing integrated platforms that cut operating time and streamline inventory. In medium-term horizons, rising trauma exposure in India, China, and Southeast Asia injects 0.8 percentage points into the projected CAGR for the trauma fixation devices market.

Growing Geriatric Population Vulnerable to Fractures

People aged 65 and older form the fastest-growing trauma cohort, often presenting with comorbidities and polypharmacy that complicate fixation. Minimally invasive plate and nail systems now dominate geriatric protocols by limiting surgical trauma and blood loss. Payers focus on long-term outcomes over device list price, encouraging premium solutions that minimize revision risk. Over the long haul, the aging trend lifts the global trauma fixation devices market by roughly 1.5 percentage points in CAGR contribution.

Technological Advances in Bio-Compatible & Bio-Absorbable Fixation Materials

The 2024 FDA recognition of ASTM F2579-18 accelerated clearances for amorphous PLA and PLGA implants. Bioabsorbable metals, such as Bioretec’s RemeOs magnesium screw, eliminate the need for removal surgery, lowering infection and anesthesia risk. 3D-printing allows surgeons to match implant stiffness and geometry to each patient, while drug-loaded polymers actively promote bone growth. These developments pump an additional 0.9 percentage points into medium-term CAGR.

Restraints Impact Analysis of Trauma Fixation Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure and device costs | -0.7% | Global, strongest in emerging economies | Short term (≤ 2 years) |

| Time-consuming regulatory approvals | -0.5% | North America & EU | Medium term (2-4 years) |

| Supply-chain shortages in Ti & nitinol | -0.4% | Global, high-volume manufacturers | Short term (≤ 2 years) |

| Multidrug-resistant implant infections | -0.6% | Global, hospital settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure & Device Costs

Premium bioabsorbable and drug-eluting implants cost more up front, limiting uptake in lower-income settings. Bundled payments push hospitals and ambulatory centers to scrutinize total episode cost, often opting for modular systems that stretch inventory budgets. This cost friction shaves 0.7 percentage points off short-term trauma fixation devices market growth.

Rising Implant-Associated MDR-Infection Concerns

Biofilm-linked infections affect roughly 5% of orthopedic operations and can necessitate implant removal, extending hospital stays and raising litigation risk. XDR Klebsiella pneumoniae and MRSA outbreaks underscore the threat. Regulatory scrutiny of antimicrobial coatings remains stringent, delaying product launches. Combined, these pressures subtract 0.6 percentage points from medium-term CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Trauma Fixation Devices Market Segment Analysis

By Device Type:

Internal Fixators Sustain Leadership Through Absorbable Metal AdoptionInternal fixators generated 63.98% of trauma fixation devices market share in 2025, while their sub-segment is set to log an 8.05% CAGR to 2031, the fastest across all device categories. The trauma fixation devices market size attributed to internal fixators will thus outpace overall industry expansion as bioabsorbable screws gain traction in pediatrics and geriatrics. Plates equipped with dynamic compression slots permit controlled micromotion that encourages callus formation; Zimmer Biomet’s MotionLoc screw exemplifies this capability.

The advent of smart alloys and modular tray layouts lets surgeons adjust construct stiffness intraoperatively, cutting inventory by up to 30%. Drug-eluting coatings further differentiate internal hardware by merging mechanical support with biologic therapy. External fixators remain indispensable for complex open fractures and damage-control orthopedics, yet reimbursement pressures drive interest toward reusable frame kits that lower per-case expenditure. Together, these trends keep internal solutions ahead but invite continuous innovation to protect share.

By Surgical Site:

Upper Extremity Dominance Meets Lower Extremity SurgeUpper extremity procedures accounted for 55.12% of the trauma fixation devices market in 2025 owing to persistent wrist and shoulder injuries in sports, work, and domestic falls. Variable-angle plates that contour to distal radius anatomy reduce tendon irritation, making them a staple in day-care surgery. Conversely, lower extremity demand is accelerating at 8.62% CAGR to 2031 as pelvic and hip fracture volumes rise in osteoporotic patients. The trauma fixation devices market size tied to lower extremity implants is projected to close the gap on upper limb usage over the next decade.

Innovations such as percutaneous hollow screws for pubic symphysis fractures allow elderly patients to avoid open surgery, shortening rehab times. Robotic navigation in spine trauma further streamlines screw placement accuracy, cutting revision risk. Collectively, evolving lower limb techniques invite manufacturers to tailor product lines to geriatric bone biology and complex pelvic geometry.

By End User:

Ambulatory Surgery Centers Capture Outpatient MomentumHospitals retained a 44.86% revenue share in 2025, driven by complex polytrauma and revision workloads. However, ambulatory surgery centers (ASCs) are projected to post the highest 7.71% CAGR through 2031, fueled by minimally invasive protocols that allow same-day discharge. Procedures migrating to ASCs include distal radius plating and clavicle fracture fixation, which traditionally required inpatient monitoring.

Enhanced regional anesthesia, rapid-recover implants, and remote patient-monitoring apps underpin the shift. The trauma fixation devices market now witnesses manufacturers bundling implant kits with disposable drapes, single-use power tools, and cloud-based navigation support suited to ASC economics. Specialty orthopedic clinics and emergency centers also broaden implant consumption, yet ASCs remain the prime outpatient growth engine across developed and developing regions alike.

Geography Analysis

North America Trauma Fixation Devices Market

North America controlled 39.05% of global revenue in 2025 and will maintain its lead through 2031 on the back of robust reimbursement and high surgical skill density. The November 2024 FDA guidance for bone plates and screws has sharpened review criteria yet also clarified pathways, shortening approval cycles for digital-ready implants. United States payers actively fund bioabsorbable implants to dodge secondary surgery, while Canadian hospitals invest in robotics aimed at smaller incisions and quicker turnover.

APAC Trauma Fixation Devices Market

Asia-Pacific is forecast to clock the fastest 7.55% CAGR over 2026-2031 as healthcare systems expand orthopedic theaters and trauma centers. China and India witness rapid trauma growth tied to urban transportation and construction, prompting procurement of versatile modular fixators. Japan’s super-aged society pushes geriatric-specific nailing systems, whereas South Korea pioneers AI-driven fracture planning. Domestic OEMs in China are entering global supply chains for titanium plates, adding competitive heat.

Europe Trauma Fixation Devices Market

Europe remains a stable third pillar, buffered by tight CE-Mark scrutiny and strong clinician–industry collaboration. Germany and the United Kingdom spearhead biodegradable implant trials aligned with environmental directives. Southern European markets accelerate adoption of reuse-optimized external fixators to curb spending. In Central-Eastern Europe, EU structural funds upgrade trauma units, giving multinationals fresh tenders.

MEA and South America Trauma Fixation Devices Market

The Middle East and Africa, alongside South America, collectively offer mid-single-digit expansion as governments channel oil proceeds and recovery funds into tertiary hospitals. Gulf states buy premium navigation-enabled systems, whereas Sub-Saharan Africa leans on donor-funded fracture programs that seek reusable ex-fix frames. Across Latin America, Brazil’s public health service increasingly reimburses drug-eluting plates for diabetic foot fracture prevention, nudging regional procurement norms higher.

Regulatory Landscape

Regulatory pathways for trauma fixation devices continue to be anchored in Class II orthopedic device controls in the United States, where plates, screws, and washers commonly proceed via 510(k) routes under 21 CFR Part 888. In February 2026, FDA's Quality Management System Regulation (QMSR) became effective, reinforcing ISO 13485:2016-aligned quality system expectations across manufacturers that supply global trauma catalogs and placing more operational emphasis on compliant design controls and postmarket processes.

In June 2026, FDA published an order on the classification of absorbable metallic bone fixation fasteners, adding a clearer federal framework for bioresorbable metal fasteners alongside established internal fixation categories. In the European Union, the European Commission published Delegated Regulations (EU) 2026/1451 and 2026/1359 in June 2026, expanding the list of Well-Established Technologies (WET) under MDR 2017/745. With entry into force in July 2026, the update creates a more standardized compliance pathway for mature trauma technologies while keeping higher evidentiary burdens for novel drug-eluting or antimicrobial combination concepts.

Competitive Landscape

The trauma fixation devices market is moderately consolidated. Stryker, DePuy Synthes, and Smith & Nephew collectively have significant revenue share, leveraging broad catalogs and digital surgery platforms. Stryker’s Blueprint Mixed Reality Guidance System overlays 3D imaging in real time, improving implant placement while feeding analytics back into product R&D. Zimmer Biomet deploys MotionLoc screws to retain compression yet allow controlled motion, differentiating hip and shoulder constructs.

Midsize challengers attack niche gaps. Bioretec secured first-in-class FDA clearance for its RemeOs magnesium screw in 2024, validating absorbable metal technology previously limited to Europe. Enovis strengthened its extremity lineup via the January 2024 acquisition of LimaCorporate, adding porous Trabecular Titanium and 3D-printed lattice architectures. Orthofix Medical extended external fixation capability with the TrueLok Elevate transverse bone transport system cleared in March 2025, targeting diabetic foot ulcer limb salvage.

Strategic themes include platform ecosystems bundling hardware, software, and AI navigation; expansion into bioactive coatings; and supply-chain localization for metal raw materials. Larger players recruit digital talent, partner with image-guided surgery start-ups, and sign multi-year value-based pricing deals with hospital systems. Smaller disruptors focus on single-use, pre-sterile kits for ASCs and biodegradable alloys for pediatrics, accelerating innovation cycles.

Trauma Fixation Devices Industry Leaders

Medtronic PLC

Stryker Corporation

Cardinal Health Inc.

Smith & Nephew PLC

Johnson & Johnson (DePuy Synthes)

- *Disclaimer: Major Players sorted in no particular order

Trauma Fixation Devices Market Companies Covered in this Report

- Arthrex

- B. Braun

- Cardinal Health

- Conmed

- Johnson & Johnson

- Orthofix

- Medtronic

- Smiths Group

- Stryker

- Zimmer Biomet

- Invibio

- Globus Medical

- Acumed

- Wright Medical Group

- NuVasive

- MicroPort

- OsteoMed LLC

- Integra LifeSciences Holdings Corp.

- Bio-Medical Enterprises Inc.

- Orthopaedic Implant Company

Market Opportunities and Future Outlook

A key opportunity is scaling outpatient-optimized trauma fixation bundles as ambulatory surgery centers gain procedural share. That shift is driving demand for pre-sterile, streamlined instrumentation and inventory-light tray concepts that reduce setup time and support faster turnover.

Product activity in 2026 supports this direction. Stryker expanded its fracture platform footprint with the European launch of the Pangea Plating System (upper and lower extremities) and introduced additional fracture and ankle fixation options, including a flexible syndesmotic device, illustrating how major suppliers are packaging implants and workflow into repeatable platforms that fit both hospital and outpatient settings. Material and design pathways are also creating openings, particularly in bioresorbables and polymer-based systems where removal-surgery avoidance and imaging compatibility can align with value-based purchasing goals. In 2026, FDA actions add regulatory clarity for next-generation internal fixation constructs, including the February 2026 510(k) clearance for the SINEFIX PEEK implant system and the June 2026 classification order for absorbable metallic bone fixation fasteners. On the competitive side, portfolio expansion through acquisition is widening distribution and pricing options, as seen in Poly Medicure's November 2025 acquisition of Citieffe Group to enter orthopedic trauma and extremities.

Recent Industry Developments in Trauma Fixation Devices Market

- May 2026: Stryker announced the European launch of the Pangea Plating System and completed a first case in Europe, extending its fracture platform for upper and lower extremity fixation beyond the United States. The rollout broadens availability of a standardized plate and instrumentation ecosystem, supporting cross-region portfolio harmonization and hospital-to-ASC workflow consistency.

- March 2025: Orthofix Medical received FDA 510(k) clearance and CE Mark for the TrueLok Elevate Transverse Bone Transport System, positioning a dedicated solution for limb preservation and diabetic foot ulcer care. The clearance expands external fixation capability into complex reconstruction use cases where integrated fixation and bone transport can influence procedure selection and competitive differentiation.

- January 2024: Enovis completed the acquisition of LimaCorporate, adding porous Trabecular Titanium and 3D-printed lattice architectures to strengthen its extremities and reconstruction capabilities. The deal deepened Enovis's access to additive-manufacturing-enabled implant designs that can be leveraged across trauma-adjacent fixation indications and surgeon preference portfolios.

Trauma Fixation Devices Market Report Scope and Research Methodology

Market Definition and Coverage

This methodology covers the trauma fixation devices market, meaning internal and external orthopedic fixation devices used to stabilize fractures and trauma-related bone injuries across common extremity cases and selected spinal trauma procedures. Revenue is measured at the manufacturer level in USD.

Scope exclusions: non-trauma elective implants, general surgical instruments, and rehabilitation aids that do not provide mechanical fracture fixation are excluded.

Segments Covered in This Report

- By Device Type

- Internal Fixators

- Plates

- Screws

- Nails

- Others

- External Fixators

- Unilateral & Bilateral Fixators

- Circular Fixators

- Hybrid Fixators

- Internal Fixators

- By Surgical Site

- Lower Extremities

- Hip & Pelvic

- Foot & Ankle

- Knee

- Others

- Upper Extremities

- Hand & Wrist

- Shoulder

- Spine

- Others

- Lower Extremities

- By End User

- Hospitals

- Ambulatory Surgery Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For this market, desk research starts with building a clean demand and supply context for fracture care and fixation usage, then mapping how devices typically move from manufacturers into hospitals and outpatient surgical settings. Public sources were used to anchor injury incidence and procedure context, including CDC injury statistics, NIH and NLM published clinical literature, FDA device and safety communications, WHO health data, and relevant orthopedic society publications.

We also reviewed company filings, investor presentations, and reputable medical press coverage to understand product mix shifts like internal versus external fixation, changes in average selling price, and any meaningful regulatory or reimbursement developments. Where needed, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used only to speed up cross-checks on revenue exposure, product launches, and innovation themes. The desk sources listed here are illustrative only, and many other public and paid references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how fracture fixation demand is behaving in hospitals and ambulatory surgery centers, and on sense-checking pricing and mix assumptions by device category. We spoke with a mix of manufacturers, distributors, orthopedic trauma clinicians, and procurement and operating room leaders across APAC, EMEA, and the Americas, so regional practice patterns and tender dynamics could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 19% | APAC: 43% |

| Mid tier: 51% | Functional/Unit leaders: 33% | EMEA: 31% |

| Smaller Players: 19% | Managers: 48% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a mixed approach where a top-down demand pool is reconstructed from trauma volume signals, procedure penetration, and typical fixation choice, then converted into value using average selling price bands by device type. To keep the model grounded, we used selective bottom-up approximations like sampled supplier roll-ups, channel checks on stocking patterns, and volume times price calculations for a few high-use fixation categories, and then adjusted totals only when the checks stayed consistent.

Key inputs in the model include fracture incidence and trauma burden indicators, the inpatient versus outpatient shift for fracture care, internal versus external fixation mix, implant usage per procedure for common extremity repairs, and pricing movement driven by material selection and hospital contracting. Forecasts were produced using scenario analysis around procedure growth and mix evolution, and the final slope was aligned with what interviewees expected for adoption and price pressure by region. When bottom-up inputs were missing for smaller countries or niche applications, gaps were handled through peer-country normalization using healthcare capacity indicators and validated ranges from primary discussions.

Data Validation & Update Cycle

Outputs were checked through multiple steps so obvious inconsistencies could be removed before sign-off. We compared model totals against independent signals like orthopedic procedure volumes, hospital purchasing behavior, and manufacturer exposure patterns, then reviewed any large variances at the region and device-type level.

If an assumption moved the market by a meaningful margin, analysts revisited the desk evidence and re-contacted selected respondents to confirm the direction and realistic bounds. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, pricing shocks, or notable portfolio shifts. Before delivery, a final analyst pass is completed so the published view reflects the latest available data and checks.

Mordor Intelligence's Trauma Fixation Devices Market Size Compared Against Other Published Estimates

Published market values for trauma fixation devices can differ because each publisher draws the scope boundary differently and uses different inputs for procedure volumes, pricing, and regional weighting. Differences also show up when a study anchors on a different base year, uses a different currency conversion timing, or applies a more aggressive or conservative adoption curve for newer fixation designs.

By tracking procedure-linked demand signals and refreshing price and mix assumptions through interviews, Mordor Intelligence keeps the model tied to internal and external fixation usage rather than blending in adjacent elective orthopedic implant revenues. Some publications appear to start from broad orthopedic device totals and allocate shares with limited checks, while others may over-rely on a single base year price point even though hospital contracting and material mix can move ASPs over time.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.45 B (2026) | |

| Global Consultancy A | USD 9.14 B (2024) | Uses a different base year and may include a wider device basket and end-use settings, which can lift the starting value when compared to a procedure and fixation-only boundary. |

| Industry Publisher B | USD 9.11 B (2025) | Applies a longer forecast window with a slower growth curve and limited detail on device-type mix and pricing refresh, which can change both the starting point and the growth path. |

The table shows that the spread mainly comes from base-year choice and what is counted inside the definition of trauma fixation, especially when adjacent orthopedic revenues are bundled together. Our approach stays repeatable because the total is built from clear demand indicators and then cross-checked with practical bottom-up signals, which makes it easier to explain what moved when assumptions change.

Key Questions Answered in the Report

What is the current value of the trauma fixation devices market?

The trauma fixation devices market size stands at USD 8.45 billion in 2026 and is projected to grow to USD 11.55 billion by 2031.

Which device category holds the largest share?

Internal fixators lead with 63.98% global trauma fixation devices market share in 2025.

Why are ambulatory surgery centers important for future growth?

ASCs combine minimally invasive techniques and lower facility overheads, enabling trauma procedures to shift outpatient and helping the segment log a 7.71% CAGR through 2031.

What technological trends will shape next-generation implants?

Bioabsorbable metals, drug-eluting coatings, 3D-printed patient-specific hardware, and mixed-reality surgical navigation rank as the most influential innovations.

How are regulatory changes affecting new product launches?

Clearer FDA guidance on bone-plate submissions and recognized standards for bioabsorbable resins have shortened approval timelines, although combination devices with antimicrobial agents still face rigorous review.

Page last updated on: