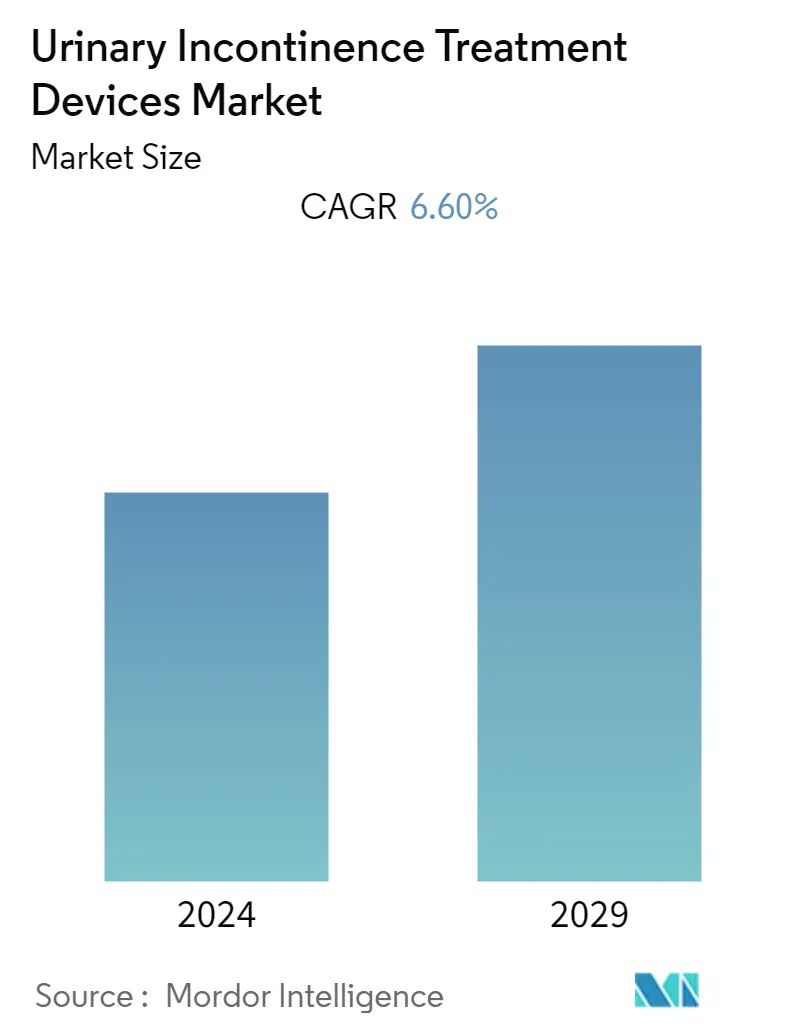

Urinary Incontinence Treatment Devices Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| CAGR | 6.60 % |

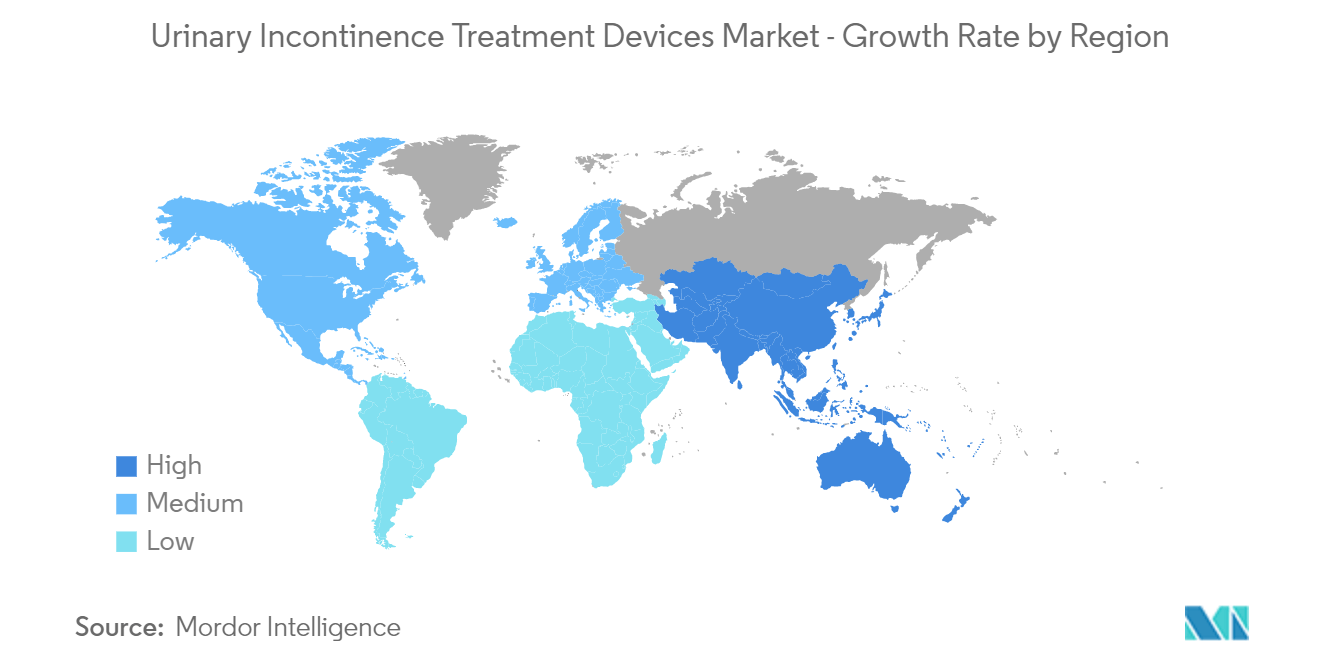

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Urinary Incontinence Treatment Devices Market Analysis

The urinary incontinence treatment devices market is expected to record a CAGR of 6.6% during the forecast period.

The COVID-19 pandemic significantly impacted the studied market, as there was an increased risk of urinary incontinence in COVID-19-infected patients. For instance, according to an article published by PubMed Central in February 2021, a study was conducted which showed that COVID19 infections cause inflammation and demyelination in the pudendal nerve, which ultimately leads to bladder incontinence. Thus, the COVID-19 pandemic significantly impacted the market initially, however as the pandemic has currently subsided, the studied market is expected to have stable growth during the forecast period of the study.

Factors such as the increasing prevalence of urinary incontinence and rise in the geriatric population and the rise in demand for minimally invasive surgery and product development are expected to boost the market growth.

The rising prevalence of urinary incontinence is one of the major factors driving the market growth. For instance, according to an article published by SpringerLink in March 2022, a study was conducted in Sweden which mentioned that urinary incontinence (UI) is defined as the complaint of involuntary loss of urine and has an estimated prevalence of about 25 to 45% among adult women. Thus, the high burden of urinary incontinence is expected to boost the adoption of urinary incontinence treatment devices.

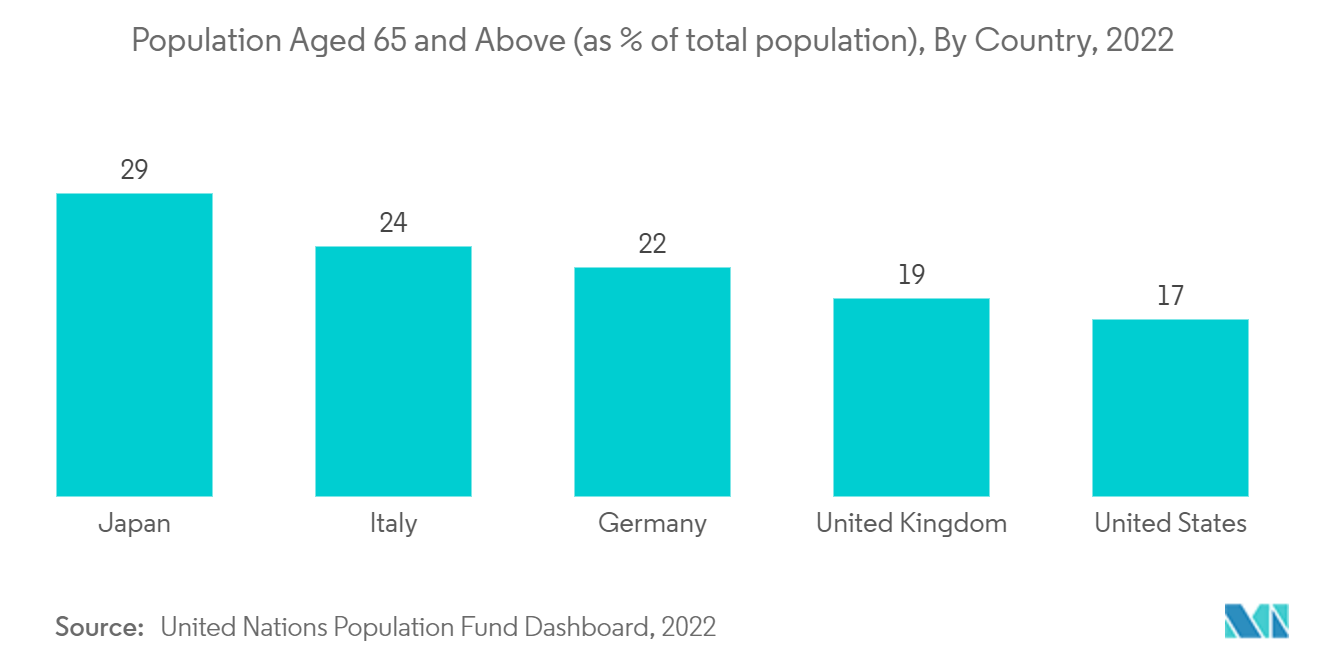

Moreover, the rising geriatric population is another major factor driving the market growth, as urinary incontinence is much more common in elderly people. For instance, according to the World Population Prospects 2022 Report published by UN in 2022, it was estimated the share of the global population aged 65 years or above is projected to rise from 10% in 2022 to 16% in 2050. By 2050, the number of persons aged 65 years or over worldwide is projected to be more than twice the number of children under age 5 and about the same as the number of children under age 12. Thus, the rising geriatric population is expected to enhance the market growth.

Furthermore, the rising developments by major market players are also expected to boost market growth. For instance, in March 2022, Medtronic announced that its investigational implantable tibial neuromodulation (TNM) device has been implanted in the first patient for its TITAN 2 pivotal study. The multicentre, prospective study is designed to assess the device's safety and efficacy in people with urinary incontinence-related overactive bladder (OAB).

Thus, the aforementioned factors such as the rising prevalence of urinary continence coupled with the rising geriatric population, and the increasing developments by major market players are expected to boost the market growth. However, factors such as a lack of awareness about devices and social stigma associated with the disease, and the risks and complications related to the procedures, are expected to impede market growth over the forecast period.

Urinary Incontinence Treatment Devices Market Trends

Urethral Slings Segment Expected to Witness Healthy Growth Over the Forecast Period

Urethral slings surgery is also known as mid-urethral sling surgery. The sling material used may be muscle, ligament, or tendon tissue. It may also be composed of synthetic material, such as plastic compatible with body tissues, or absorbable polymer that disintegrates over time. The urethral slings segment is expected to witness growth as these are highly recommended for surgical treatment for the treatment of stress urinary incontinence. Factors such as the rising prevalence of urinary incontinence, rising geriatric populations, and increasing developments by key market players are expected to boost segment growth.

According to an article published by PubMed Central in December 2022, a study was conducted in UAE which showed that the quality of life was affected in an estimated 90% of the patients suffering from urinary incontinence. Thus, the rising burden of urinary incontinence among women and the aging population is boosting the demand for urethral slings.

Furthermore, according to an article published by PubMed in January 2021, a study was conducted in Argentina which showed that there is a high prevalence of stress urinary incontinence among Argentinian women. The article also stated that among the patients who were having stress urinary incontinence, the prevalence of uncomplicated stress urinary incontinence was 39%. Thus, the high burden of urinary incontinence in the country is expected to boost the adoption of urethral sling.

Moreover, according to the data updated by WHO in October 2022, it is estimated that by 2030, 1 in 6 people around the world will be aged 60 years or over, and the share of the population aged 60 years and over will increase from 1 billion in 2020 to 1.4 billion in 2030, and by 2050, the world's population of people aged 60 years and older will double to 2.1 billion. It is also estimated that the number of persons aged 80 years or older is expected to triple between 2020 and 2050 to reach 426 million. As the geriatric population is often associated with urinary incontinence, the rising geriatric population is expected to boost market growth.

Thus, the aforementioned factors such as the rising prevalence of urinary incotinence, and the rising geriatric population are expected to boost the studied segment growth.

North America Expected to Hold a Significant Market Share over the Forecast Period

The major factors driving the market growth in the North American region are increases in the prevalence of urinary incontinence (UI), the geriatric population, and the demand for minimally invasive surgeries in the region.

For instance, according to an article updated by NCBI in August 2022, it is estimated that approximately 13 million Americans experience urinary incontinence annually, and the prevalence is 50% or greater among residents of nursing facilities. Similarly, according to an article published by Taylor & Francis Online in February 2023, a study was conducted in Mexico which examined the relationship between gender and the different urinary incontinence subtypes in community residents of the country in people aged 50 years old and above, it was found that in elderly females, mixed urinary incontinence had the highest incidence rate of 8.7%, which increased with age from 6.9% in 50 to 59-year-olds to 11.8% in 90 year olds. Thus, the high prevalence of urinary incontinence is expected to boost the market growth in the region.

Moreover, the rising geriatric population is also a major factor in market growth. For instance, according to the data published by Statistics Canada in July 2022, it is estimated that around 7,330,605 people are 65 years of age or older in Canada, which accounts for 18.8% of the total population.

Strategies adopted by major companies, such as research and development, mergers and acquisitions, and product launches to strengthen their market position are other driving factors for the growth of the market studied. For instance, in April 2021, Medtronic announced that they have gained approval from the United States FDA to proceed with an investigational device exemption (IDE) trial to evaluate its internally-developed, implantable tibial neuromodulation (TNM) device, which is designed to provide relief from symptoms of bladder incontinence.

Therefore, these aforementioned factors such as the rising prevalence of urinary incontinence, the rising geriatric population, and the increasing developments by key market players are expected to boost the urinary incontinence treatment devices market in the region over the forecast period.

Urinary Incontinence Treatment Devices Industry Overview

The urinary incontinence treatment devices market is moderately competitive. Some of the companies currently dominating the market are Boston Scientific Corporation, Becton, Dickinson and Company, Coloplast Corp., Promedon Group, AMI GmbH, Johnson & Johnson (Ethicon), Zephyr Surgical Implants, Medtronic PLC, Caldera Medical Inc., Hollister Incorporated B Braun SE, and ConvaTec Group PLC, among others.

Urinary Incontinence Treatment Devices Market Leaders

Promedon Group

Boston Scientific Corporation

BD

A.M.I. GmbH

Coloplast Corp

*Disclaimer: Major Players sorted in no particular order

Urinary Incontinence Treatment Devices Market News

- In December 2022, Axonics, Inc. announced that Health Canada has approved the company's fourth-generation rechargeable sacral neuromodulation system. It provides safe and durable symptom relief to women with stress urinary incontinence (SUI).

- In May 2022, BlueWind Medical, Ltd., announced the closing of a USD 64 million Series B funding round. The funding is raised for the development of the innovative RENOVA iStim implantable tibial neuromodulation device under investigation for the treatment of urgency incontinence alone or in combination with urinary urgency and/or urinary frequency.

Urinary Incontinence Treatment Devices Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Increasing Prevalence of Urinary Incontinence and Rise in Geriatric Population

4.2.2 Rise in Demand for Minimally Invasive Surgery and Product Development

4.3 Market Restraints

4.3.1 Lack of Awareness about Devices and Social Stigma Associated with the Disease

4.3.2 Risks and Complications from the Procedures

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

5.1 By Product

5.1.1 Urethral Slings

5.1.2 Electrical Stimulation Devices

5.1.3 Artificial Urinary Sphincters

5.1.4 Catheters and Others

5.2 By End User

5.2.1 Hospitals

5.2.2 Ambulatory Surgical Centers

5.2.3 Other End Users

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 South Korea

5.3.3.6 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 GCC

5.3.4.2 South Africa

5.3.4.3 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6. COMPANY PROFILES AND COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Boston Scientific Corporation

6.1.2 BD

6.1.3 Colopast Group

6.1.4 PROMEDON GmbH

6.1.5 AMI GmbH

6.1.6 Johnson & Johnson (Ethicon)

6.1.7 Zephyr Surgical Implants

6.1.8 Medtronic

6.1.9 Caldera Medical Inc.

6.1.10 Hollister Incorporated

6.1.11 B Braun SE

6.1.12 ConvaTec Group PLC

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Urinary Incontinence Treatment Devices Industry Segmentation

As per the scope of the report, urinary incontinence is a condition that defines any involuntary leakage of urine. The condition is categorized according to its underlying cause. Urinary incontinence results from difficulties in either filling, storing, or emptying the bladder, and some people may even suffer from a combination of these problems. The urinary incontinence treatment devices market is segmented by product (urethral slings, electrical stimulation devices, artificial urinary sphincters, and catheters and others), end user (hospitals, ambulatory surgical centers, and other end users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Product | |

| Urethral Slings | |

| Electrical Stimulation Devices | |

| Artificial Urinary Sphincters | |

| Catheters and Others |

| By End User | |

| Hospitals | |

| Ambulatory Surgical Centers | |

| Other End Users |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Urinary Incontinence Treatment Devices Market Research FAQs

What is the current Urinary Incontinence Treatment Devices Market size?

The Urinary Incontinence Treatment Devices Market is projected to register a CAGR of 6.60% during the forecast period (2024-2029)

Who are the key players in Urinary Incontinence Treatment Devices Market?

Promedon Group, Boston Scientific Corporation, BD, A.M.I. GmbH and Coloplast Corp are the major companies operating in the Urinary Incontinence Treatment Devices Market.

Which is the fastest growing region in Urinary Incontinence Treatment Devices Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Urinary Incontinence Treatment Devices Market?

In 2024, the North America accounts for the largest market share in Urinary Incontinence Treatment Devices Market.

What years does this Urinary Incontinence Treatment Devices Market cover?

The report covers the Urinary Incontinence Treatment Devices Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Urinary Incontinence Treatment Devices Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Europe Neurology Monitoring Industry Report

Statistics for the 2024 Europe Neurology Monitoring market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Europe Neurology Monitoring analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.