Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

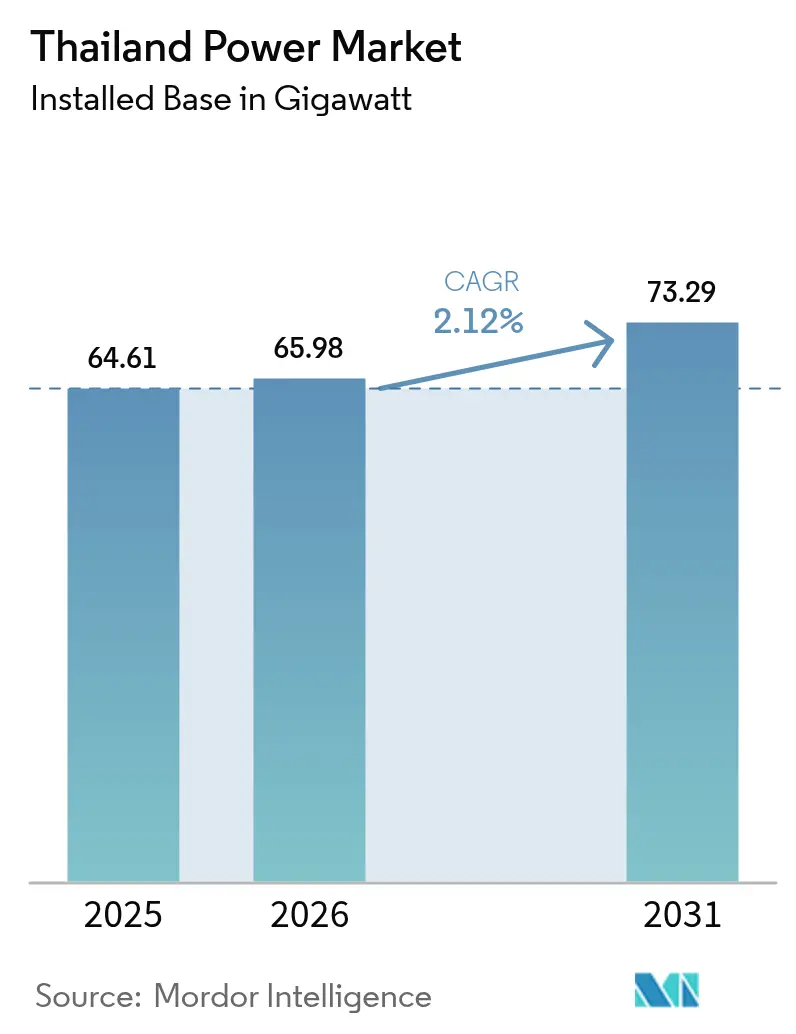

| Base Year Market Size (2025) | 64.61 gigawatt |

| Market Volume (2026) | 65.98 gigawatt |

| Market Volume (2031) | 73.29 gigawatt |

| Growth Rate (2026 - 2031) | 2.12% CAGR |

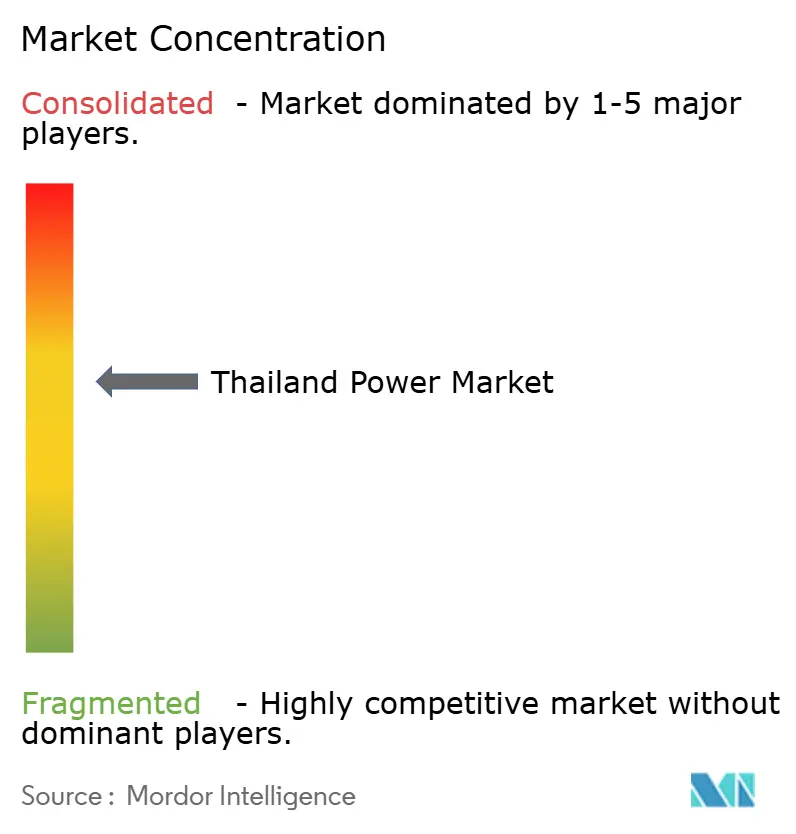

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Power Market Analysis by Mordor Intelligence

The Thailand Power Market size is expected to grow from 64.61 gigawatt in 2025 to 65.98 gigawatt in 2026 and is forecast to reach 73.29 gigawatt by 2031 at 2.12% CAGR over 2026-2031.

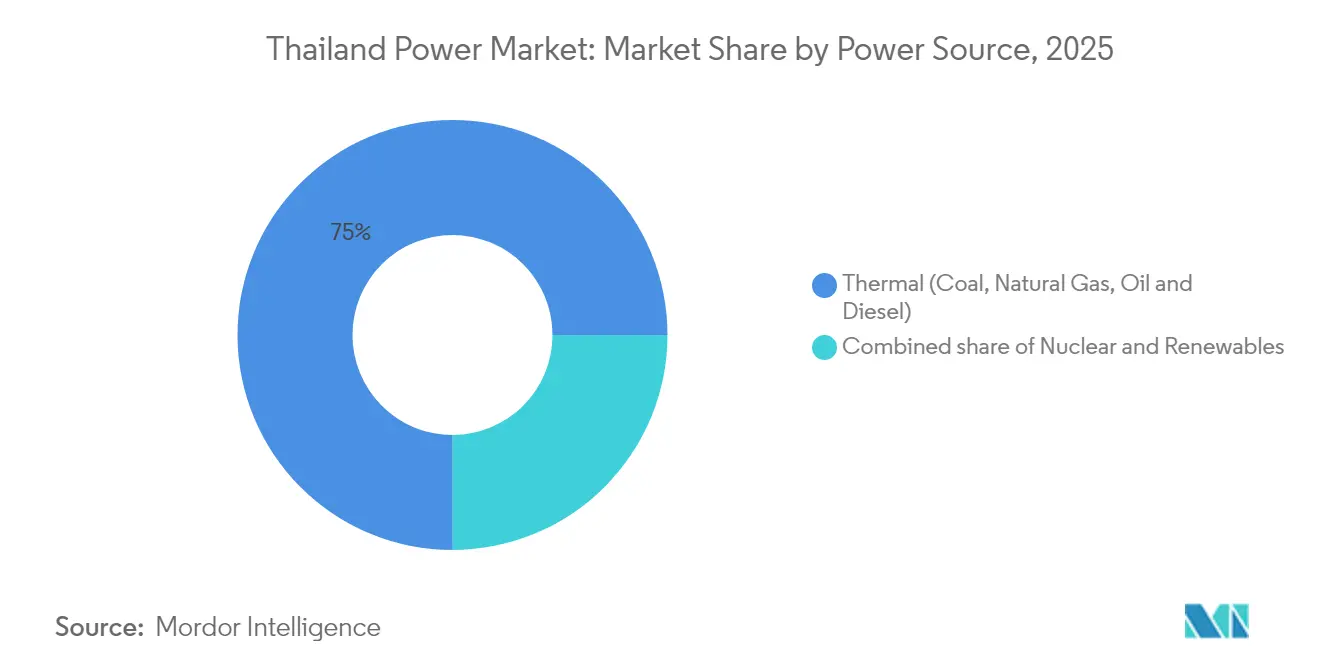

Installed thermal capacity, dominated by natural-gas plants, accounted for 75.6% of the Thailand power market in 2024, yet solar-led renewables are expanding the fastest as equipment prices fall and corporate power-purchase agreements (PPAs) multiply. Battery storage paired with photovoltaic systems outperforms peaking gas units on a levelized cost basis, encouraging independent power producers (IPPs) to advance hybrid portfolios despite the postponement of the Power Development Plan 2024 (PDP-2024). Grid modernization outlays of THB 90 billion (approximately USD 2.6 billion) for pumped-storage dams and high-voltage corridors underscore the imperative for system flexibility as coal retirements accelerate. Meanwhile, Thailand’s 30@30 electric-vehicle (EV) policy and the Utility Green Tariff (UGT) are lifting commercial and industrial (C&I) demand, reinforcing the structural shift toward distributed renewables and direct corporate procurement.

Key Report Takeaways

- By power source, thermal generation held 75.02% of Thailand's power market share in 2025, while renewables are forecast to advance at a 5.05% CAGR through 2031.

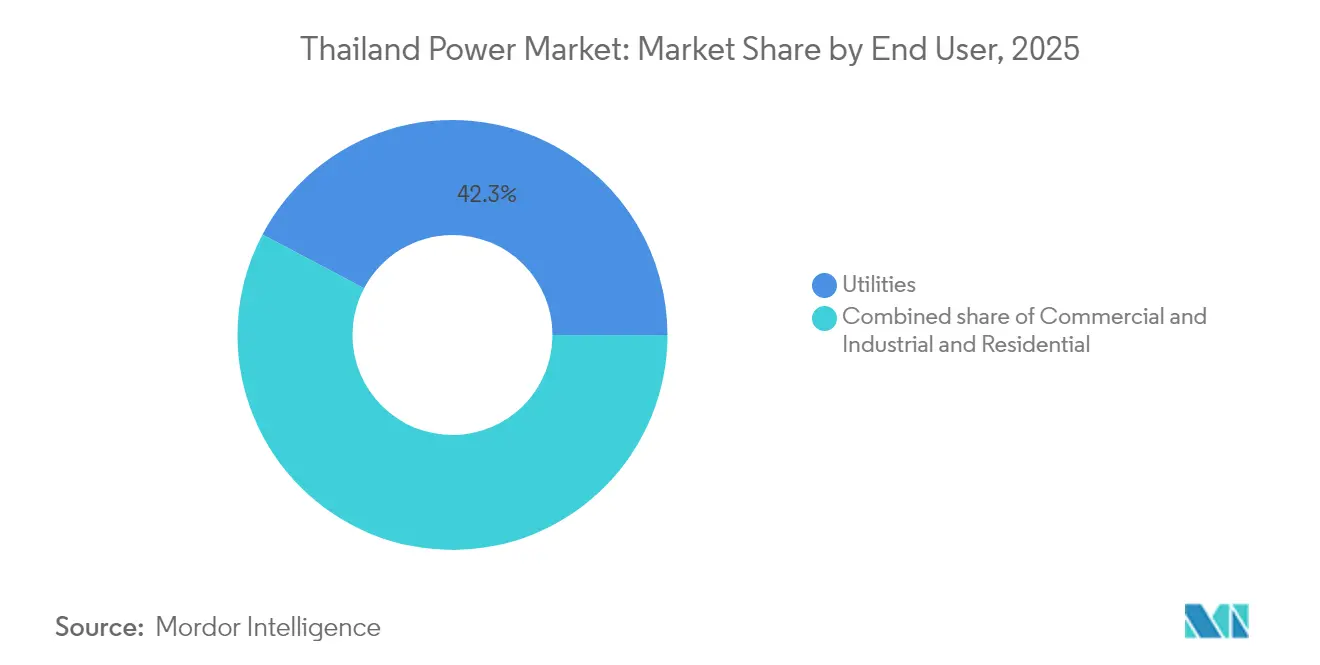

- By end user, utilities captured 42.25% of demand in 2025; the C&I segment is projected to expand at a 4.65% CAGR to 2031.

- The Central region accounted for 44.55% of 2025 consumption; the Eastern Economic Corridor is poised to post the fastest growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising renewables capacity additions | +0.8% | Central plains (solar), Northern provinces (hydro) | Medium term (2-4 years) |

| Modernization of ageing T&D grid | +0.5% | Southern corridor, Eastern Economic Corridor | Long term (≥ 4 years) |

| Steady electricity-demand growth from EV rollout | +0.3% | Urban clusters (Bangkok, Chiang Mai, Phuket) | Medium term (2-4 years) |

| Rapid cost decline of battery-integrated hybrid PV | +0.4% | Industrial estates, nationwide rooftop segments | Short term (≤ 2 years) |

| Rooftop FiT 2025 spurring distributed solar boom | +0.3% | Commercial buildings, industrial facilities | Short term (≤ 2 years) |

| ASEAN LTMS-PIP cross-border power-trade corridor | +0.2% | Regional (Laos imports, Malaysia link, Singapore offtake) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Renewables Capacity Additions

Thailand installed nearly 3 GW of solar photovoltaic (PV) capacity in 2024, increasing cumulative solar capacity to 11.875 GW and making solar the leading contributor to incremental capacity. EGAT’s floating-solar roadmap spans nine reservoirs totaling more than 2,700 MW, a strategy that sidesteps land constraints and speeds tie-ins via existing hydro grid nodes. The 2022 feed-in-tariff (FiT) auction awarded 5 GW across solar, wind, and battery projects, but southern congestion has delayed roughly 500 MW of grid connections, exposing generation-transmission interdependencies. Biomass and waste-to-energy remain niche, constrained by seasonal variability in feedstock availability despite supportive tariffs. Finalization of Third-Party Access (TPA) codes in 2025 is expected to unlock up to 2 GW of direct PPAs for data centers and export-manufacturing clusters, reducing reliance on utility offtake.

Modernization of Ageing T&D Grid

EGAT adopted Energy Exemplar’s PLEXOS model in January 2025 to optimize dispatch and renewable integration, signaling a digital pivot toward advanced grid analytics.(1)Energy Exemplar, “EGAT Picks PLEXOS for Dispatch Planning,” ENERGYEXEMPLAR.COM A THB 1.72 billion (USD 50 million) upgrade at the Ban Bueng 2 substation underscores capital intensity as voltage levels rise in the Eastern Economic Corridor. Three pumped-storage projects, totaling 2,472 MW, anchor the flexibility build-out, dwarfing the existing 1,531 MW fleet and providing the inertia lost from coal retirements. The Renewable Energy Forecast Center and Demand Response Control Center will coordinate curtailment once smart meter penetration, still below 10%, improves. Hitachi Energy’s grid-forming inverters are being piloted to furnish rapid frequency response compared with synchronous condensers.

Steady Electricity-Demand Growth from EV Rollout

Thailand’s 30@30 policy is expected to spur 150,000 EV registrations by the end of 2024, and EGAT has expanded public chargers from 211 to 321, illustrating the grid’s readiness to absorb the new load. Peak demand reached 36,792 MW in May 2024, and transport electrification could add 1,200-1,500 MW by 2030, comparable to the output of one large combined-cycle plant. Geographic clustering in Bangkok and tourism hubs heightens the risk of transformer overload, prompting the Metropolitan and Provincial Electricity Authorities to accelerate feeder upgrades. Hyperscale data-center developers are negotiating 20-year renewable PPAs, redirecting up to 2 GW of solar-plus-storage capacity toward industrial estates. Absent dynamic pricing, however, off-peak arbitrage remains underutilized, limiting demand-response potential.

Rapid Cost Decline of Battery-Integrated Hybrid PV

Lithium-ion battery prices fell below USD 140 per kWh in 2023, pushing solar-plus-storage hybrids below peaking gas on a levelized cost and widening the addressable dispatch window.(2)International Energy Agency, “Battery Cost Tracking 2024,” IEA.ORG Gulf Energy's 649 MW solar portfolio paired with 396 MWh of batteries drew USD 820 million in ADB financing, validating hybrid bankability under 20-year PPAs. Ember's analysis indicates that scaling hybrids beyond PDP targets could result in USD 1.8 billion in savings in LNG and transmission expenditures between 2026 and 2037.CLIMATE. Sungrow and Huawei Digital Power's local assembly has reduced inverter lead times to six months, enabling B.Grimm Power to commission 323 MW of solar six months ahead of schedule. ERC's forthcoming ancillary-services market will enable batteries to bid for frequency regulation and spinning reserve, monetizing their sub-second response capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for large-scale grid upgrades | -0.4% | Transmission backbone and pumped-storage projects nationwide | Long term (≥ 4 years) |

| Exposure to volatile imported LNG pricing | -0.3% | Gas-fired hubs in Map Ta Phut and Rayong | Short term (≤ 2 years) |

| Southern corridor grid congestion delaying RE projects | -0.2% | Surat Thani, Nakhon Si Thammarat, Songkhla | Medium term (2-4 years) |

| PDP-2024 postponement creating investor uncertainty | -0.2% | National (IPP financing and PPA negotiations) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex for Large-Scale Grid Upgrades

EGAT’s THB 90 billion (USD 2.6 billion) pumped-storage program implies costs exceeding USD 1 million per MW when civil works and environmental mitigation are included. The utility’s THB 13 billion (USD 380 million) floating-solar plan further stretches the balance sheet, and multilateral financing exposes projects to exchange-rate volatility. Southern 500 kV line reinforcements, priced at THB 20 billion (USD 580 million), are facing land-acquisition delays, stalling 500 MW of renewable connections and forcing developers into curtailment clauses. EGAT’s debt-to-equity ratio is near regulatory ceilings, limiting incremental borrowing unless tariffs rise or equity injections are made. Smaller IPPs cannot self-finance grid extensions, creating stranded generation until Third-Party Access enables private wheeling.

Exposure to Volatile Imported LNG Pricing

Imported LNG met 35.53% of Thailand’s gas demand in 2024, and spot cargo costs can swing 200% quarter-to-quarter, exposing gas-linked tariffs to abrupt hikes. The Map Ta Phut terminal’s 10 million-ton regas capacity covers only 60% of contracted imports, leaving a floating tranche exposed to global volatility. The Hin Kong plant became the first to secure private LNG under a Gulf-RATCH venture, hinting at potential procurement liberalization yet raising credit-risk questions for lenders. EPPO’s concept of a strategic gas reserve remains shelved due to cavern costs and tied-up working capital. Until battery storage reaches the gigawatt-hour scale, baseload gas plants will continue to anchor reliability, thereby sustaining exposure to LNG price shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Thermal Dominance Yields to Renewable Momentum

Thermal generation supplied 75.02% of capacity in 2025, yet solar additions lifted renewable output by 5.05% CAGR, signaling a pivot as coal and oil plants retire. Natural gas produced 57.74% of electricity; however, rising LNG dependence and carbon-neutrality targets are pressuring planners to cap new gas builds. Solar reached 11.875 GW on the back of floating-PV tenders totaling 2,656 MW, achieving capacity factors above 18% owing to cooler reservoir temperatures. Hydropower contributed 15.63% via Lao PDR imports, positioning Thailand as a transit hub in the Lao-Thai-Malaysia-Singapore (LTMS-PIP) corridor. Wind remains marginal, although offshore feasibility studies suggest a potential of 2-3 GW post-2028. Biomass and waste-to-energy projects expand slowly due to feedstock constraints. Nuclear and geothermal remain exploratory and are unlikely to influence the Thai power market before 2035.

Energy storage is the fulcrum of the transition: once lithium-ion breaches USD 100 per kWh, solar-plus-battery hybrids will undercut gas peakers, accelerating coal phase-outs and trimming LNG procurement. Consequently, the Thailand power market size for renewable hybrids is projected to grow faster than any thermal category over the 2026-2031 period. Reservoir-based floating solar, bundled with existing hydro tie-ins, offers near-term scale without new rights-of-way, highlighting the role of integrative assets in balancing variable supply.

By End User: Utilities Anchor Demand, C&I Surges

Utilities absorbed 42.25% of 2025 demand, reflecting EGAT’s monopoly over high-voltage transmission and bulk sales to the Metropolitan and Provincial Electricity Authorities. The C&I segment is forecast to grow at a 4.65% CAGR on data-center build-outs, automotive electrification, and petrochemical expansion in the Eastern Economic Corridor. Hyperscale cloud operators are negotiating 2 GW of direct renewable PPAs, bypassing utility offtake and fragmenting wholesale demand. Residential consumption grows just 1.7% CAGR as aging demographics cap load, though rooftop solar under the 2025 FiT refresh converts households into prosumers.

Industrial estates in Rayong and Map Ta Phut consumed approximately 8,000-9,000 GWh in 2024 and are expected to require an additional 1,500-2,000 MW by 2030. The Utility Green Tariff enables multinationals to pay premiums for low-carbon supply, redirecting 500-800 MW of solar toward industry by 2027. Bangkok’s air-conditioning-driven peaks spur demand-response pilots, while solar-powered irrigation pumps dampen agricultural diesel use. This divergence underlines how the Thai power industry must cater to both high-density urban load centers and distributed rural prosumers.

Geography Analysis

Thailand's Central region, including Bangkok, Ayutthaya, and Pathum Thani, accounted for 44.55% of the nation's electricity consumption in 2025, driven by dense residential populations, financial services, and the emergence of data centers. The Eastern Economic Corridor (EEC), spanning Chonburi, Rayong, and Chachoengsao, represents the fastest-growing pocket, expanding at a rate of 6-6.8% annually as EV factories, petrochemical complexes, and hyperscale data centers break ground. EGAT's priority upgrades to Ban Bueng and Pluak Daeng substations illustrate the grid-reinforcement imperative as variable renewables and industrial clusters converge.

Southern provinces, notably Surat Thani, Nakhon Si Thammarat, and Songkhla, offer abundant solar and biomass resources, yet face 500 kV corridor congestion that has deferred 500 MW of contracted renewable energy projects. Transmission upgrades costing THB 20 billion (USD 580 million) are currently under public consultation, but land-acquisition hurdles risk prolonging curtailment penalties. Northern provinces benefit from Lao PDR hydro imports; the Xayaburi dam alone delivers over 1,200 MW, making the region a transit node for the LTMS-PIP corridor.

The Northeast (Isan) region transitions from lignite reliance at the Mae Moh complex toward biomass co-firing and floating solar on irrigation canals, but achieving bidirectional flow requires THB 15-20 billion (USD 440-580 million) in distribution upgrades. Metropolitan Electricity Authority serves 5.8 million Bangkok customers and deploys time-of-use tariffs to shave 15-20% seasonal peaks. Tourist hubs such as Phuket experience 30-40% seasonal swings, prompting mobile substations to avoid overcapitalization. Finally, EEGAT'sfloating-PV pipeline leverages Central and Northern reservoirs, allowing projects to reach commercial operation within 24 months, underscoring geography's role in compressing lead times.

Competitive Landscape

The Thai power market features a hybrid structure: EGAT monopolizes high-voltage networks and most hydro assets, while IPPs, including Gulf Energy, RATCH Group, EGCO, and B.Grimm Power, have invested over USD 2 billion in new renewables and regional acquisitions since late 2024. Gulf Energy’s USD 820 million ADB-backed hybrid-solar financing exemplifies the multilateral appetite for long-term debt tied to 20-year PPAs. Equipment vendors JinkoSolar, Sungrow, Huawei Digital Power, Vestas, and Siemens Gamesa localize their assembly lines to reduce logistics costs, enabling B.Grimm to deliver 323 MW six months ahead of schedule.

Ancillary-services liberalization slated for late 2025 will let battery operators bid for frequency regulation at sub-second granularity, a market that Gulf Energy and BCPG have pre-positioned for through hybrid portfolios. Corporate PPAs and direct-access frameworks fragment demand, with hyperscale data centers expected to secure 2 GW by 2027, forcing utilities to recalibrate their tariffs and capacity-planning models. EGAT’s adoption of Energy Exemplar’s PLEXOS tool indicates a strategic turn toward data-driven dispatch, while pilot deployments of Hitachi Energy’s grid-forming inverters in the Southern corridor signal technology modernization

Thailand Power Industry Leaders

Electricity Generation Authority of Thailand

Gulf Energy Development PLC

RATCH Group Public Co. Ltd.

Electricity Generating Public Co. Ltd. (EGCO)

B.Grimm Power PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: EGAT issued a tender for 205 MWp of floating photovoltaic (FPV) hybrid capacity, targeting commissioning by Q4 2026 and further expanding its reservoir-based solar pipeline.

- January 2025: Thailand introduced the Utility Green Tariff (UGT) with a rate of 4.21 THB per kWh in its first phase (UGT1) to promote renewable energy among businesses. This slightly higher tariff allows eligible companies to purchase renewable energy and Renewable Energy Certificates (RECs) through an integrated electricity billing process.

- November 2024: Asian Development Bank (ADB) has provided USD 820 million in financing to Gulf Energy Development for 649 MW of solar projects with 396 MWh of battery storage. This marks one of Southeast Asia's largest hybrid-asset financings, showcasing the bankability of solar-plus-storage under long-term Power Purchase Agreements (PPAs).

- October 2024: BCPG clinched a THB 4.2 billion (USD 122 million) loan from TISCO Bank, earmarked for solar expansions in Thailand's Central and Northeastern regions. The projects are set to be commissioned in Q3 2025.

Thailand Power Market Report Scope

Generally, electricity generation refers to the production of electric power from primary energy sources. Electricity generation for utilities in the electricity industry involves delivering (through transmission, distribution, etc.) electricity to end users or storing it.

The Thailand Power Market is segmented by power source, end user, and T&D (Transmission and Distribution) voltage levels (qualitative analysis only). By power source, the market is segmented into thermal, nuclear, and renewables. By end user, the market is segmented into utilities, commercial and industrial, and residential. By T&D (qualitative analysis only), the market is segmented into High-Voltage Transmission, Sub-Transmission, Medium-Voltage Distribution, and Low-Voltage Distribution. The market size and forecasts for each segment are provided in installed capacity (GW).

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By T&D Voltage Level (Qualitative Analysis only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (Up to 1 kV) |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By T&D Voltage Level (Qualitative Analysis only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (Up to 1 kV) |

Key Questions Answered in the Report

How large is the Thailand power market in 2026?

The Thailand power market size reached 65.98 GW of installed capacity in 2026.

What CAGR is forecast for Thailand’s power capacity between 2026 and 2031?

Capacity is projected to grow at a 2.12% CAGR, reaching 73.29 GW in 2031.

Which segment is growing fastest within Thailand’s demand profile?

Commercial and industrial customers are expected to post a 4.65% CAGR through 2031, bolstered by data-center and EV-manufacturing expansion.

Why are floating solar projects important for Thailand?

Reservoir-based floating PV avoids land constraints, leverages existing hydro grid connections, and accelerates commissioning to 18-24 months.

How will battery storage influence Thailand’s generation mix?

Falling lithium-ion costs below USD 140 per kWh make solar-plus-storage hybrids cost-competitive with gas peakers, enabling faster coal retirements and LNG displacement.

What is the role of the Utility Green Tariff?

Introduced in January 2025, the tariff allows large consumers to purchase renewable electricity directly, helping multinationals meet decarbonization targets and redirecting up to 800 MW of solar toward industrial offtake.

Page last updated on: