Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.95 Billion |

| Market Size (2031) | USD 20.88 Billion |

| Growth Rate (2026 - 2031) | 15.97% CAGR |

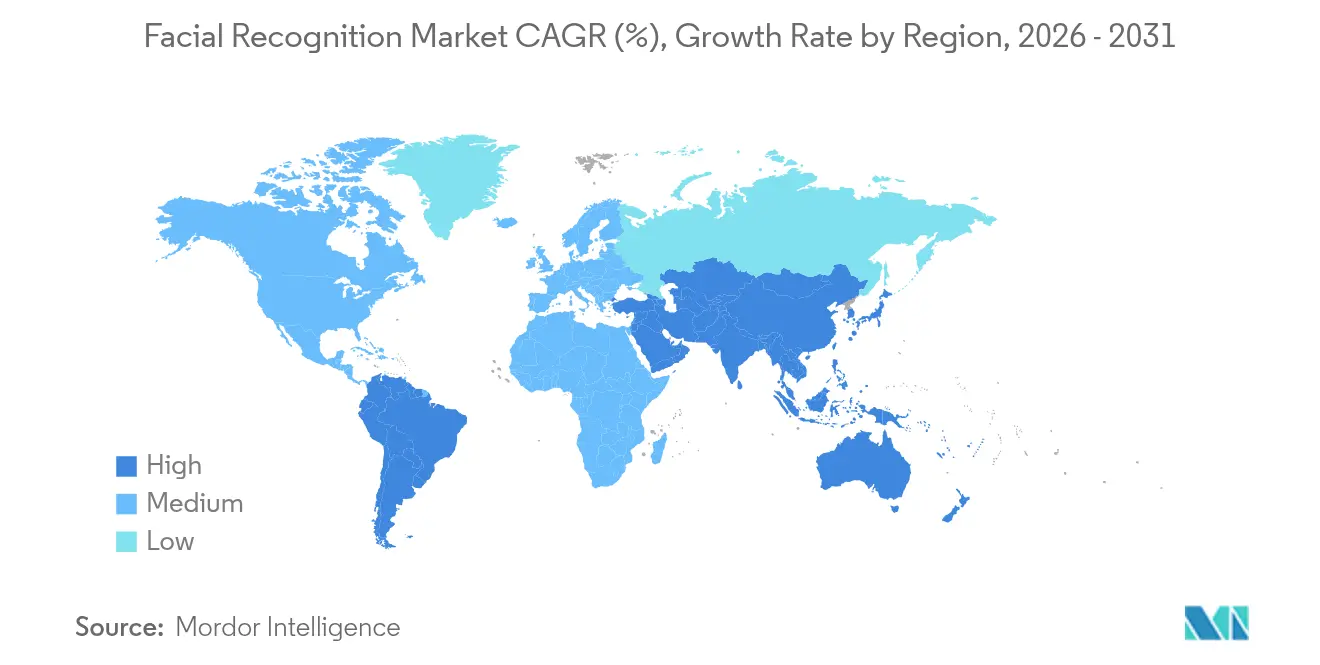

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Facial Recognition Market Analysis by Mordor Intelligence

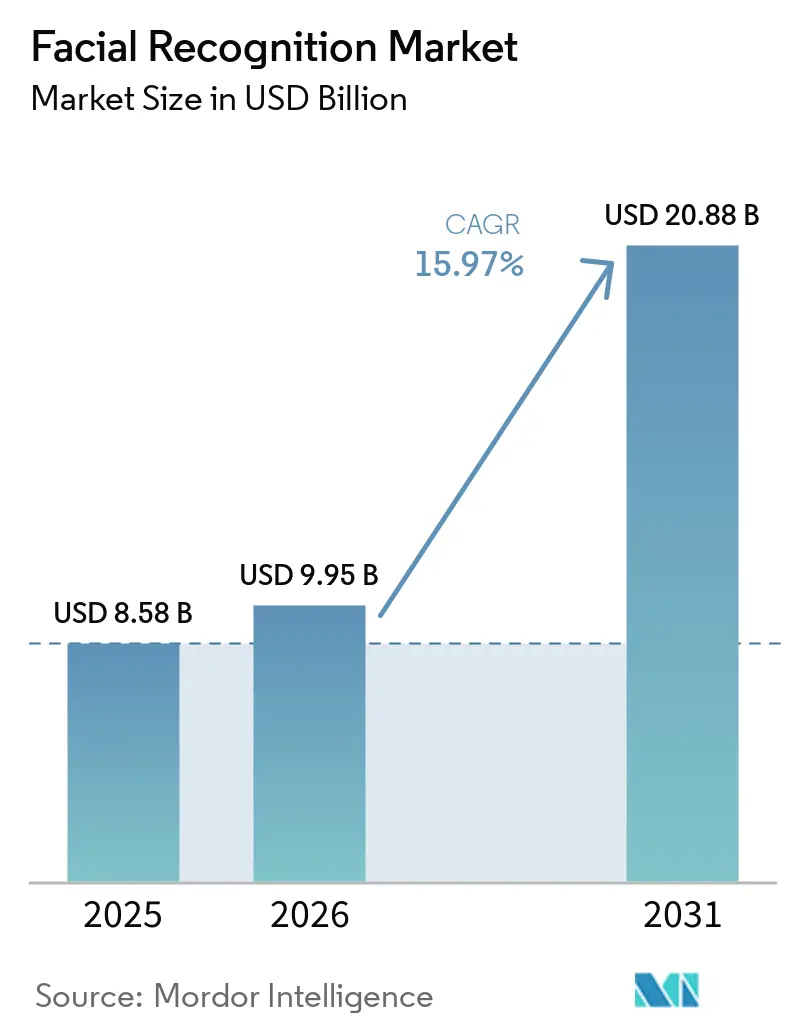

The Facial Recognition market size is expected to grow from USD 8.58 billion in 2025 to USD 9.95 billion in 2026 and is forecast to reach USD 20.88 billion by 2031 at 15.97% CAGR over 2026-2031. Growth now relies on edge-based architectures that deliver sub-second inference while allowing biometric data to remain on-device, a requirement embedded in new laws such as China’s Security Management Measures for Facial Recognition Technology. Stricter consent rules under the EU AI Act steer European buyers toward privacy-preserving designs, pushing vendors to integrate differential privacy, homomorphic encryption, and federated learning by default.[1]IAPP Staff, “Biometrics in the EU: Navigating the GDPR, AI Act,” iapp.org Hardware miniaturization and low-power AI accelerators have turned smartphones, body cameras, and kiosks into enrolment points, broadening the addressable base well beyond fixed CCTV. Finally, payments, passenger facilitation, and retail analytics now complement traditional security use cases, diversifying revenue streams and smoothing demand cycles across regions.

Key Report Takeaways

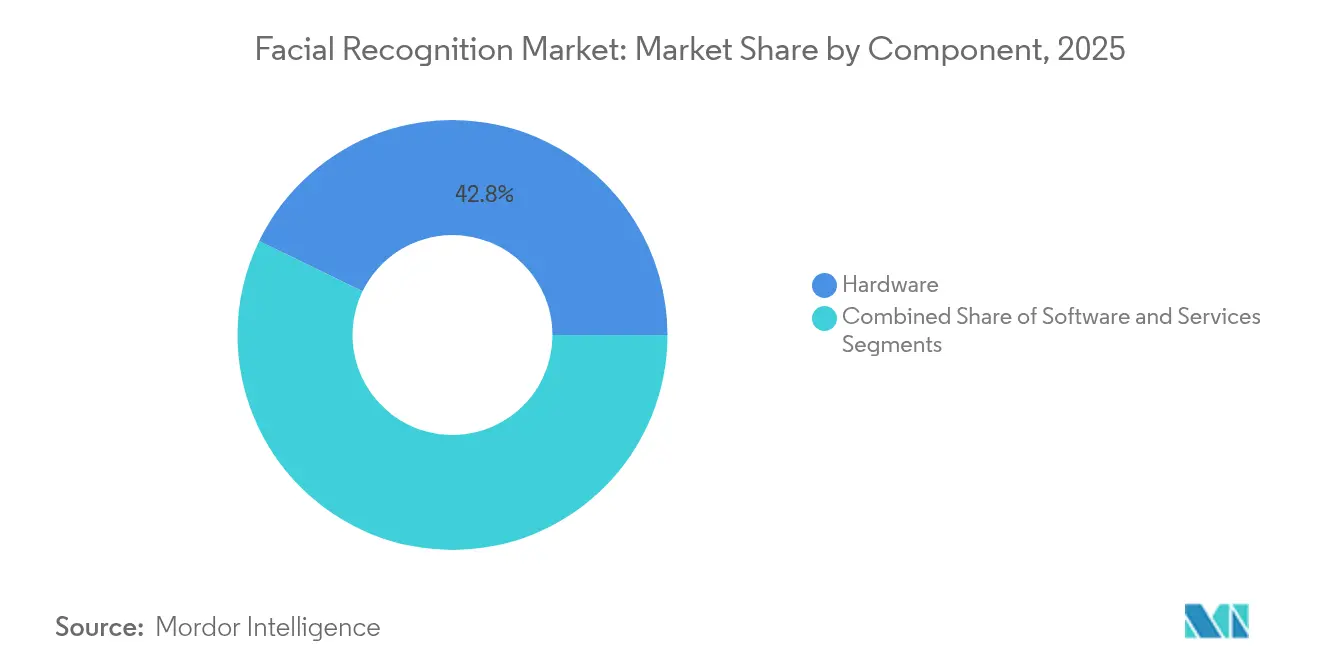

- By component, software held 57.20% of the facial recognition market share in 2025; edge hardware is poised to grow at a 18.76% CAGR through 2031.

- By technology, 2-D solutions led with 43.10% revenue in 2025, while facial analytics and emotion AI is forecast to post an 18.11% CAGR to 2031.

- By deployment, on-premise solutions represented 61.45% of the facial recognition market size in 2025; edge and on-device rollouts will expand at a 16.98% CAGR to 2031.

- By device form-factor, fixed cameras captured 55.05% of the facial recognition market share in 2025; mobile and wearables are tracking an 17.72% CAGR to 2031.

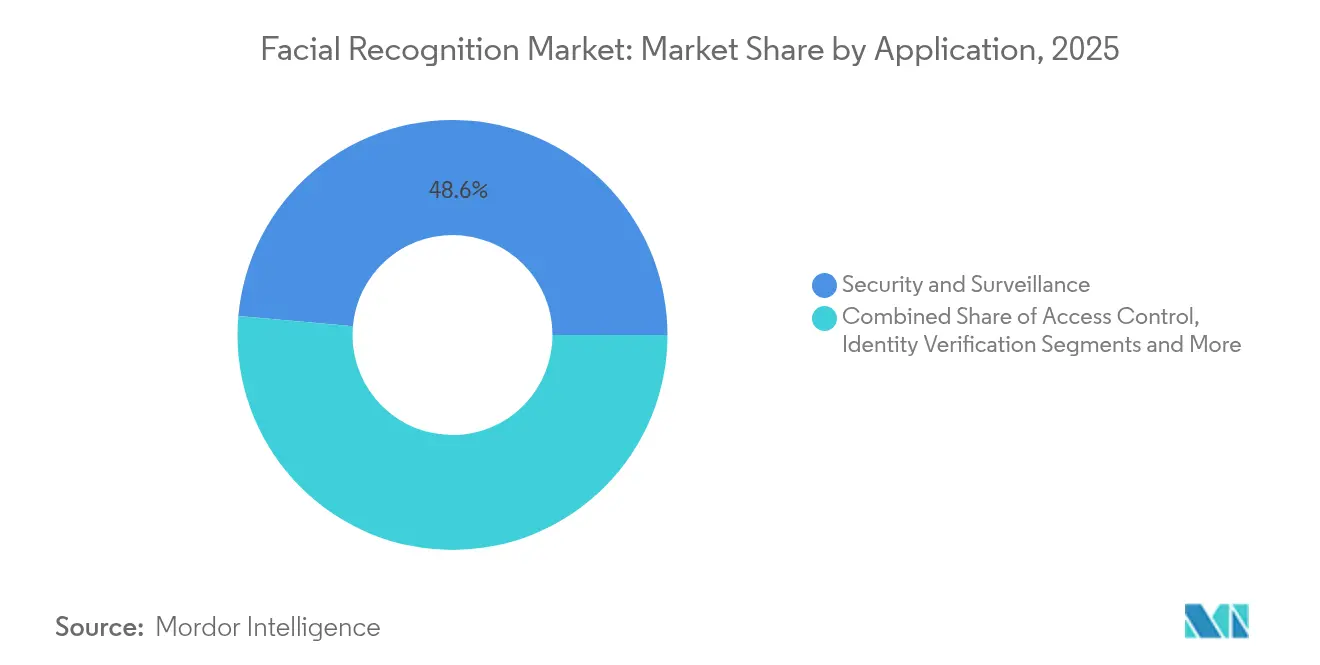

- By application, security and surveillance generated 48.60% of 2025 revenue, whereas payments will register the fastest 17.12% CAGR through 2031.

- By end-user industry, government and law enforcement accounted for 45.40% of 2025 spend; retail and e-commerce will advance at an 17.96% CAGR to 2031.

- By geography, Asia contributed 38.25% of global revenue in 2025; the Middle East will be the fastest-growing region at 16.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Facial Recognition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating National ID and e-Passport Roll-outs in Emerging Asia | +3.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Soaring Adoption of Edge-based Smart Cameras in Retail Chains | +2.8% | Global, with early gains in North America & EU | Short term (≤ 2 years) |

| Mandated Biometric Boarding by North-American Airlines | +2.1% | North America, expanding to EU | Short term (≤ 2 years) |

| Rapid Uptake of Face Pay and KYC-lite Wallets in GCC Fintech | +1.9% | Middle East GCC, pilot expansion to APAC | Medium term (2-4 years) |

| Post-COVID Hospital Triage Automation | +1.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating National ID and e-Passport Roll-outs in Emerging Asia

By 2025 Vietnam requires biometric authentication at every border, while Singapore’s passport-free lanes at Changi have cut wait times by 40% and target 95% automated use by 2026.[2]Ryan Browne, “Singapore launches biometric immigration processing at Changi Airport,” cnbc.com Malaysia and Papua New Guinea have scheduled nationwide deployments that push cumulative APAC enrolments above 800 million citizens, creating the world’s largest testing ground for on-device facial verification systems. Vendors gain not only licence revenue but also reference architectures that influence public-sector bids from Africa to Latin America. Interoperability standards drafted in these projects reduce integration risk for financial-service players that later reuse the same ID wallets. The result is a structural pull-through for software, edge hardware, and managed compliance services across the facial recognition market.

Soaring Adoption of Edge-Based Smart Cameras in Retail Chains

Organized retail crime exceeded USD 100 billion in the United States in 2024, accelerating deployment of edge AI cameras that analyse faces and behaviours without streaming to cloud servers.[3]Asif Anwar, “Retail Technology's Rapid Evolution,” securityinfowatch.com Asda’s pilot with FaiceTech achieves 99.992% accuracy and deletes non-matches instantly to satisfy GDPR mandates. Fifteen of the top 50 US grocers now use facial recognition to flag repeat offenders and detect employee–customer “sweethearting” fraud. Real-time analytics delivered on Nvidia Jetson or EdgeCortix SAKURA-II boards reduce shrinkage and generate footfall intelligence that feeds marketing systems, giving retailers a hard ROI within months. This twin benefit of loss prevention and experience personalisation keeps retail the fastest-growing private-sector adopter in the facial recognition market.

Mandated Biometric Boarding by North-American Airlines

The TSA has rolled out facial recognition to 25 major airports and plans hundreds more by end-2025, lowering average passenger verification time to eight seconds. United, Air Canada, and American Airlines let travellers enrol from mobile apps, pass checkpoints touch-free, and board without documents. Integration extends to bag drop and customs, with survey data showing 79% traveller approval. Airlines obtain operational savings and revenue-generating crowd analytics, while vendors gain recurring licence deals tied to passenger volumes. This regulated, high-visibility setting validates accuracy, resilience, and privacy safeguards, reassuring other transport nodes and driving cross-border harmonisation that enlarges the facial recognition market.

Rapid Uptake of Face Pay and KYC-Lite Wallets in GCC Fintech

The UAE Pass platform processed 600 million logins across 5,000 services by mid-2025, proving that facial authentication can handle national-scale financial and e-government workflows. Banks such as Emirates NBD already link UAE Pass to instant account opening, while Dubai is piloting passport-free travel where a user’s face unlocks every airport checkpoint. Fintech apps in Saudi Arabia and Qatar now embed sub-second facial KYC for micro-payments, reducing onboarding abandonment rates by 25%. The combination of sovereign IDs and facial payment wallets creates an ecosystem effect: once users enrol for one service, cost of extending to adjacent use cases approaches zero, fuelling network-driven growth for the facial recognition market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict GDPR Biometric Consent Requirements (EU-27) | -2.4% | EU-27, spillover to privacy-conscious markets | Long term (≥ 4 years) |

| Algorithmic Bias Litigation Risk in the U.S. | -1.8% | North America, expanding to developed markets | Medium term (2-4 years) |

| China Cyber-Security Classified Protection 2.0 Hardware Certification Bottlenecks | -1.3% | China, affecting global supply chains | Short term (≤ 2 years) |

| Public Push-back on City-wide Camera Expansion | -0.9% | Global, concentrated in democratic societies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict GDPR Biometric Consent Requirements (EU-27)

The EU AI Act classifies remote biometric identification as “high-risk,” banning real-time use for law enforcement except under narrow exemptions and prohibiting emotion recognition at work. Deployers must run Data Protection Impact Assessments, justify legitimate interest, and obtain explicit consent where power imbalances exist. Compliance costs rise 20–30% as integrators add masking, on-device processing, and audit logs. Vendors building EU-ready versions often re-use the privacy-by-design stack for other markets, but smaller firms exit or defer Europe, slowing short-term diffusion of the facial recognition market.

Algorithmic Bias Litigation Risk in the United States

Wrongful arrests linked to facial misidentification have sparked lawsuits such as the USD 10 million claim against Macy’s and EssilorLuxottica. The FTC’s order banning Rite Aid from facial surveillance for five years highlights potential penalties for biased or poorly governed deployments. Insurers now price liability premiums based on algorithm audit scores, adding 5–12% to total cost of ownership for riskier models. This drives demand for bias-testing services but also prompts conservative buyers to postpone projects, curbing near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Drives AI Innovation

Software accounted for 57.20% of global revenue in 2025 as algorithmic improvements lowered false accept rates to below 0.1% and enabled deployment on standard CPUs. Edge hardware remains the fastest-growing slice at 18.76% CAGR because compliance teams in finance and healthcare insist that biometric templates never leave the premises. SAKURA-II chips run complex models within 10 W power budgets, making autonomous kiosks viable inside convenience stores and transit hubs.

API-based licensing lets developers embed facial verification into mobile apps in hours, eliminating the multi-year cycles typical of earlier turnkey projects. At the same time, hardware vendors bundle computer-vision SDKs with secure-element storage and dedicated accelerators, locking in annuity streams as every new analytics module becomes a firmware download. This two-sided model keeps software sticky while raising switching costs for the entire facial recognition market.

By Technology: Facial Analytics Goes Beyond Identification

2-D algorithms still ride on existing CCTV infrastructure and therefore generated 43.10% of 2025 revenue. Yet “emotion AI” engines that map micro-expressions, attention span, or drowsiness will grow at 18.11% CAGR, reshaping customer-experience and road-safety applications. The facial recognition market size for analytics-driven modules is forecast to rise 3.40 × by 2031 as retailers, insurers, and automakers monetise behavioural insights.

Hybrid stacks blend 3-D depth cues with 2-D RGB frames to thwart spoofing and deliver liveness checks that comply with ISO/IEC 30107-3. Suprema’s Q-Vision Pro validates up to 50,000 users per device and encrypts every transaction end-to-end, allowing ATM operators to eliminate PIN pads. Such crossover of security and analytics keeps R&D pipelines full and diversifies revenue across licence, hardware, and service layers.

By Deployment: Edge Processing Mitigates Privacy Risk

On-premise deployments accounted for 61.45% of the facial recognition market size in 2025 because public agencies and banks prefer direct control over biometric repositories. Edge and on-device setups, however, will outpace all other modes at a 16.98% CAGR as new chipsets deliver 30 TOPS within smartphone-grade thermal envelopes. Google’s Kirkland campus test shows how corporates now swap badge swipes for silent, local face checks that never touch the cloud.

Hybrid architectures emerge where edge nodes run immediate decisions and send encrypted metadata to a central lake for trend analytics. Models like EdgeFace, with only 1.77 million parameters, reduce bandwidth by 95% and cut inference latency below 40 ms. These efficiency gains let companies comply with consent rules without sacrificing user experience, fuelling broader acceptance across the facial recognition market.

By Device Form-factor: Mobility Accelerates Penetration

Fixed cameras brought in 55.05% of 2025 revenue, but mobile and wearables will deliver the fastest 17.72% CAGR. Apple’s 90 active patents ranging from facial heat maps to partial-face unlocking signal continuous expansion of Face ID into mixed-reality headsets and automotive dashboards.

At the edge of experimentation, Harvard students built working facial recognition glasses in days using open-source code and off-the-shelf cameras, revealing low barriers to DIY innovation. For enterprise, body-worn cameras that auto-redact non-subject faces offer compliance-ready evidence capture. As devices proliferate, platform vendors monetise through per-endpoint licences, cementing network effects inside the facial recognition market.

By Application: Payments Unlock New Commercial Horizons

Security and surveillance held 48.60% of 2025 spend, but payments will post a 17.12% CAGR as card networks, acquirers, and merchants co-create consent-led checkout lanes. Mastercard’s tie-up with NEC piloted face-based payments in Brazil and Japan, reducing average transaction time by 15 seconds and lifting basket conversion by 7%.

JPMorgan’s partnership with PopID lets US diners “Pay by Face” at quick-serve outlets, eliminating terminal touch during peak hours. Because biometric POS systems reuse existing loyalty databases, merchants avoid new hardware where scanners integrate into camera-equipped kiosks. This razor-thin incremental cost speeds deployment, expanding addressable spend for the facial recognition market.

By End-User: Retail Challenges Government Primacy

Government and law enforcement still contributed 45.40% of 2025 revenue due to nation-state scale ID schemes and policing tools. Yet retail and e-commerce will show the highest 17.96% CAGR. Stores lose USD 100 billion annually to theft, a pain point now tackled through real-time offender watchlists and AI-flagged sweethearting schemes.

Fintech, healthcare, and automotive trail but present outsized margin potential. Hospitals moving to biometric triage, carmakers fitting driver-monitoring cabins, and banks deploying selfie-based KYC all require continuous algorithm updates. These subscription-heavy models enhance lifetime value, pushing the facial recognition market toward recurring, service-led economics.

Geography Analysis

Asia held 38.25% of 2025 revenue thanks to states that embed facial recognition into digital public infrastructure. China’s Security Management Measures force any entity that stores templates for more than 100,000 persons to register with provincial cyber authorities, establishing a vetting hurdle that favours established vendors with secure supply chains. Japan’s 2025 Osaka-Kansai Expo will run NEC face-payments for an anticipated 1.2 million visitors, a live showcase that can seed exports across Southeast Asia.

The Middle East will expand at a 16.88% CAGR as UAE’s biometric ID replaces plastic cards across banking, healthcare, and public portals. Dubai Airport plans passport-free travel that links passengers’ faces to boarding and retail wallets in one corridor, positioning the region as a laboratory for frictionless mobility. Gulf governments bankroll proof-of-concepts and rapidly convert them to nationwide policies, compressing adoption cycles and accelerating revenue capture for suppliers within the facial recognition market.

North America remains pivotal through airline rollouts and law-enforcement budgets but faces the strongest litigation risk. Congressional scrutiny over TSA’s expansion highlights civil-liberty concerns even as passenger throughput gains are undeniable. Federal fragmentation spawns a patchwork of state laws Illinois’ BIPA, California’s CPRA making cross-border deployments complex. Europe’s strict regime slows real-time city surveillance but ramps demand for edge devices running on-device redaction and consent management, giving privacy-tech vendors a foothold in the facial recognition industry.

Competitive Landscape

The market is moderately fragmented: the top five vendors command near-30% combined revenue, leaving ample space for specialists. NEC leads NIST accuracy tables with a 0.07% error rate and markets a cloud-agnostic stack that wins national tenders in Asia and Latin America. Thales and IDEMIA leverage passport issuance contracts to bundle border-control e-gates, while SenseTime pivots toward generative AI after US sanctions and local saturation.

Strategic partnering is central. Mastercard aligns with NEC to enter retail payments; IdentityE2E joins forces with Paravision to target US federal contracts. Patent depth matters, too: Apple’s 90 patents cover thermal mapping and millimetre-wave expression tracking, extending defensible moats into mixed reality. M&A remains active Metropolis acquired Oosto for USD 125 million, gaining access to its edge analytics IP after the firm raised USD 352 million. Regulatory headwinds may spur further consolidation as only vendors with compliance tooling and diverse revenue can withstand lengthening procurement cycles.

Facial Recognition Industry Leaders

Panasonic Corporation

Thales Group

Cognitec Systems GmbH

Aware, Inc.

NEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: UAE Pass surpassed 600 million logins across 5,000 services, illustrating hyperscale biometric orchestration.

- June 2025: China enforced security filings for entities storing >100k facial templates, raising procedural barriers for smaller suppliers.

- May 2025: American Airlines activated touchless ID at four US airports, extending end-to-end biometric journey coverage.

- April 2025: UAE announced plans to phase out physical Emirates ID cards within 12 months, banking on AI-driven face verification.

Global Facial Recognition Market Report Scope

The market is defined by the revenue generated from the sale of facial recognition solutions globally.

The facial recognition market is segmented by technology (2d facial recognition, 3d facial recognition, and facial analytics), application (access control, security and surveillance, and other applications), end user (security and law enforcement, healthcare, retail and e-commerce, BFSI, automobile and transportation, telecom and it, media and entertainment, and other end users), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Component

| Hardware | Cameras and Sensors |

| Edge AI Chips | |

| Software | Face Detection and Alignment |

| Feature Extraction and Matching | |

| Liveness Detection | |

| Services | Managed Services |

| Professional Services |

By Technology

| 2-D Facial Recognition |

| 3-D Facial Recognition |

| Thermal/Infra-red Facial Recognition |

| Facial Analytics and Emotion AI |

| Hybrid and Multimodal Algorithms |

By Deployment

| On-premise |

| Cloud-based |

| Edge / On-device |

By Device Form-factor

| Fixed Surveillance Cameras | |

| Mobile and Wearables | Smartphones |

| Body-worn Cameras | |

| Kiosks and Access Terminals |

By Application

| Security and Surveillance | Border Control / e-Gates |

| Public Area CCTV Analytics | |

| Access Control | Corporate and Campus Entry |

| Smart Locks (Residential) | |

| Identity Verification / e-KYC | Digital Banking On-boarding |

| SIM Registration | |

| Payments and Transactions | Face Pay (Retail POS) |

| Customer Analytics and Personalisation | In-store Targeted Advertising |

By End-user

| Government and Law-Enforcement |

| BFSI |

| Retail and E-commerce |

| Healthcare |

| Automotive and Transportation |

| Telecom and IT |

| Hospitality and Entertainment |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | Cameras and Sensors | |

| Edge AI Chips | |||

| Software | Face Detection and Alignment | ||

| Feature Extraction and Matching | |||

| Liveness Detection | |||

| Services | Managed Services | ||

| Professional Services | |||

| By Technology | 2-D Facial Recognition | ||

| 3-D Facial Recognition | |||

| Thermal/Infra-red Facial Recognition | |||

| Facial Analytics and Emotion AI | |||

| Hybrid and Multimodal Algorithms | |||

| By Deployment | On-premise | ||

| Cloud-based | |||

| Edge / On-device | |||

| By Device Form-factor | Fixed Surveillance Cameras | ||

| Mobile and Wearables | Smartphones | ||

| Body-worn Cameras | |||

| Kiosks and Access Terminals | |||

| By Application | Security and Surveillance | Border Control / e-Gates | |

| Public Area CCTV Analytics | |||

| Access Control | Corporate and Campus Entry | ||

| Smart Locks (Residential) | |||

| Identity Verification / e-KYC | Digital Banking On-boarding | ||

| SIM Registration | |||

| Payments and Transactions | Face Pay (Retail POS) | ||

| Customer Analytics and Personalisation | In-store Targeted Advertising | ||

| By End-user | Government and Law-Enforcement | ||

| BFSI | |||

| Retail and E-commerce | |||

| Healthcare | |||

| Automotive and Transportation | |||

| Telecom and IT | |||

| Hospitality and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the facial recognition market expected to grow?

The facial recognition market is projected to expand from USD 9.95 billion in 2026 to USD 20.88 billion by 2031, reflecting a CAGR of 15.97%.

Which component will drive future revenue?

Edge hardware will post the quickest 18.76% CAGR as organisations shift processing on-device to satisfy privacy and latency demands.

What region shows the strongest growth outlook?

The Middle East leads with a 16.88% CAGR, powered by government-funded biometric ID schemes and seamless-travel projects.

Why are retailers embracing facial recognition?

Retailers deploy edge-based cameras that cut shrinkage tied to organised crime and enable personalised service, producing measurable ROI.

How does regulation influence adoption in Europe?

GDPR and the EU AI Act classify remote biometric identification as high-risk, enforcing strict consent and audit rules that drive demand for privacy-by-design solutions.

What is the main litigation risk in the United States?

Misidentification leading to wrongful arrests exposes deployers to civil suits and FTC action, prompting stronger bias-testing requirements.

Page last updated on: