Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.04 Billion |

| Market Size (2031) | USD 11.87 Billion |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thermal Energy Storage Market Analysis by Mordor Intelligence

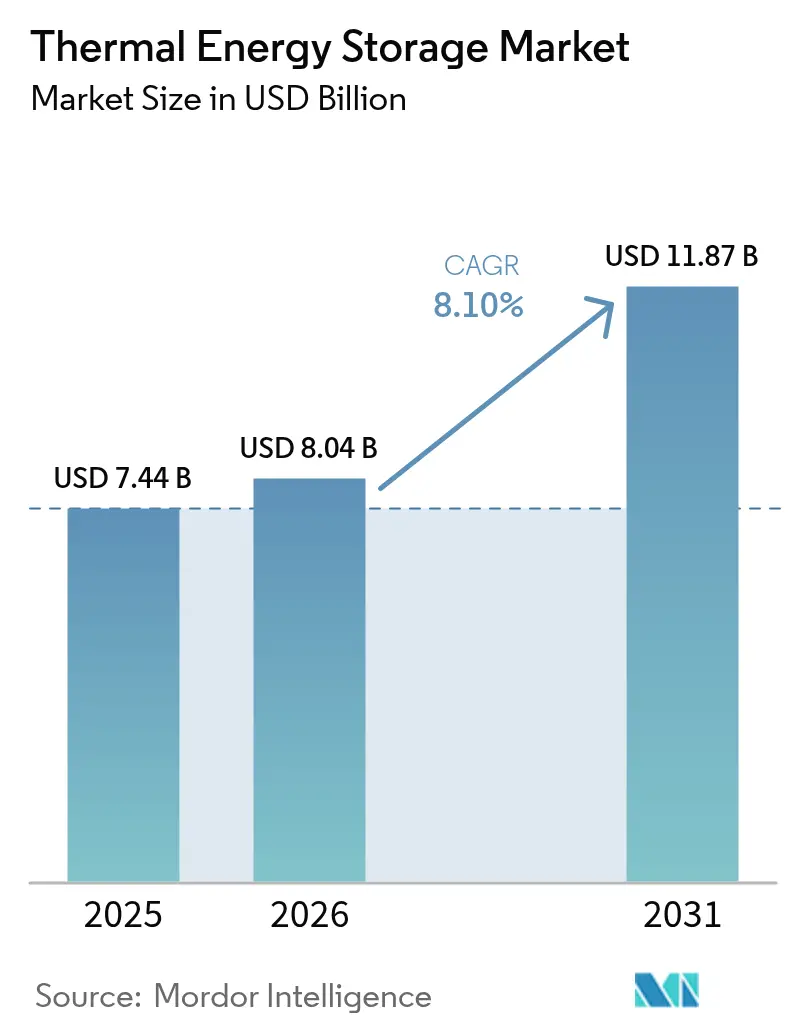

Thermal Energy Storage market size in 2026 is estimated at USD 8.04 billion, growing from 2025 value of USD 7.44 billion with 2031 projections showing USD 11.87 billion, growing at 8.1% CAGR over 2026-2031.

Growing demand for renewable-centric power systems that require more than 8 hours of storage, stricter industrial decarbonization mandates, and rapid build-out of concentrated solar power (CSP) plants are steering the growth curve. Utilities keep deploying molten-salt systems to firm solar output, while commercial and industrial sites adopt modular phase-change or sand-based units to cut peak-demand charges and capture waste heat. Venture capital flows toward solutions that outcompete lithium-ion batteries on cost beyond 8-hour durations, especially as raw-material constraints tighten battery supply chains. Europe’s fourth-generation district heating upgrade, Asia-Pacific’s CSP pipeline, and North America’s investment tax credits create a diversified demand base that cushions regional risk and accelerates scale-driven cost reductions in the thermal energy storage market.

Key Report Takeaways

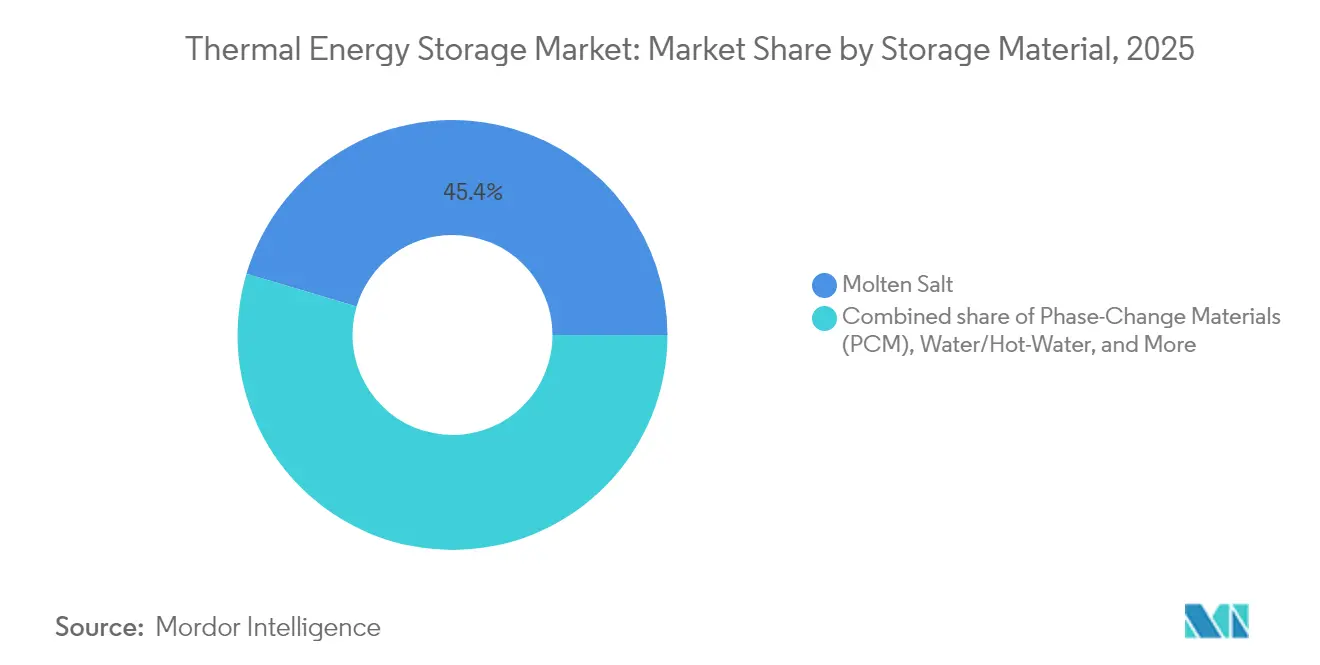

- By storage material, molten salt led with 45.40% of the thermal energy storage market share in 2025, while phase-change materials are projected to expand at 15.6% CAGR through 2031.

- By technology, sensible heat systems accounted for 73.20% of the thermal energy storage market size in 2025, and thermochemical solutions are progressing at an 17.1% CAGR to 2031.

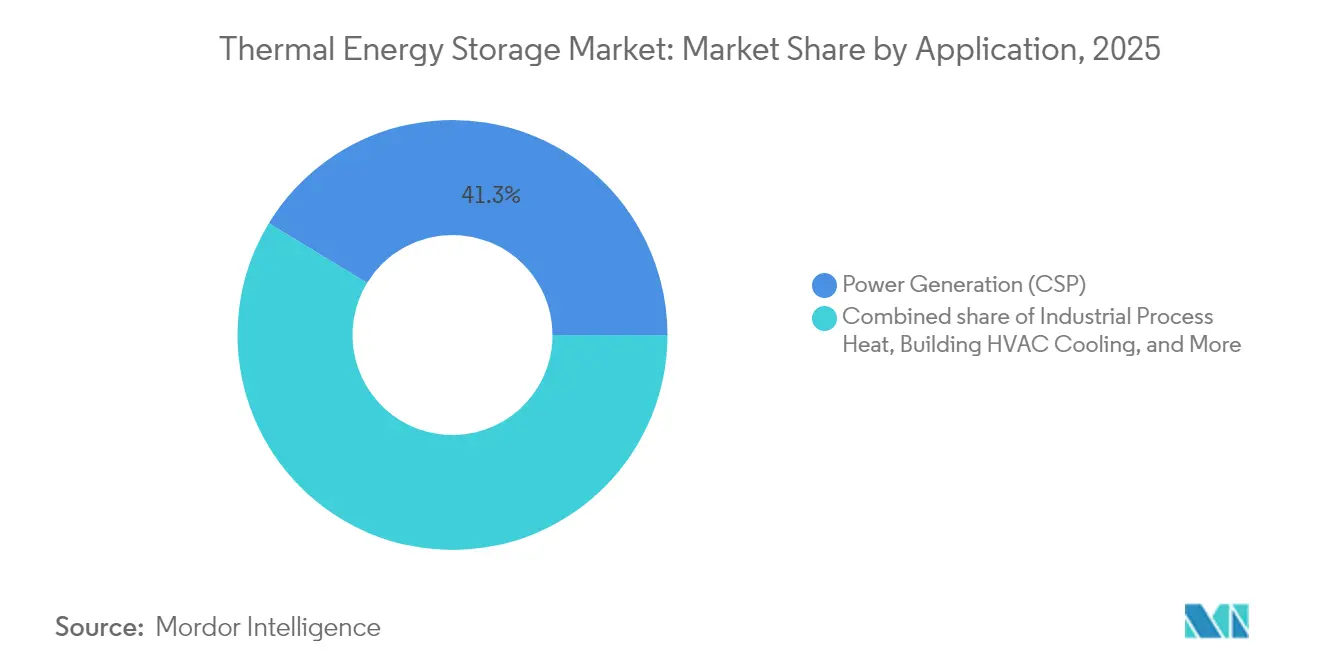

- By application, power generation contributed a 41.30% share of the thermal energy storage market size in 2025, whereas industrial process heat is rising at a 14.9% CAGR through 2031.

- By end-user, utilities held 58.20% of 2025 revenue, but commercial and industrial customers are growing at a 14.1% CAGR to 2031.

- By geography, Europe commanded 34.60% revenue in 2025; Asia-Pacific records the fastest regional CAGR at 13.4% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Thermal Energy Storage Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid build-out of CSP plants integrating ≥8-h molten-salt TES | +2.2% | Global, concentrated in MENA, China, India | Medium term (2-4 years) |

| Mandatory renewable capacity auctions bundling TES adders | +1.8% | Europe, California, Australia | Short term (≤ 2 years) |

| Expansion of fourth-generation district heating & cooling grids | +1.5% | Northern Europe, Scandinavia | Long term (≥ 4 years) |

| Industrial waste-heat recovery mandates | +1.2% | EU, Japan, South Korea | Medium term (2-4 years) |

| Super-hot-sand "thermal batteries" targeting < USD 10/kWh LCoS | +0.8% | Global, early adoption in US, Finland | Long term (≥ 4 years) |

| Coupling long-duration TES with green-hydrogen electrolyzers | +0.5% | Global, early adoption in Germany, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Build-Out of CSP Plants Integrating ≥8-Hour Molten-Salt TES

Mandatory eight-hour storage rules in China's 4.8 GW CSP program and India’s 5 GW pipeline have turned molten-salt tanks into standard equipment for dispatchable solar power.[1]SolarPACES, “China’s 4.8 GW CSP Pipeline,” solarpaces.org Lenders now treat the storage block as a revenue enhancer because it enables capacity-market earnings and reduces curtailment risk. Achieving levelized costs that rival gas-fired peakers has unlocked new sovereign-backed auctions across MENA. EPC firms are standardizing dual-tank designs, lowering balance-of-plant costs by 12% since 2024, further strengthening the bankability of large-scale thermal energy storage market projects. Pipeline visibility beyond 2027 fosters domestic salt and alloy supply chains in China and India, de-risking raw-material access.

Mandatory Renewable Capacity Auctions Bundling TES Adders

California’s Clean Power 2030 framework and the EU’s Building Performance Directive 2024/1275 require new renewable assets, including long-duration storage, awarding higher auction points to TES-equipped bids.[2]National Law Review, “EU Directive 2024/1275 Overview,” natlawreview.com These rules erase the prior split between generation and storage procurement, enabling unified project finance that favors thermal solutions once discharge windows exceed 6 hours. In Australia, renewable-energy zones grant grid-connection priority to thermal-storage projects that provide inertia and voltage support, trimming interconnection queuing delays by a year on average. The policy shift noticeably increases the thermal energy storage market’s addressable capacity in utility solicitations announced for 2026 and beyond.

Expansion of Fourth-Generation District Heating & Cooling Grids

Northern Europe’s push toward 50–70 °C district heating loops improves TES round-trip efficiency and unlocks seasonal applications. Denmark targets 50% district-heating coverage by 2030, with pit-thermal-storage fields shaving winter peak heat loads by up to 40%. Finland’s 90 GWh seasonal sand store demonstrates sub-USD 10 per kWh economics, while Germany allocates EUR 3 billion (USD 3.3 billion) for network upgrades that require domestic TES content. These deployments validate multi-gigawatt-hour systems, anchoring supply chains and permitting frameworks that benefit other European regions planning similar retrofits. Investors increasingly tag the thermal energy storage market as a district-energy asset class rather than an experimental technology.

Industrial Waste-Heat Recovery Mandates

The EU Industrial Emissions Directive compels large factories to capture low-grade heat by 2027, and Japan’s Top Runner Program extends similar obligations to heavy industry. Thermal storage modules enable time-shifting of batch-process exhaust heat, matching it with continuous demand and delivering 15–25% fuel-saving paybacks under five years. Cement and steel plants adopt firebrick or sand batteries operating above 1,000 °C, avoiding battery safety limits while slashing CO₂ emissions. Government grants covering up to 40% of capex in Germany and South Korea lower financing hurdles, broadening the customer base within the thermal energy storage market.

Restraints Impact Analysis of Thermal Energy Storage Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex of large-scale molten-salt tanks | -1.3% | Global, particularly utility-scale projects | Short term (≤ 2 years) |

| Competition from low-cost Li-ion and flow batteries | -0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Absence of bankable revenue stacks for behind-the-meter TES | -0.7% | North America, Europe | Short term (≤ 2 years) |

| Supply-chain bottlenecks for high-purity phase-change materials | -0.6% | Global, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex of Large-Scale Molten-Salt Tanks

Utility-scale molten-salt fields cost USD 15–25 per kWh, largely driven by stainless-steel containment and corrosion-resistant salt blends. Limited operating history keeps debt providers cautious, pushing projects toward higher-priced equity that inflates hurdle rates. The U.S. Department of Energy’s USD 305 million loan guarantee for a 2025 deployment signals rising public-sector confidence but has yet to materially compress financing spreads. OEMs are exploring prefabricated tank modules and low-chrome alloys that could shave 20% off capex by 2027, yet short-term economics remain a headwind for some thermal energy storage market bids.

Competition from Low-Cost Li-ion and Flow Batteries

Lithium-ion pack prices dropped 85% from 2010 to 2024 and continue to fall 10–15% each year, allowing batteries to dominate sub-8-hour grid services.[3]Source: Pacific Northwest National Laboratory, “Battery Cost Trends,” pnnl.gov Flow batteries add depth by enabling unlimited cycling, attracting frequency-regulation contracts that TES rarely pursues. For durations above 10 hours, however, lithium-ion costs escalate sharply and supply-chain exposure to nickel and lithium prices grows, reinforcing TES's competitiveness in the thermal energy storage market. Technology-specific procurement—batteries for fast response, TES for high-temperature or multi-day storage—is increasingly common, limiting direct substitution but still capping TES penetration in short-duration niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Thermal Energy Storage Market Segment Analysis

By Storage Material:

Phase-Change and Solid Media Accelerate AdoptionMarket leaders continued to favor molten salt, which retained 45.40% revenue in 2025, yet phase-change materials (PCM) are projected to capture an outsized share of new installations by growing at 15.6% CAGR. Compact PCMs lower installation footprint by up to 40%, easing siting inside commercial facilities and pushing incremental penetration in the thermal energy storage market. Solid media such as sand or concrete advance quickly: Finland’s 1 MW/100 MWh sand battery demonstrated 44% power-conversion efficiency, validating multi-day storage at sub-USD 10 per kWh. PCMs handle cooling loads effectively, especially in ice-based systems for commercial buildings. Meanwhile, solid media’s ability to sustain >1,000 °C unlocks direct industrial process-heat delivery without costly heat exchangers. As module suppliers scale production, unit costs are forecast to converge with molten salt by 2027, strengthening competitive parity across storage materials inside the thermal energy storage market.

Second-generation molten-salt recipes now tolerate 565 °C, allowing hybrid salt-plus-particle systems to edge closer to thermo-chemical densities. Suppliers are bundling salt supply contracts with recycled nitrate feedstocks, mitigating price volatility that previously discouraged offtakers. Regulatory preference for low-toxicity materials, especially in Europe, keeps water-based PCMs relevant for HVAC peak-shaving even though their energy density lags other chemistries. Overall, customer selection is becoming application-driven: PCMs for space-cooling peaks, molten salt for CSP baseload, and sand for extreme-temperature industrial furnaces, widening option sets within the thermal energy storage market.

By Technology:

Thermochemical Storage Moves Beyond DemonstrationSensible-heat technologies—water pits, molten-salt tanks, refractory bricks—retained 73.20% of 2025 revenue owing to proven performance and straightforward O&M. Yet thermochemical systems are forecast to register an 17.1% CAGR to 2031, the fastest within the thermal energy storage market, because they deliver three-fold higher volumetric density and negligible self-discharge. Pilot units based on salt-hydrate cycles now exceed 1 MWh, and metal-oxide redox loops are nearing 100-hour discharge tests. Contrastingly, latent-heat solutions using bio-based PCMs bridge the complexity gap by offering energy densities double those of sensible heat without active chemical reactors.

Research at Kaunas University of Technology showed soil-embedded thermochemical capsules that retrofit beneath existing buildings, eliminating separate tank infrastructure and cutting installed costs. The integration of AI-based control software optimizes charging when renewable curtailment surges, enhancing revenue stacking from energy-arbitrage plus heat-offtake contracts. As thermochemical vendors achieve ≥95% round-trip efficiency in targeted temperature bands, EPC firms are beginning to quote turnkey pricing for 5-10 MWh blocks, reinforcing commercialization prospects and expanding the thermal energy storage industry footprint.

By Application:

Industrial Process Heat Overtakes Power Generation GrowthPower generation retained 41.30% revenue in 2025, mainly because CSP projects still form the backbone of multi-hundred-megawatt installations. Yet industrial process heat is advancing at a 14.9% CAGR, the clear growth engine for the thermal energy storage market. Steel, cement, and chemical plants adopt firebrick resistive heaters or sand batteries to decouple furnace operation from electricity prices, slashing Scope 1 emissions by replacing natural gas. Waste-heat recovery regulations in the EU and South Korea drive retrofits that supply low-pressure steam or hot air directly from stored heat.

District-energy operators add seasonal TES ponds to raise solar and biomass share in mixed-fuel networks, while commercial real-estate owners install ice tanks for HVAC demand-charge avoidance. Buildings account for smaller absolute megawatt hours but deliver high-margin retrofits, making them attractive for start-ups pitching modular units. Military forward-operating bases and remote islands deploy containerized thermal systems paired with PV to reduce diesel reliance, adding niche but strategic visibility to the thermal energy storage market.

By End-User:

Commercial & Industrial Sites Expand Behind-the-Meter PortfolioUtilities remained the top buyers with 58.20% 2025 revenue because their grid-scale CSP and district-heating assets are capital-intensive. However, commercial and industrial (C&I) customers are projected to grow at a 14.1% CAGR, steadily eroding the utility share of the thermal energy storage market. High demand charges in urban grids incentivize C&I facilities to store off-peak electricity as thermal energy, displacing peak-period consumption. Food-processing plants use PCM cold stores to maintain product integrity during grid outages. Semiconductor fabs integrate sand batteries to stabilize process heat, ensuring product yield and adding resiliency credits under ISO-compliant audits.

Industrial players favor TES because systems can deliver high-temperature heat and backup power when coupled with turbines or solid-oxide fuel cells. Financing models are shifting from capex to heat-as-a-service contracts, bundling storage, heat delivery, and performance guarantees, which lowers adoption barriers for medium-sized enterprises. Consequently, the thermal energy storage industry is poised for deeper penetration in behind-the-meter installations where multi-value revenue stacks create swift payback.

Geography Analysis

Europe Thermal Energy Storage Market

Europe controlled 34.60% of global revenue in 2025 by exploiting mature district-energy systems, stringent carbon policies, and generous heat-network grants. Germany’s EUR 3 billion (USD 3.3 billion) modernization fund accelerates pit-thermal-storage adoption, while Denmark’s target for 50% district-heating coverage by 2030 implies multi-gigawatt-hour seasonal reservoirs. Scandinavia’s seasonal mismatch between abundant summer solar and winter heat loads makes TES indispensable, pushing network operators to procure modular sand or water-pit systems. Building-performance mandates now label long-duration heat storage as critical infrastructure, mainstreaming procurement processes and expanding the thermal energy storage market across municipal utilities.

APAC Thermal Energy Storage Market

Asia-Pacific is the fastest-growing region with a 13.4% CAGR to 2031, buoyed by China’s 30 GW storage target and India’s CSP mandates that require eight-hour TES. Domestic supply chains in China reduce molten-salt tank costs by 18% compared with imported systems, sharpening price competitiveness in the thermal energy storage market. Australia’s renewable-energy zones award expedited grid interconnection to projects bundling TES, and pilot approvals for firebrick batteries in industrial mines add proof points. Japan and South Korea focus on high-temperature waste-heat capture in steel and petrochemical complexes, leveraging favorable depreciation schemes to replace imported LNG with stored solar or grid electricity.

North America Thermal Energy Storage Market

North America benefits from the Inflation Reduction Act, which provides a 30% investment-tax credit for qualified thermal storage. California’s Clean Power 2030 plan mandates TES in new utility solar solicitations, and New York’s building decarbonization codes push high-density storage for space-heating retrofits. The U.S. Department of Energy’s USD 305 million loan guarantee to a large-scale project signaled federal support that eases lender risk perceptions. Industrial off-takers such as data-center operators trial sand batteries to recycle server waste heat into facility heating, illustrating a demand-side driver that complements utility procurements and broadens the thermal energy storage market addressable base.

Regulatory Landscape

Thermal energy storage (TES) adoption is increasingly tied to heat and power decarbonization policy, through a mix of binding directives, state-level legislation, and technical standards. In Europe, Directive (EU) 2023/2413 (RED III) sets requirements for renewable heat and system flexibility across 2026-2030, which supports district heating and cooling upgrades where pit and tank storage improve network efficiency and help integrate more renewables. In the United States, district energy regulation remains fragmented, but New York State has advanced policy work on utility thermal energy networks (TENs). Rhode Island legislation (Utility Thermal Energy Network and Jobs Act, active in 2026) directs the Public Utilities Commission to establish market-access and cost-recovery frameworks for utility-owned thermal networks, while Colorado SB26-142 similarly signals statutory direction to reduce legal and financial soft costs for thermal network projects.

On the compliance and engineering side, project bankability increasingly relies on recognized design and performance specifications. ASME TES-1-2023 provides an American National Standard framework for the design, construction, and operation of molten-salt TES systems, and IEC TS 62862-2-1:2021 offers technical specifications for characterizing TES in solar thermal electric plants, both of which support engineering assurance and lender diligence for utility-scale deployments. At the same time, EU policy briefs tied to district heating modernization note that some large-scale TES classes are not explicitly recognized in parts of the regulatory framework, which can restrict how storage value is captured through flexibility and market mechanisms even when broader decarbonization mandates exist.

Competitive Landscape

The thermal energy storage market remains moderately fragmented, with technology-specialist start-ups competing against diversified energy majors. Rondo Energy raised USD 107 million and inked a gigawatt-scale deployment agreement with Saudi Aramco, showcasing the primacy of commercial demonstration over lab innovation. Sulzer’s 2025 partnership with Hyme Energy reflects incumbents pairing EPC expertise with next-gen TES modules to bid turnkey process-heat contracts. Siemens Energy is pivoting from turbine-heavy portfolios toward sand-battery integration, expecting first-wave deployments at European chemical plants from 2026.

Vendors differentiate primarily on levelized cost, operating temperature, and modularity. By leveraging ubiquitous raw materials and automated brick presses, Firebrick and sand-based systems target sub-USD 10 per kWh. Molten-salt incumbents defend ground with proven multi-100 MW references and integrated solar receivers. Thermochemical start-ups like Antora Energy capitalize on threefold energy density to win space-constrained industrial sites. Strategic acquisitions are rising; for example, an oil-and-gas major acquired a PCM vendor in early 2025 to secure intellectual property and diversify clean-energy assets.

As of 2025, the top five suppliers account for roughly 35% of installed capacity; the remainder is spread across dozens of regional specialists. OEM partnerships with construction majors are central because installation cost often equals or exceeds component cost. Consequently, the competitive field favors companies capable of supplying technology plus bankability evidence, which speeds lender due diligence and reinforces late-stage financing for large thermal energy storage market projects.

Thermal Energy Storage Industry Leaders

-

Siemens Energy AG

-

Abengoa SA

-

Aalborg CSP A/S

-

BrightSource Energy Inc.

-

CALMAC Corp.

- *Disclaimer: Major Players sorted in no particular order

Thermal Energy Storage Market Companies Covered in this Report

- Aalborg CSP A/S

- Abengoa SA (ENGIE CSP)

- BrightSource Energy Inc.

- Siemens Energy AG

- CALMAC Corp.

- EVAPCO Inc.

- SaltX Technology Holding AB

- Trane Technologies plc

- Rondo Energy

- Antora Energy

- Brenmiller Energy

- Hyme Energy

- Energy Nest (Aker Solutions)

- Malta Inc.

- Terrafore Technologies LLC

- Vantaa Energy Ltd.

- SR Energy

- Baltimore Aircoil Company (BAC)

- Burns & McDonnell

- Ice Energy

- Additional validated firms

Market Opportunities and Future Outlook

Industrial process heat electrification and heat network modernization are creating the most actionable whitespace for thermal energy storage beyond traditional CSP-linked molten-salt deployments. Industrial sites with continuous heat demand are moving from pilots to commercial-scale systems, illustrated by Antora Energy and POET announcing commissioning of a 5 GWh thermal energy storage system at POET's Big Stone City, South Dakota bioprocessing facility in May 2026, with the project completed in less than 12 months. In Europe, Rondo Energy and Covestro broke ground in January 2026 on a 100 MWh thermal energy storage system at Covestro's Brunsbuttel chemical site, reinforcing the shift toward behind-the-meter and on-site heat supply contracts that avoid the duration and temperature constraints of electrochemical storage.

A second opportunity track is policy and program-backed demonstrations that reduce technical and commercial risk for emerging storage media and system architectures. The U.S. Department of Energy and the California Energy Commission continue to fund pilot-scale work across particle-based, pressurized-water, and sulfur-based thermal storage approaches, supporting replication of validated designs and integration learnings at industrial facilities. In district heating, RED III-driven renewable-heat increases and national network modernization programs (including the Germanys district heating upgrade funding referenced in the report context) keep seasonal and multi-day TES visible in municipal procurement, even where explicit market recognition of some large-scale TES types remains uneven. These proof points and program structures point to practical demand for standardized modular installation, utility tariff and rate design for thermal storage charging, and industrial retrofits aimed at the 100-300 C band of medium-temperature heat demand highlighted in recent literature for Europe.

Recent Industry Developments in Thermal Energy Storage Market

- May 2026: Antora Energy and POET announced commissioning of a 5 GWh thermal energy storage system at POET's bioprocessing facility in Big Stone City, South Dakota, with the build completed in less than 12 months. The project pairs storage with an enabling electric rate structure, adding a replicable template for industrial sites that need firm, low-carbon heat without relying on long-duration electrochemical storage.

- February 2026: Brenmiller Energy reported completion of electrical works at the Tempo Beverages thermal energy storage project in Israel, enabling full electrification and moving the site toward commissioning activities. The milestone underscores the market's growing emphasis on turnkey integration steps (electrical, controls, and balance-of-plant) that convert TES from equipment supply into operating-asset delivery for industrial heat users.

- November 2025: Nostromo Energy and Olivine announced thermal energy storage participation in wholesale energy markets using Nostromo's IceBrick system, positioning it as a standalone resource rather than only a behind-the-meter HVAC asset. Wholesale market participation broadens monetization paths for building-focused TES by connecting thermal storage to grid services and dispatch signals.

Thermal Energy Storage Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the thermal energy storage market is defined as revenue generated from systems that store heat or cold for later use, including sensible, latent, and thermochemical storage used across power generation and heating and cooling applications.

Scope exclusions: This sizing does not include general electrical battery storage, standalone HVAC equipment without a storage function, or balance-of-plant items that are not part of the storage system sale.

Segments Covered in This Report

-

By Storage Material

- Molten Salt

- Water/Hot-Water

- Ice/Chilled-Water

- Phase-Change Materials (PCM)

- Solid Media (Concrete, Sand, Brick)

- Others

-

By Technology

- Sensible Heat Storage

- Latent Heat Storage

- Thermochemical Heat Storage

-

By Application

- Power Generation (CSP, Grid-integrated)

- District Heating

- Industrial Process Heat

- Building HVAC Cooling

- Other Niche (Peak-shaving, Military, etc.)

-

By End-User

- Utilities

- Commercial and Industrial

- Residential

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

We start with public information that helps set the market boundaries and provides reference points on energy storage deployment, thermal demand, and renewable integration. Sources typically reviewed include the International Energy Agency (IEA), the US Energy Information Administration (EIA), Eurostat, the International Renewable Energy Agency (IRENA), and UN Comtrade trade statistics for relevant equipment flows.

In parallel, we use widely available company annual reports, investor presentations, project announcements, and reputable press to track how applications such as district cooling, industrial heat recovery, and concentrated solar power are funded and built. Select paid subscriptions for company financials and intelligence, patent databases, and an import-export shipment-level database are used to cross-check project timelines, product positioning, and pricing direction. The sources listed here are illustrative, and many other public references were also used to collect data, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Insights from expert interviews and structured surveys are used to pressure-test the model, especially where project economics and adoption rates change quickly across regions. We speak with a mix of developers, EPC-side stakeholders, thermal storage system suppliers, and large end users, then reconcile differences across APAC, EMEA, and the Americas to reduce location bias in assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 17% | APAC: 45% |

| Mid tier: 43% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 18% | Managers: 53% | Americas: 26% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where energy and heat demand indicators, renewable capacity additions, and policy-linked deployment signals are used to reconstruct the addressable demand pool for thermal shifting and peak shaving. Once that demand pool is formed, we corroborate the results using selective bottom-up approximations such as sampled project counts by application, typical storage duration ranges, and ASP x volume checks from supplier and channel discussions, then adjust totals when the two views do not align.

Inputs that commonly matter in this market include new CSP project activity where molten salt storage is paired with generation, district cooling expansions in high cooling-load cities, industrial process-heat decarbonization programs, reported storage duration ranges by application, and observed pricing movement for storage media and system integration. For forecasting, scenario analysis is used so adoption can flex under different policy support and fuel-price conditions, and scenario weights are refined based on expert expectations gathered during interviews. When bottom-up visibility is limited in smaller countries, we use proxy indicators such as build-out rates and installation intensity, then re-check the implied penetration with experts before finalizing.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as project pipelines, regional build-out pace, and the implied mix shift across power generation versus heating and cooling. If an outlier shows up, we review assumptions behind prices, deployment timing, and regional shares, and trigger follow-up calls when the variance cannot be explained with public evidence.

Before sign-off, the work goes through multi-step analyst review so calculation logic, units, and conversions are consistent across regions and years. Reports are refreshed annually, and interim updates are made when material events change the outlook, such as major policy moves or large project awards. Right before delivery, we perform a fresh pass so clients receive the most current view supported by the same repeatable steps.

Mordor Intelligence's Global Thermal Energy Storage Market Market Sizing Compared With Other Published Estimates

Published market sizes for thermal energy storage can differ a lot, even when the topic name looks identical, because each publisher draws the scope line in a slightly different way and then applies different pricing and adoption assumptions. Differences also show up from the chosen base year, exchange-rate timing, and how frequently project pipelines and ASPs are refreshed.

Some estimates fold broader adjacent value, such as non-storage HVAC equipment or wider energy storage categories, which can push the total up or down depending on what is included. In the Mordor Intelligence model, revenue is counted only for thermal storage systems and solutions tied to sensible, latent, and thermochemical storage across power generation and heating and cooling, and general electrical storage and non-storage HVAC are kept out so the demand pool stays traceable to thermal shifting needs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.04 B (2026) | |

| Industry Publisher A | USD 7.09 B (2025) | Uses a different base year and forecast window and provides limited clarity in the public summary on how installed project pipelines and pricing updates are validated year to year, which can shift the starting point. |

| Industry Publisher B | USD 2.51 B (2025) | The published figure appears to reflect a narrower counted revenue pool in practice, likely excluding parts of utility-scale deployments and certain system configurations, and the public overview does not spell out the full inclusion logic. |

The spread in the table mostly comes from what gets counted as storage revenue and how base-year pricing and project timing are treated. By tying the size to clear application demand signals and then checking those totals with supplier-side price and volume reality checks, the final number stays explainable and repeatable for decision making.

Key Questions Answered in the Report

What is the current size of the thermal energy storage market?

The thermal energy storage market size reached USD 8.04 billion in 2026 and is projected to grow to USD 11.87 billion by 2031.

Which segment is expanding fastest within the market?

Phase-change materials are forecast to register a 15.6% CAGR, the highest among storage-material segments.

Why is industrial process heat a major growth driver?

Regulatory mandates for waste-heat recovery and the need for high-temperature decarbonization solutions push process-heat applications to a 14.9% CAGR through 2031.

How do molten-salt systems compare with lithium-ion batteries on cost?

Although molten-salt tanks require higher upfront capex, their cost per stored kilowatt-hour can fall below lithium-ion for discharge durations exceeding 8 hours.

Which region leads the market today, and which is growing fastest?

Europe leads with 34.60% revenue, while Asia-Pacific is the fastest-growing region at a 13.4% CAGR.

What innovations could disrupt future pricing?

Sand-based thermal batteries targeting sub-USD 10 per kWh promise to reshape cost structures and remove lithium supply-chain constraints.

Page last updated on: