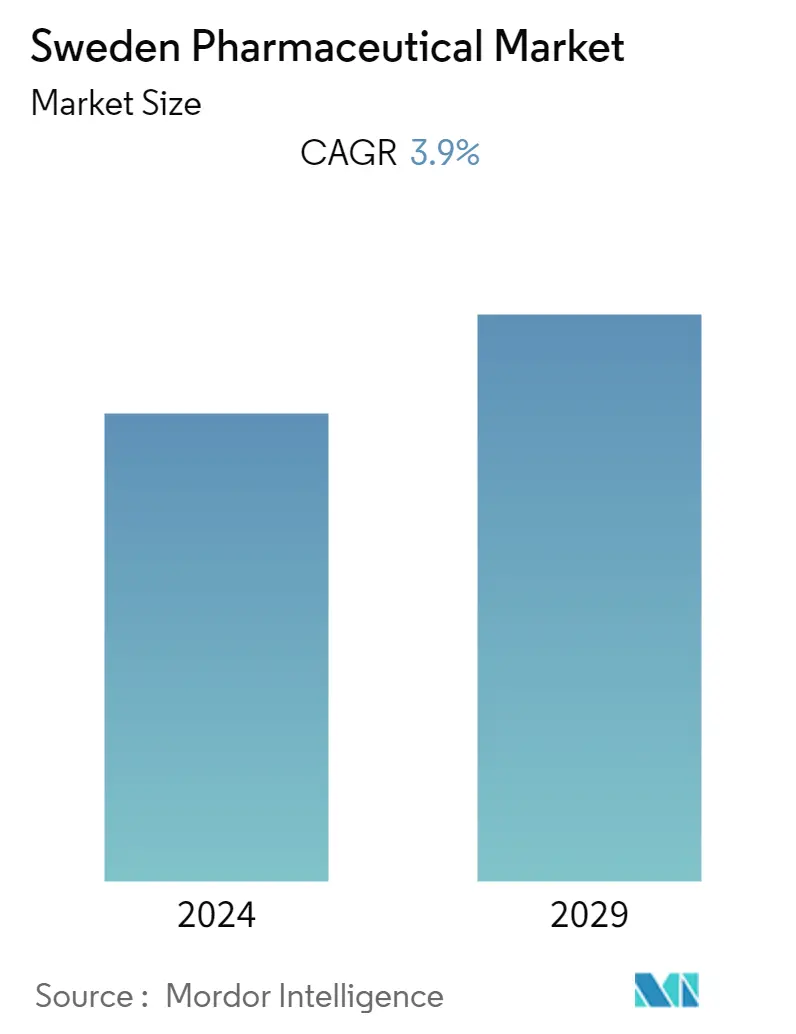

Sweden Pharmaceutical Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | 3.90 % |

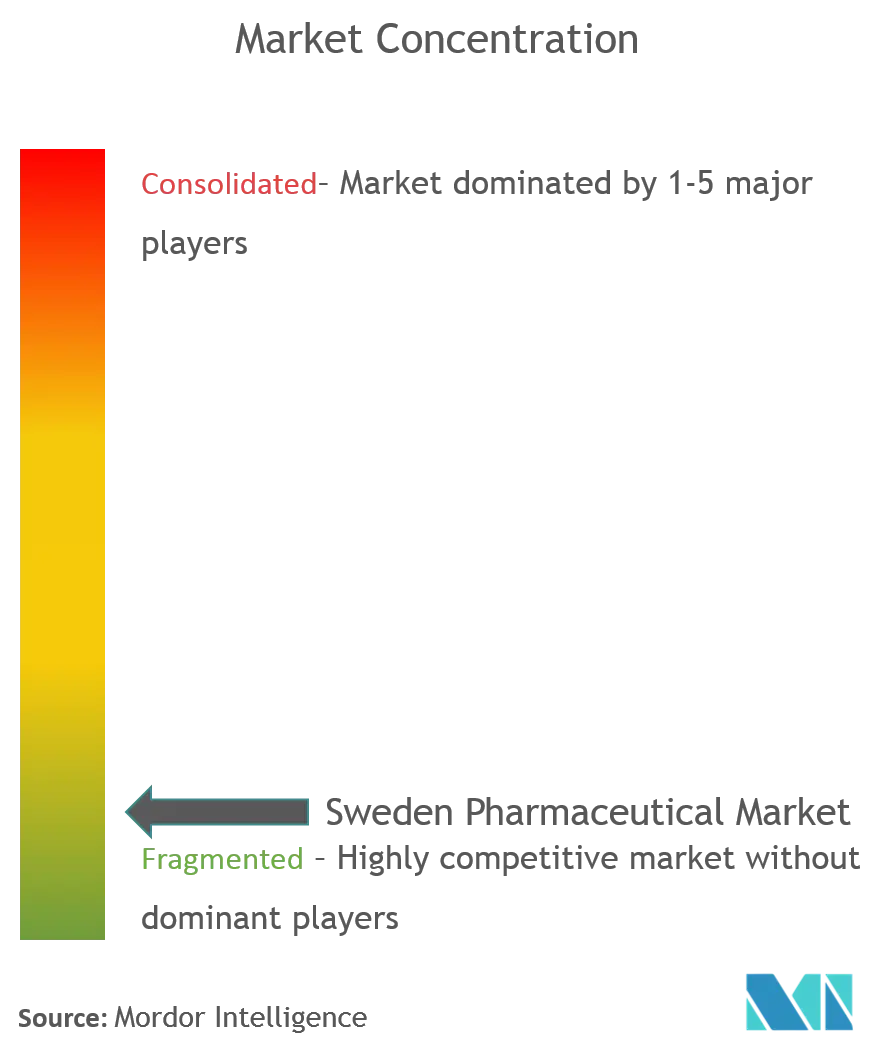

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Sweden Pharmaceutical Market Analysis

The Sweden Pharmaceutical market is anticipated to register a CAGR of 3.9% over the forecast period (2022-2027).

The outbreak of COVID-19 impacted the Sweden pharmaceuticals market in Sweden as healthcare services were significantly reduced due to social distancing measures enforced globally. The Sweden supply chains and the procurement of essential medical supplies are under unheard-of pressure as a result of the COVID-19 pandemic. This includes pharmaceutical products required in the management of various diseases. According to the study titled "Patterns of prescription dispensation and over-the-counter medication sales in Sweden during the COVID-19 pandemic' published in the PLOS ONE Journal in August 2021, following recommendations from public authorities, the weekly volume of defined daily doses (DDDs) quickly decreased; however, the volume of Over the Counter Drug (OTC) sales increased by 96%. particularly in Anatomical Therapeutic Chemical (ATC) therapeutic subgroups for vitamins, antipyretics, painkillers, and remedies for the nose, throat, cough, and cold. However, the onset of the COVID-19 pandemic has also led to an increase in product launches for pharmaceutical drugs, thereby contributing to the market's growth. For instance, in February 2021, the Swedish Medical Products Agency authorized the emergency use of the Bamlanivimab drug in COVID-19 patients with underlying conditions that make them more vulnerable to the virus. As a result of the COVID-19 pandemic, the aforementioned claims that the Swedish pharmaceuticals market experienced significant growth.

Further, the factors contributing to the market's growth are the rising geriatric population and the rising incidence of chronic disease.

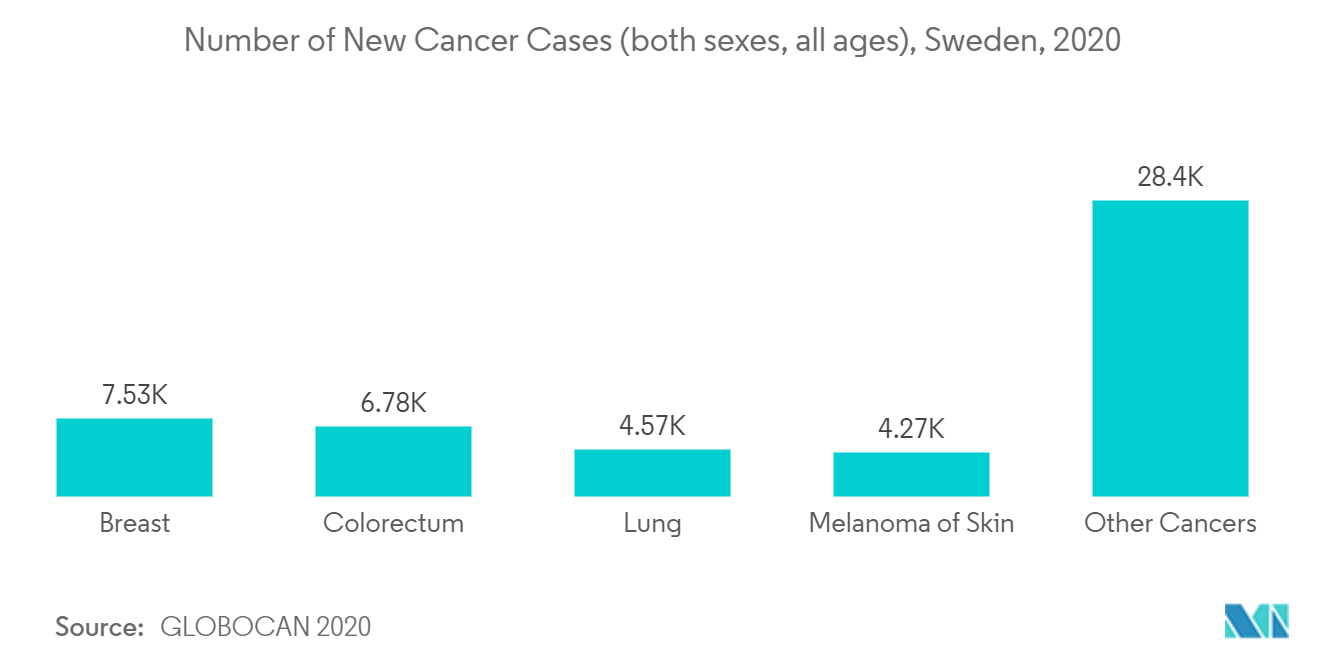

The rising incidence of chronic diseases is a major factor driving the market growth in Sweden. For instance, according to the data published by "socialstyrelsen", the National Board of Health and Welfare in Sweden in December 2021, over 22,200 people experienced an acute heart attacn in 2020, with over 4,800 casualties. A total of 25,400 people experienced strokes, with 6,100 deaths either due to cerebral infarction or brain hemorrhage. Furthermore, the same source stated that approximately 2% to 3% of all babies are born with a birth defect or chromosomal abnormality. Moreover, as per the International Diabetes Federation (IDF) Diabetes Atlas 10th Edition 2021, the estimated number of people with diabetes in 2021 was 496.2 per thousand, and the number is estimated to reach 541.1 per thousand by 2045 in Sweden. Thus, such statistics indicate the high burden of chronic and lifestyle disorders within the country, which will ultimately drive the demand for pharmaceutical drugs in Sweden.

Additionally, as the demand for pharmaceutical drugs is higher in the aging population, the growing geriatric population in Sweden, which is more susceptible to chronic diseases, supports market growth. For instance, according to the World Data Atlas 2021, In Sweden, there were 20.5% of the population over 65 in 2021. The average annual growth rate of the population is 0.74%. Hence, the growing geriatric population in the country is expected to rise the demand for pharmaceutical products thereby boosting the market growth.

Moreover, according to the latest data published in February 2022, by Lif, a trade organization for Swedish research pharmaceutical companies, stated that Sweden exported over SEK 100 billion worth of medications in 2021. Such developments are expected to have a positive impact on the growth of the market over the analysis period. However, growing product launches by the key market players are anticipated to boost the market growth. For Instance, in December 2021, Apellis Pharmaceuticals, Inc. and Swedish Orphan Biovitrum AB reported that the European Commission (EC) has approved Aspaveli (pegcetacoplan), the first and only targeted C3 therapy, for the treatment of adults with paroxysmal nocturnal hemoglobinuria (PNH) who are anemic after treatment with a C5 inhibitor for at least three months. Additionally, in September 2021, Swedish Orphan Biovitrum AB, an international biopharmaceutical company, received an offer from private equity firm Advent International and Singapore's sovereign wealth fund, GIC, to buy out the company for SEK 69.4 billion. In September 2021, Swedish pharmaceutical retailer, Apoteket expanded its partnership with TCS to accelerate its digital transformation and growth.

However, the stringent regulatory scenario is a major factor restraining the growth of the Sweden pharmaceutical market.

Sweden Pharmaceutical Market Trends

This section covers the major market trends shaping the Sweden Pharmaceutical Market according to our research experts:

Prescription Drugs segment Holds the Largest Share and Expected to do Same in the Forecast Period

By prescription type, the prescription drugs segment is expected to garner a larger market share over the forecast period. Some of the key factors driving the growth of the segment include advanced research and development activities, a growing geriatric population, the rising incidence of chronic diseases such as cardiovascular disease and cancer, coupled with new product launches. According to the study titled "Regional variation in the intensity of inhaled asthma medication and oral corticosteroid use in Denmark, Finland, and Sweden" published in European Journal of Respiratory Journal in May 2022, A total of 711,012 people in Sweden have been diagnosed with asthma (prevalence of 8.1% ). More than half (53.6%) of asthma patients in Sweden have poorly controlled asthma, making up about 4.2 percent of those with severe asthma. Thus, the growing prevalence of chronic diseases such as asthma is anticipated to boost the segment growth. Additionally, according to "socialstyrelsen", in 2020, 65% of Sweden's population was prescribed at least one drug. Amongst which, women accounted for 73 percent of the total, including contraception. The most prescribed medications were for high blood pressure, followed by painkillers, antibiotics, allergies, and antidepressants.

Furthermore, several companies are also engaged in product launches, thereby contributing to the segment's growth. For instance, in February 2022, Almirall S.A., a global biopharmaceutical company focused on skin health, announced the European launch of Wynzora cream (50 µg/g calcipotriol and 0.5 mg/g betamethasone as dipropionate), developed a topical treatment for mild to moderate plaque psoriasis in adults, including the scalp. The product is expected to roll out in other European countries during the coming months once national marketing authorizations are granted. The product has received regulatory approval in Sweden. Such developments are likely to have a positive impact on the segment growth.

Moreover, a news article published in January 2022, stated that after a robust 35 percent increase in revenue, Johnson & Johnson topped the Swedish sales list for 2021 with its subsidiary Janssen. Berkeley Vincent, the CEO of Janssen Sweden, detailed that in 2021, Janssen sold pharmaceuticals worth SEK 2.5 billion in Sweden. Thus, the above-mentioned factors are expected to boost the segment's growth over the forecast period.

Sweden Pharmaceutical Industry Overview

The Sweden pharmaceutical market is highly competitive and consists of several major players. In terms of market share, a few of the major players are currently dominating the market. And some prominent players are vigorously making acquisitions and joint ventures with other companies to consolidate their market positions in the country. Some of the key companies that are currently dominating the market are AbbVie Inc., Merck & Co., Inc., Amgen Inc., Pfizer Inc., and GlaxoSmithKline plc.

Sweden Pharmaceutical Market Leaders

Amgen Inc.

Pfizer Inc.

Novartis International AG

Orifarm Group A/S

Merck & Co., Inc.

*Disclaimer: Major Players sorted in no particular order

Sweden Pharmaceutical Market News

- In July 2022, The European Union approved a drug developed by British-Swedish pharmaceutical company AstraZeneca and Japanese Daiichi Sankyo to treat an aggressive form of breast cancer. The drug was approved for the treatment of patients with unresectable or metastatic HER2-positive breast cancer who have received one or more prior anti-HER2-based regimens

- In January 2022, Annexin Pharmaceuticals AB reported that its collaborators at Maastricht University Hospital, Maastricht, the Netherlands, have received approvals from the Dutch regulatory authority and Hospital committees to start a trial with ANXV (a recombinant human Annexin A5) in hospitalized COVID-19 patients.

Sweden Pharmaceutical Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions & Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.1.1 Healthcare Expenditure

4.1.2 Pharmaceutical Imports and Exports

4.1.3 Epidemiology Data For key Diseases

4.1.4 Regulatory Landscape/Regulatory Bodies

4.1.5 Licensing and Market Authorization

4.1.6 Pipeline Analysis

4.1.6.1 By Phase

4.1.6.2 By Sponsor

4.1.6.3 By Disease

4.1.7 Statistical Overview

4.1.7.1 Number of Hospitals

4.1.7.2 Employment in the Pharmaceutical Sector

4.1.7.3 R&D Expenditure

4.1.8 Ease of Doing Business

4.2 Market Drivers

4.2.1 Rising Geriatric Population

4.2.2 Rising Incidence of Chronic Disease

4.3 Market Restraints

4.3.1 Stringent Regulatory Scenario

4.4 Porter's Five Force Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD million)

5.1 By ATC/Therapeutic Class

5.1.1 Digestive orgnas and metabolism

5.1.2 Blood and Blood Forming Organs

5.1.3 Heart and Circulation

5.1.4 Skin Preparation

5.1.5 Urinary and Genital Organs and Sex Hormones

5.1.6 Systemic Hormonal Preparations, Excluding Sex Hormone and Insulin

5.1.7 Antiinfectives For Systemic Use

5.1.8 Tumors and Disorder of Immune System

5.1.9 Musculo-Skeletal System

5.1.10 Nervous System

5.1.11 Antiparasitic Products, Insecticides and Repellents

5.1.12 Respiratory System

5.1.13 Sensory Organs

5.1.14 Others

5.2 By Drug Type

5.2.1 Branded

5.2.2 Generic

5.3 By Prescription Type

5.3.1 Prescription Drugs (Rx)

5.3.2 OTC Drugs

6. COMPETITIVE LANDSCAPE & COMPANY PROFILES

6.1 Company Profile

6.1.1 AbbVie Inc.

6.1.2 Merck & Co., Inc.

6.1.3 Amgen Inc.

6.1.4 Pfizer Inc.

6.1.5 GlaxoSmithKline plc

6.1.6 F. Hoffmann-La Roche AG

6.1.7 AstraZeneca plc

6.1.8 Eli Lilly and Company

6.1.9 Novartis International AG

6.1.10 Sanofi S.A.

6.1.11 Swedish Orphan Biovitrum AB

6.1.12 InDex Pharmaceuticals Holding AB

6.1.13 Medartuum AB

6.1.14 Life Medical Sweden AB

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Sweden Pharmaceutical Industry Segmentation

As per the scope of this report, pharmaceuticals are referred to as prescribed and non-prescription drugs. These medicines can be bought by an individual with or without the doctor's prescription and are safe for consumption for various illnesses with or without the doctor's consent. The market is segmented by ATC/Therapeutic Class (Digestive Organs and Metabolism, Blood and Blood Forming Organs, Heart and Circulation, Skin Preparation, Urinary and Genital Organs and Sex Hormones, Systemic Hormonal Preparations, Excluding Sex Hormone and Insulin, Antiinfectives for Systemic Use, Tumors and Disorders of Immune System, Musculoskeletal System, Nervous System, Antiparasitic Products, Insecticides and Repellents, Respiratory System and Others), Drug Type(Branded and Generic), and Prescription Type(Prescription Drugs(Rx) and OTC Drugs). The report offers the value (in USD million) for the above segments.

| By ATC/Therapeutic Class | |

| Digestive orgnas and metabolism | |

| Blood and Blood Forming Organs | |

| Heart and Circulation | |

| Skin Preparation | |

| Urinary and Genital Organs and Sex Hormones | |

| Systemic Hormonal Preparations, Excluding Sex Hormone and Insulin | |

| Antiinfectives For Systemic Use | |

| Tumors and Disorder of Immune System | |

| Musculo-Skeletal System | |

| Nervous System | |

| Antiparasitic Products, Insecticides and Repellents | |

| Respiratory System | |

| Sensory Organs | |

| Others |

| By Drug Type | |

| Branded | |

| Generic |

| By Prescription Type | |

| Prescription Drugs (Rx) | |

| OTC Drugs |

Sweden Pharmaceutical Market Research FAQs

What is the current Sweden Pharmaceutical Market size?

The Sweden Pharmaceutical Market is projected to register a CAGR of 3.9% during the forecast period (2024-2029)

Who are the key players in Sweden Pharmaceutical Market?

Amgen Inc., Pfizer Inc., Novartis International AG, Orifarm Group A/S and Merck & Co., Inc. are the major companies operating in the Sweden Pharmaceutical Market.

What years does this Sweden Pharmaceutical Market cover?

The report covers the Sweden Pharmaceutical Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Sweden Pharmaceutical Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Sweden Pharmaceutical Industry Report

Statistics for the 2023 Sweden Pharmaceutical market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Sweden Pharmaceutical analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.