Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.86 Billion |

| Market Size (2026) | USD 21.54 Billion |

| Market Size (2031) | USD 99.43 Billion |

| Growth Rate (2026 - 2031) | 35.80% CAGR |

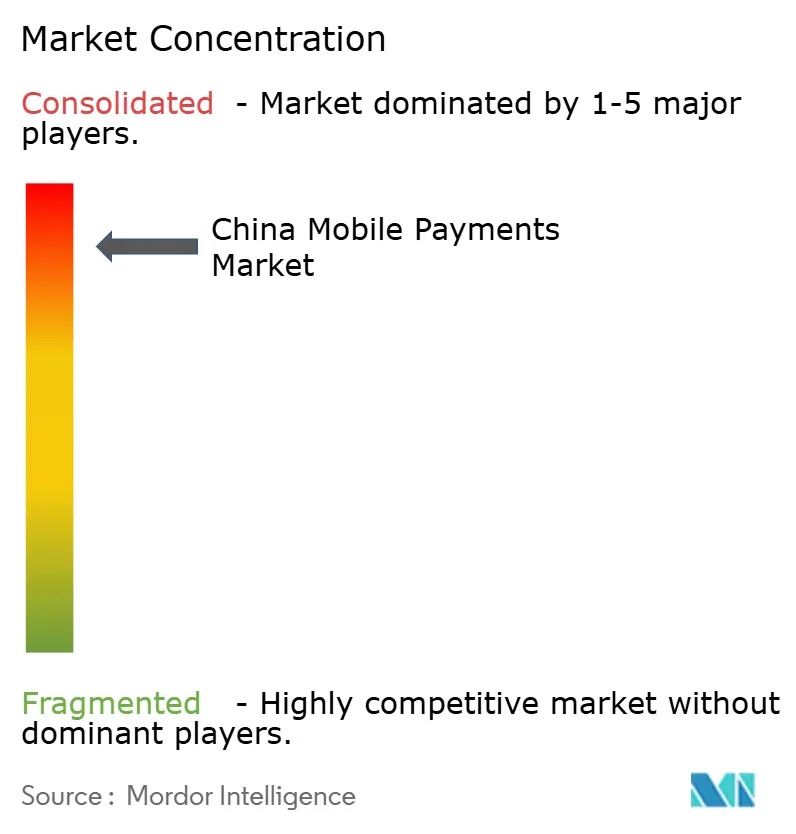

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Mobile Payments Market Analysis by Mordor Intelligence

China mobile payments market size in 2026 is estimated at USD 21.54 billion, growing from 2025 value of USD 15.86 billion with 2031 projections showing USD 99.43 billion, growing at 35.80% CAGR over 2026-2031. The continuous surge reflects the country’s role as a global benchmark for mobile-first commerce, with rising consumer willingness to transact digitally, accelerated merchant onboarding, and a supportive regulatory environment that elevates daily transaction velocity. Expanded spending limits for foreign visitors, unified barcode standards, and ongoing digital-yuan pilots work in tandem to expand addressable volumes and reduce friction for both domestic and inbound users.[1]John Doe, “Foreign Visitors Get Bigger Mobile-Payment Limit in China,” chinabriefing.com Mobile payment leaders leverage entrenched QR ecosystems, super-app engagement loops, and near-universal merchant acceptance to defend their positions, while platform diversification into NFC, BNPL, and cross-border wallets underpins the next growth leg. Regulatory vigilance remains a double-edged sword: data-security and capital-adequacy rules add compliance headwinds, yet they also weed out under-capitalized players, thereby channeling traffic toward sophisticated networks that can turn scale into cost efficiency. The confluence of these structural drivers places the China mobile payments market on a path of rapid monetization, deeper penetration in lower-tier cities, and broader integration across logistics, transit, and B2B supply-chain workflows.

Key Report Takeaways

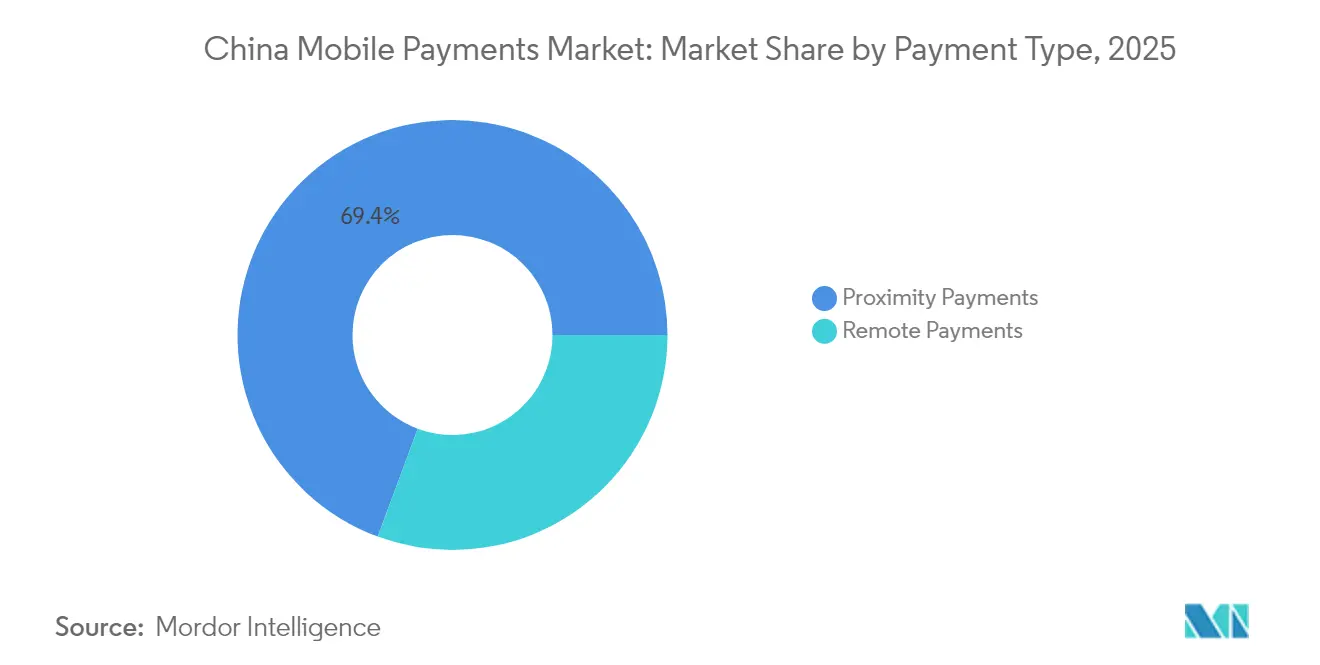

- By payment type, Proximity Payments led with 69.35% revenue share in 2025, while Remote Payments are projected to expand at a 42.60% CAGR through 2031.

- By transaction type, In-store POS controlled 34.60% of the China mobile payments market share in 2025; Person-to-Merchant checkout is forecast to grow 40.90% annually to 2031.

- By application, Retail & eCommerce commanded 37.80% of the China mobile payments market size in 2025, whereas Transportation & Logistics is set to accelerate at a 43.10% CAGR.

- By end-user, Personal users generated 89.60% of 2025 transaction volume, though Business adoption is advancing at a 43.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ubiquity of QR-code Ecosystems & Near-Universal Merchant Acceptance | +8.5% | National, with highest penetration in Tier-1 cities | Short term (≤ 2 years) |

| Government Push for Cashless Society & Digital Yuan Integration | +7.2% | National, with pilot programs in major cities | Medium term (2-4 years) |

| Super-App Lifestyle Ecosystems Boosting Daily Payment Frequency | +6.8% | National, strongest in urban centers | Short term (≤ 2 years) |

| Expansion of NFC/QuickPass Contactless Transit Acceptance | +4.9% | Urban centers, expanding to Tier-2/3 cities | Medium term (2-4 years) |

| BNPL Micro-Credit Features Driving Gen Z Spend Growth | +5.3% | National, concentrated in e-commerce hubs | Short term (≤ 2 years) |

| PBOC Unified Barcode Interoperability Reducing Friction | +3.8% | National implementation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ubiquity of QR-code ecosystems & near-universal merchant acceptance

QR codes enjoy 92.7% penetration, transforming them into the default interface for everything from street-food stalls to luxury boutiques.[2]Jane Smith, “QR Codes Dominate China’s Retail Payments,” thebanker.com Regional interoperability has enabled outbound Chinese travelers to settle purchases across Southeast Asia and Japan, further reinforcing the technology’s utility at home. With foreign-visitor mobile-payment volumes quadrupling in 1H-2024, merchants perceive QR acceptance as essential for retaining foot traffic and eliminating cash-handling costs. The resulting network effect entrenches platform loyalty, raises daily payment frequency, and lifts the average fee pool without an equivalent rise in marketing spend.

Government push for cashless society & digital-yuan integration

The digital yuan processed USD 250 billion by mid-2023, validating state ambitions to embed programmable money within retail payment rails. Salary disbursements in e-CNY across pilot cities showcase new public-sector use cases, though immediate cash conversion by some recipients highlights lingering trust and interest-bearing gaps. By running a parallel state-backed system, the PBOC pressures private wallets to elevate compliance while promoting universal access for the 11.3% unbanked adult cohort.

Super-app lifestyle ecosystems boosting daily payment frequency

WeChat’s 1.4 billion MAUs initiate payments inside messaging, social feeds, and mini programs, allowing a single user to perform multiple low-ticket transactions each day.[3]Rebecca Chen, “New Capital Minimum Hits China FinTechs,” cnbc.com Alibaba mirrors the model by embedding commerce, entertainment, and financial services into Alipay. Because super-apps monetize engagement rather than one-off transactions, they optimize for repeat use, upselling, and data-driven personalization—all of which expand total addressable transaction value.

Expansion of NFC/QuickPass contactless transit acceptance

UnionPay’s QuickPass and Alipay’s “Tap Once” have rolled out to metro gates, buses, and convenience stores in 50+ cities, reducing dwell time and elevating user experience during high-frequency journeys. For operators, contactless throughput trims congestion and labor costs, while users benefit from speed and offline fallback when cellular coverage lags.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Tightening on FinTech Giants Raising Compliance Costs | -4.2% | National, with strongest impact on major platforms | Short term (≤ 2 years) |

| Personal Information Protection Law Heightening Data-Use Limitations | -3.1% | National implementation | Medium term (2-4 years) |

| Merchant Discount Rate (MDR) Caps Compressing PSP Margins | -2.8% | National, affecting all payment service providers | Short term (≤ 2 years) |

| Rural-Elderly Digital Divide Hindering Full Adoption | -1.9% | Rural areas and aging population centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory tightening on FinTech giants raising compliance costs

Minimum registered-capital rules of RMB 1 billion (USD 139 million) triple entry barriers, forcing sub-scale PSPs to exit or merge. Even incumbent leaders have posted volatile quarterly earnings as remediation budgets balloon, diverting resources from product R&D to audit and risk controls.

Personal Information Protection Law heightening data-use limitations

Sweeping data-governance mandates reduce the scope for behavioral profiling and targeted cross-selling, one of the core monetization levers for super-apps. Compliance introduces costly consent management, localization of servers, and mandatory risk assessments, pressing platforms to revamp consent frameworks and anonymization protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Remote Payments Power Cross-Border Scale

Remote Payments unlocked a 42.60% forecast CAGR by leveraging China’s outbound e-commerce surge and the Alipay+ acceptance network connecting 88 million merchants in 57 countries. The segment thrives on friction-free checkout, dynamic FX conversion, and a unified refund process that reduces chargeback risk for merchants. Strategic alignment with tourism recovery allows platforms to monetize spending beyond China’s borders while collecting data to refine loyalty programs.

Proximity Payments retain 69.35% dominance due to QR ubiquity and minimal hardware cost, yet margins tighten as global schemes slash foreign-card fees to 1.5%. Alipay’s NFC push attempts to future-proof the segment, promising sub-second tap speeds that outpace QR scanning in busy transit hubs. Future revenue depends on layering value-added services such as in-app marketing, instant invoice issuance, and loyalty integration inside the China mobile payments market.

By Transaction Type: P2M Checkout Fuels Instant Retail

Person-to-Merchant (P2M) checkout is on course for 40.90% CAGR, energized by group-buy and hyperlocal delivery models that batch orders for last-mile efficiency. The integration of American Express cards into Alipay widens consumer choice, removing a key barrier for high-spend inbound travelers.

In-store POS upholds a 34.60% share, fortified by mature NFC terminals and campus-card systems that cultivate habitual tapping among students. Peer-to-Peer transfers remain foundational inside WeChat groups for bill-splitting and social gifting, while utility-bill and public-sector payments piggyback on digital-yuan rollouts that trim cash-handling overhead for municipal agencies.

By Application: Logistics Leads Acceleration

Transportation & Logistics is projected to grow at 43.10% CAGR as courier marketplaces and ride-hailing fleets embed one-click disbursement and real-time reconciliation. Bank of China’s taxi pilot, using consumer-grade NFC phones as acceptance devices, illustrates how low-cost hardware broadens merchant coverage in metered mobility. Seamless settlement enables dynamic pricing and tip-incentive models, cementing user preference for digital wallets within the China mobile payments market.

Retail & eCommerce still delivers the largest slice at 37.80%, supported by Alibaba’s algorithmic promotions that drive basket-size expansion and repeat purchase frequency. Hospitality adopts “Tap Once” to compress ordering queues, improve table-turnover, and reduce cashier workload. Public-sector applications benefit from payroll digitization, though mass adoption hinges on building citizen trust in state-run wallets.

By End-User: Business Accounts Fast-Track Digitization

Business users clock a 43.40% CAGR as supply-chain platforms issue up to RMB 10 trillion (USD 1.39 trillion) in electronic receivable certificates annually, automating liquidity flows for SMEs. JD.com’s stablecoin prototype for cross-border settlements underscores mounting demand for instant, 24/7 clearing that traditional bank rails cannot match.

Personal users keep a 89.60% volume share thanks to lifestyle integration, yet incremental growth shifts from new adopters to higher ticket sizes and subscription renewals. Rural uptake, now at 904 million users, extends inclusion benefits such as lower remittance costs and access to micro-insurance, mitigating income shocks for low-asset households. The dual-segment dynamic positions super-apps to cross-pollinate consumer and enterprise services inside the China mobile payments market, fostering stickier ecosystems.

Geography Analysis

Adoption peaks in Tier-1 corridors where smartphone penetration, 5G coverage, and merchant digitalization converge. Beijing’s campus NFC success demonstrates how dense populations accelerate proof-of-concept scale-up before nationwide rollouts. Shenzhen pilots, from taxi NFC to digital-yuan payroll, exploit municipal agility to pressure-test next-gen standards. Cross-border enclaves—especially Hong Kong—act as gateways for overseas wallets, with Alipay+ enabling 14 e-wallets to transact locally and catalyzing tourist spending rebounds.

In lower-tier cities, QuickPass subsidies and simplified KYC workflows extend acceptance among micro-merchants, aligning with state goals to narrow the rural-urban payment gap. Rural residents enjoy tangible welfare benefits as digital payments cut travel time to bank branches and unlock credit scoring for agri-input loans. The government balances inclusion with autonomy by mandating cash acceptance for the elderly and ensuring free SMS payment prompts for feature-phone users.

Internationally, Chinese wallets export QR standards to ASEAN markets, allowing inbound tourists to pay in-app while the merchant settles in local currency. This strategy deepens platform moats, captures FX spreads, and reinforces the China mobile payments market’s influence over regional standards. Future territory gains will hinge on bilateral agreements to recognize Chinese e-signatures and KYC protocols, streamlining compliance for merchants abroad.

Competitive Landscape

Alipay and WeChat Pay dominate with a combined 90% grip, forming an oligopoly that translates network scale into bargaining power with merchants and regulators. To diversify revenue, Ant Group split Alipay into Digital Payment and Alipay Business units, aiming to commercialize traffic via merchant services, local-life commerce, and wealth-management cross-sell. Tencent counteracts by embedding retailer mini-programs and ad engines inside WeChat to boost marketing-services income by 20% YoY.

New entrants gravitate toward niche verticals—cross-border P2M, SME financing, and wearable payments—where differentiation pivots on specialized APIs and hardware innovation. UnionPay’s transparent NFC-antenna patent for wrist devices signals a hardware-software convergence race. Foreign networks are gaining a toehold: American Express now clears on-shore RMB and links cards to Alipay wallets, while Visa and Mastercard’s fee cuts aim to recapture tourist spend lost to QR dominance.

Regulation remains the primary strategic variable. Capital thresholds eliminate under-capitalized PSPs but also raise the cost of innovation. Leaders with diversified income streams and compliance infrastructure can absorb audit overheads and recycle capital into R&D, giving them endurance over single-product challengers. The resulting market topology is concentrated yet dynamic, favoring incumbents that integrate new rails—NFC, e-CNY, BNPL—without cannibalizing core QR volumes inside the China mobile payments market.

China Mobile Payments Industry Leaders

Paypal Inc.

Alipay (Ant Group Co., Ltd.)

99Bill Corporation

Huawei Technologies Co., Ltd. (Huawei Pay)

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: American Express partnered with Alipay to let global card members link their cards to the Alipay wallet, broadening inbound card acceptance and capturing higher-yield cross-border volumes. The move extends AmEx’s on-shore RMB clearing license and positions the network to tap China’s tourism rebound while Alipay gains premium-cardholder traffic.

- December 2024: Ant Group restructured Alipay into Digital Payment and Alipay Business units to sharpen product focus and monetize ecosystem traffic beyond payment fees. The revamp signals a pivot toward merchant SaaS, credit-tech, and local-services marketing in response to tighter margin caps.

- December 2024: UnionPay International enabled cross-scan functionality whereby eight overseas wallets can scan Weixin Pay QR codes, accelerating interoperability and enlarging acceptance for inbound visitors. Strategic intent centers on capturing FX spreads and reinforcing UnionPay rails against global card networks.

- November 2024: UnionPay allowed foreign-issued UnionPay cards to link with Alipay and WeChat, enhancing visitor convenience and positioning UnionPay as the go-to bridge between global plastic and China’s wallet ecosystems.

China Mobile Payments Market Report Scope

Mobile payments refer to the transactions that are taking place under the purview of various regulatory bodies using mobile devices as part of initiatives to digitize payments across the globe. Mobile device payments act as alternatives to cash, cheques, or physical credit cards.

The scope of the report includes proximity and remote payments that are done through mobile devices. The study considers the impact of COVID-19 on the market.

By Payment Type

| Proximity Payments |

| Remote Payments |

By Transaction Type

| Peer-to-Peer (P2P) |

| In-store Point-of-Sale (POS) |

| Person-to-Merchant (P2M/Checkout) |

| Other Transaction Types |

By Application

| Retail and eCommerce |

| Transportation and Logistics |

| Hospitality and Food-Service |

| Government and Public Sector |

| Other Applications (Education, Healthcare) |

By End-user

| Personal |

| Business |

| By Payment Type | Proximity Payments |

| Remote Payments | |

| By Transaction Type | Peer-to-Peer (P2P) |

| In-store Point-of-Sale (POS) | |

| Person-to-Merchant (P2M/Checkout) | |

| Other Transaction Types | |

| By Application | Retail and eCommerce |

| Transportation and Logistics | |

| Hospitality and Food-Service | |

| Government and Public Sector | |

| Other Applications (Education, Healthcare) | |

| By End-user | Personal |

| Business |

Key Questions Answered in the Report

What is the current size of the China mobile payments market?

The market is valued at USD 21.54 billion in 2026 and is projected to hit USD 99.43 billion by 2031.

Which payment type is growing fastest?

Remote Payments lead with a forecast CAGR of 42.60% as Chinese wallets expand across borders.

How dominant are Alipay and WeChat Pay?

Together they control more than 90% of total transaction volume, signaling high market concentration.

Why is the Transportation & Logistics segment important?

It forecasts a 43.10% CAGR, driven by ride-hailing, delivery platforms, and NFC transit adoption.

What role does the digital yuan play?

The e-CNY processed USD 250 billion by mid-2023, offering state-backed alternatives and fostering financial inclusion.

How are regulators impacting the market?

Capital-adequacy rules and data-protection laws raise compliance costs, benefiting well-capitalized incumbents while trimming fringe operators.

Page last updated on: