Pectin Market Size

| Study Period | 2019 - 2029 |

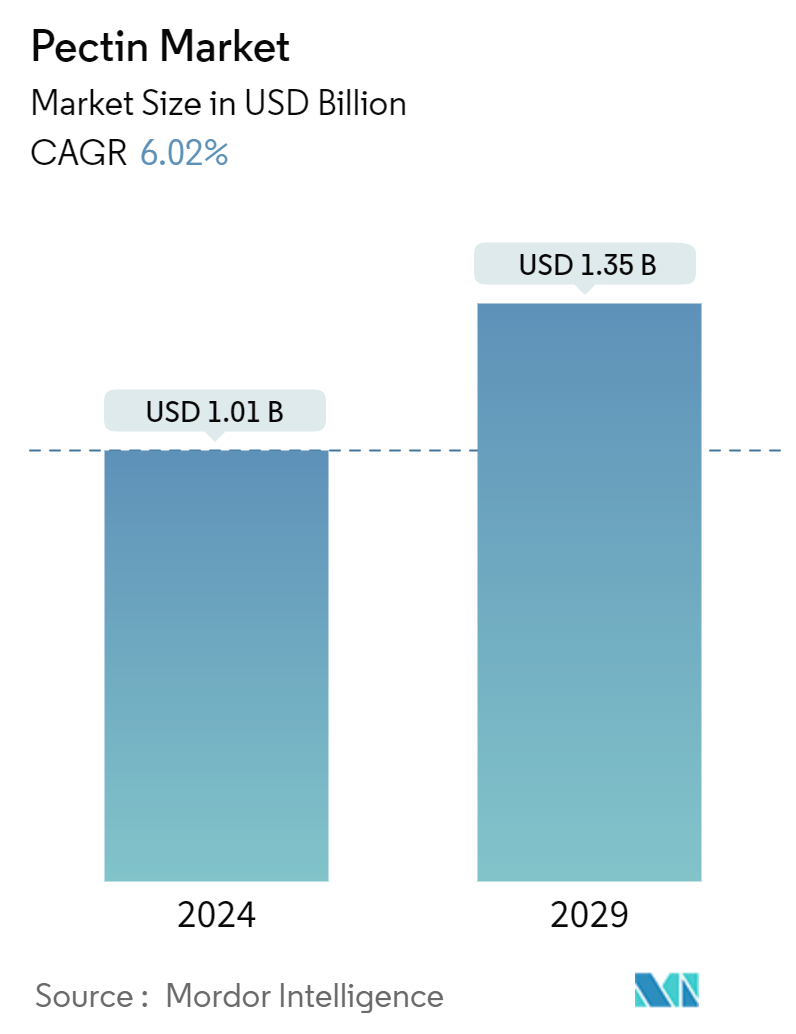

| Market Size (2024) | USD 1.01 Billion |

| Market Size (2029) | USD 1.35 Billion |

| CAGR (2024 - 2029) | 6.02 % |

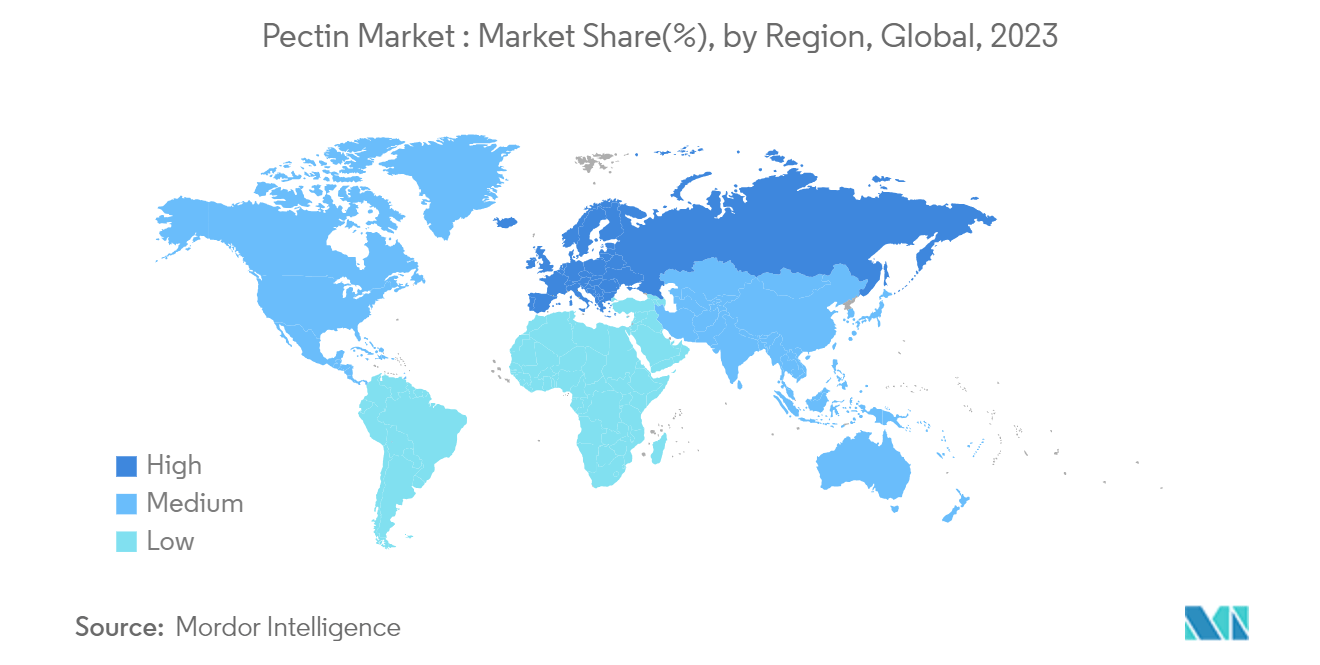

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Pectin Market Analysis

The Pectin Market size is estimated at USD 1.01 billion in 2024, and is expected to reach USD 1.35 billion by 2029, growing at a CAGR of 6.02% during the forecast period (2024-2029).

Diverse applications in industries such as pharmaceutical, cosmetics, and food and beverage have contributed to the growth of the market studied. Jams, jellies, and marmalade are the major application areas of pectin. Also, with technological advancement, players in the market have been developing pectin suitable for various applications. For instance, GENU Pectin, by CP Kelco, has been gaining ground in the personal care and beauty market as a nature-based skin feel aid, stabilizer, and pH-balancing ingredient. In line with this, with a growing number of diet-conscious consumers seeking alternatives to reduce fats and calories, pectin is gaining prominence as a healthy replacement in such products.

Additionally, the increased usage of pectin in fruit juices for improved mouthfeel, in acidified dairy applications for protein stabilization, in low-calorie jams, and in acidified protein drinks has been supporting the growth of the market for the last few years. The increasing awareness about the multifunctionality of pectin among food and beverage manufacturers, such as its reduced cooking time, improved texture and color, and increased shelf life, are among the factors that have been fueling the pectin market. Moreover, extensive research and development investments in the market under study have also contributed to market growth.

Pectin Market Trends

Demand for Natural and Clean Label Ingredients

Pectin is a hydrocolloid type sourced from natural fruits and vegetables. Many consumers lean toward plant-based ingredients such as fruit-based pectin instead of animal-based gelatin and prefer clean flavors. Pectin manufacturers are taking initiatives to offer clean-label ingredients for processed food manufacturers. Clean-label ingredients are gaining popularity among consumers globally as they are perceived to be beneficial for health and better for the planet. Consumers prioritize products containing natural, recognizable, simple, and less processed ingredients.

Moreover, consumers are becoming increasingly aware of the harmful effects of artificial ingredients and processed and unnatural food products, thus enabling food and beverage manufacturers to opt for cleaner, organic, and more natural ingredients and provide transparency about the food ingredients. Furthermore, consumers associate clean-label food products with simple, easy-to-recognize, healthy, and free from preservatives and artificial additives. Thus, there is an increasing demand for natural preservatives like pectin as thickeners, gelling agents, texturizers, and stabilizers to improve the shelf-life of food products and preserve them during heating.

Thus, surging demand for clean labeled ingredients and natural food additives like pectin among food and beverage manufacturers and regulations from various governmental bodies favoring the use of natural additives in food products propels the market growth in the studied period.

Europe Holds the Major Share in Pectin Market

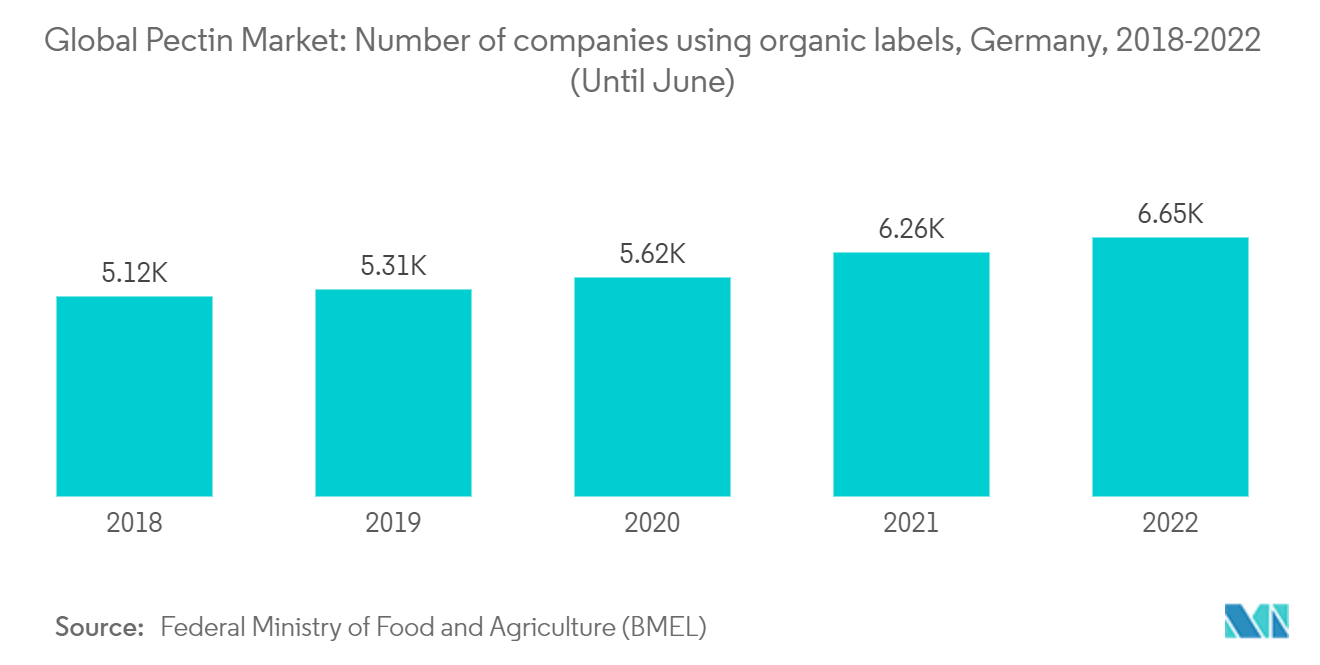

Europe holds the largest market share in the pectin market, followed by North America. The demand in the region is high owing to the presence and growth of end-use applications for the product. Pectin has been used for various purposes, including thickeners, stabilizers, film and gel formers, and, generally, to maintain or improve food quality. The increasing application area of hydrocolloids, such as managing watery foods' thickening and gelling qualities, is driving the market growth. The growing vegan population is also shaping the market. Customers are reducing meat consumption and looking for naturally derived or vegan options, which may help pectin market growth. For instance, according to The Smart Project (a European Commission-funded collaboration between ProVeg, the Good Food Institute, and 31 partner organizations from 21 different countries), the sales value of plant-based food in Spain was EUR 447.4 million in 2022. This indicates that consumer inclination toward plant-based ingredients might shape the market growth of pectin in the region since it is derived from plant cell walls.

Pectin Industry Overview

The global pectin market is competitive, with international players dominating the market studied. Some key players in the market include International Flavors & Fragrances, Inc., Cargill Incorporated, Herbstreith Fox Corporate Group, JM Huber Corporation, and Royal DSM. The prominent players have been focusing on developing new and innovative products by targeting new formulations specific to an application. Additionally, these companies are focusing on increasing the production capacities of their existing plants while investing in R&D activities. Thus, the market studied is expected to witness numerous product launches during the forecast period.

Pectin Market Leaders

Cargill Incorporated

Royal DSM

Herbstreith and Fox Corporate Group

International Flavors & Fragrances

JM Huber Corporation

*Disclaimer: Major Players sorted in no particular order

Pectin Market News

- January 2024: IFF launched Grindsted Pectin FB 420 for baking applications. It is ideal for baking applications, has unique sensory qualities for bake-stable fruit fillings, and is label-friendly and process-efficient.

- December 2023: Herbstreith & Fox GmbH & Co. KG launched a new subsidiary, H&F Italy SRL, in Milan, Italy. The new subsidiary represents the H&F Group's interests in the Italian market.

- September 2023: Cargill introduced a line of LM conventional (LMC) pectins that provide a novel texture for fruit-filled food items with "organic" or "conventional" labels. Pectin, a soluble fiber derived from fruits, is used in low-sugar fruit jam and bakery fruit filling. The Unipectine LMCplus range offers a higher gel strength and spreadability than standard LMCs.

Pectin Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Drivers

4.1.1 Demand for Natural and Clean-label Ingredients

4.1.2 Rising Consumption of Packaged Food Products

4.2 Market Restraints

4.2.1 Availability of Economically Feasible Alternatives

4.3 Porter's Five Force Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 By Source

5.1.1 Citrus Fruits

5.1.2 Sugar Beet

5.1.3 Apple

5.1.4 Other Sources

5.2 By Application

5.2.1 Beauty and Personal Care

5.2.2 Food and Beverage

5.2.2.1 Jam, Jelly, and Preserve

5.2.2.2 Baked Goods

5.2.2.3 Dairy Products

5.2.2.4 Other Foods and Beverages

5.2.3 Pharmaceuticals

5.2.4 Other Applications

5.2.4.1 Edible Films and Coatings

5.2.4.2 Paper Substitutes

5.2.4.3 Foams and Plasticizers

5.3 By Type

5.3.1 High Methoxyl Pectin

5.3.2 Low Methoxyl Pectin

5.4 Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Mexico

5.4.1.4 Rest of North America

5.4.2 Europe

5.4.2.1 United Kingdom

5.4.2.2 Germany

5.4.2.3 France

5.4.2.4 Russia

5.4.2.5 Italy

5.4.2.6 Spain

5.4.2.7 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 India

5.4.3.2 China

5.4.3.3 Japan

5.4.3.4 Australia

5.4.3.5 Rest of Asia-Pacific

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of South America

5.4.5 Middle East & Africa

5.4.5.1 South Africa

5.4.5.2 Saudi Arabia

5.4.5.3 Rest of Middle East & Africa

6. COMPETITIVE LANDSCAPE

6.1 Most Adopted Strategies

6.2 Market Share Analysis

6.3 Company Profiles

6.3.1 International Flavors & Fragrances

6.3.2 JM Huber Corporation (CP Kelco)

6.3.3 Cargill Incorported

6.3.4 Herbstreith and Fox Corporate Group

6.3.5 Silvateam SpA

6.3.6 Royal DSM

6.3.7 Foodchem International Corporation

6.3.8 Ingredion Incorporated

6.3.9 Lucid Colloids Ltd

6.3.10 Pacific Pectin Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Pectin Industry Segmentation

Pectin is a structural acidic heteropolysaccharide found in the primary and middle lamellae and cell walls of terrestrial plants. It is made from real fruit, and its forms, from dry pectin to liquid pectin to mass-produced commercial pectin, are sourced entirely from plants.

The market studied is segmented by source, application, type, and geography. By source, the market studied is segmented into citrus fruits, sugar beet, apple, and other sources. By application, the market studied is segmented into beauty and personal care, food and beverages, pharmaceuticals, and other applications. The food and beverages segment is further classified into jam, jelly, and preserves, baked goods, dairy products, and other food and beverages. The other applications segment is further classified into edible films and coatings, paper substitutes, and foams and plasticizers. By type, the market studied is segmented into high methoxyl pectin and low methoxyl pectin. Based on geography, the market studied is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

For each segment, the market sizing and forecasting have been done in value terms USD.

| By Source | |

| Citrus Fruits | |

| Sugar Beet | |

| Apple | |

| Other Sources |

| By Application | ||||||

| Beauty and Personal Care | ||||||

| ||||||

| Pharmaceuticals | ||||||

|

| By Type | |

| High Methoxyl Pectin | |

| Low Methoxyl Pectin |

| Geography | |||||||||

| |||||||||

| |||||||||

| |||||||||

| |||||||||

|

Pectin Market Research FAQs

How big is the Pectin Market?

The Pectin Market size is expected to reach USD 1.01 billion in 2024 and grow at a CAGR of 6.02% to reach USD 1.35 billion by 2029.

What is the current Pectin Market size?

In 2024, the Pectin Market size is expected to reach USD 1.01 billion.

Who are the key players in Pectin Market?

Cargill Incorporated, Royal DSM, Herbstreith and Fox Corporate Group, International Flavors & Fragrances and JM Huber Corporation are the major companies operating in the Pectin Market.

Which is the fastest growing region in Pectin Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Pectin Market?

In 2024, the Europe accounts for the largest market share in Pectin Market.

What years does this Pectin Market cover, and what was the market size in 2023?

In 2023, the Pectin Market size was estimated at USD 0.95 billion. The report covers the Pectin Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Pectin Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Pectin Industry Report

Statistics for the 2024 Pectin market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Pectin analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.